Walbridge PESTLE Analysis

Your Shortcut to Market Insight Starts Here

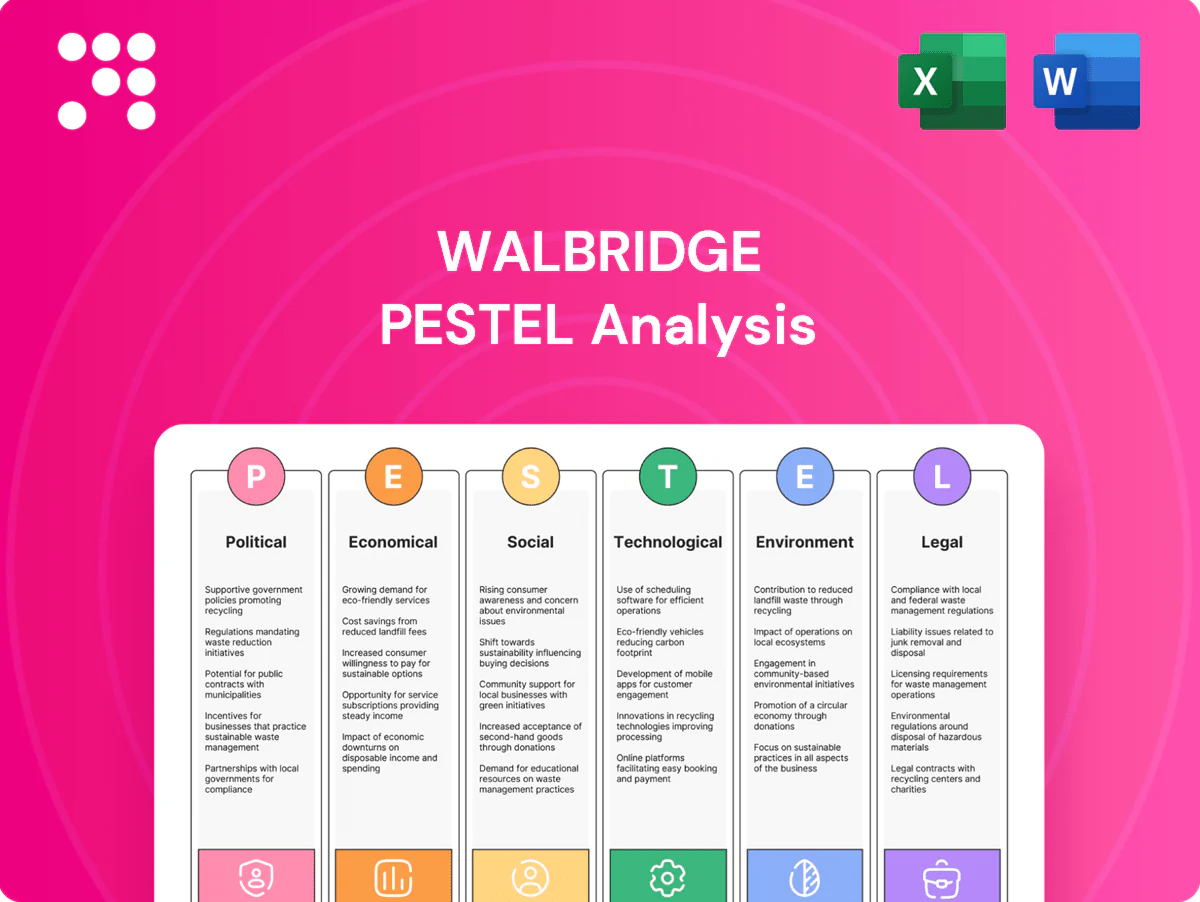

Gain a strategic edge with our focused PESTLE Analysis of Walbridge, revealing the political, economic, social, technological, legal, and environmental forces shaping its future. Use these concise insights to spot risks and growth opportunities fast. Purchase the full analysis now for the complete, actionable report ready for immediate use.

Political factors

Federal infrastructure spending

Federal infrastructure funding cycles, anchored by the Bipartisan Infrastructure Law with roughly $550 billion in new investments including about $110 billion for roads and bridges and $55 billion for water, drive multi-year project pipelines. Bipartisan programs stabilize backlog and enable long-duration award structures, while shifts in appropriations or continuing resolutions routinely delay starts and strain cash flow. Walbridge’s national scale positions it to pursue federally-backed megaprojects funded through these programs.

Industrial policy incentives

IRA's roughly $369 billion in clean-energy incentives, the CHIPS Act's ~280 billion authorization including about $52.7 billion for semiconductor incentives, and targeted advanced-manufacturing credits are catalyzing factories, battery plants and power projects. Incentive clarity affects client site selection and project timelines, while domestic-content and critical-mineral rules determine sourcing and self-perform strategies. Walbridge can align delivery models and trades integration to help clients meet compliance thresholds and capture credits.

Trade and tariff dynamics

Tariffs on steel (25%) and aluminum (10%) and levies on equipment directly inflate bid prices and trigger escalation clauses. Geopolitical shifts since 2022 have disrupted global supply chains for specialized components, raising procurement volatility. Early procurement and alternate sourcing reduce exposure and schedule risk. Clients increasingly demand transparent tariff pass-throughs and cost breakdowns from contractors.

Labor and union relations

Project labor agreements and prevailing wage rules materially shape project cost structures; EO 14063 (2021) encourages PLA use on federal projects over $35 million and the Davis-Bacon Act applies prevailing wages on federal contracts above $2,000. Political support for organized labor can expand PLA adoption, while collaborative labor strategies help ensure craft availability across regions and Walbridge’s self-perform model benefits from stable labor frameworks.

- EO 14063 — PLA encouragement on federal projects >35,000,000

- Davis-Bacon — prevailing wages on federal contracts >2,000

- PLAs increase cost predictability

- Walbridge self-perform reduces subcontract exposure

Energy and permitting policy

Transmission, generation mix, and grid modernization priorities drive power-sector demand; the Inflation Reduction Act provided about 369 billion for energy and climate and the Bipartisan Infrastructure Law dedicated 7.5 billion for EV charging, boosting project pipelines.

Streamlined federal and state permitting reduces schedule risk on complex sites; policy support—including roughly 6 billion in Civil Nuclear Credit and expanded renewables tax credits—creates new build categories Walbridge can target.

- Transmission investment: higher grid upgrade demand

- Permitting: lower schedule risk

- Support: nuclear, renewables, EV charging

- Positioning: target policy tailwinds

BIL, IRA and CHIPS spur megaproject pipelines; tariffs, labor rules and scale raise bid volatility

Federal infrastructure funding (BIL ~$550B), IRA ($369B) and CHIPS ($280B) create multi-year pipelines; tariffs (steel 25%, aluminum 10%) and supply-chain shifts raise bid volatility. Labor rules (EO 14063 >35,000,000; Davis-Bacon >2,000) inflate costs; Walbridge scale and self-perform reduce subcontract exposure and capture federally backed megaprojects.

| Metric | Value |

|---|---|

| BIL | $550B |

| IRA | $369B |

| CHIPS | $280B |

| Steel tariff | 25% |

What is included in the product

Explores how external macro-environmental factors uniquely affect Walbridge across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with each category expanded into detailed, business-specific sub-points and forward-looking insights. Backed by current data and market/regulatory dynamics, it’s formatted for direct use in business plans, pitch decks, and executive decision-making.

The Walbridge PESTLE Analysis delivers a concise, visually segmented summary of external factors that’s easily editable and shareable, enabling quick alignment across teams and streamlined use in presentations or planning sessions.

Economic factors

Interest rate environment

Higher policy rates—federal funds near 5.25–5.50% and 10-year Treasury around 4.0–4.5% in mid-2025—raise private developers’ hurdle rates and push out notices to proceed. Public owners often sustain planned spend while private manufacturing projects stagger starts. Design-build with guaranteed pricing gains appeal in this volatile rate regime. Walbridge’s strong balance sheet and bonding capacity enable competitive terms.

Materials cost volatility

Volatility in steel (spot swings ~25% YoY in 2023–24), concrete and electrical gear prices plus switchgear lead times often stretching 20–28 weeks materially complicate bid assumptions and contingency sizing. Index-linked contracts and escalation clauses have become standard to protect margins amid ~6% construction materials inflation in 2023. Early lock-ins and strategic supplier alliances cut exposure to spot moves, while Walbridge’s procurement scale yields allocation priority and negotiated price discounts.

Skilled labor supply

Trade shortages push up labor costs and raise productivity expectations; 80% of contractors reported difficulty hiring skilled craft workers in AGC’s 2024 survey. Robust training pipelines and apprenticeship partnerships are vital to delivery certainty and reduce turnover. Walbridge’s self-perform capabilities give schedule control and quality advantages. Guaranteeing dedicated crews lets Walbridge capture premium, time-sensitive work.

Manufacturing and auto cycles

Global EV sales were roughly 14 million units in 2024, driving strong OEM capex and supplier EV programs that feed Walbridge’s core backlog; cycle turns dictate plant upgrades, retooling and greenfield builds as OEMs phase new EV lines. Diversification into power and industrial reduces exposure to auto cyclicality, while Walbridge’s track record in complex process facilities differentiates it on large retrofit and greenfield work.

- OEM capex & supplier programs: primary backlog driver

- Cycle turns: trigger upgrades, retooling, greenfields

- Diversification: power/industrial cushions automotive swings

- Competitive edge: experience in complex process facilities

Client capital allocation

Client capital allocation favors reshoring and resilience, driving U.S. facility growth as manufacturing represents roughly 11% of GDP; inventory and dual-sourcing strategies increase demand for fast-build plants. CFOs prioritizing total cost of ownership lift demand for lifecycle and speed-to-market solutions, while off-balance-sheet and P3 structures can unlock constrained credit. Walbridge can win by packaging EPC, fast-track delivery, and cost-certainty guarantees.

- Reshoring-driven facility expansion

- CFO TCO focus → lifecycle solutions

- P3/off-balance-sheet unlocks projects

- Walbridge: EPC + fast-track + cost certainty

BIL, IRA and CHIPS spur megaproject pipelines; tariffs, labor rules and scale raise bid volatility

Higher rates (FF 5.25–5.50%, 10y 4.0–4.5% mid‑2025) raise hurdle rates and favor fixed‑price DB work; materials inflation (~6% in 2023) and steel spot swings ~25% YoY squeeze margins; skilled labor shortages (AGC: ~80% reporting 2024) elevate labor costs; EV demand (~14M sales in 2024) sustains OEM capex and backlog.

| Metric | Value | Impact |

|---|---|---|

| Fed funds | 5.25–5.50% | Higher hurdle rates |

| 10y | 4.0–4.5% | Capex cost |

| Materials inflation | ~6% | Margin pressure |

| EV sales | ~14M (2024) | Backlog driver |

What You See Is What You Get

Walbridge PESTLE Analysis

The Walbridge PESTLE analysis shown here is the actual document you’ll receive after purchase—fully formatted, professionally structured, and ready to use. The preview reflects the final content, layout, and structure with no placeholders or omissions. After checkout you’ll instantly download this exact file and can apply the insights immediately.

Your Shortcut to Market Insight Starts Here

Gain a strategic edge with our focused PESTLE Analysis of Walbridge, revealing the political, economic, social, technological, legal, and environmental forces shaping its future. Use these concise insights to spot risks and growth opportunities fast. Purchase the full analysis now for the complete, actionable report ready for immediate use.

Political factors

Federal infrastructure spending

Federal infrastructure funding cycles, anchored by the Bipartisan Infrastructure Law with roughly $550 billion in new investments including about $110 billion for roads and bridges and $55 billion for water, drive multi-year project pipelines. Bipartisan programs stabilize backlog and enable long-duration award structures, while shifts in appropriations or continuing resolutions routinely delay starts and strain cash flow. Walbridge’s national scale positions it to pursue federally-backed megaprojects funded through these programs.

Industrial policy incentives

IRA's roughly $369 billion in clean-energy incentives, the CHIPS Act's ~280 billion authorization including about $52.7 billion for semiconductor incentives, and targeted advanced-manufacturing credits are catalyzing factories, battery plants and power projects. Incentive clarity affects client site selection and project timelines, while domestic-content and critical-mineral rules determine sourcing and self-perform strategies. Walbridge can align delivery models and trades integration to help clients meet compliance thresholds and capture credits.

Trade and tariff dynamics

Tariffs on steel (25%) and aluminum (10%) and levies on equipment directly inflate bid prices and trigger escalation clauses. Geopolitical shifts since 2022 have disrupted global supply chains for specialized components, raising procurement volatility. Early procurement and alternate sourcing reduce exposure and schedule risk. Clients increasingly demand transparent tariff pass-throughs and cost breakdowns from contractors.

Labor and union relations

Project labor agreements and prevailing wage rules materially shape project cost structures; EO 14063 (2021) encourages PLA use on federal projects over $35 million and the Davis-Bacon Act applies prevailing wages on federal contracts above $2,000. Political support for organized labor can expand PLA adoption, while collaborative labor strategies help ensure craft availability across regions and Walbridge’s self-perform model benefits from stable labor frameworks.

- EO 14063 — PLA encouragement on federal projects >35,000,000

- Davis-Bacon — prevailing wages on federal contracts >2,000

- PLAs increase cost predictability

- Walbridge self-perform reduces subcontract exposure

Energy and permitting policy

Transmission, generation mix, and grid modernization priorities drive power-sector demand; the Inflation Reduction Act provided about 369 billion for energy and climate and the Bipartisan Infrastructure Law dedicated 7.5 billion for EV charging, boosting project pipelines.

Streamlined federal and state permitting reduces schedule risk on complex sites; policy support—including roughly 6 billion in Civil Nuclear Credit and expanded renewables tax credits—creates new build categories Walbridge can target.

- Transmission investment: higher grid upgrade demand

- Permitting: lower schedule risk

- Support: nuclear, renewables, EV charging

- Positioning: target policy tailwinds

BIL, IRA and CHIPS spur megaproject pipelines; tariffs, labor rules and scale raise bid volatility

Federal infrastructure funding (BIL ~$550B), IRA ($369B) and CHIPS ($280B) create multi-year pipelines; tariffs (steel 25%, aluminum 10%) and supply-chain shifts raise bid volatility. Labor rules (EO 14063 >35,000,000; Davis-Bacon >2,000) inflate costs; Walbridge scale and self-perform reduce subcontract exposure and capture federally backed megaprojects.

| Metric | Value |

|---|---|

| BIL | $550B |

| IRA | $369B |

| CHIPS | $280B |

| Steel tariff | 25% |

What is included in the product

Explores how external macro-environmental factors uniquely affect Walbridge across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with each category expanded into detailed, business-specific sub-points and forward-looking insights. Backed by current data and market/regulatory dynamics, it’s formatted for direct use in business plans, pitch decks, and executive decision-making.

The Walbridge PESTLE Analysis delivers a concise, visually segmented summary of external factors that’s easily editable and shareable, enabling quick alignment across teams and streamlined use in presentations or planning sessions.

Economic factors

Interest rate environment

Higher policy rates—federal funds near 5.25–5.50% and 10-year Treasury around 4.0–4.5% in mid-2025—raise private developers’ hurdle rates and push out notices to proceed. Public owners often sustain planned spend while private manufacturing projects stagger starts. Design-build with guaranteed pricing gains appeal in this volatile rate regime. Walbridge’s strong balance sheet and bonding capacity enable competitive terms.

Materials cost volatility

Volatility in steel (spot swings ~25% YoY in 2023–24), concrete and electrical gear prices plus switchgear lead times often stretching 20–28 weeks materially complicate bid assumptions and contingency sizing. Index-linked contracts and escalation clauses have become standard to protect margins amid ~6% construction materials inflation in 2023. Early lock-ins and strategic supplier alliances cut exposure to spot moves, while Walbridge’s procurement scale yields allocation priority and negotiated price discounts.

Skilled labor supply

Trade shortages push up labor costs and raise productivity expectations; 80% of contractors reported difficulty hiring skilled craft workers in AGC’s 2024 survey. Robust training pipelines and apprenticeship partnerships are vital to delivery certainty and reduce turnover. Walbridge’s self-perform capabilities give schedule control and quality advantages. Guaranteeing dedicated crews lets Walbridge capture premium, time-sensitive work.

Manufacturing and auto cycles

Global EV sales were roughly 14 million units in 2024, driving strong OEM capex and supplier EV programs that feed Walbridge’s core backlog; cycle turns dictate plant upgrades, retooling and greenfield builds as OEMs phase new EV lines. Diversification into power and industrial reduces exposure to auto cyclicality, while Walbridge’s track record in complex process facilities differentiates it on large retrofit and greenfield work.

- OEM capex & supplier programs: primary backlog driver

- Cycle turns: trigger upgrades, retooling, greenfields

- Diversification: power/industrial cushions automotive swings

- Competitive edge: experience in complex process facilities

Client capital allocation

Client capital allocation favors reshoring and resilience, driving U.S. facility growth as manufacturing represents roughly 11% of GDP; inventory and dual-sourcing strategies increase demand for fast-build plants. CFOs prioritizing total cost of ownership lift demand for lifecycle and speed-to-market solutions, while off-balance-sheet and P3 structures can unlock constrained credit. Walbridge can win by packaging EPC, fast-track delivery, and cost-certainty guarantees.

- Reshoring-driven facility expansion

- CFO TCO focus → lifecycle solutions

- P3/off-balance-sheet unlocks projects

- Walbridge: EPC + fast-track + cost certainty

BIL, IRA and CHIPS spur megaproject pipelines; tariffs, labor rules and scale raise bid volatility

Higher rates (FF 5.25–5.50%, 10y 4.0–4.5% mid‑2025) raise hurdle rates and favor fixed‑price DB work; materials inflation (~6% in 2023) and steel spot swings ~25% YoY squeeze margins; skilled labor shortages (AGC: ~80% reporting 2024) elevate labor costs; EV demand (~14M sales in 2024) sustains OEM capex and backlog.

| Metric | Value | Impact |

|---|---|---|

| Fed funds | 5.25–5.50% | Higher hurdle rates |

| 10y | 4.0–4.5% | Capex cost |

| Materials inflation | ~6% | Margin pressure |

| EV sales | ~14M (2024) | Backlog driver |

What You See Is What You Get

Walbridge PESTLE Analysis

The Walbridge PESTLE analysis shown here is the actual document you’ll receive after purchase—fully formatted, professionally structured, and ready to use. The preview reflects the final content, layout, and structure with no placeholders or omissions. After checkout you’ll instantly download this exact file and can apply the insights immediately.

Description

Your Shortcut to Market Insight Starts Here

Gain a strategic edge with our focused PESTLE Analysis of Walbridge, revealing the political, economic, social, technological, legal, and environmental forces shaping its future. Use these concise insights to spot risks and growth opportunities fast. Purchase the full analysis now for the complete, actionable report ready for immediate use.

Political factors

Federal infrastructure spending

Federal infrastructure funding cycles, anchored by the Bipartisan Infrastructure Law with roughly $550 billion in new investments including about $110 billion for roads and bridges and $55 billion for water, drive multi-year project pipelines. Bipartisan programs stabilize backlog and enable long-duration award structures, while shifts in appropriations or continuing resolutions routinely delay starts and strain cash flow. Walbridge’s national scale positions it to pursue federally-backed megaprojects funded through these programs.

Industrial policy incentives

IRA's roughly $369 billion in clean-energy incentives, the CHIPS Act's ~280 billion authorization including about $52.7 billion for semiconductor incentives, and targeted advanced-manufacturing credits are catalyzing factories, battery plants and power projects. Incentive clarity affects client site selection and project timelines, while domestic-content and critical-mineral rules determine sourcing and self-perform strategies. Walbridge can align delivery models and trades integration to help clients meet compliance thresholds and capture credits.

Trade and tariff dynamics

Tariffs on steel (25%) and aluminum (10%) and levies on equipment directly inflate bid prices and trigger escalation clauses. Geopolitical shifts since 2022 have disrupted global supply chains for specialized components, raising procurement volatility. Early procurement and alternate sourcing reduce exposure and schedule risk. Clients increasingly demand transparent tariff pass-throughs and cost breakdowns from contractors.

Labor and union relations

Project labor agreements and prevailing wage rules materially shape project cost structures; EO 14063 (2021) encourages PLA use on federal projects over $35 million and the Davis-Bacon Act applies prevailing wages on federal contracts above $2,000. Political support for organized labor can expand PLA adoption, while collaborative labor strategies help ensure craft availability across regions and Walbridge’s self-perform model benefits from stable labor frameworks.

- EO 14063 — PLA encouragement on federal projects >35,000,000

- Davis-Bacon — prevailing wages on federal contracts >2,000

- PLAs increase cost predictability

- Walbridge self-perform reduces subcontract exposure

Energy and permitting policy

Transmission, generation mix, and grid modernization priorities drive power-sector demand; the Inflation Reduction Act provided about 369 billion for energy and climate and the Bipartisan Infrastructure Law dedicated 7.5 billion for EV charging, boosting project pipelines.

Streamlined federal and state permitting reduces schedule risk on complex sites; policy support—including roughly 6 billion in Civil Nuclear Credit and expanded renewables tax credits—creates new build categories Walbridge can target.

- Transmission investment: higher grid upgrade demand

- Permitting: lower schedule risk

- Support: nuclear, renewables, EV charging

- Positioning: target policy tailwinds

BIL, IRA and CHIPS spur megaproject pipelines; tariffs, labor rules and scale raise bid volatility

Federal infrastructure funding (BIL ~$550B), IRA ($369B) and CHIPS ($280B) create multi-year pipelines; tariffs (steel 25%, aluminum 10%) and supply-chain shifts raise bid volatility. Labor rules (EO 14063 >35,000,000; Davis-Bacon >2,000) inflate costs; Walbridge scale and self-perform reduce subcontract exposure and capture federally backed megaprojects.

| Metric | Value |

|---|---|

| BIL | $550B |

| IRA | $369B |

| CHIPS | $280B |

| Steel tariff | 25% |

What is included in the product

Explores how external macro-environmental factors uniquely affect Walbridge across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with each category expanded into detailed, business-specific sub-points and forward-looking insights. Backed by current data and market/regulatory dynamics, it’s formatted for direct use in business plans, pitch decks, and executive decision-making.

The Walbridge PESTLE Analysis delivers a concise, visually segmented summary of external factors that’s easily editable and shareable, enabling quick alignment across teams and streamlined use in presentations or planning sessions.

Economic factors

Interest rate environment

Higher policy rates—federal funds near 5.25–5.50% and 10-year Treasury around 4.0–4.5% in mid-2025—raise private developers’ hurdle rates and push out notices to proceed. Public owners often sustain planned spend while private manufacturing projects stagger starts. Design-build with guaranteed pricing gains appeal in this volatile rate regime. Walbridge’s strong balance sheet and bonding capacity enable competitive terms.

Materials cost volatility

Volatility in steel (spot swings ~25% YoY in 2023–24), concrete and electrical gear prices plus switchgear lead times often stretching 20–28 weeks materially complicate bid assumptions and contingency sizing. Index-linked contracts and escalation clauses have become standard to protect margins amid ~6% construction materials inflation in 2023. Early lock-ins and strategic supplier alliances cut exposure to spot moves, while Walbridge’s procurement scale yields allocation priority and negotiated price discounts.

Skilled labor supply

Trade shortages push up labor costs and raise productivity expectations; 80% of contractors reported difficulty hiring skilled craft workers in AGC’s 2024 survey. Robust training pipelines and apprenticeship partnerships are vital to delivery certainty and reduce turnover. Walbridge’s self-perform capabilities give schedule control and quality advantages. Guaranteeing dedicated crews lets Walbridge capture premium, time-sensitive work.

Manufacturing and auto cycles

Global EV sales were roughly 14 million units in 2024, driving strong OEM capex and supplier EV programs that feed Walbridge’s core backlog; cycle turns dictate plant upgrades, retooling and greenfield builds as OEMs phase new EV lines. Diversification into power and industrial reduces exposure to auto cyclicality, while Walbridge’s track record in complex process facilities differentiates it on large retrofit and greenfield work.

- OEM capex & supplier programs: primary backlog driver

- Cycle turns: trigger upgrades, retooling, greenfields

- Diversification: power/industrial cushions automotive swings

- Competitive edge: experience in complex process facilities

Client capital allocation

Client capital allocation favors reshoring and resilience, driving U.S. facility growth as manufacturing represents roughly 11% of GDP; inventory and dual-sourcing strategies increase demand for fast-build plants. CFOs prioritizing total cost of ownership lift demand for lifecycle and speed-to-market solutions, while off-balance-sheet and P3 structures can unlock constrained credit. Walbridge can win by packaging EPC, fast-track delivery, and cost-certainty guarantees.

- Reshoring-driven facility expansion

- CFO TCO focus → lifecycle solutions

- P3/off-balance-sheet unlocks projects

- Walbridge: EPC + fast-track + cost certainty

BIL, IRA and CHIPS spur megaproject pipelines; tariffs, labor rules and scale raise bid volatility

Higher rates (FF 5.25–5.50%, 10y 4.0–4.5% mid‑2025) raise hurdle rates and favor fixed‑price DB work; materials inflation (~6% in 2023) and steel spot swings ~25% YoY squeeze margins; skilled labor shortages (AGC: ~80% reporting 2024) elevate labor costs; EV demand (~14M sales in 2024) sustains OEM capex and backlog.

| Metric | Value | Impact |

|---|---|---|

| Fed funds | 5.25–5.50% | Higher hurdle rates |

| 10y | 4.0–4.5% | Capex cost |

| Materials inflation | ~6% | Margin pressure |

| EV sales | ~14M (2024) | Backlog driver |

What You See Is What You Get

Walbridge PESTLE Analysis

The Walbridge PESTLE analysis shown here is the actual document you’ll receive after purchase—fully formatted, professionally structured, and ready to use. The preview reflects the final content, layout, and structure with no placeholders or omissions. After checkout you’ll instantly download this exact file and can apply the insights immediately.