Walker & Dunlop SWOT Analysis

Go Beyond the Preview—Access the Full Strategic Report

Walker & Dunlop SWOT snapshot highlights strong market position in commercial real estate finance, scale advantages, and regulatory and interest-rate risks; competitive pressures and loan concentration warrant close review. Want deeper financial context, strategic recommendations, and editable Word/Excel deliverables? Purchase the full SWOT analysis to access a research-backed, investor-ready report for planning, pitching, and decision-making.

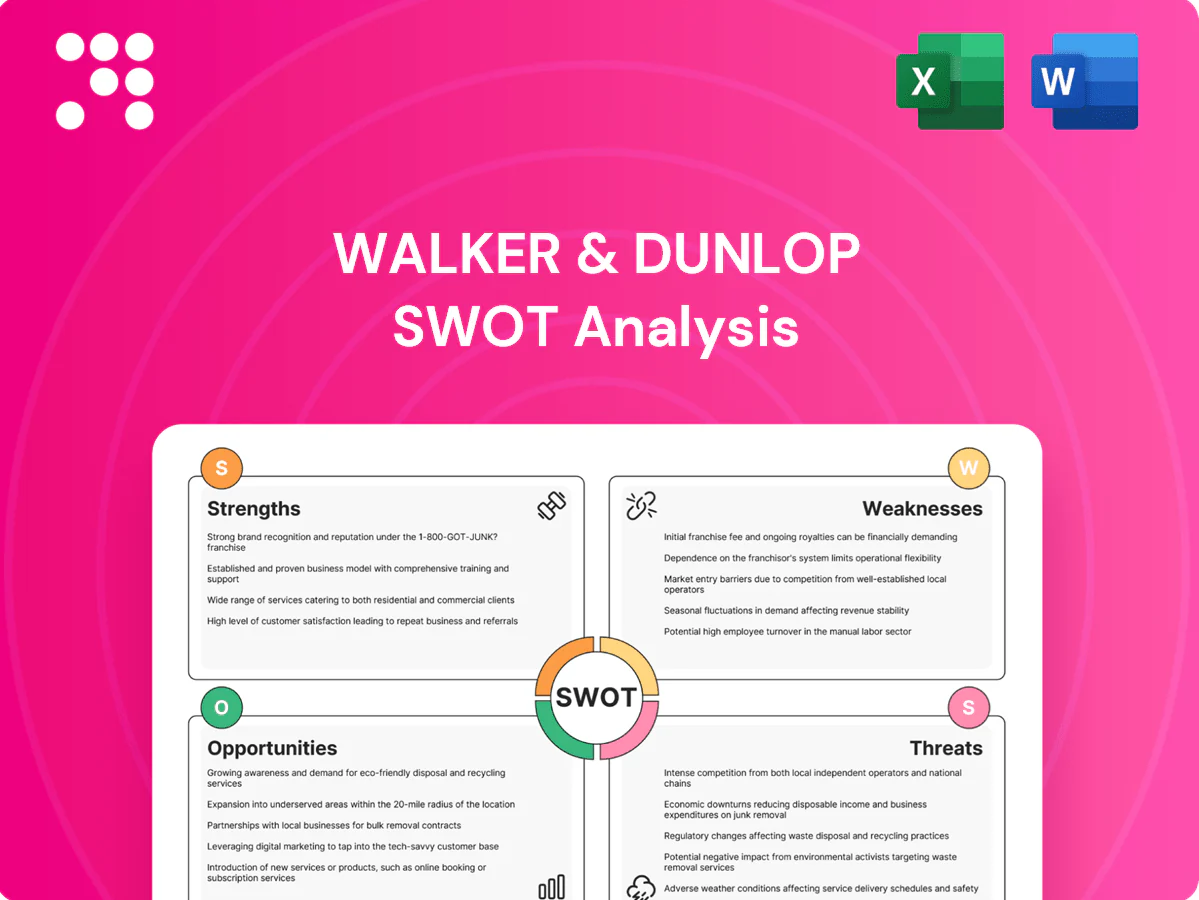

Strengths

Top-tier multifamily lender

Consistently ranked among the largest agency multifamily lenders, Walker & Dunlop originated over $35 billion in multifamily loans in 2024, reinforcing brand credibility and steady deal flow with Fannie Mae, Freddie Mac and HUD.

Deep agency relationships deliver execution certainty and competitive pricing, while scale drives data advantages, helping retain repeat clients (over 40% share) and attracting brokers, borrowers and institutional partners.

Diverse capital solutions

Walker & Dunlop offers agency, bridge, life company, CMBS and bank placements across multifamily and commercial lending, enabling one-stop tailored capital structures across cycles; cross-product advisory increased win rates and wallet share, with diversified channels driving resilience and reducing dependence on any single funding source (2024 origination platform exceeded $50 billion).

Recurring servicing and fee income

Walker & Dunlop’s servicing arm, with a servicing portfolio exceeding $100 billion, generates predictable, high-margin annuity-like cash flows that bolster valuation. Servicing relationships increase client stickiness and create upsell pathways across CMBS, agency and balance-sheet products. Countercyclical fee streams help offset origination volatility, while long-dated contracts improve cash flow visibility and support higher multiples.

Integrated sales and investment management

Integrated sales and investment management at Walker & Dunlop aligns investment sales with debt placement, improving information flow and underwriting accuracy while capturing AUM-based fees and co-invest alignment to boost recurring revenue and sponsor alignment. The platform enables stronger cross-selling and full-lifecycle client coverage, creating an ecosystem advantage over monoline lenders.

- Improved underwriting via bidirectional deal intel

- AUM fees + co-invests = recurring, aligned revenue

- Cross-sell across origination, servicing, asset management

- Differentiates versus single-product lenders

Data and technology capabilities

Walker & Dunlop leverages proprietary analytics and appraisal tech to accelerate underwriting and pricing, reducing cycle times and improving margin capture; the platform supported the firm’s expanded originations in 2024. Technology-driven screening and pipeline conversion lift credit selection and deal velocity across CRE segments. Scalable systems enable national coverage with specialized teams, and data advantages compound as transaction volume grows.

- Proprietary analytics: faster underwriting

- Appraisal tech: improved pricing accuracy

- Pipeline conversion: higher deal velocity

- Scalable systems: national + segment specialization

- Data compounding: stronger with rising transaction volume

Agency multifamily leader: $35B+ originations, $100B+ servicing, 40%+ repeat clients

Ranked among largest agency multifamily lenders, Walker & Dunlop originated >$35B multifamily loans in 2024, reinforcing brand and agency access.

Scale and deep Fannie/Freddie/HUD relationships drive execution certainty, competitive pricing and >40% repeat client share.

Servicing portfolio >$100B delivers annuity-like fees; proprietary analytics and appraisal tech accelerate underwriting and margin capture.

| Metric | 2024 |

|---|---|

| Multifamily originations | $35B+ |

| Total origination platform | $50B+ |

| Servicing portfolio | $100B+ |

| Repeat client share | >40% |

What is included in the product

Delivers a strategic overview of Walker & Dunlop’s internal and external business factors, outlining strengths, weaknesses, opportunities, and threats that shape its competitive position and growth prospects.

Delivers a concise SWOT matrix tailored to Walker & Dunlop for rapid strategy alignment. Ideal for executives and teams needing a stakeholder-ready snapshot to ease decision-making.

Weaknesses

Rate and volume sensitivity

Origination revenues at Walker & Dunlop are highly correlated with interest rate levels and market liquidity; the 30-year fixed mortgage rate peaking at 7.79% in October 2023 and averaging around 6.7% through 2024 sharply reduced refinance demand. Spikes in rates compress borrower proceeds and curtail originations, while elevated rate volatility increases pipeline fallouts and pressures fee income. As a result, earnings can be lumpy quarter-to-quarter, tied to rate-driven origination cycles.

Reliance on GSE channels

Reliance on GSE channels exposes Walker & Dunlop to agency caps, pricing shifts, and underwriting changes that can swiftly reduce origination volumes. Concentration in agency executions limits flexibility when GSE allocations tighten, forcing deal cadence and cash flow volatility. Heightened competition for agency mandates compresses margins and policy changes from regulators add planning uncertainty.

Exposure to CRE cyclicality

Walker & Dunlop remains highly exposed to CRE cyclicality: national office vacancy was about 16.6% in Q1 2025 (CBRE) and cap rates have widened roughly 150 bps since 2021, which dampens borrower demand. CRE transaction volumes are down roughly 50% from the 2021 peak, wider credit spreads and a 10-year Treasury near 4.2% reduce proceeds and feasibility, leaving revenue diversification still tied to the CRE cycle.

Margin pressure from competition

Walker & Dunlop (NYSE: WD) faces margin pressure as it competes with global brokers like CBRE and JLL and specialist lenders such as Berkadia, forcing fee compression that often emerges in bull markets and becomes entrenched as pricing norms shift.

Winning mandates increasingly requires pricing concessions or bundled services, and scale advantages are frequently offset by a crowded field and intense competition for the same deals.

- Competition: CBRE, JLL, Berkadia

- Market effect: fee compression in bull markets

- Sales tactic: pricing concessions or added services

- Scale risk: benefits offset by crowded market

Limited balance-sheet lending

An originate-to-sell model limits Walker & Dunlop's control versus balance-sheet lenders during market dislocations, reducing pricing and execution flexibility. Reliance on third-party investors can delay closings when markets seize, slowing deal flow and client service. Limited ability to warehouse credit constrains opportunistic plays and keeps revenue tied to placement fees rather than net interest income.

- originate-to-sell exposure

- third-party investor timing risk

- limited risk warehousing

- fee-driven revenue model

Rate swings and agency limits squeeze mortgage origination and CRE volumes

Origination revenues are highly rate-sensitive (30-year fixed ~6.7% avg in 2024; peak 7.79% in Oct 2023), causing lumpy quarterly earnings and pipeline fallouts. Heavy reliance on GSE channels limits flexibility when agency caps or pricing shift, compressing volumes and fees. Significant CRE cyclicality (office vacancy 16.6% Q1 2025; transaction volume ~50% below 2021) tightens demand and margin pressure.

| Metric | Value |

|---|---|

| 30-yr fixed rate (avg 2024) | 6.7% |

| 30-yr peak | 7.79% (Oct 2023) |

| Office vacancy | 16.6% (Q1 2025) |

| CRE transaction vols vs 2021 | -50% |

Full Version Awaits

Walker & Dunlop SWOT Analysis

This is the actual Walker & Dunlop SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full report you'll get; buying unlocks the complete, editable version. You’re viewing a live excerpt of the real file, structured and ready to use. The full document becomes available immediately after checkout.

Go Beyond the Preview—Access the Full Strategic Report

Walker & Dunlop SWOT snapshot highlights strong market position in commercial real estate finance, scale advantages, and regulatory and interest-rate risks; competitive pressures and loan concentration warrant close review. Want deeper financial context, strategic recommendations, and editable Word/Excel deliverables? Purchase the full SWOT analysis to access a research-backed, investor-ready report for planning, pitching, and decision-making.

Strengths

Top-tier multifamily lender

Consistently ranked among the largest agency multifamily lenders, Walker & Dunlop originated over $35 billion in multifamily loans in 2024, reinforcing brand credibility and steady deal flow with Fannie Mae, Freddie Mac and HUD.

Deep agency relationships deliver execution certainty and competitive pricing, while scale drives data advantages, helping retain repeat clients (over 40% share) and attracting brokers, borrowers and institutional partners.

Diverse capital solutions

Walker & Dunlop offers agency, bridge, life company, CMBS and bank placements across multifamily and commercial lending, enabling one-stop tailored capital structures across cycles; cross-product advisory increased win rates and wallet share, with diversified channels driving resilience and reducing dependence on any single funding source (2024 origination platform exceeded $50 billion).

Recurring servicing and fee income

Walker & Dunlop’s servicing arm, with a servicing portfolio exceeding $100 billion, generates predictable, high-margin annuity-like cash flows that bolster valuation. Servicing relationships increase client stickiness and create upsell pathways across CMBS, agency and balance-sheet products. Countercyclical fee streams help offset origination volatility, while long-dated contracts improve cash flow visibility and support higher multiples.

Integrated sales and investment management

Integrated sales and investment management at Walker & Dunlop aligns investment sales with debt placement, improving information flow and underwriting accuracy while capturing AUM-based fees and co-invest alignment to boost recurring revenue and sponsor alignment. The platform enables stronger cross-selling and full-lifecycle client coverage, creating an ecosystem advantage over monoline lenders.

- Improved underwriting via bidirectional deal intel

- AUM fees + co-invests = recurring, aligned revenue

- Cross-sell across origination, servicing, asset management

- Differentiates versus single-product lenders

Data and technology capabilities

Walker & Dunlop leverages proprietary analytics and appraisal tech to accelerate underwriting and pricing, reducing cycle times and improving margin capture; the platform supported the firm’s expanded originations in 2024. Technology-driven screening and pipeline conversion lift credit selection and deal velocity across CRE segments. Scalable systems enable national coverage with specialized teams, and data advantages compound as transaction volume grows.

- Proprietary analytics: faster underwriting

- Appraisal tech: improved pricing accuracy

- Pipeline conversion: higher deal velocity

- Scalable systems: national + segment specialization

- Data compounding: stronger with rising transaction volume

Agency multifamily leader: $35B+ originations, $100B+ servicing, 40%+ repeat clients

Ranked among largest agency multifamily lenders, Walker & Dunlop originated >$35B multifamily loans in 2024, reinforcing brand and agency access.

Scale and deep Fannie/Freddie/HUD relationships drive execution certainty, competitive pricing and >40% repeat client share.

Servicing portfolio >$100B delivers annuity-like fees; proprietary analytics and appraisal tech accelerate underwriting and margin capture.

| Metric | 2024 |

|---|---|

| Multifamily originations | $35B+ |

| Total origination platform | $50B+ |

| Servicing portfolio | $100B+ |

| Repeat client share | >40% |

What is included in the product

Delivers a strategic overview of Walker & Dunlop’s internal and external business factors, outlining strengths, weaknesses, opportunities, and threats that shape its competitive position and growth prospects.

Delivers a concise SWOT matrix tailored to Walker & Dunlop for rapid strategy alignment. Ideal for executives and teams needing a stakeholder-ready snapshot to ease decision-making.

Weaknesses

Rate and volume sensitivity

Origination revenues at Walker & Dunlop are highly correlated with interest rate levels and market liquidity; the 30-year fixed mortgage rate peaking at 7.79% in October 2023 and averaging around 6.7% through 2024 sharply reduced refinance demand. Spikes in rates compress borrower proceeds and curtail originations, while elevated rate volatility increases pipeline fallouts and pressures fee income. As a result, earnings can be lumpy quarter-to-quarter, tied to rate-driven origination cycles.

Reliance on GSE channels

Reliance on GSE channels exposes Walker & Dunlop to agency caps, pricing shifts, and underwriting changes that can swiftly reduce origination volumes. Concentration in agency executions limits flexibility when GSE allocations tighten, forcing deal cadence and cash flow volatility. Heightened competition for agency mandates compresses margins and policy changes from regulators add planning uncertainty.

Exposure to CRE cyclicality

Walker & Dunlop remains highly exposed to CRE cyclicality: national office vacancy was about 16.6% in Q1 2025 (CBRE) and cap rates have widened roughly 150 bps since 2021, which dampens borrower demand. CRE transaction volumes are down roughly 50% from the 2021 peak, wider credit spreads and a 10-year Treasury near 4.2% reduce proceeds and feasibility, leaving revenue diversification still tied to the CRE cycle.

Margin pressure from competition

Walker & Dunlop (NYSE: WD) faces margin pressure as it competes with global brokers like CBRE and JLL and specialist lenders such as Berkadia, forcing fee compression that often emerges in bull markets and becomes entrenched as pricing norms shift.

Winning mandates increasingly requires pricing concessions or bundled services, and scale advantages are frequently offset by a crowded field and intense competition for the same deals.

- Competition: CBRE, JLL, Berkadia

- Market effect: fee compression in bull markets

- Sales tactic: pricing concessions or added services

- Scale risk: benefits offset by crowded market

Limited balance-sheet lending

An originate-to-sell model limits Walker & Dunlop's control versus balance-sheet lenders during market dislocations, reducing pricing and execution flexibility. Reliance on third-party investors can delay closings when markets seize, slowing deal flow and client service. Limited ability to warehouse credit constrains opportunistic plays and keeps revenue tied to placement fees rather than net interest income.

- originate-to-sell exposure

- third-party investor timing risk

- limited risk warehousing

- fee-driven revenue model

Rate swings and agency limits squeeze mortgage origination and CRE volumes

Origination revenues are highly rate-sensitive (30-year fixed ~6.7% avg in 2024; peak 7.79% in Oct 2023), causing lumpy quarterly earnings and pipeline fallouts. Heavy reliance on GSE channels limits flexibility when agency caps or pricing shift, compressing volumes and fees. Significant CRE cyclicality (office vacancy 16.6% Q1 2025; transaction volume ~50% below 2021) tightens demand and margin pressure.

| Metric | Value |

|---|---|

| 30-yr fixed rate (avg 2024) | 6.7% |

| 30-yr peak | 7.79% (Oct 2023) |

| Office vacancy | 16.6% (Q1 2025) |

| CRE transaction vols vs 2021 | -50% |

Full Version Awaits

Walker & Dunlop SWOT Analysis

This is the actual Walker & Dunlop SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full report you'll get; buying unlocks the complete, editable version. You’re viewing a live excerpt of the real file, structured and ready to use. The full document becomes available immediately after checkout.

Original: $10.00

-65%$10.00

$3.50Description

Go Beyond the Preview—Access the Full Strategic Report

Walker & Dunlop SWOT snapshot highlights strong market position in commercial real estate finance, scale advantages, and regulatory and interest-rate risks; competitive pressures and loan concentration warrant close review. Want deeper financial context, strategic recommendations, and editable Word/Excel deliverables? Purchase the full SWOT analysis to access a research-backed, investor-ready report for planning, pitching, and decision-making.

Strengths

Top-tier multifamily lender

Consistently ranked among the largest agency multifamily lenders, Walker & Dunlop originated over $35 billion in multifamily loans in 2024, reinforcing brand credibility and steady deal flow with Fannie Mae, Freddie Mac and HUD.

Deep agency relationships deliver execution certainty and competitive pricing, while scale drives data advantages, helping retain repeat clients (over 40% share) and attracting brokers, borrowers and institutional partners.

Diverse capital solutions

Walker & Dunlop offers agency, bridge, life company, CMBS and bank placements across multifamily and commercial lending, enabling one-stop tailored capital structures across cycles; cross-product advisory increased win rates and wallet share, with diversified channels driving resilience and reducing dependence on any single funding source (2024 origination platform exceeded $50 billion).

Recurring servicing and fee income

Walker & Dunlop’s servicing arm, with a servicing portfolio exceeding $100 billion, generates predictable, high-margin annuity-like cash flows that bolster valuation. Servicing relationships increase client stickiness and create upsell pathways across CMBS, agency and balance-sheet products. Countercyclical fee streams help offset origination volatility, while long-dated contracts improve cash flow visibility and support higher multiples.

Integrated sales and investment management

Integrated sales and investment management at Walker & Dunlop aligns investment sales with debt placement, improving information flow and underwriting accuracy while capturing AUM-based fees and co-invest alignment to boost recurring revenue and sponsor alignment. The platform enables stronger cross-selling and full-lifecycle client coverage, creating an ecosystem advantage over monoline lenders.

- Improved underwriting via bidirectional deal intel

- AUM fees + co-invests = recurring, aligned revenue

- Cross-sell across origination, servicing, asset management

- Differentiates versus single-product lenders

Data and technology capabilities

Walker & Dunlop leverages proprietary analytics and appraisal tech to accelerate underwriting and pricing, reducing cycle times and improving margin capture; the platform supported the firm’s expanded originations in 2024. Technology-driven screening and pipeline conversion lift credit selection and deal velocity across CRE segments. Scalable systems enable national coverage with specialized teams, and data advantages compound as transaction volume grows.

- Proprietary analytics: faster underwriting

- Appraisal tech: improved pricing accuracy

- Pipeline conversion: higher deal velocity

- Scalable systems: national + segment specialization

- Data compounding: stronger with rising transaction volume

Agency multifamily leader: $35B+ originations, $100B+ servicing, 40%+ repeat clients

Ranked among largest agency multifamily lenders, Walker & Dunlop originated >$35B multifamily loans in 2024, reinforcing brand and agency access.

Scale and deep Fannie/Freddie/HUD relationships drive execution certainty, competitive pricing and >40% repeat client share.

Servicing portfolio >$100B delivers annuity-like fees; proprietary analytics and appraisal tech accelerate underwriting and margin capture.

| Metric | 2024 |

|---|---|

| Multifamily originations | $35B+ |

| Total origination platform | $50B+ |

| Servicing portfolio | $100B+ |

| Repeat client share | >40% |

What is included in the product

Delivers a strategic overview of Walker & Dunlop’s internal and external business factors, outlining strengths, weaknesses, opportunities, and threats that shape its competitive position and growth prospects.

Delivers a concise SWOT matrix tailored to Walker & Dunlop for rapid strategy alignment. Ideal for executives and teams needing a stakeholder-ready snapshot to ease decision-making.

Weaknesses

Rate and volume sensitivity

Origination revenues at Walker & Dunlop are highly correlated with interest rate levels and market liquidity; the 30-year fixed mortgage rate peaking at 7.79% in October 2023 and averaging around 6.7% through 2024 sharply reduced refinance demand. Spikes in rates compress borrower proceeds and curtail originations, while elevated rate volatility increases pipeline fallouts and pressures fee income. As a result, earnings can be lumpy quarter-to-quarter, tied to rate-driven origination cycles.

Reliance on GSE channels

Reliance on GSE channels exposes Walker & Dunlop to agency caps, pricing shifts, and underwriting changes that can swiftly reduce origination volumes. Concentration in agency executions limits flexibility when GSE allocations tighten, forcing deal cadence and cash flow volatility. Heightened competition for agency mandates compresses margins and policy changes from regulators add planning uncertainty.

Exposure to CRE cyclicality

Walker & Dunlop remains highly exposed to CRE cyclicality: national office vacancy was about 16.6% in Q1 2025 (CBRE) and cap rates have widened roughly 150 bps since 2021, which dampens borrower demand. CRE transaction volumes are down roughly 50% from the 2021 peak, wider credit spreads and a 10-year Treasury near 4.2% reduce proceeds and feasibility, leaving revenue diversification still tied to the CRE cycle.

Margin pressure from competition

Walker & Dunlop (NYSE: WD) faces margin pressure as it competes with global brokers like CBRE and JLL and specialist lenders such as Berkadia, forcing fee compression that often emerges in bull markets and becomes entrenched as pricing norms shift.

Winning mandates increasingly requires pricing concessions or bundled services, and scale advantages are frequently offset by a crowded field and intense competition for the same deals.

- Competition: CBRE, JLL, Berkadia

- Market effect: fee compression in bull markets

- Sales tactic: pricing concessions or added services

- Scale risk: benefits offset by crowded market

Limited balance-sheet lending

An originate-to-sell model limits Walker & Dunlop's control versus balance-sheet lenders during market dislocations, reducing pricing and execution flexibility. Reliance on third-party investors can delay closings when markets seize, slowing deal flow and client service. Limited ability to warehouse credit constrains opportunistic plays and keeps revenue tied to placement fees rather than net interest income.

- originate-to-sell exposure

- third-party investor timing risk

- limited risk warehousing

- fee-driven revenue model

Rate swings and agency limits squeeze mortgage origination and CRE volumes

Origination revenues are highly rate-sensitive (30-year fixed ~6.7% avg in 2024; peak 7.79% in Oct 2023), causing lumpy quarterly earnings and pipeline fallouts. Heavy reliance on GSE channels limits flexibility when agency caps or pricing shift, compressing volumes and fees. Significant CRE cyclicality (office vacancy 16.6% Q1 2025; transaction volume ~50% below 2021) tightens demand and margin pressure.

| Metric | Value |

|---|---|

| 30-yr fixed rate (avg 2024) | 6.7% |

| 30-yr peak | 7.79% (Oct 2023) |

| Office vacancy | 16.6% (Q1 2025) |

| CRE transaction vols vs 2021 | -50% |

Full Version Awaits

Walker & Dunlop SWOT Analysis

This is the actual Walker & Dunlop SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full report you'll get; buying unlocks the complete, editable version. You’re viewing a live excerpt of the real file, structured and ready to use. The full document becomes available immediately after checkout.