Walsh Group Boston Consulting Group Matrix

Actionable Strategy Starts Here

The Walsh Group BCG Matrix preview gives you a quick read on which products lead, which fund growth, and which may be dragging returns. Ready for the full picture? Purchase the complete BCG Matrix to get quadrant-level placements, data-backed recommendations, and downloadable Word and Excel files so you can act fast and present with confidence.

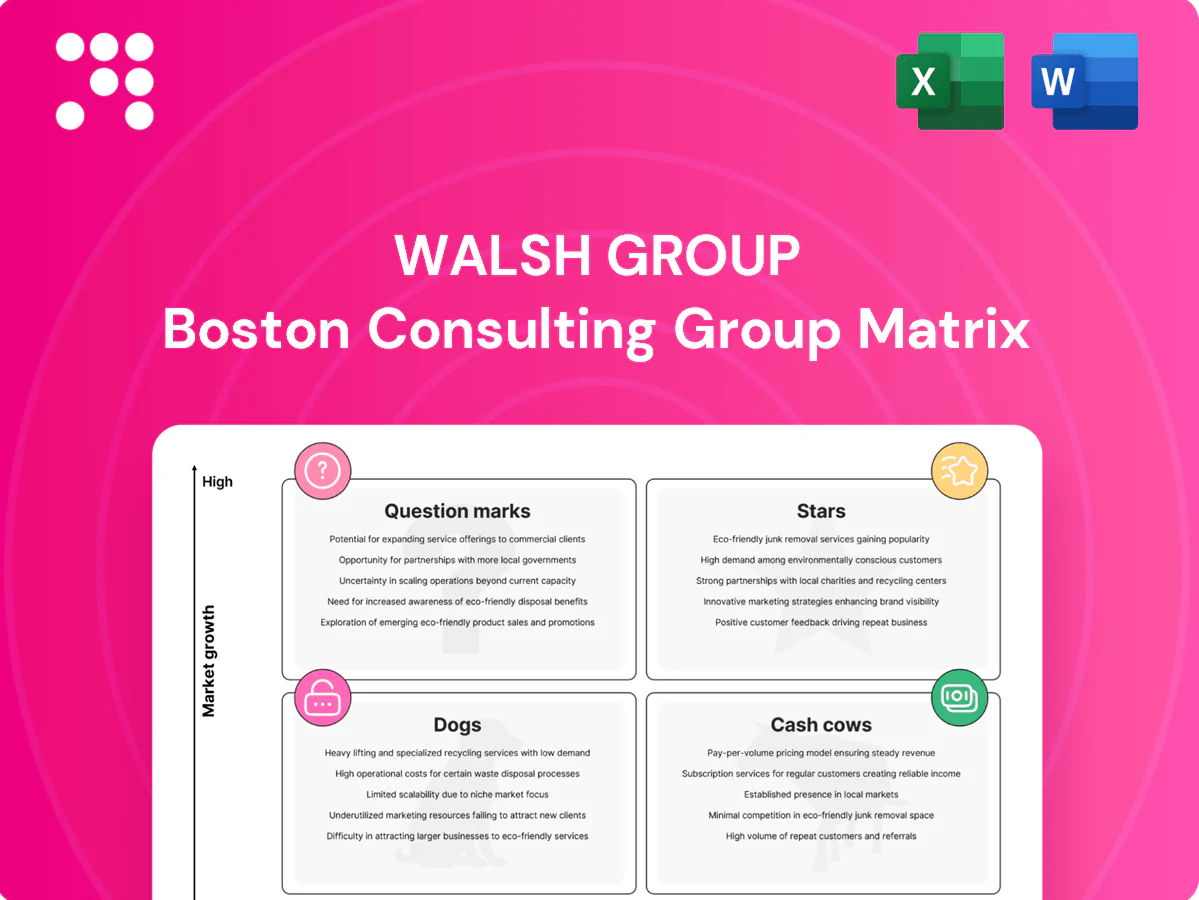

Stars

Design‑build transportation megaprojects

Design-build transportation megaprojects are Stars for Walsh, capturing a significant share of projects tied to the Bipartisan Infrastructure Law’s $550 billion in new spending; a growing pipeline of highways, bridges and rail boosts market share. Walsh’s integrated design-build chops deliver speed and schedule certainty, winning awards and backlog. These projects consume cash on delivery but create authority, margin and recurring revenue; continued reinvestment turns them into long-term cash machines.

Water and wastewater treatment programs

Urban growth and 2024 climate and water-quality mandates keep the water and wastewater segment hot; federal Infrastructure Law directed roughly 55 billion for U.S. water infrastructure, sustaining project pipelines. Walsh’s proven complex-plant delivery and commissioning give a competitive edge on high-capex, high-technical-risk builds. If Walsh sustains share, these plants convert into annuity-like long-term service and O&M revenue streams.

Aviation terminals and airfield upgrades

With IATA reporting 2023 RPKs at about 94% of 2019 levels and 2024 traffic near full recovery, demand fuels terminal expansion while FAA Airport Improvement Program apportionment (~$3.35B in 2024) and stable PFC cap ($4.50) underwrite projects. Walsh’s strength in large, phased live‑environment builds requires heavy upfront coordination and cash draw but yields outsized brand lift. Hold position and harvest as federal funding normalizes.

Healthcare and higher‑ed complexes

Healthcare and higher-ed complexes are specialty builds with strict codes and tight phasing; Walsh’s CM/GC plus self-perform turns theoretical schedules into realized timelines, cutting punch-list time and change orders. These projects command high visibility, repeat owners, and premium fees when executed well; Dodge Data reported ~6% growth in healthcare and education starts in 2024, so defend the lead.

- Specialty codes, tight phasing

- CM/GC + self-perform = reliable schedules

- High visibility, repeat owners, premium fees

- Market growth ~6% in 2024 — protect position

Alternative delivery and P3 execution

Owners demand risk transfer and single‑throat accountability; Walsh’s end‑to‑end design-build-finance-operate capabilities secure early table positioning. These P3s require substantial capital and top talent, but successful bids reset firm ceilings—public infrastructure funding (IIJA) remains $1.2 trillion commitment since 2021, sustaining 2024 pipelines.

- Risk transfer

- Early entry

- High capital/talent

- Ceiling reset

- Invest where pipeline strong

Design-build surge: transport, water, airports, healthcare drive 2024 pipelines

Walsh Stars: design‑build transportation, water, airports and healthcare show strong 2024 pipelines—IIJA/Bipartisan Infrastructure Law ~$1.2T since 2021 with $550B new spending; US water ~$55B; FAA AIP ~$3.35B (2024); healthcare/edu starts +6% (2024). These high-capex segments drive margin, backlog and annuity potential.

| Segment | 2024 Cue | Impact |

|---|---|---|

| Transport | $550B IIJA new | Backlog, margin |

| Water | $55B | O&M annuities |

| Airports | AIP $3.35B | Phased terminals |

| Healthcare | +6% starts | Premium fees |

What is included in the product

Comprehensive BCG Matrix for Walsh Group, identifying Stars, Cash Cows, Question Marks and Dogs with clear strategic actions.

One-page Walsh BCG Matrix placing each unit in a quadrant to remove clutter and speed C-level decisions

Cash Cows

General contracting for mature building markets

Corporate interiors, K‑12 and municipal building work—anchored by Walsh Group’s Chicago base—deliver steady, predictable cash flows with high share in key geographies; the portfolio sits in low single-digit market growth and stable public budget allocations in 2024. Minimal promotion is needed as long‑standing client relationships drive pipeline; focus is on operational efficiency and margin preservation.

Construction management at‑risk for repeat public clients

Construction management at‑risk secures repeat city, county and agency work by delivering reliable outcomes; with the Bipartisan Infrastructure Law still driving $550 billion in new investment as of 2024, public funding remains stable. The moat is process knowledge over flash; retain teams, standardize playbooks, and milk efficiency through repeatable delivery.

Self‑perform concrete and civil packages

Self-perform concrete and civil packages act as cash cows: core craft controls cost and schedule, driving outsized margin lift with industry-average civil contractor EBITDA around 6–10% in 2024. Demand remains steady across infrastructure, commercial and industrial sectors, supporting consistent backlog and utilization near 80–85%. With heavy equipment capex already depreciated and crews seasoned, incremental utilization squeezes yield and converts steady revenue into cash flow.

Facility renewal and small capital programs

Facility renewal and small capital programs at Walsh function as cash cows: on‑call work, task orders and light renovation produce steady, repeatable revenue with low sales burn and quick turns, keeping mobilization times short and execution predictable. Backlog cycles smoothly with minimal bid risk, providing reliable margin visibility and acting as a strong working capital generator through rapid billing and collections.

- On‑call/task orders: steady demand, rapid deployment

- Light renovation: quick revenue recognition, low capex

- Low marketing burn: high ROI on bids

- Backlog stability: minimal risk, predictable cash flow

- Working capital: fast invoicing, strong liquidity

Operations support and closeout services

Operations support and closeout services—commissioning, turnover documentation, client training and warranty management—are Walsh Group cash cows: routine, margin‑friendly and highly scalable, with industry closeout gross margins typically in the low double digits in 2024 and attachment rates exceeding 70% on core projects.

- commissioning

- turnover docs

- training

- warranty

- standardize & bundle to protect margins

- high attachment rate → steady cash flow

Cash-cow services: interiors, CMAR & self-perform civil — standardize playbooks, retain crews

Walsh cash cows—corporate interiors, CMAR, self‑perform civil, facility renewals and closeout services—generate stable, high‑visibility cash flow with low sales burn and margins supported by repeat work. Backlog utilization ~80–85%, civil EBITDA ~6–10% (2024), and BIL funding ~$550B sustain public demand. Focus: standardize playbooks, retain crews, maximize utilization to convert revenue into cash.

| Metric | 2024 |

|---|---|

| Backlog utilization | 80–85% |

| Civil EBITDA | 6–10% |

| BIL funding | $550B |

| Closeout margins | low double digits |

Full Transparency, Always

Walsh Group BCG Matrix

The file you're previewing is the final Walsh Group BCG Matrix you'll receive after purchase. No watermarks or sample pages—just a fully formatted, ready-to-use strategic report. It’s the exact same document delivered to your inbox for editing, printing, or presenting. Buy once and unlock a professional, analysis-ready asset with no surprises.

Actionable Strategy Starts Here

The Walsh Group BCG Matrix preview gives you a quick read on which products lead, which fund growth, and which may be dragging returns. Ready for the full picture? Purchase the complete BCG Matrix to get quadrant-level placements, data-backed recommendations, and downloadable Word and Excel files so you can act fast and present with confidence.

Stars

Design‑build transportation megaprojects

Design-build transportation megaprojects are Stars for Walsh, capturing a significant share of projects tied to the Bipartisan Infrastructure Law’s $550 billion in new spending; a growing pipeline of highways, bridges and rail boosts market share. Walsh’s integrated design-build chops deliver speed and schedule certainty, winning awards and backlog. These projects consume cash on delivery but create authority, margin and recurring revenue; continued reinvestment turns them into long-term cash machines.

Water and wastewater treatment programs

Urban growth and 2024 climate and water-quality mandates keep the water and wastewater segment hot; federal Infrastructure Law directed roughly 55 billion for U.S. water infrastructure, sustaining project pipelines. Walsh’s proven complex-plant delivery and commissioning give a competitive edge on high-capex, high-technical-risk builds. If Walsh sustains share, these plants convert into annuity-like long-term service and O&M revenue streams.

Aviation terminals and airfield upgrades

With IATA reporting 2023 RPKs at about 94% of 2019 levels and 2024 traffic near full recovery, demand fuels terminal expansion while FAA Airport Improvement Program apportionment (~$3.35B in 2024) and stable PFC cap ($4.50) underwrite projects. Walsh’s strength in large, phased live‑environment builds requires heavy upfront coordination and cash draw but yields outsized brand lift. Hold position and harvest as federal funding normalizes.

Healthcare and higher‑ed complexes

Healthcare and higher-ed complexes are specialty builds with strict codes and tight phasing; Walsh’s CM/GC plus self-perform turns theoretical schedules into realized timelines, cutting punch-list time and change orders. These projects command high visibility, repeat owners, and premium fees when executed well; Dodge Data reported ~6% growth in healthcare and education starts in 2024, so defend the lead.

- Specialty codes, tight phasing

- CM/GC + self-perform = reliable schedules

- High visibility, repeat owners, premium fees

- Market growth ~6% in 2024 — protect position

Alternative delivery and P3 execution

Owners demand risk transfer and single‑throat accountability; Walsh’s end‑to‑end design-build-finance-operate capabilities secure early table positioning. These P3s require substantial capital and top talent, but successful bids reset firm ceilings—public infrastructure funding (IIJA) remains $1.2 trillion commitment since 2021, sustaining 2024 pipelines.

- Risk transfer

- Early entry

- High capital/talent

- Ceiling reset

- Invest where pipeline strong

Design-build surge: transport, water, airports, healthcare drive 2024 pipelines

Walsh Stars: design‑build transportation, water, airports and healthcare show strong 2024 pipelines—IIJA/Bipartisan Infrastructure Law ~$1.2T since 2021 with $550B new spending; US water ~$55B; FAA AIP ~$3.35B (2024); healthcare/edu starts +6% (2024). These high-capex segments drive margin, backlog and annuity potential.

| Segment | 2024 Cue | Impact |

|---|---|---|

| Transport | $550B IIJA new | Backlog, margin |

| Water | $55B | O&M annuities |

| Airports | AIP $3.35B | Phased terminals |

| Healthcare | +6% starts | Premium fees |

What is included in the product

Comprehensive BCG Matrix for Walsh Group, identifying Stars, Cash Cows, Question Marks and Dogs with clear strategic actions.

One-page Walsh BCG Matrix placing each unit in a quadrant to remove clutter and speed C-level decisions

Cash Cows

General contracting for mature building markets

Corporate interiors, K‑12 and municipal building work—anchored by Walsh Group’s Chicago base—deliver steady, predictable cash flows with high share in key geographies; the portfolio sits in low single-digit market growth and stable public budget allocations in 2024. Minimal promotion is needed as long‑standing client relationships drive pipeline; focus is on operational efficiency and margin preservation.

Construction management at‑risk for repeat public clients

Construction management at‑risk secures repeat city, county and agency work by delivering reliable outcomes; with the Bipartisan Infrastructure Law still driving $550 billion in new investment as of 2024, public funding remains stable. The moat is process knowledge over flash; retain teams, standardize playbooks, and milk efficiency through repeatable delivery.

Self‑perform concrete and civil packages

Self-perform concrete and civil packages act as cash cows: core craft controls cost and schedule, driving outsized margin lift with industry-average civil contractor EBITDA around 6–10% in 2024. Demand remains steady across infrastructure, commercial and industrial sectors, supporting consistent backlog and utilization near 80–85%. With heavy equipment capex already depreciated and crews seasoned, incremental utilization squeezes yield and converts steady revenue into cash flow.

Facility renewal and small capital programs

Facility renewal and small capital programs at Walsh function as cash cows: on‑call work, task orders and light renovation produce steady, repeatable revenue with low sales burn and quick turns, keeping mobilization times short and execution predictable. Backlog cycles smoothly with minimal bid risk, providing reliable margin visibility and acting as a strong working capital generator through rapid billing and collections.

- On‑call/task orders: steady demand, rapid deployment

- Light renovation: quick revenue recognition, low capex

- Low marketing burn: high ROI on bids

- Backlog stability: minimal risk, predictable cash flow

- Working capital: fast invoicing, strong liquidity

Operations support and closeout services

Operations support and closeout services—commissioning, turnover documentation, client training and warranty management—are Walsh Group cash cows: routine, margin‑friendly and highly scalable, with industry closeout gross margins typically in the low double digits in 2024 and attachment rates exceeding 70% on core projects.

- commissioning

- turnover docs

- training

- warranty

- standardize & bundle to protect margins

- high attachment rate → steady cash flow

Cash-cow services: interiors, CMAR & self-perform civil — standardize playbooks, retain crews

Walsh cash cows—corporate interiors, CMAR, self‑perform civil, facility renewals and closeout services—generate stable, high‑visibility cash flow with low sales burn and margins supported by repeat work. Backlog utilization ~80–85%, civil EBITDA ~6–10% (2024), and BIL funding ~$550B sustain public demand. Focus: standardize playbooks, retain crews, maximize utilization to convert revenue into cash.

| Metric | 2024 |

|---|---|

| Backlog utilization | 80–85% |

| Civil EBITDA | 6–10% |

| BIL funding | $550B |

| Closeout margins | low double digits |

Full Transparency, Always

Walsh Group BCG Matrix

The file you're previewing is the final Walsh Group BCG Matrix you'll receive after purchase. No watermarks or sample pages—just a fully formatted, ready-to-use strategic report. It’s the exact same document delivered to your inbox for editing, printing, or presenting. Buy once and unlock a professional, analysis-ready asset with no surprises.

Description

Actionable Strategy Starts Here

The Walsh Group BCG Matrix preview gives you a quick read on which products lead, which fund growth, and which may be dragging returns. Ready for the full picture? Purchase the complete BCG Matrix to get quadrant-level placements, data-backed recommendations, and downloadable Word and Excel files so you can act fast and present with confidence.

Stars

Design‑build transportation megaprojects

Design-build transportation megaprojects are Stars for Walsh, capturing a significant share of projects tied to the Bipartisan Infrastructure Law’s $550 billion in new spending; a growing pipeline of highways, bridges and rail boosts market share. Walsh’s integrated design-build chops deliver speed and schedule certainty, winning awards and backlog. These projects consume cash on delivery but create authority, margin and recurring revenue; continued reinvestment turns them into long-term cash machines.

Water and wastewater treatment programs

Urban growth and 2024 climate and water-quality mandates keep the water and wastewater segment hot; federal Infrastructure Law directed roughly 55 billion for U.S. water infrastructure, sustaining project pipelines. Walsh’s proven complex-plant delivery and commissioning give a competitive edge on high-capex, high-technical-risk builds. If Walsh sustains share, these plants convert into annuity-like long-term service and O&M revenue streams.

Aviation terminals and airfield upgrades

With IATA reporting 2023 RPKs at about 94% of 2019 levels and 2024 traffic near full recovery, demand fuels terminal expansion while FAA Airport Improvement Program apportionment (~$3.35B in 2024) and stable PFC cap ($4.50) underwrite projects. Walsh’s strength in large, phased live‑environment builds requires heavy upfront coordination and cash draw but yields outsized brand lift. Hold position and harvest as federal funding normalizes.

Healthcare and higher‑ed complexes

Healthcare and higher-ed complexes are specialty builds with strict codes and tight phasing; Walsh’s CM/GC plus self-perform turns theoretical schedules into realized timelines, cutting punch-list time and change orders. These projects command high visibility, repeat owners, and premium fees when executed well; Dodge Data reported ~6% growth in healthcare and education starts in 2024, so defend the lead.

- Specialty codes, tight phasing

- CM/GC + self-perform = reliable schedules

- High visibility, repeat owners, premium fees

- Market growth ~6% in 2024 — protect position

Alternative delivery and P3 execution

Owners demand risk transfer and single‑throat accountability; Walsh’s end‑to‑end design-build-finance-operate capabilities secure early table positioning. These P3s require substantial capital and top talent, but successful bids reset firm ceilings—public infrastructure funding (IIJA) remains $1.2 trillion commitment since 2021, sustaining 2024 pipelines.

- Risk transfer

- Early entry

- High capital/talent

- Ceiling reset

- Invest where pipeline strong

Design-build surge: transport, water, airports, healthcare drive 2024 pipelines

Walsh Stars: design‑build transportation, water, airports and healthcare show strong 2024 pipelines—IIJA/Bipartisan Infrastructure Law ~$1.2T since 2021 with $550B new spending; US water ~$55B; FAA AIP ~$3.35B (2024); healthcare/edu starts +6% (2024). These high-capex segments drive margin, backlog and annuity potential.

| Segment | 2024 Cue | Impact |

|---|---|---|

| Transport | $550B IIJA new | Backlog, margin |

| Water | $55B | O&M annuities |

| Airports | AIP $3.35B | Phased terminals |

| Healthcare | +6% starts | Premium fees |

What is included in the product

Comprehensive BCG Matrix for Walsh Group, identifying Stars, Cash Cows, Question Marks and Dogs with clear strategic actions.

One-page Walsh BCG Matrix placing each unit in a quadrant to remove clutter and speed C-level decisions

Cash Cows

General contracting for mature building markets

Corporate interiors, K‑12 and municipal building work—anchored by Walsh Group’s Chicago base—deliver steady, predictable cash flows with high share in key geographies; the portfolio sits in low single-digit market growth and stable public budget allocations in 2024. Minimal promotion is needed as long‑standing client relationships drive pipeline; focus is on operational efficiency and margin preservation.

Construction management at‑risk for repeat public clients

Construction management at‑risk secures repeat city, county and agency work by delivering reliable outcomes; with the Bipartisan Infrastructure Law still driving $550 billion in new investment as of 2024, public funding remains stable. The moat is process knowledge over flash; retain teams, standardize playbooks, and milk efficiency through repeatable delivery.

Self‑perform concrete and civil packages

Self-perform concrete and civil packages act as cash cows: core craft controls cost and schedule, driving outsized margin lift with industry-average civil contractor EBITDA around 6–10% in 2024. Demand remains steady across infrastructure, commercial and industrial sectors, supporting consistent backlog and utilization near 80–85%. With heavy equipment capex already depreciated and crews seasoned, incremental utilization squeezes yield and converts steady revenue into cash flow.

Facility renewal and small capital programs

Facility renewal and small capital programs at Walsh function as cash cows: on‑call work, task orders and light renovation produce steady, repeatable revenue with low sales burn and quick turns, keeping mobilization times short and execution predictable. Backlog cycles smoothly with minimal bid risk, providing reliable margin visibility and acting as a strong working capital generator through rapid billing and collections.

- On‑call/task orders: steady demand, rapid deployment

- Light renovation: quick revenue recognition, low capex

- Low marketing burn: high ROI on bids

- Backlog stability: minimal risk, predictable cash flow

- Working capital: fast invoicing, strong liquidity

Operations support and closeout services

Operations support and closeout services—commissioning, turnover documentation, client training and warranty management—are Walsh Group cash cows: routine, margin‑friendly and highly scalable, with industry closeout gross margins typically in the low double digits in 2024 and attachment rates exceeding 70% on core projects.

- commissioning

- turnover docs

- training

- warranty

- standardize & bundle to protect margins

- high attachment rate → steady cash flow

Cash-cow services: interiors, CMAR & self-perform civil — standardize playbooks, retain crews

Walsh cash cows—corporate interiors, CMAR, self‑perform civil, facility renewals and closeout services—generate stable, high‑visibility cash flow with low sales burn and margins supported by repeat work. Backlog utilization ~80–85%, civil EBITDA ~6–10% (2024), and BIL funding ~$550B sustain public demand. Focus: standardize playbooks, retain crews, maximize utilization to convert revenue into cash.

| Metric | 2024 |

|---|---|

| Backlog utilization | 80–85% |

| Civil EBITDA | 6–10% |

| BIL funding | $550B |

| Closeout margins | low double digits |

Full Transparency, Always

Walsh Group BCG Matrix

The file you're previewing is the final Walsh Group BCG Matrix you'll receive after purchase. No watermarks or sample pages—just a fully formatted, ready-to-use strategic report. It’s the exact same document delivered to your inbox for editing, printing, or presenting. Buy once and unlock a professional, analysis-ready asset with no surprises.