Washington Trust Porter's Five Forces Analysis

A Must-Have Tool for Decision-Makers

Washington Trust faces moderate buyer power, evolving digital threats, and concentrated competitor pressure that shape its margin and growth outlook; this snapshot highlights key tensions but omits force-by-force ratings and visuals. Unlock the full Porter's Five Forces Analysis for a consultant-grade, data-driven breakdown, Excel/Word deliverables, and actionable strategy recommendations to guide investment or strategic decisions.

Suppliers Bargaining Power

Concentrated core tech vendors

Washington Trust depends on a small set of core banking and payments providers for mission-critical systems, notably the three dominant vendors FIS, Fiserv and Jack Henry which together held over 60% of the U.S. core market in 2024. Vendor concentration raises switching costs and strengthens supplier leverage on pricing and contract terms. Integration complexity and heightened regulatory scrutiny further lock in these relationships. Periodic platform renewals are key inflection points for cost or capability concessions.

Wholesale funding and capital markets

In periods of deposit pressure Washington Trust may tap FHLB advances or brokered CDs, where pricing rests with market conditions and counterparties. With the federal funds target at 5.25–5.50% in 2024, wholesale yields rose, elevating funding costs and shortening duration. Covenants and collateral on FHLB lines can add constraints. Diversifying stable retail deposits reduces reliance on these suppliers.

Payment networks and rails

Card networks and ACH/real-time operators set interchange and routing rules that banks must absorb or pass on; merchant fees typically run 1.5–3.5% per transaction and interchange makes up the bulk of that. Limited alternatives and interoperability needs (FedNow reached roughly 1,000 participants by 2024) give networks meaningful leverage. Pricing shifts can compress interchange margins or raise operating costs. Larger banks secure volume-based discounts regional peers cannot match.

Talent and specialized services

Skilled lenders, wealth advisors, compliance and cybersecurity partners are critical inputs for Washington Trust; in 2024 global cybersecurity spend topped $200B, underscoring vendor value and cost pressure. Tight regional labor markets and regulatory complexity pushed financial-sector compensation up roughly 5% in 2024, increasing supplier bargaining power. Retention, non-competes and client portability risk amplify costs, while insourcing core capabilities can reduce third-party dependence.

- Skilled hires: limited supply

- Compliance/cyber: high spend

- Compensation: ~+5% (2024)

- Retention/non-compete: affects client portability

- Mitigation: build in-house capabilities

Data, credit, and insurance carriers

Access to credit bureaus, risk models, and insurance underwriters is essential for delivering Washington Trust products and controlling loss; the three major US credit bureaus (Equifax, Experian, TransUnion) account for roughly 90% of consumer credit data, concentrating supplier power. Dominant data suppliers enforce standardized pricing and license terms, and shifts in data access or carrier appetite can quickly alter product economics. Multi-sourcing and proprietary analytics materially blunt this leverage.

- Data concentration: three bureaus ~90%

- Standardized licensing raises switching costs

- Policy/carrier changes → immediate margin impact

- Proprietary models/multi-sourcing reduce supplier risk

Concentrated vendor power, rising funding and merchant fee pressure squeeze regional banks

Washington Trust faces concentrated tech/data suppliers (FIS/Fiserv/Jack Henry >60% core market, credit bureaus ~90%), raising switching costs. Wholesale funding tightened with fed funds 5.25–5.50% (2024), boosting FHLB/brokered funding costs. Card networks set 1.5–3.5% merchant fees; labor/cyber spend rose ~5% (2024), increasing vendor leverage.

| Supplier | 2024 stat | Impact |

|---|---|---|

| Core vendors | >60% market | High switching cost |

| Credit bureaus | ~90% | Pricing power |

| Card networks | 1.5–3.5% | Fee pressure |

What is included in the product

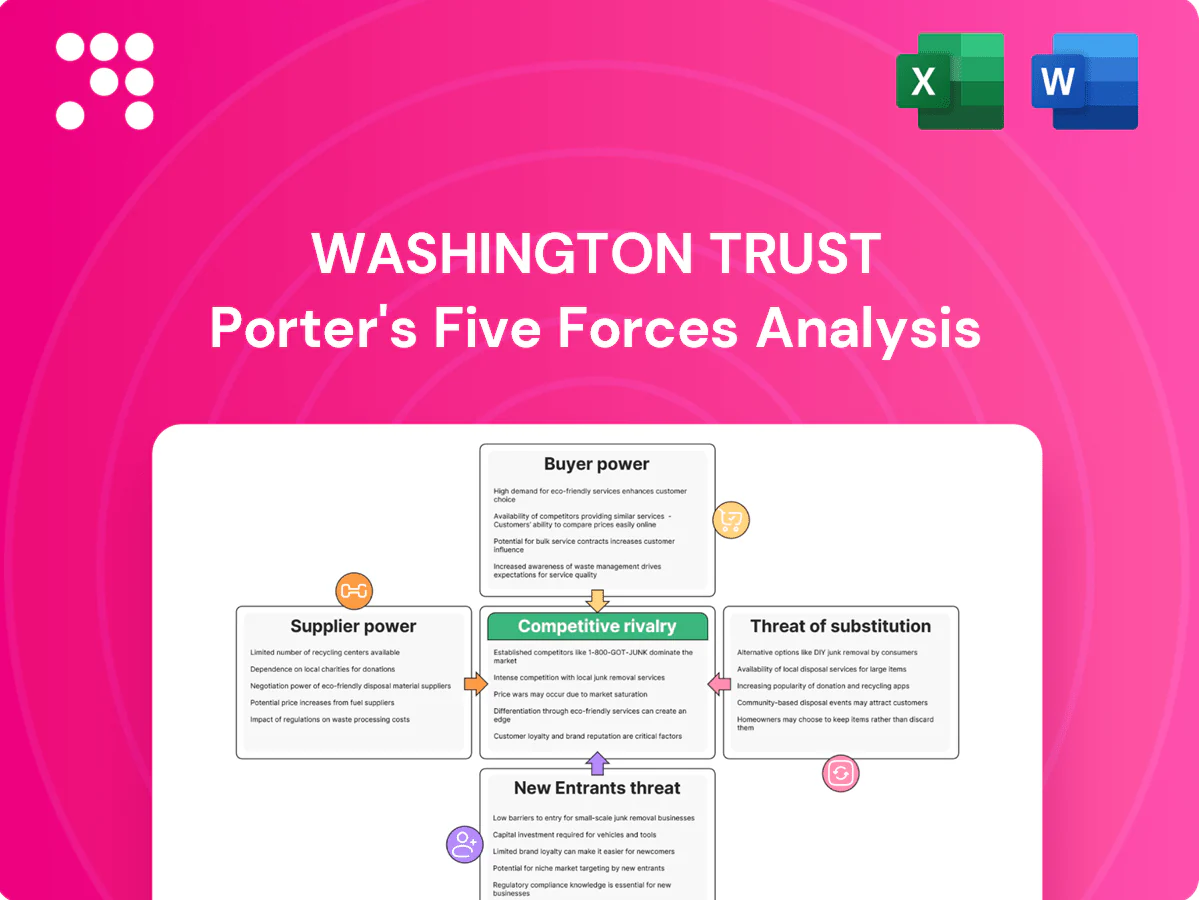

Comprehensive Porter's Five Forces for Washington Trust, revealing competitive intensity, buyer/supplier leverage, barriers deterring new entrants, and substitute threats to inform pricing, profitability, and strategic positioning.

A concise, one-sheet Porter's Five Forces for Washington Trust that highlights competitive pressure points and relief strategies—ready to drop into board decks or stakeholder briefs.

Customers Bargaining Power

Rate-sensitive depositors

Rate-sensitive depositors have rising leverage as digital channels and instant transfers (Zelle ~175M users in 2024) let consumers and businesses switch deposits quickly. Online banks and money market funds offering APYs of roughly 4–5% in 2024 heighten rate pressure on Washington Trust. Relationship benefits and branches still reduce churn for some customers. Tiered pricing and loyalty programs help retain balances.

Commercial borrowers and treasury clients

Middle-market commercial borrowers and treasury clients exert strong bargaining power by shopping loans and cash management across multiple banks, negotiating spreads, fees, covenants, and service levels to extract better terms.

Bundling treasury and lending increases client stickiness but also invites competitive bids when pricing or technology lags.

Faster decisioning and deep industry expertise reduce price sensitivity and help Washington Trust defend margins.

Mortgage customers

Mortgage origination is highly price-transparent; with the 30-year fixed averaging about 6.8% in 2024 and origination volumes roughly 40% below the 2020 peak, borrowers frequently shop brokers and press for lower rates or lender credits as pipelines slow. Secondary market execution and investor overlays cap discounting, while faster processing and local underwriting allow Washington Trust to sustain modest premiums of 10–25 basis points.

Wealth management and HNW clients

- Fee sensitivity

- Portability = leverage

- Trust services = lock-in

- Reporting & UX = differentiation

Insurance and fee-based services

Customers increasingly solicit multiple online quotes, compressing margins—by 2024 about 64% of US consumers used online comparison tools for insurance, elevating buyer leverage and commoditization of fee-based products.

Washington Trust can temper churn via cross-sell inside banking relationships; value-added advice and proactive policy servicing sustain retention despite price pressure.

- Online quote usage ~64% (2024)

- Commoditization raises buyer power

- Cross-sell reduces churn

- Advice and servicing support retention

Digital switching and price transparency push banks to win via bundling, speed and underwriting

Customers wield rising price leverage via instant digital switching and high-rate alternatives; commercial clients and affluent households negotiate spreads and fees aggressively, while mortgages and fee products face strong price transparency. Washington Trust offsets pressure with bundling, faster decisioning, local underwriting and trust services.

| Metric | 2024 | Impact |

|---|---|---|

| Zelle users | 175M | faster switching |

| 30y fixed | 6.8% | mortgage shopping |

| MMF APY | 4–5% | deposit pressure |

| Online quotes | 64% | fee compression |

What You See Is What You Get

Washington Trust Porter's Five Forces Analysis

This preview displays the Washington Trust Porter's Five Forces Analysis and is the exact document you'll receive after purchase—fully formatted and ready to use. No placeholders, mockups, or samples are shown here. Once you buy, you get instant access to this same file.

A Must-Have Tool for Decision-Makers

Washington Trust faces moderate buyer power, evolving digital threats, and concentrated competitor pressure that shape its margin and growth outlook; this snapshot highlights key tensions but omits force-by-force ratings and visuals. Unlock the full Porter's Five Forces Analysis for a consultant-grade, data-driven breakdown, Excel/Word deliverables, and actionable strategy recommendations to guide investment or strategic decisions.

Suppliers Bargaining Power

Concentrated core tech vendors

Washington Trust depends on a small set of core banking and payments providers for mission-critical systems, notably the three dominant vendors FIS, Fiserv and Jack Henry which together held over 60% of the U.S. core market in 2024. Vendor concentration raises switching costs and strengthens supplier leverage on pricing and contract terms. Integration complexity and heightened regulatory scrutiny further lock in these relationships. Periodic platform renewals are key inflection points for cost or capability concessions.

Wholesale funding and capital markets

In periods of deposit pressure Washington Trust may tap FHLB advances or brokered CDs, where pricing rests with market conditions and counterparties. With the federal funds target at 5.25–5.50% in 2024, wholesale yields rose, elevating funding costs and shortening duration. Covenants and collateral on FHLB lines can add constraints. Diversifying stable retail deposits reduces reliance on these suppliers.

Payment networks and rails

Card networks and ACH/real-time operators set interchange and routing rules that banks must absorb or pass on; merchant fees typically run 1.5–3.5% per transaction and interchange makes up the bulk of that. Limited alternatives and interoperability needs (FedNow reached roughly 1,000 participants by 2024) give networks meaningful leverage. Pricing shifts can compress interchange margins or raise operating costs. Larger banks secure volume-based discounts regional peers cannot match.

Talent and specialized services

Skilled lenders, wealth advisors, compliance and cybersecurity partners are critical inputs for Washington Trust; in 2024 global cybersecurity spend topped $200B, underscoring vendor value and cost pressure. Tight regional labor markets and regulatory complexity pushed financial-sector compensation up roughly 5% in 2024, increasing supplier bargaining power. Retention, non-competes and client portability risk amplify costs, while insourcing core capabilities can reduce third-party dependence.

- Skilled hires: limited supply

- Compliance/cyber: high spend

- Compensation: ~+5% (2024)

- Retention/non-compete: affects client portability

- Mitigation: build in-house capabilities

Data, credit, and insurance carriers

Access to credit bureaus, risk models, and insurance underwriters is essential for delivering Washington Trust products and controlling loss; the three major US credit bureaus (Equifax, Experian, TransUnion) account for roughly 90% of consumer credit data, concentrating supplier power. Dominant data suppliers enforce standardized pricing and license terms, and shifts in data access or carrier appetite can quickly alter product economics. Multi-sourcing and proprietary analytics materially blunt this leverage.

- Data concentration: three bureaus ~90%

- Standardized licensing raises switching costs

- Policy/carrier changes → immediate margin impact

- Proprietary models/multi-sourcing reduce supplier risk

Concentrated vendor power, rising funding and merchant fee pressure squeeze regional banks

Washington Trust faces concentrated tech/data suppliers (FIS/Fiserv/Jack Henry >60% core market, credit bureaus ~90%), raising switching costs. Wholesale funding tightened with fed funds 5.25–5.50% (2024), boosting FHLB/brokered funding costs. Card networks set 1.5–3.5% merchant fees; labor/cyber spend rose ~5% (2024), increasing vendor leverage.

| Supplier | 2024 stat | Impact |

|---|---|---|

| Core vendors | >60% market | High switching cost |

| Credit bureaus | ~90% | Pricing power |

| Card networks | 1.5–3.5% | Fee pressure |

What is included in the product

Comprehensive Porter's Five Forces for Washington Trust, revealing competitive intensity, buyer/supplier leverage, barriers deterring new entrants, and substitute threats to inform pricing, profitability, and strategic positioning.

A concise, one-sheet Porter's Five Forces for Washington Trust that highlights competitive pressure points and relief strategies—ready to drop into board decks or stakeholder briefs.

Customers Bargaining Power

Rate-sensitive depositors

Rate-sensitive depositors have rising leverage as digital channels and instant transfers (Zelle ~175M users in 2024) let consumers and businesses switch deposits quickly. Online banks and money market funds offering APYs of roughly 4–5% in 2024 heighten rate pressure on Washington Trust. Relationship benefits and branches still reduce churn for some customers. Tiered pricing and loyalty programs help retain balances.

Commercial borrowers and treasury clients

Middle-market commercial borrowers and treasury clients exert strong bargaining power by shopping loans and cash management across multiple banks, negotiating spreads, fees, covenants, and service levels to extract better terms.

Bundling treasury and lending increases client stickiness but also invites competitive bids when pricing or technology lags.

Faster decisioning and deep industry expertise reduce price sensitivity and help Washington Trust defend margins.

Mortgage customers

Mortgage origination is highly price-transparent; with the 30-year fixed averaging about 6.8% in 2024 and origination volumes roughly 40% below the 2020 peak, borrowers frequently shop brokers and press for lower rates or lender credits as pipelines slow. Secondary market execution and investor overlays cap discounting, while faster processing and local underwriting allow Washington Trust to sustain modest premiums of 10–25 basis points.

Wealth management and HNW clients

- Fee sensitivity

- Portability = leverage

- Trust services = lock-in

- Reporting & UX = differentiation

Insurance and fee-based services

Customers increasingly solicit multiple online quotes, compressing margins—by 2024 about 64% of US consumers used online comparison tools for insurance, elevating buyer leverage and commoditization of fee-based products.

Washington Trust can temper churn via cross-sell inside banking relationships; value-added advice and proactive policy servicing sustain retention despite price pressure.

- Online quote usage ~64% (2024)

- Commoditization raises buyer power

- Cross-sell reduces churn

- Advice and servicing support retention

Digital switching and price transparency push banks to win via bundling, speed and underwriting

Customers wield rising price leverage via instant digital switching and high-rate alternatives; commercial clients and affluent households negotiate spreads and fees aggressively, while mortgages and fee products face strong price transparency. Washington Trust offsets pressure with bundling, faster decisioning, local underwriting and trust services.

| Metric | 2024 | Impact |

|---|---|---|

| Zelle users | 175M | faster switching |

| 30y fixed | 6.8% | mortgage shopping |

| MMF APY | 4–5% | deposit pressure |

| Online quotes | 64% | fee compression |

What You See Is What You Get

Washington Trust Porter's Five Forces Analysis

This preview displays the Washington Trust Porter's Five Forces Analysis and is the exact document you'll receive after purchase—fully formatted and ready to use. No placeholders, mockups, or samples are shown here. Once you buy, you get instant access to this same file.

Original: $10.00

-65%$10.00

$3.50Description

A Must-Have Tool for Decision-Makers

Washington Trust faces moderate buyer power, evolving digital threats, and concentrated competitor pressure that shape its margin and growth outlook; this snapshot highlights key tensions but omits force-by-force ratings and visuals. Unlock the full Porter's Five Forces Analysis for a consultant-grade, data-driven breakdown, Excel/Word deliverables, and actionable strategy recommendations to guide investment or strategic decisions.

Suppliers Bargaining Power

Concentrated core tech vendors

Washington Trust depends on a small set of core banking and payments providers for mission-critical systems, notably the three dominant vendors FIS, Fiserv and Jack Henry which together held over 60% of the U.S. core market in 2024. Vendor concentration raises switching costs and strengthens supplier leverage on pricing and contract terms. Integration complexity and heightened regulatory scrutiny further lock in these relationships. Periodic platform renewals are key inflection points for cost or capability concessions.

Wholesale funding and capital markets

In periods of deposit pressure Washington Trust may tap FHLB advances or brokered CDs, where pricing rests with market conditions and counterparties. With the federal funds target at 5.25–5.50% in 2024, wholesale yields rose, elevating funding costs and shortening duration. Covenants and collateral on FHLB lines can add constraints. Diversifying stable retail deposits reduces reliance on these suppliers.

Payment networks and rails

Card networks and ACH/real-time operators set interchange and routing rules that banks must absorb or pass on; merchant fees typically run 1.5–3.5% per transaction and interchange makes up the bulk of that. Limited alternatives and interoperability needs (FedNow reached roughly 1,000 participants by 2024) give networks meaningful leverage. Pricing shifts can compress interchange margins or raise operating costs. Larger banks secure volume-based discounts regional peers cannot match.

Talent and specialized services

Skilled lenders, wealth advisors, compliance and cybersecurity partners are critical inputs for Washington Trust; in 2024 global cybersecurity spend topped $200B, underscoring vendor value and cost pressure. Tight regional labor markets and regulatory complexity pushed financial-sector compensation up roughly 5% in 2024, increasing supplier bargaining power. Retention, non-competes and client portability risk amplify costs, while insourcing core capabilities can reduce third-party dependence.

- Skilled hires: limited supply

- Compliance/cyber: high spend

- Compensation: ~+5% (2024)

- Retention/non-compete: affects client portability

- Mitigation: build in-house capabilities

Data, credit, and insurance carriers

Access to credit bureaus, risk models, and insurance underwriters is essential for delivering Washington Trust products and controlling loss; the three major US credit bureaus (Equifax, Experian, TransUnion) account for roughly 90% of consumer credit data, concentrating supplier power. Dominant data suppliers enforce standardized pricing and license terms, and shifts in data access or carrier appetite can quickly alter product economics. Multi-sourcing and proprietary analytics materially blunt this leverage.

- Data concentration: three bureaus ~90%

- Standardized licensing raises switching costs

- Policy/carrier changes → immediate margin impact

- Proprietary models/multi-sourcing reduce supplier risk

Concentrated vendor power, rising funding and merchant fee pressure squeeze regional banks

Washington Trust faces concentrated tech/data suppliers (FIS/Fiserv/Jack Henry >60% core market, credit bureaus ~90%), raising switching costs. Wholesale funding tightened with fed funds 5.25–5.50% (2024), boosting FHLB/brokered funding costs. Card networks set 1.5–3.5% merchant fees; labor/cyber spend rose ~5% (2024), increasing vendor leverage.

| Supplier | 2024 stat | Impact |

|---|---|---|

| Core vendors | >60% market | High switching cost |

| Credit bureaus | ~90% | Pricing power |

| Card networks | 1.5–3.5% | Fee pressure |

What is included in the product

Comprehensive Porter's Five Forces for Washington Trust, revealing competitive intensity, buyer/supplier leverage, barriers deterring new entrants, and substitute threats to inform pricing, profitability, and strategic positioning.

A concise, one-sheet Porter's Five Forces for Washington Trust that highlights competitive pressure points and relief strategies—ready to drop into board decks or stakeholder briefs.

Customers Bargaining Power

Rate-sensitive depositors

Rate-sensitive depositors have rising leverage as digital channels and instant transfers (Zelle ~175M users in 2024) let consumers and businesses switch deposits quickly. Online banks and money market funds offering APYs of roughly 4–5% in 2024 heighten rate pressure on Washington Trust. Relationship benefits and branches still reduce churn for some customers. Tiered pricing and loyalty programs help retain balances.

Commercial borrowers and treasury clients

Middle-market commercial borrowers and treasury clients exert strong bargaining power by shopping loans and cash management across multiple banks, negotiating spreads, fees, covenants, and service levels to extract better terms.

Bundling treasury and lending increases client stickiness but also invites competitive bids when pricing or technology lags.

Faster decisioning and deep industry expertise reduce price sensitivity and help Washington Trust defend margins.

Mortgage customers

Mortgage origination is highly price-transparent; with the 30-year fixed averaging about 6.8% in 2024 and origination volumes roughly 40% below the 2020 peak, borrowers frequently shop brokers and press for lower rates or lender credits as pipelines slow. Secondary market execution and investor overlays cap discounting, while faster processing and local underwriting allow Washington Trust to sustain modest premiums of 10–25 basis points.

Wealth management and HNW clients

- Fee sensitivity

- Portability = leverage

- Trust services = lock-in

- Reporting & UX = differentiation

Insurance and fee-based services

Customers increasingly solicit multiple online quotes, compressing margins—by 2024 about 64% of US consumers used online comparison tools for insurance, elevating buyer leverage and commoditization of fee-based products.

Washington Trust can temper churn via cross-sell inside banking relationships; value-added advice and proactive policy servicing sustain retention despite price pressure.

- Online quote usage ~64% (2024)

- Commoditization raises buyer power

- Cross-sell reduces churn

- Advice and servicing support retention

Digital switching and price transparency push banks to win via bundling, speed and underwriting

Customers wield rising price leverage via instant digital switching and high-rate alternatives; commercial clients and affluent households negotiate spreads and fees aggressively, while mortgages and fee products face strong price transparency. Washington Trust offsets pressure with bundling, faster decisioning, local underwriting and trust services.

| Metric | 2024 | Impact |

|---|---|---|

| Zelle users | 175M | faster switching |

| 30y fixed | 6.8% | mortgage shopping |

| MMF APY | 4–5% | deposit pressure |

| Online quotes | 64% | fee compression |

What You See Is What You Get

Washington Trust Porter's Five Forces Analysis

This preview displays the Washington Trust Porter's Five Forces Analysis and is the exact document you'll receive after purchase—fully formatted and ready to use. No placeholders, mockups, or samples are shown here. Once you buy, you get instant access to this same file.