Waterdrop Porter's Five Forces Analysis

Don't Miss the Bigger Picture

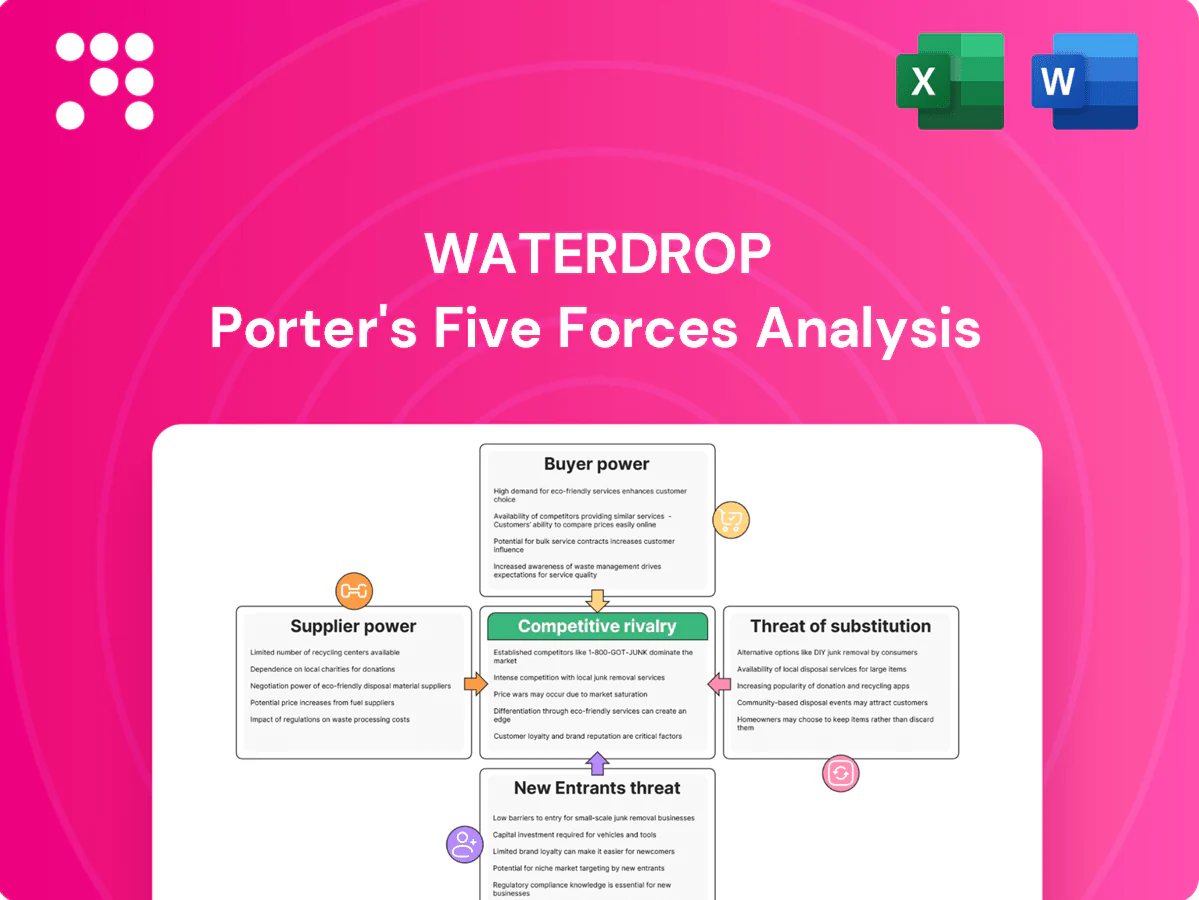

Waterdrop’s Porter's Five Forces highlights intense rivalry, moderate supplier power, rising buyer sophistication, looming substitute threats, and barriers that shape growth and margins. This snapshot frames strategic risks and opportunities for investors and managers. Unlock the full Porter's Five Forces Analysis to explore Waterdrop’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentrated insurers and reinsurers

In 2024 Waterdrop depends on a concentrated group of state-owned and top private insurers for health and life products and underwriting capacity, giving those partners leverage over commission rates, product exclusivity and data access.

Platform gatekeepers and traffic sources

User acquisition for Waterdrop depends heavily on super-app ecosystems and ad platforms (WeChat, Alipay, Douyin, Baidu), which together captured over 70% of China mobile ad spend in 2024; these concentrated channels can raise ad prices, tweak algorithms, or limit insurance promos, driving CAC volatility and giving suppliers negotiation leverage, while diversification into organic channels only partially offsets this power.

Payments and fintech infrastructure

Alipay and WeChat Pay together control over 90% of China’s mobile payments (Alipay ≈54%, WeChat Pay ≈39% in 2024), setting fees, platform rules and user flows. Policy or fee shifts can sharply affect Waterdrop’s conversion, refunds and crowdfunding disbursements. Their leverage lets them extract fees or impose compliance burdens. Switching costs are high due to entrenched user habits and network effects.

Medical data, TPAs, and provider networks

Claims verification, health data feeds and TPA services for Waterdrop depend on specialized vendors and hospital networks; high-quality providers are limited and bound by China’s PIPL/Data Security Law enforcement in 2024, raising switching costs and enabling vendors to price-discriminate or favor larger partners while complex integration locks in customers.

- Limited providers

- Regulatory compliance (PIPL/Data Security Law 2024)

- High switching costs

- Vendor pricing power

- Integration dependency

Exclusive product and API access

Insurers granting exclusive APIs and co-branded products to preferred channels materially shape conversion and differentiation; exclusive API access can lift channel conversion by an estimated 30-40% in 2024, concentrating product influence with suppliers and tying Waterdrop’s roadmap to partner priorities.

Negotiating stronger SLAs and exclusivity typically demands volume commitments (often quarterly or annual quotas), increasing supplier leverage and raising switching costs; this dynamic heightens supplier bargaining power.

- Exclusive API access: drives 30-40% higher conversion (2024 est.)

- Volume-linked SLAs: quarterly/annual commitments common

- Result: increased supplier leverage over product roadmap

2024: Insurers, super-apps and payment duopoly amplify supplier power over health platforms

In 2024 Waterdrop faces high supplier power: concentrated insurers control underwriting and API access, super-apps (WeChat, Alipay, Douyin, Baidu) drive >70% mobile ad spend and set user acquisition terms, and Alipay+WeChat Pay hold ≈90% mobile payments, raising fees and switching costs; vendor scarcity for TPAs/health data and regulatory data rules (PIPL) further boost supplier leverage.

| Metric | 2024 |

|---|---|

| Super-app ad share | >70% |

| Alipay / WeChat Pay | ≈54% / ≈39% (≈90% total) |

| API conversion lift | 30–40% est. |

What is included in the product

Tailored Porter's Five Forces analysis for Waterdrop that uncovers competitive drivers, supplier and buyer influence, substitutes and disruptive threats, and evaluates entry barriers shaping its pricing and profitability.

Concise Waterdrop Porter's Five Forces one-sheet that instantly clarifies competitive, supplier, buyer and regulatory pressures—ideal for quick decision-making and boardroom use.

Customers Bargaining Power

Price-sensitive, informed consumers

Users can instantly compare premiums, coverage, and riders across platforms, with 60% of insurance shoppers using online comparison tools in 2024, increasing transparency and deal-seeking. Low switching costs and frequent promotions compress platform commission margins and raise price pressure on agents. Transparent reviews and social sharing amplify negative network effects for poor offers. Together, these trends materially raise buyer bargaining power in Waterdrop’s marketplace.

Trust and claims experience expectations

Policyholders demand seamless claims and empathetic service, and poor experiences drive churn; negative word-of-mouth on social channels and press accelerates reputational damage and tightens service SLAs. Buyers also press for faster underwriting and clearer exclusions, forcing Waterdrop to invest heavily in customer service and claims tech, which compresses margins.

Crowdfunding campaigners’ urgency

Patients seeking medical funds demand fast approval, high visibility, and low fees. They can migrate to alternative platforms or charitable foundations if terms seem unfavorable. Platform choice hinges on transparency and fraud controls; in 2024 US leaders like GoFundMe use 0% platform fees but payment processing ~2.9% + $0.30. Situational leverage raises expectations on speed and outreach.

Multi-homing across super-apps

Users routinely multi-home across WeChat (~1.3 billion MAU in 2024 per Tencent) and Alipay (>1 billion users in 2024 per Ant Group) mini-programs plus competitor apps, eroding lock-in and amplifying customer bargaining power. Loyalty points give limited stickiness versus super-app convenience, forcing Waterdrop to continuously optimize funnels and conversion metrics to retain users.

- Multi-homing: increases choice, reduces switching costs

- Scale: super-app reach >1B users

- Retention: loyalty weaker than ecosystem

- Action: constant funnel/device optimization

Enterprise and affinity partners

Enterprise and affinity partners—Corporate HR, communities, and KOLs—can steer large cohorts toward specific Waterdrop products, securing discounted group rates or higher revenue shares; in 2024 these channels reportedly drove about 45% of new policy volumes, magnifying partner bargaining power and making losing one large partner disproportionately hit volumes.

- Concentration: top accounts drive ~45% of new volumes (2024)

- Leverage: group discounts/higher revenue shares common

- Risk: single-partner loss causes outsized volume decline

60% compare online; 45% partner share erodes pricing

Buyers use online comparison (60% in 2024), lowering price tolerance and boosting deal-seeking. Low switching costs, social reviews and multi-homing on WeChat (1.3B MAU) and Alipay (>1B) erode lock-in. Enterprise partners supplied ~45% of new policies in 2024, creating concentrated bargaining power. Fast claims, clear exclusions and low fees (eg GoFundMe 0% platform + ~2.9%+0.30) drive expectations.

| Metric | 2024 | Implication |

|---|---|---|

| Comparison use | 60% | Higher price pressure |

| WeChat MAU | 1.3B | Multi-homing |

| Alipay users | >1B | Low lock-in |

| Partner share | ~45% | Concentrated leverage |

Full Version Awaits

Waterdrop Porter's Five Forces Analysis

This preview displays the exact Waterdrop Porter's Five Forces analysis you'll receive after purchase—no placeholders or mockups. The document is the final, fully formatted file, ready for immediate download and use the moment you buy. What you see here is precisely the deliverable you'll get, complete and professional.

Don't Miss the Bigger Picture

Waterdrop’s Porter's Five Forces highlights intense rivalry, moderate supplier power, rising buyer sophistication, looming substitute threats, and barriers that shape growth and margins. This snapshot frames strategic risks and opportunities for investors and managers. Unlock the full Porter's Five Forces Analysis to explore Waterdrop’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentrated insurers and reinsurers

In 2024 Waterdrop depends on a concentrated group of state-owned and top private insurers for health and life products and underwriting capacity, giving those partners leverage over commission rates, product exclusivity and data access.

Platform gatekeepers and traffic sources

User acquisition for Waterdrop depends heavily on super-app ecosystems and ad platforms (WeChat, Alipay, Douyin, Baidu), which together captured over 70% of China mobile ad spend in 2024; these concentrated channels can raise ad prices, tweak algorithms, or limit insurance promos, driving CAC volatility and giving suppliers negotiation leverage, while diversification into organic channels only partially offsets this power.

Payments and fintech infrastructure

Alipay and WeChat Pay together control over 90% of China’s mobile payments (Alipay ≈54%, WeChat Pay ≈39% in 2024), setting fees, platform rules and user flows. Policy or fee shifts can sharply affect Waterdrop’s conversion, refunds and crowdfunding disbursements. Their leverage lets them extract fees or impose compliance burdens. Switching costs are high due to entrenched user habits and network effects.

Medical data, TPAs, and provider networks

Claims verification, health data feeds and TPA services for Waterdrop depend on specialized vendors and hospital networks; high-quality providers are limited and bound by China’s PIPL/Data Security Law enforcement in 2024, raising switching costs and enabling vendors to price-discriminate or favor larger partners while complex integration locks in customers.

- Limited providers

- Regulatory compliance (PIPL/Data Security Law 2024)

- High switching costs

- Vendor pricing power

- Integration dependency

Exclusive product and API access

Insurers granting exclusive APIs and co-branded products to preferred channels materially shape conversion and differentiation; exclusive API access can lift channel conversion by an estimated 30-40% in 2024, concentrating product influence with suppliers and tying Waterdrop’s roadmap to partner priorities.

Negotiating stronger SLAs and exclusivity typically demands volume commitments (often quarterly or annual quotas), increasing supplier leverage and raising switching costs; this dynamic heightens supplier bargaining power.

- Exclusive API access: drives 30-40% higher conversion (2024 est.)

- Volume-linked SLAs: quarterly/annual commitments common

- Result: increased supplier leverage over product roadmap

2024: Insurers, super-apps and payment duopoly amplify supplier power over health platforms

In 2024 Waterdrop faces high supplier power: concentrated insurers control underwriting and API access, super-apps (WeChat, Alipay, Douyin, Baidu) drive >70% mobile ad spend and set user acquisition terms, and Alipay+WeChat Pay hold ≈90% mobile payments, raising fees and switching costs; vendor scarcity for TPAs/health data and regulatory data rules (PIPL) further boost supplier leverage.

| Metric | 2024 |

|---|---|

| Super-app ad share | >70% |

| Alipay / WeChat Pay | ≈54% / ≈39% (≈90% total) |

| API conversion lift | 30–40% est. |

What is included in the product

Tailored Porter's Five Forces analysis for Waterdrop that uncovers competitive drivers, supplier and buyer influence, substitutes and disruptive threats, and evaluates entry barriers shaping its pricing and profitability.

Concise Waterdrop Porter's Five Forces one-sheet that instantly clarifies competitive, supplier, buyer and regulatory pressures—ideal for quick decision-making and boardroom use.

Customers Bargaining Power

Price-sensitive, informed consumers

Users can instantly compare premiums, coverage, and riders across platforms, with 60% of insurance shoppers using online comparison tools in 2024, increasing transparency and deal-seeking. Low switching costs and frequent promotions compress platform commission margins and raise price pressure on agents. Transparent reviews and social sharing amplify negative network effects for poor offers. Together, these trends materially raise buyer bargaining power in Waterdrop’s marketplace.

Trust and claims experience expectations

Policyholders demand seamless claims and empathetic service, and poor experiences drive churn; negative word-of-mouth on social channels and press accelerates reputational damage and tightens service SLAs. Buyers also press for faster underwriting and clearer exclusions, forcing Waterdrop to invest heavily in customer service and claims tech, which compresses margins.

Crowdfunding campaigners’ urgency

Patients seeking medical funds demand fast approval, high visibility, and low fees. They can migrate to alternative platforms or charitable foundations if terms seem unfavorable. Platform choice hinges on transparency and fraud controls; in 2024 US leaders like GoFundMe use 0% platform fees but payment processing ~2.9% + $0.30. Situational leverage raises expectations on speed and outreach.

Multi-homing across super-apps

Users routinely multi-home across WeChat (~1.3 billion MAU in 2024 per Tencent) and Alipay (>1 billion users in 2024 per Ant Group) mini-programs plus competitor apps, eroding lock-in and amplifying customer bargaining power. Loyalty points give limited stickiness versus super-app convenience, forcing Waterdrop to continuously optimize funnels and conversion metrics to retain users.

- Multi-homing: increases choice, reduces switching costs

- Scale: super-app reach >1B users

- Retention: loyalty weaker than ecosystem

- Action: constant funnel/device optimization

Enterprise and affinity partners

Enterprise and affinity partners—Corporate HR, communities, and KOLs—can steer large cohorts toward specific Waterdrop products, securing discounted group rates or higher revenue shares; in 2024 these channels reportedly drove about 45% of new policy volumes, magnifying partner bargaining power and making losing one large partner disproportionately hit volumes.

- Concentration: top accounts drive ~45% of new volumes (2024)

- Leverage: group discounts/higher revenue shares common

- Risk: single-partner loss causes outsized volume decline

60% compare online; 45% partner share erodes pricing

Buyers use online comparison (60% in 2024), lowering price tolerance and boosting deal-seeking. Low switching costs, social reviews and multi-homing on WeChat (1.3B MAU) and Alipay (>1B) erode lock-in. Enterprise partners supplied ~45% of new policies in 2024, creating concentrated bargaining power. Fast claims, clear exclusions and low fees (eg GoFundMe 0% platform + ~2.9%+0.30) drive expectations.

| Metric | 2024 | Implication |

|---|---|---|

| Comparison use | 60% | Higher price pressure |

| WeChat MAU | 1.3B | Multi-homing |

| Alipay users | >1B | Low lock-in |

| Partner share | ~45% | Concentrated leverage |

Full Version Awaits

Waterdrop Porter's Five Forces Analysis

This preview displays the exact Waterdrop Porter's Five Forces analysis you'll receive after purchase—no placeholders or mockups. The document is the final, fully formatted file, ready for immediate download and use the moment you buy. What you see here is precisely the deliverable you'll get, complete and professional.

Original: $10.00

-65%$10.00

$3.50Description

Don't Miss the Bigger Picture

Waterdrop’s Porter's Five Forces highlights intense rivalry, moderate supplier power, rising buyer sophistication, looming substitute threats, and barriers that shape growth and margins. This snapshot frames strategic risks and opportunities for investors and managers. Unlock the full Porter's Five Forces Analysis to explore Waterdrop’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentrated insurers and reinsurers

In 2024 Waterdrop depends on a concentrated group of state-owned and top private insurers for health and life products and underwriting capacity, giving those partners leverage over commission rates, product exclusivity and data access.

Platform gatekeepers and traffic sources

User acquisition for Waterdrop depends heavily on super-app ecosystems and ad platforms (WeChat, Alipay, Douyin, Baidu), which together captured over 70% of China mobile ad spend in 2024; these concentrated channels can raise ad prices, tweak algorithms, or limit insurance promos, driving CAC volatility and giving suppliers negotiation leverage, while diversification into organic channels only partially offsets this power.

Payments and fintech infrastructure

Alipay and WeChat Pay together control over 90% of China’s mobile payments (Alipay ≈54%, WeChat Pay ≈39% in 2024), setting fees, platform rules and user flows. Policy or fee shifts can sharply affect Waterdrop’s conversion, refunds and crowdfunding disbursements. Their leverage lets them extract fees or impose compliance burdens. Switching costs are high due to entrenched user habits and network effects.

Medical data, TPAs, and provider networks

Claims verification, health data feeds and TPA services for Waterdrop depend on specialized vendors and hospital networks; high-quality providers are limited and bound by China’s PIPL/Data Security Law enforcement in 2024, raising switching costs and enabling vendors to price-discriminate or favor larger partners while complex integration locks in customers.

- Limited providers

- Regulatory compliance (PIPL/Data Security Law 2024)

- High switching costs

- Vendor pricing power

- Integration dependency

Exclusive product and API access

Insurers granting exclusive APIs and co-branded products to preferred channels materially shape conversion and differentiation; exclusive API access can lift channel conversion by an estimated 30-40% in 2024, concentrating product influence with suppliers and tying Waterdrop’s roadmap to partner priorities.

Negotiating stronger SLAs and exclusivity typically demands volume commitments (often quarterly or annual quotas), increasing supplier leverage and raising switching costs; this dynamic heightens supplier bargaining power.

- Exclusive API access: drives 30-40% higher conversion (2024 est.)

- Volume-linked SLAs: quarterly/annual commitments common

- Result: increased supplier leverage over product roadmap

2024: Insurers, super-apps and payment duopoly amplify supplier power over health platforms

In 2024 Waterdrop faces high supplier power: concentrated insurers control underwriting and API access, super-apps (WeChat, Alipay, Douyin, Baidu) drive >70% mobile ad spend and set user acquisition terms, and Alipay+WeChat Pay hold ≈90% mobile payments, raising fees and switching costs; vendor scarcity for TPAs/health data and regulatory data rules (PIPL) further boost supplier leverage.

| Metric | 2024 |

|---|---|

| Super-app ad share | >70% |

| Alipay / WeChat Pay | ≈54% / ≈39% (≈90% total) |

| API conversion lift | 30–40% est. |

What is included in the product

Tailored Porter's Five Forces analysis for Waterdrop that uncovers competitive drivers, supplier and buyer influence, substitutes and disruptive threats, and evaluates entry barriers shaping its pricing and profitability.

Concise Waterdrop Porter's Five Forces one-sheet that instantly clarifies competitive, supplier, buyer and regulatory pressures—ideal for quick decision-making and boardroom use.

Customers Bargaining Power

Price-sensitive, informed consumers

Users can instantly compare premiums, coverage, and riders across platforms, with 60% of insurance shoppers using online comparison tools in 2024, increasing transparency and deal-seeking. Low switching costs and frequent promotions compress platform commission margins and raise price pressure on agents. Transparent reviews and social sharing amplify negative network effects for poor offers. Together, these trends materially raise buyer bargaining power in Waterdrop’s marketplace.

Trust and claims experience expectations

Policyholders demand seamless claims and empathetic service, and poor experiences drive churn; negative word-of-mouth on social channels and press accelerates reputational damage and tightens service SLAs. Buyers also press for faster underwriting and clearer exclusions, forcing Waterdrop to invest heavily in customer service and claims tech, which compresses margins.

Crowdfunding campaigners’ urgency

Patients seeking medical funds demand fast approval, high visibility, and low fees. They can migrate to alternative platforms or charitable foundations if terms seem unfavorable. Platform choice hinges on transparency and fraud controls; in 2024 US leaders like GoFundMe use 0% platform fees but payment processing ~2.9% + $0.30. Situational leverage raises expectations on speed and outreach.

Multi-homing across super-apps

Users routinely multi-home across WeChat (~1.3 billion MAU in 2024 per Tencent) and Alipay (>1 billion users in 2024 per Ant Group) mini-programs plus competitor apps, eroding lock-in and amplifying customer bargaining power. Loyalty points give limited stickiness versus super-app convenience, forcing Waterdrop to continuously optimize funnels and conversion metrics to retain users.

- Multi-homing: increases choice, reduces switching costs

- Scale: super-app reach >1B users

- Retention: loyalty weaker than ecosystem

- Action: constant funnel/device optimization

Enterprise and affinity partners

Enterprise and affinity partners—Corporate HR, communities, and KOLs—can steer large cohorts toward specific Waterdrop products, securing discounted group rates or higher revenue shares; in 2024 these channels reportedly drove about 45% of new policy volumes, magnifying partner bargaining power and making losing one large partner disproportionately hit volumes.

- Concentration: top accounts drive ~45% of new volumes (2024)

- Leverage: group discounts/higher revenue shares common

- Risk: single-partner loss causes outsized volume decline

60% compare online; 45% partner share erodes pricing

Buyers use online comparison (60% in 2024), lowering price tolerance and boosting deal-seeking. Low switching costs, social reviews and multi-homing on WeChat (1.3B MAU) and Alipay (>1B) erode lock-in. Enterprise partners supplied ~45% of new policies in 2024, creating concentrated bargaining power. Fast claims, clear exclusions and low fees (eg GoFundMe 0% platform + ~2.9%+0.30) drive expectations.

| Metric | 2024 | Implication |

|---|---|---|

| Comparison use | 60% | Higher price pressure |

| WeChat MAU | 1.3B | Multi-homing |

| Alipay users | >1B | Low lock-in |

| Partner share | ~45% | Concentrated leverage |

Full Version Awaits

Waterdrop Porter's Five Forces Analysis

This preview displays the exact Waterdrop Porter's Five Forces analysis you'll receive after purchase—no placeholders or mockups. The document is the final, fully formatted file, ready for immediate download and use the moment you buy. What you see here is precisely the deliverable you'll get, complete and professional.