Waystar Porter's Five Forces Analysis

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

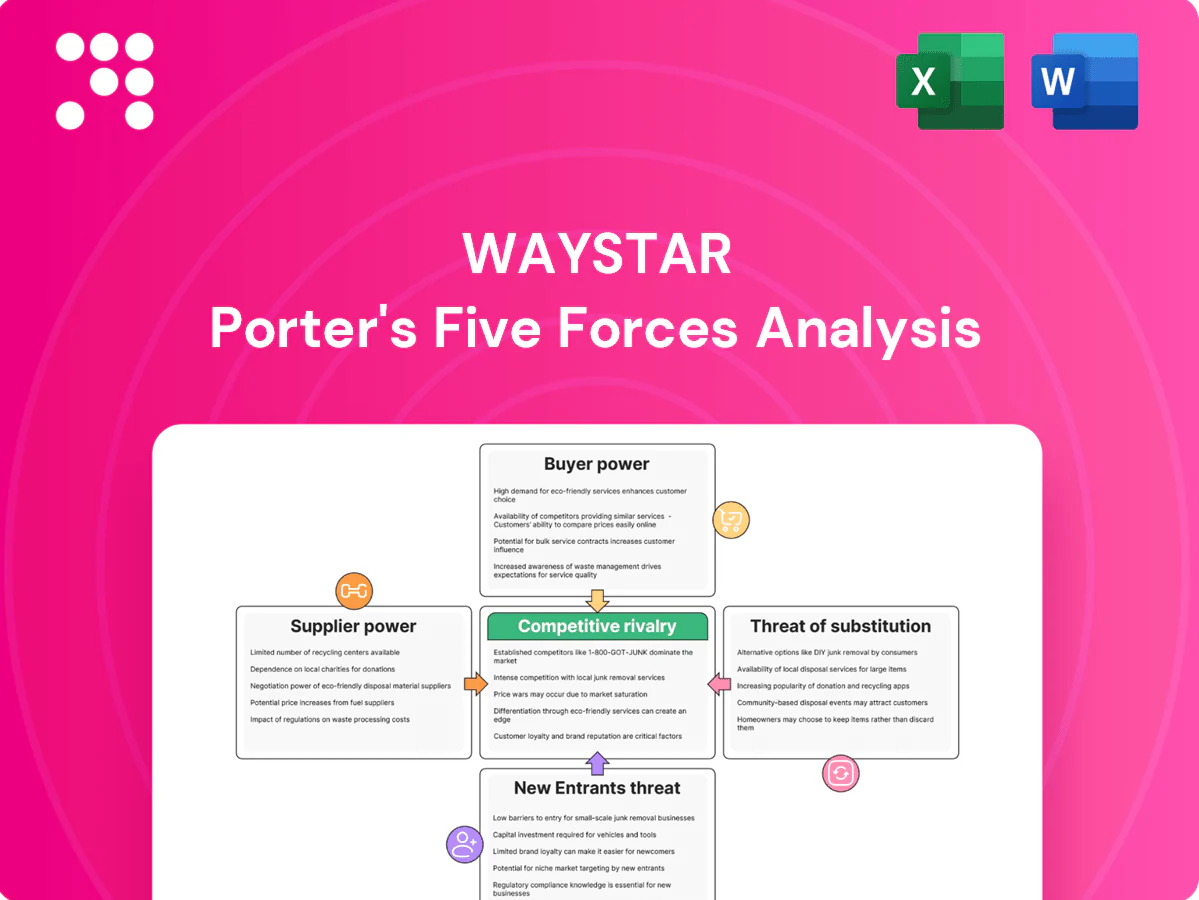

Waystar faces moderate buyer power, high supplier complexity, and intensifying competitive rivalry as healthcare payments digitize. Regulatory shifts and tech-enabled entrants raise threat levels while switching costs offer some protection. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Waystar’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Dependence on cloud and core infrastructure

Waystar relies on hyperscale cloud providers for compute, storage and uptime SLAs, with AWS, Azure and GCP holding roughly 33%, 23% and 11% market share in 2024, giving those vendors moderate leverage.

Pricing shifts and reserved/committed-use dynamics materially affect COGS and margins; committed discounts can cut cloud spend by up to 70% on some offerings.

Adopting multi-cloud and containerization can mitigate lock-in but raises operational complexity and orchestration costs, making long-term capacity planning and committed-use contracts critical to reduce exposure.

EHR and data interface providers

Deep integrations with EHRs like Epic (roughly 34% US hospital market share in 2024) and Oracle Health (about 26%) give those vendors leverage over API access, certifications and support, and proprietary interfaces plus certification fees materially raise switching costs for Waystar. FHIR adoption climbed above 70% by 2024, and interoperability mandates are gradually reducing supplier power. Joint roadmaps and co-marketing partnerships are effective levers to rebalance negotiations.

Payment networks and processors

Card networks, merchant acquirers, and ACH gateways set pricing for patient payments and remittances; interchange and assessment fees typically run about 1%–3% per transaction and are largely non-negotiable, constraining Waystar's take-rates.

Volume aggregation and routing optimization can reduce effective fees by roughly 10%–30% on large portfolios.

RTP and FedNow (live since 2023) provide incremental leverage for lower-cost instant rails over time.

Clearinghouse connectivity and payer rules content

Access to payer EDI, edits and rules engines often sits with third‑party clearinghouses, which in 2024 charged roughly $0.50–$3.00 per transaction and leverage SLAs (typical uptime 99.9%), directly affecting denial rates; industry data show about 60% of denials are preventable, so rules accuracy materially impacts client ROI. Building proprietary rules cuts supplier dependence but demands continuous investment and rapid updates as CMS and payers change rules annually.

- Third‑party fee pressure: $0.50–$3/tx (2024)

- Preventable denials ≈60% (industry)

- SLA uptime ~99.9%

- Regulatory churn: annual CMS/payer updates

Specialized talent and cybersecurity vendors

AI/ML engineers, compliance experts, and security partners were scarce in 2024, commanding premium rates often 30–40% above general developer pay; HITRUST and SOC2 auditors plus security tooling vendors exert strong price influence because certifications are critical and audits/tooling commonly cost tens to hundreds of thousands annually. Labor markets cyclically shift but remained tight for healthcare fintech in 2024; Waystar offsets pressure with a strong employer brand and automation.

- AI/ML talent: 30–40% pay premium

- Compliance/security vendors: audits/tooling cost tens–hundreds k/year

- Market tightness: healthcare fintech talent scarce in 2024

- Mitigation: employer brand + automation

Hyperscale clouds, dominant EHRs and rising fees drive moderate-high supplier leverage

Waystar relies on hyperscale clouds (AWS33%, Azure23%, GCP11%) and EHRs (Epic34%, Oracle26%), creating moderate–high supplier leverage. Payments fees 1–3% and clearinghouses $0.5–3/tx constrain margins. Talent/audit costs (+30–40% pay premium; audits tens–100ks) further increase supplier power.

| Supplier | 2024 |

|---|---|

| Cloud | AWS33%/Azure23%/GCP11% |

| EHRs | Epic34%/Oracle26% |

| Payments | Fees1–3%/Clearing$0.5–3 |

| Talent/Audit | Premium30–40%/audits10k–100k+ |

What is included in the product

Uncovers key drivers of competition, buyer and supplier power, barriers to entry, substitutes and disruptive threats specific to Waystar, with strategic commentary and industry data; fully editable Word format for use in investor materials, business plans, internal strategy decks, or academic projects.

A one-sheet Waystar Five Forces summary with editable pressure sliders and radar chart—instantly highlights competitive pain points, ready for pitch decks or integration into Excel dashboards; no macros, customizable for pre/post-regulation scenarios and quick decision-making.

Customers Bargaining Power

Consolidated health systems and IDNs

Consolidated health systems and IDNs exert strong buyer power: by 2024 roughly two-thirds of U.S. hospitals belong to multi-hospital systems, enabling large-scale RFPs that drive significant price and contract leverage. They demand enterprise discounts, outcome-based SLAs, and integration commitments while facing high switching costs, yet use multi-vendor bidding to extract concessions. Strong referenceability and performance proof points materially limit vendor givebacks.

Mid-market providers and physician groups

Smaller mid-market providers and physician groups are highly price sensitive but often lack IT staff—AMA 2023 reports roughly 60% of practices have 10 or fewer clinicians—limiting negotiation leverage. Bundled modules and rapid time-to-value (often framed as 3–6 months) sway buying decisions and justify standard packaging. Standardized offers constrain discounting, while churn risk rises quickly if measurable ROI is absent within months.

Demand for measurable financial outcomes

Buyers increasingly demand guarantees tied to denial reduction, cash acceleration, and cost-to-collect, with 2024 surveys showing roughly 62% of US health systems preferring performance-based contracts.

This shifts power toward customers via performance-based pricing, pressuring vendors to offer transparent analytics and benchmarking to defend fees.

Shared-savings models, used by many large systems in 2024, align interests while capping vendor downside and preserving upside participation.

Integration and switching costs

Deep EHR workflows and embedded billing operations create high switching costs that temper buyer power after implementation; data migration, retraining, and interface rebuilds act as strong deterrents to frequent supplier changes.

Buyers retain some leverage via termination and renewal clauses, but once integrated the practical friction keeps churn low and pricing power with vendors elevated.

Smooth migration playbooks and turnkey interfaces reduce perceived risk and can materially shorten sales cycles.

Regulatory and security expectations

Buyers demand HIPAA, HITRUST and 99.9%+ uptime and will extract concessions if gaps exist; in 2024 HITRUST reported about 10,000 certified organizations, raising baseline buyer expectations. Security questionnaires and risk reviews commonly extend sales cycles by ~90 days and add negotiating friction. Strong compliance and incident-free track records shift power back to Waystar, while competitor breaches temporarily reduce buyer alternatives.

- HIPAA/HITRUST: baseline requirement; ~10,000 HITRUST certs (2024)

- Uptime: 99.9%+ expected SLA

- Procurement delay: ~90-day security review

- Incidents: competitor breaches reduce alternatives

Consolidated hospital systems gain pricing leverage; performance contracts empower buyers

Consolidated systems (≈66% of US hospitals in systems by 2024) wield strong price and contract leverage, forcing enterprise discounts and outcome SLAs. Mid-market practices (~60% have ≤10 clinicians in 2023) are price sensitive but lack IT leverage. Performance-based contracts (~62% preference in 2024) shift power to buyers; high EHR integration and migration costs limit churn.

| Metric | 2023–24 |

|---|---|

| Hospitals in systems | ≈66% |

| Small practices (≤10 clinicians) | ≈60% |

| Prefer performance contracts | ≈62% |

Preview Before You Purchase

Waystar Porter's Five Forces Analysis

This preview shows the exact Waystar Porter’s Five Forces analysis you'll receive immediately after purchase—no placeholders or sample sections. The document is fully formatted and professionally written, ready for download and use the moment you buy. What you see here is the final deliverable, available instantly upon payment.

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Waystar faces moderate buyer power, high supplier complexity, and intensifying competitive rivalry as healthcare payments digitize. Regulatory shifts and tech-enabled entrants raise threat levels while switching costs offer some protection. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Waystar’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Dependence on cloud and core infrastructure

Waystar relies on hyperscale cloud providers for compute, storage and uptime SLAs, with AWS, Azure and GCP holding roughly 33%, 23% and 11% market share in 2024, giving those vendors moderate leverage.

Pricing shifts and reserved/committed-use dynamics materially affect COGS and margins; committed discounts can cut cloud spend by up to 70% on some offerings.

Adopting multi-cloud and containerization can mitigate lock-in but raises operational complexity and orchestration costs, making long-term capacity planning and committed-use contracts critical to reduce exposure.

EHR and data interface providers

Deep integrations with EHRs like Epic (roughly 34% US hospital market share in 2024) and Oracle Health (about 26%) give those vendors leverage over API access, certifications and support, and proprietary interfaces plus certification fees materially raise switching costs for Waystar. FHIR adoption climbed above 70% by 2024, and interoperability mandates are gradually reducing supplier power. Joint roadmaps and co-marketing partnerships are effective levers to rebalance negotiations.

Payment networks and processors

Card networks, merchant acquirers, and ACH gateways set pricing for patient payments and remittances; interchange and assessment fees typically run about 1%–3% per transaction and are largely non-negotiable, constraining Waystar's take-rates.

Volume aggregation and routing optimization can reduce effective fees by roughly 10%–30% on large portfolios.

RTP and FedNow (live since 2023) provide incremental leverage for lower-cost instant rails over time.

Clearinghouse connectivity and payer rules content

Access to payer EDI, edits and rules engines often sits with third‑party clearinghouses, which in 2024 charged roughly $0.50–$3.00 per transaction and leverage SLAs (typical uptime 99.9%), directly affecting denial rates; industry data show about 60% of denials are preventable, so rules accuracy materially impacts client ROI. Building proprietary rules cuts supplier dependence but demands continuous investment and rapid updates as CMS and payers change rules annually.

- Third‑party fee pressure: $0.50–$3/tx (2024)

- Preventable denials ≈60% (industry)

- SLA uptime ~99.9%

- Regulatory churn: annual CMS/payer updates

Specialized talent and cybersecurity vendors

AI/ML engineers, compliance experts, and security partners were scarce in 2024, commanding premium rates often 30–40% above general developer pay; HITRUST and SOC2 auditors plus security tooling vendors exert strong price influence because certifications are critical and audits/tooling commonly cost tens to hundreds of thousands annually. Labor markets cyclically shift but remained tight for healthcare fintech in 2024; Waystar offsets pressure with a strong employer brand and automation.

- AI/ML talent: 30–40% pay premium

- Compliance/security vendors: audits/tooling cost tens–hundreds k/year

- Market tightness: healthcare fintech talent scarce in 2024

- Mitigation: employer brand + automation

Hyperscale clouds, dominant EHRs and rising fees drive moderate-high supplier leverage

Waystar relies on hyperscale clouds (AWS33%, Azure23%, GCP11%) and EHRs (Epic34%, Oracle26%), creating moderate–high supplier leverage. Payments fees 1–3% and clearinghouses $0.5–3/tx constrain margins. Talent/audit costs (+30–40% pay premium; audits tens–100ks) further increase supplier power.

| Supplier | 2024 |

|---|---|

| Cloud | AWS33%/Azure23%/GCP11% |

| EHRs | Epic34%/Oracle26% |

| Payments | Fees1–3%/Clearing$0.5–3 |

| Talent/Audit | Premium30–40%/audits10k–100k+ |

What is included in the product

Uncovers key drivers of competition, buyer and supplier power, barriers to entry, substitutes and disruptive threats specific to Waystar, with strategic commentary and industry data; fully editable Word format for use in investor materials, business plans, internal strategy decks, or academic projects.

A one-sheet Waystar Five Forces summary with editable pressure sliders and radar chart—instantly highlights competitive pain points, ready for pitch decks or integration into Excel dashboards; no macros, customizable for pre/post-regulation scenarios and quick decision-making.

Customers Bargaining Power

Consolidated health systems and IDNs

Consolidated health systems and IDNs exert strong buyer power: by 2024 roughly two-thirds of U.S. hospitals belong to multi-hospital systems, enabling large-scale RFPs that drive significant price and contract leverage. They demand enterprise discounts, outcome-based SLAs, and integration commitments while facing high switching costs, yet use multi-vendor bidding to extract concessions. Strong referenceability and performance proof points materially limit vendor givebacks.

Mid-market providers and physician groups

Smaller mid-market providers and physician groups are highly price sensitive but often lack IT staff—AMA 2023 reports roughly 60% of practices have 10 or fewer clinicians—limiting negotiation leverage. Bundled modules and rapid time-to-value (often framed as 3–6 months) sway buying decisions and justify standard packaging. Standardized offers constrain discounting, while churn risk rises quickly if measurable ROI is absent within months.

Demand for measurable financial outcomes

Buyers increasingly demand guarantees tied to denial reduction, cash acceleration, and cost-to-collect, with 2024 surveys showing roughly 62% of US health systems preferring performance-based contracts.

This shifts power toward customers via performance-based pricing, pressuring vendors to offer transparent analytics and benchmarking to defend fees.

Shared-savings models, used by many large systems in 2024, align interests while capping vendor downside and preserving upside participation.

Integration and switching costs

Deep EHR workflows and embedded billing operations create high switching costs that temper buyer power after implementation; data migration, retraining, and interface rebuilds act as strong deterrents to frequent supplier changes.

Buyers retain some leverage via termination and renewal clauses, but once integrated the practical friction keeps churn low and pricing power with vendors elevated.

Smooth migration playbooks and turnkey interfaces reduce perceived risk and can materially shorten sales cycles.

Regulatory and security expectations

Buyers demand HIPAA, HITRUST and 99.9%+ uptime and will extract concessions if gaps exist; in 2024 HITRUST reported about 10,000 certified organizations, raising baseline buyer expectations. Security questionnaires and risk reviews commonly extend sales cycles by ~90 days and add negotiating friction. Strong compliance and incident-free track records shift power back to Waystar, while competitor breaches temporarily reduce buyer alternatives.

- HIPAA/HITRUST: baseline requirement; ~10,000 HITRUST certs (2024)

- Uptime: 99.9%+ expected SLA

- Procurement delay: ~90-day security review

- Incidents: competitor breaches reduce alternatives

Consolidated hospital systems gain pricing leverage; performance contracts empower buyers

Consolidated systems (≈66% of US hospitals in systems by 2024) wield strong price and contract leverage, forcing enterprise discounts and outcome SLAs. Mid-market practices (~60% have ≤10 clinicians in 2023) are price sensitive but lack IT leverage. Performance-based contracts (~62% preference in 2024) shift power to buyers; high EHR integration and migration costs limit churn.

| Metric | 2023–24 |

|---|---|

| Hospitals in systems | ≈66% |

| Small practices (≤10 clinicians) | ≈60% |

| Prefer performance contracts | ≈62% |

Preview Before You Purchase

Waystar Porter's Five Forces Analysis

This preview shows the exact Waystar Porter’s Five Forces analysis you'll receive immediately after purchase—no placeholders or sample sections. The document is fully formatted and professionally written, ready for download and use the moment you buy. What you see here is the final deliverable, available instantly upon payment.

Description

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Waystar faces moderate buyer power, high supplier complexity, and intensifying competitive rivalry as healthcare payments digitize. Regulatory shifts and tech-enabled entrants raise threat levels while switching costs offer some protection. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Waystar’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Dependence on cloud and core infrastructure

Waystar relies on hyperscale cloud providers for compute, storage and uptime SLAs, with AWS, Azure and GCP holding roughly 33%, 23% and 11% market share in 2024, giving those vendors moderate leverage.

Pricing shifts and reserved/committed-use dynamics materially affect COGS and margins; committed discounts can cut cloud spend by up to 70% on some offerings.

Adopting multi-cloud and containerization can mitigate lock-in but raises operational complexity and orchestration costs, making long-term capacity planning and committed-use contracts critical to reduce exposure.

EHR and data interface providers

Deep integrations with EHRs like Epic (roughly 34% US hospital market share in 2024) and Oracle Health (about 26%) give those vendors leverage over API access, certifications and support, and proprietary interfaces plus certification fees materially raise switching costs for Waystar. FHIR adoption climbed above 70% by 2024, and interoperability mandates are gradually reducing supplier power. Joint roadmaps and co-marketing partnerships are effective levers to rebalance negotiations.

Payment networks and processors

Card networks, merchant acquirers, and ACH gateways set pricing for patient payments and remittances; interchange and assessment fees typically run about 1%–3% per transaction and are largely non-negotiable, constraining Waystar's take-rates.

Volume aggregation and routing optimization can reduce effective fees by roughly 10%–30% on large portfolios.

RTP and FedNow (live since 2023) provide incremental leverage for lower-cost instant rails over time.

Clearinghouse connectivity and payer rules content

Access to payer EDI, edits and rules engines often sits with third‑party clearinghouses, which in 2024 charged roughly $0.50–$3.00 per transaction and leverage SLAs (typical uptime 99.9%), directly affecting denial rates; industry data show about 60% of denials are preventable, so rules accuracy materially impacts client ROI. Building proprietary rules cuts supplier dependence but demands continuous investment and rapid updates as CMS and payers change rules annually.

- Third‑party fee pressure: $0.50–$3/tx (2024)

- Preventable denials ≈60% (industry)

- SLA uptime ~99.9%

- Regulatory churn: annual CMS/payer updates

Specialized talent and cybersecurity vendors

AI/ML engineers, compliance experts, and security partners were scarce in 2024, commanding premium rates often 30–40% above general developer pay; HITRUST and SOC2 auditors plus security tooling vendors exert strong price influence because certifications are critical and audits/tooling commonly cost tens to hundreds of thousands annually. Labor markets cyclically shift but remained tight for healthcare fintech in 2024; Waystar offsets pressure with a strong employer brand and automation.

- AI/ML talent: 30–40% pay premium

- Compliance/security vendors: audits/tooling cost tens–hundreds k/year

- Market tightness: healthcare fintech talent scarce in 2024

- Mitigation: employer brand + automation

Hyperscale clouds, dominant EHRs and rising fees drive moderate-high supplier leverage

Waystar relies on hyperscale clouds (AWS33%, Azure23%, GCP11%) and EHRs (Epic34%, Oracle26%), creating moderate–high supplier leverage. Payments fees 1–3% and clearinghouses $0.5–3/tx constrain margins. Talent/audit costs (+30–40% pay premium; audits tens–100ks) further increase supplier power.

| Supplier | 2024 |

|---|---|

| Cloud | AWS33%/Azure23%/GCP11% |

| EHRs | Epic34%/Oracle26% |

| Payments | Fees1–3%/Clearing$0.5–3 |

| Talent/Audit | Premium30–40%/audits10k–100k+ |

What is included in the product

Uncovers key drivers of competition, buyer and supplier power, barriers to entry, substitutes and disruptive threats specific to Waystar, with strategic commentary and industry data; fully editable Word format for use in investor materials, business plans, internal strategy decks, or academic projects.

A one-sheet Waystar Five Forces summary with editable pressure sliders and radar chart—instantly highlights competitive pain points, ready for pitch decks or integration into Excel dashboards; no macros, customizable for pre/post-regulation scenarios and quick decision-making.

Customers Bargaining Power

Consolidated health systems and IDNs

Consolidated health systems and IDNs exert strong buyer power: by 2024 roughly two-thirds of U.S. hospitals belong to multi-hospital systems, enabling large-scale RFPs that drive significant price and contract leverage. They demand enterprise discounts, outcome-based SLAs, and integration commitments while facing high switching costs, yet use multi-vendor bidding to extract concessions. Strong referenceability and performance proof points materially limit vendor givebacks.

Mid-market providers and physician groups

Smaller mid-market providers and physician groups are highly price sensitive but often lack IT staff—AMA 2023 reports roughly 60% of practices have 10 or fewer clinicians—limiting negotiation leverage. Bundled modules and rapid time-to-value (often framed as 3–6 months) sway buying decisions and justify standard packaging. Standardized offers constrain discounting, while churn risk rises quickly if measurable ROI is absent within months.

Demand for measurable financial outcomes

Buyers increasingly demand guarantees tied to denial reduction, cash acceleration, and cost-to-collect, with 2024 surveys showing roughly 62% of US health systems preferring performance-based contracts.

This shifts power toward customers via performance-based pricing, pressuring vendors to offer transparent analytics and benchmarking to defend fees.

Shared-savings models, used by many large systems in 2024, align interests while capping vendor downside and preserving upside participation.

Integration and switching costs

Deep EHR workflows and embedded billing operations create high switching costs that temper buyer power after implementation; data migration, retraining, and interface rebuilds act as strong deterrents to frequent supplier changes.

Buyers retain some leverage via termination and renewal clauses, but once integrated the practical friction keeps churn low and pricing power with vendors elevated.

Smooth migration playbooks and turnkey interfaces reduce perceived risk and can materially shorten sales cycles.

Regulatory and security expectations

Buyers demand HIPAA, HITRUST and 99.9%+ uptime and will extract concessions if gaps exist; in 2024 HITRUST reported about 10,000 certified organizations, raising baseline buyer expectations. Security questionnaires and risk reviews commonly extend sales cycles by ~90 days and add negotiating friction. Strong compliance and incident-free track records shift power back to Waystar, while competitor breaches temporarily reduce buyer alternatives.

- HIPAA/HITRUST: baseline requirement; ~10,000 HITRUST certs (2024)

- Uptime: 99.9%+ expected SLA

- Procurement delay: ~90-day security review

- Incidents: competitor breaches reduce alternatives

Consolidated hospital systems gain pricing leverage; performance contracts empower buyers

Consolidated systems (≈66% of US hospitals in systems by 2024) wield strong price and contract leverage, forcing enterprise discounts and outcome SLAs. Mid-market practices (~60% have ≤10 clinicians in 2023) are price sensitive but lack IT leverage. Performance-based contracts (~62% preference in 2024) shift power to buyers; high EHR integration and migration costs limit churn.

| Metric | 2023–24 |

|---|---|

| Hospitals in systems | ≈66% |

| Small practices (≤10 clinicians) | ≈60% |

| Prefer performance contracts | ≈62% |

Preview Before You Purchase

Waystar Porter's Five Forces Analysis

This preview shows the exact Waystar Porter’s Five Forces analysis you'll receive immediately after purchase—no placeholders or sample sections. The document is fully formatted and professionally written, ready for download and use the moment you buy. What you see here is the final deliverable, available instantly upon payment.