WD-40 Porter's Five Forces Analysis

Go Beyond the Preview—Access the Full Strategic Report

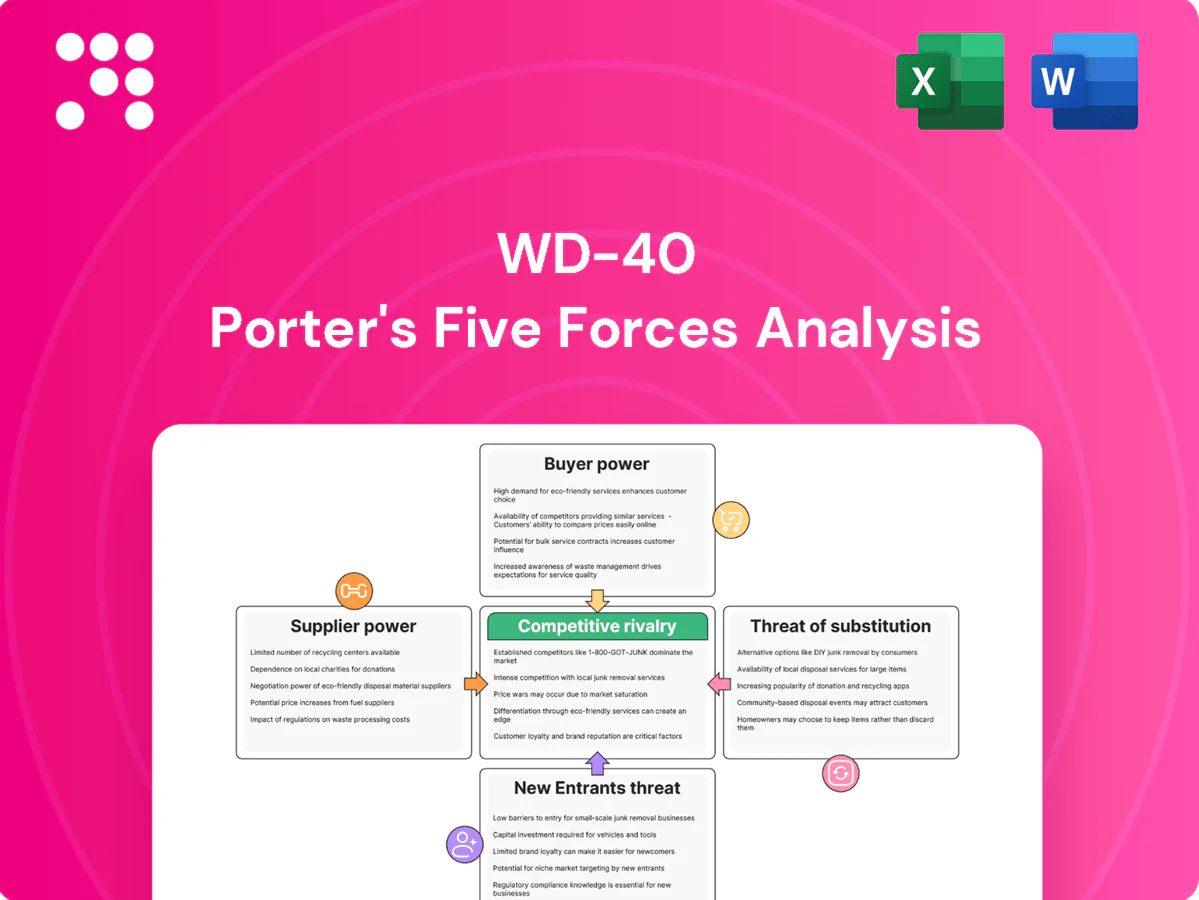

WD-40 faces moderate supplier power, steady buyer demand, low threat of new entrants but rising substitute pressure in specialty maintenance markets; rivalry hinges on brand trust and distribution reach. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore WD-40’s competitive dynamics in detail.

Suppliers Bargaining Power

Concentrated raw material categories

WD-40 sources petroleum distillates, propellants and metal aerosol packaging from a relatively concentrated set of global suppliers, creating coordination risk and some upstream leverage. These inputs are largely commoditized, allowing multi-sourcing and global procurement strategies. WD-40’s scale—selling in 176 countries—and FY2024 net sales of $519.7 million strengthen its negotiating position and continuity of supply.

Commodity price volatility

Input costs for hydrocarbons, solvents and tin/steel move with oil and metals cycles—Brent averaged about $85/bbl in 2024, tin rose roughly 15% and steel costs climbed near 8% year-over-year. Suppliers can push price increases faster than brands adjust, compressing margins. WD-40 mitigates via hedging, multi‑year contracts and periodic pricing actions, but lag effects still squeeze margins during spikes.

Regulatory and ESG constraints

Regulatory limits on propellants and VOCs (notably stricter in the EU and California) shrink approved suppliers and, combined with WD-40’s global quality standards, raises supplier power; in FY2024 WD-40 reported net sales of $686.5 million, underscoring reliance on compliant aerosol supply chains. Compliance-driven reformulation often locks in specialized vendors, though long-term partnerships and supply agreements mitigate bargaining disadvantages.

Contract manufacturing dependency

Use of third-party fillers and packagers creates switching frictions for WD-40, raising relocation costs and lead-time risk for bottle, aerosol and pouch formats.

Capacity tightness or line-time scarcity gives contract manufacturers leverage in peak periods; dual-sourcing and validated alternates are employed to reduce interruption risk, while service-level and quality clauses partially rebalance supplier power.

- Third-party dependency: switching frictions

- Capacity tightness: peak leverage

- Mitigation: dual-sourcing, validated alternates

- Controls: service-level and quality clauses

Logistics and lead-time dynamics

Logistics and lead-time dynamics raise supplier power for WD-40 as global shipping and hazmat handling periodically extend replenishment cycles, with 2024 liner schedule reliability around 60% per industry reports, amplifying lane control and surge-capacity leverage. WD-40’s regional hubs and inventory buffers reduce disruption risk, but tight logistics during shocks still elevate suppliers’ negotiating position.

- Critical lanes control: increases supplier leverage

- Hazmat adds handling delays: longer lead times

- Inventory buffers: mitigate but not eliminate risk

Lubricant leader hit by oil, tin and hazmat logistics squeeze; margins under pressure

WD-40 faces moderate supplier power: commoditized inputs enable multi-sourcing but concentrated aerosol/propellant suppliers and hazmat logistics raise leverage. FY2024 net sales $519.7M and global reach reduce supplier influence, but oil at ~$85/bbl, tin +15% and 60% liner reliability in 2024 squeezed margins. Dual-sourcing, hedging and SLAs partially offset switching frictions and peak-period capacity leverage.

| Metric | 2024 |

|---|---|

| Net sales | $519.7M |

| Brent | $85/bbl |

| Tin | +15% YoY |

| Liner reliability | 60% |

What is included in the product

Analyzes competitive rivalry, buyer and supplier power, threat of substitutes and new entrants for WD‑40, highlighting key drivers, vulnerabilities, and strategic levers to protect margins, market share, and long‑term positioning.

A concise Porter's Five Forces one-sheet pinpointing competitive pressures for WD‑40, letting teams quickly identify and alleviate strategic pain points like supplier concentration, new entrants, substitute sprays, and buyer power for faster, actionable decisions.

Customers Bargaining Power

Concentrated retail and industrial channels

Big-box retailers, auto aftermarket chains and industrial distributors control shelf space and terms, leveraging scale to demand price concessions and promotional support; WD-40 Company reported fiscal 2024 net sales of about $517 million, underscoring exposure to these channels. Their buying power translates into significant price and promotion leverage, which WD-40’s strong brand mitigates but does not remove. Trade spend and vendor-program compliance remain ongoing, material costs for maintaining placement and promotions.

Low switching costs, high brand loyalty

Low switching costs let end users easily try alternatives, implying theoretical buyer power, but WD-40’s iconic brand and >90% aided awareness and ~535 million USD net sales in FY2024 drive habit and repeat purchase, reducing price elasticity versus private labels.

Private label and house brands

Retailers leverage private labels—which captured roughly 22% penetration in U.S. household/hardware categories in 2024—to threaten substitution and secure better terms, pressuring price points and margin mix. WD-40, which reported about $564 million in net sales in FY2024, defends through strong differentiation, global brand equity and superior merchandising. Nevertheless, the company must carefully manage price gaps in price-sensitive segments to protect volume and margins.

Demand visibility and forecasting

Seasonality and promotion-led lifts force collaborative planning; in FY2024 WD-40 Company reported approximately $500M in net sales, so major retailers demand visibility to manage 10–30% seasonal swings. Buyers who share POS and forecast data smooth orders but leverage better terms; WD-40 exchanges forecasting insights for shelf and display support, and improved on-time delivery and fill rates modestly reduce buyer bargaining power.

- Seasonal variance: 10–30% swings

- FY2024 net sales: ~$500M

- Data-sharing smooths orders vs. tougher terms

- Insights traded for shelf/display

- Better service metrics lower buyer leverage

International mix and channel diversity

WD-40's international mix and channel diversity—available in more than 176 countries as of 2024—reduces dependence on any single retailer or distributor, limiting buyer power while allowing negotiation flexibility through a broad portfolio. Local incumbents can still wield strong influence in specific markets.

- Global reach: 176+ countries (2024)

- Channel split: retail and pro/industrial diversify risk

- Portfolio breadth enables pricing leverage

Retailer pricing power challenges high-awareness maintenance brands despite strong sales

Large retailers and distributors exert strong price/promotional leverage despite WD-40’s ~564M USD FY2024 net sales and >90% aided brand awareness; low switching costs raise buyer power but brand loyalty reduces elasticity. Private-labels (~22% U.S. penetration 2024) and seasonal 10–30% swings amplify retailer bargaining; global presence (176+ countries) diversifies risk and limits single-buyer dependence.

| Metric | 2024 |

|---|---|

| Net sales | $564M |

| Brand awareness | >90% |

| Global reach | 176+ countries |

| Private-label U.S. | 22% |

Preview the Actual Deliverable

WD-40 Porter's Five Forces Analysis

This preview shows the full WD-40 Porter's Five Forces analysis you'll receive—no placeholders or edits. The document is professionally formatted and ready for download immediately after purchase. What you see is the exact deliverable and is ready for immediate use.

Go Beyond the Preview—Access the Full Strategic Report

WD-40 faces moderate supplier power, steady buyer demand, low threat of new entrants but rising substitute pressure in specialty maintenance markets; rivalry hinges on brand trust and distribution reach. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore WD-40’s competitive dynamics in detail.

Suppliers Bargaining Power

Concentrated raw material categories

WD-40 sources petroleum distillates, propellants and metal aerosol packaging from a relatively concentrated set of global suppliers, creating coordination risk and some upstream leverage. These inputs are largely commoditized, allowing multi-sourcing and global procurement strategies. WD-40’s scale—selling in 176 countries—and FY2024 net sales of $519.7 million strengthen its negotiating position and continuity of supply.

Commodity price volatility

Input costs for hydrocarbons, solvents and tin/steel move with oil and metals cycles—Brent averaged about $85/bbl in 2024, tin rose roughly 15% and steel costs climbed near 8% year-over-year. Suppliers can push price increases faster than brands adjust, compressing margins. WD-40 mitigates via hedging, multi‑year contracts and periodic pricing actions, but lag effects still squeeze margins during spikes.

Regulatory and ESG constraints

Regulatory limits on propellants and VOCs (notably stricter in the EU and California) shrink approved suppliers and, combined with WD-40’s global quality standards, raises supplier power; in FY2024 WD-40 reported net sales of $686.5 million, underscoring reliance on compliant aerosol supply chains. Compliance-driven reformulation often locks in specialized vendors, though long-term partnerships and supply agreements mitigate bargaining disadvantages.

Contract manufacturing dependency

Use of third-party fillers and packagers creates switching frictions for WD-40, raising relocation costs and lead-time risk for bottle, aerosol and pouch formats.

Capacity tightness or line-time scarcity gives contract manufacturers leverage in peak periods; dual-sourcing and validated alternates are employed to reduce interruption risk, while service-level and quality clauses partially rebalance supplier power.

- Third-party dependency: switching frictions

- Capacity tightness: peak leverage

- Mitigation: dual-sourcing, validated alternates

- Controls: service-level and quality clauses

Logistics and lead-time dynamics

Logistics and lead-time dynamics raise supplier power for WD-40 as global shipping and hazmat handling periodically extend replenishment cycles, with 2024 liner schedule reliability around 60% per industry reports, amplifying lane control and surge-capacity leverage. WD-40’s regional hubs and inventory buffers reduce disruption risk, but tight logistics during shocks still elevate suppliers’ negotiating position.

- Critical lanes control: increases supplier leverage

- Hazmat adds handling delays: longer lead times

- Inventory buffers: mitigate but not eliminate risk

Lubricant leader hit by oil, tin and hazmat logistics squeeze; margins under pressure

WD-40 faces moderate supplier power: commoditized inputs enable multi-sourcing but concentrated aerosol/propellant suppliers and hazmat logistics raise leverage. FY2024 net sales $519.7M and global reach reduce supplier influence, but oil at ~$85/bbl, tin +15% and 60% liner reliability in 2024 squeezed margins. Dual-sourcing, hedging and SLAs partially offset switching frictions and peak-period capacity leverage.

| Metric | 2024 |

|---|---|

| Net sales | $519.7M |

| Brent | $85/bbl |

| Tin | +15% YoY |

| Liner reliability | 60% |

What is included in the product

Analyzes competitive rivalry, buyer and supplier power, threat of substitutes and new entrants for WD‑40, highlighting key drivers, vulnerabilities, and strategic levers to protect margins, market share, and long‑term positioning.

A concise Porter's Five Forces one-sheet pinpointing competitive pressures for WD‑40, letting teams quickly identify and alleviate strategic pain points like supplier concentration, new entrants, substitute sprays, and buyer power for faster, actionable decisions.

Customers Bargaining Power

Concentrated retail and industrial channels

Big-box retailers, auto aftermarket chains and industrial distributors control shelf space and terms, leveraging scale to demand price concessions and promotional support; WD-40 Company reported fiscal 2024 net sales of about $517 million, underscoring exposure to these channels. Their buying power translates into significant price and promotion leverage, which WD-40’s strong brand mitigates but does not remove. Trade spend and vendor-program compliance remain ongoing, material costs for maintaining placement and promotions.

Low switching costs, high brand loyalty

Low switching costs let end users easily try alternatives, implying theoretical buyer power, but WD-40’s iconic brand and >90% aided awareness and ~535 million USD net sales in FY2024 drive habit and repeat purchase, reducing price elasticity versus private labels.

Private label and house brands

Retailers leverage private labels—which captured roughly 22% penetration in U.S. household/hardware categories in 2024—to threaten substitution and secure better terms, pressuring price points and margin mix. WD-40, which reported about $564 million in net sales in FY2024, defends through strong differentiation, global brand equity and superior merchandising. Nevertheless, the company must carefully manage price gaps in price-sensitive segments to protect volume and margins.

Demand visibility and forecasting

Seasonality and promotion-led lifts force collaborative planning; in FY2024 WD-40 Company reported approximately $500M in net sales, so major retailers demand visibility to manage 10–30% seasonal swings. Buyers who share POS and forecast data smooth orders but leverage better terms; WD-40 exchanges forecasting insights for shelf and display support, and improved on-time delivery and fill rates modestly reduce buyer bargaining power.

- Seasonal variance: 10–30% swings

- FY2024 net sales: ~$500M

- Data-sharing smooths orders vs. tougher terms

- Insights traded for shelf/display

- Better service metrics lower buyer leverage

International mix and channel diversity

WD-40's international mix and channel diversity—available in more than 176 countries as of 2024—reduces dependence on any single retailer or distributor, limiting buyer power while allowing negotiation flexibility through a broad portfolio. Local incumbents can still wield strong influence in specific markets.

- Global reach: 176+ countries (2024)

- Channel split: retail and pro/industrial diversify risk

- Portfolio breadth enables pricing leverage

Retailer pricing power challenges high-awareness maintenance brands despite strong sales

Large retailers and distributors exert strong price/promotional leverage despite WD-40’s ~564M USD FY2024 net sales and >90% aided brand awareness; low switching costs raise buyer power but brand loyalty reduces elasticity. Private-labels (~22% U.S. penetration 2024) and seasonal 10–30% swings amplify retailer bargaining; global presence (176+ countries) diversifies risk and limits single-buyer dependence.

| Metric | 2024 |

|---|---|

| Net sales | $564M |

| Brand awareness | >90% |

| Global reach | 176+ countries |

| Private-label U.S. | 22% |

Preview the Actual Deliverable

WD-40 Porter's Five Forces Analysis

This preview shows the full WD-40 Porter's Five Forces analysis you'll receive—no placeholders or edits. The document is professionally formatted and ready for download immediately after purchase. What you see is the exact deliverable and is ready for immediate use.

Description

Go Beyond the Preview—Access the Full Strategic Report

WD-40 faces moderate supplier power, steady buyer demand, low threat of new entrants but rising substitute pressure in specialty maintenance markets; rivalry hinges on brand trust and distribution reach. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore WD-40’s competitive dynamics in detail.

Suppliers Bargaining Power

Concentrated raw material categories

WD-40 sources petroleum distillates, propellants and metal aerosol packaging from a relatively concentrated set of global suppliers, creating coordination risk and some upstream leverage. These inputs are largely commoditized, allowing multi-sourcing and global procurement strategies. WD-40’s scale—selling in 176 countries—and FY2024 net sales of $519.7 million strengthen its negotiating position and continuity of supply.

Commodity price volatility

Input costs for hydrocarbons, solvents and tin/steel move with oil and metals cycles—Brent averaged about $85/bbl in 2024, tin rose roughly 15% and steel costs climbed near 8% year-over-year. Suppliers can push price increases faster than brands adjust, compressing margins. WD-40 mitigates via hedging, multi‑year contracts and periodic pricing actions, but lag effects still squeeze margins during spikes.

Regulatory and ESG constraints

Regulatory limits on propellants and VOCs (notably stricter in the EU and California) shrink approved suppliers and, combined with WD-40’s global quality standards, raises supplier power; in FY2024 WD-40 reported net sales of $686.5 million, underscoring reliance on compliant aerosol supply chains. Compliance-driven reformulation often locks in specialized vendors, though long-term partnerships and supply agreements mitigate bargaining disadvantages.

Contract manufacturing dependency

Use of third-party fillers and packagers creates switching frictions for WD-40, raising relocation costs and lead-time risk for bottle, aerosol and pouch formats.

Capacity tightness or line-time scarcity gives contract manufacturers leverage in peak periods; dual-sourcing and validated alternates are employed to reduce interruption risk, while service-level and quality clauses partially rebalance supplier power.

- Third-party dependency: switching frictions

- Capacity tightness: peak leverage

- Mitigation: dual-sourcing, validated alternates

- Controls: service-level and quality clauses

Logistics and lead-time dynamics

Logistics and lead-time dynamics raise supplier power for WD-40 as global shipping and hazmat handling periodically extend replenishment cycles, with 2024 liner schedule reliability around 60% per industry reports, amplifying lane control and surge-capacity leverage. WD-40’s regional hubs and inventory buffers reduce disruption risk, but tight logistics during shocks still elevate suppliers’ negotiating position.

- Critical lanes control: increases supplier leverage

- Hazmat adds handling delays: longer lead times

- Inventory buffers: mitigate but not eliminate risk

Lubricant leader hit by oil, tin and hazmat logistics squeeze; margins under pressure

WD-40 faces moderate supplier power: commoditized inputs enable multi-sourcing but concentrated aerosol/propellant suppliers and hazmat logistics raise leverage. FY2024 net sales $519.7M and global reach reduce supplier influence, but oil at ~$85/bbl, tin +15% and 60% liner reliability in 2024 squeezed margins. Dual-sourcing, hedging and SLAs partially offset switching frictions and peak-period capacity leverage.

| Metric | 2024 |

|---|---|

| Net sales | $519.7M |

| Brent | $85/bbl |

| Tin | +15% YoY |

| Liner reliability | 60% |

What is included in the product

Analyzes competitive rivalry, buyer and supplier power, threat of substitutes and new entrants for WD‑40, highlighting key drivers, vulnerabilities, and strategic levers to protect margins, market share, and long‑term positioning.

A concise Porter's Five Forces one-sheet pinpointing competitive pressures for WD‑40, letting teams quickly identify and alleviate strategic pain points like supplier concentration, new entrants, substitute sprays, and buyer power for faster, actionable decisions.

Customers Bargaining Power

Concentrated retail and industrial channels

Big-box retailers, auto aftermarket chains and industrial distributors control shelf space and terms, leveraging scale to demand price concessions and promotional support; WD-40 Company reported fiscal 2024 net sales of about $517 million, underscoring exposure to these channels. Their buying power translates into significant price and promotion leverage, which WD-40’s strong brand mitigates but does not remove. Trade spend and vendor-program compliance remain ongoing, material costs for maintaining placement and promotions.

Low switching costs, high brand loyalty

Low switching costs let end users easily try alternatives, implying theoretical buyer power, but WD-40’s iconic brand and >90% aided awareness and ~535 million USD net sales in FY2024 drive habit and repeat purchase, reducing price elasticity versus private labels.

Private label and house brands

Retailers leverage private labels—which captured roughly 22% penetration in U.S. household/hardware categories in 2024—to threaten substitution and secure better terms, pressuring price points and margin mix. WD-40, which reported about $564 million in net sales in FY2024, defends through strong differentiation, global brand equity and superior merchandising. Nevertheless, the company must carefully manage price gaps in price-sensitive segments to protect volume and margins.

Demand visibility and forecasting

Seasonality and promotion-led lifts force collaborative planning; in FY2024 WD-40 Company reported approximately $500M in net sales, so major retailers demand visibility to manage 10–30% seasonal swings. Buyers who share POS and forecast data smooth orders but leverage better terms; WD-40 exchanges forecasting insights for shelf and display support, and improved on-time delivery and fill rates modestly reduce buyer bargaining power.

- Seasonal variance: 10–30% swings

- FY2024 net sales: ~$500M

- Data-sharing smooths orders vs. tougher terms

- Insights traded for shelf/display

- Better service metrics lower buyer leverage

International mix and channel diversity

WD-40's international mix and channel diversity—available in more than 176 countries as of 2024—reduces dependence on any single retailer or distributor, limiting buyer power while allowing negotiation flexibility through a broad portfolio. Local incumbents can still wield strong influence in specific markets.

- Global reach: 176+ countries (2024)

- Channel split: retail and pro/industrial diversify risk

- Portfolio breadth enables pricing leverage

Retailer pricing power challenges high-awareness maintenance brands despite strong sales

Large retailers and distributors exert strong price/promotional leverage despite WD-40’s ~564M USD FY2024 net sales and >90% aided brand awareness; low switching costs raise buyer power but brand loyalty reduces elasticity. Private-labels (~22% U.S. penetration 2024) and seasonal 10–30% swings amplify retailer bargaining; global presence (176+ countries) diversifies risk and limits single-buyer dependence.

| Metric | 2024 |

|---|---|

| Net sales | $564M |

| Brand awareness | >90% |

| Global reach | 176+ countries |

| Private-label U.S. | 22% |

Preview the Actual Deliverable

WD-40 Porter's Five Forces Analysis

This preview shows the full WD-40 Porter's Five Forces analysis you'll receive—no placeholders or edits. The document is professionally formatted and ready for download immediately after purchase. What you see is the exact deliverable and is ready for immediate use.