WD-40 PESTLE Analysis

Your Shortcut to Market Insight Starts Here

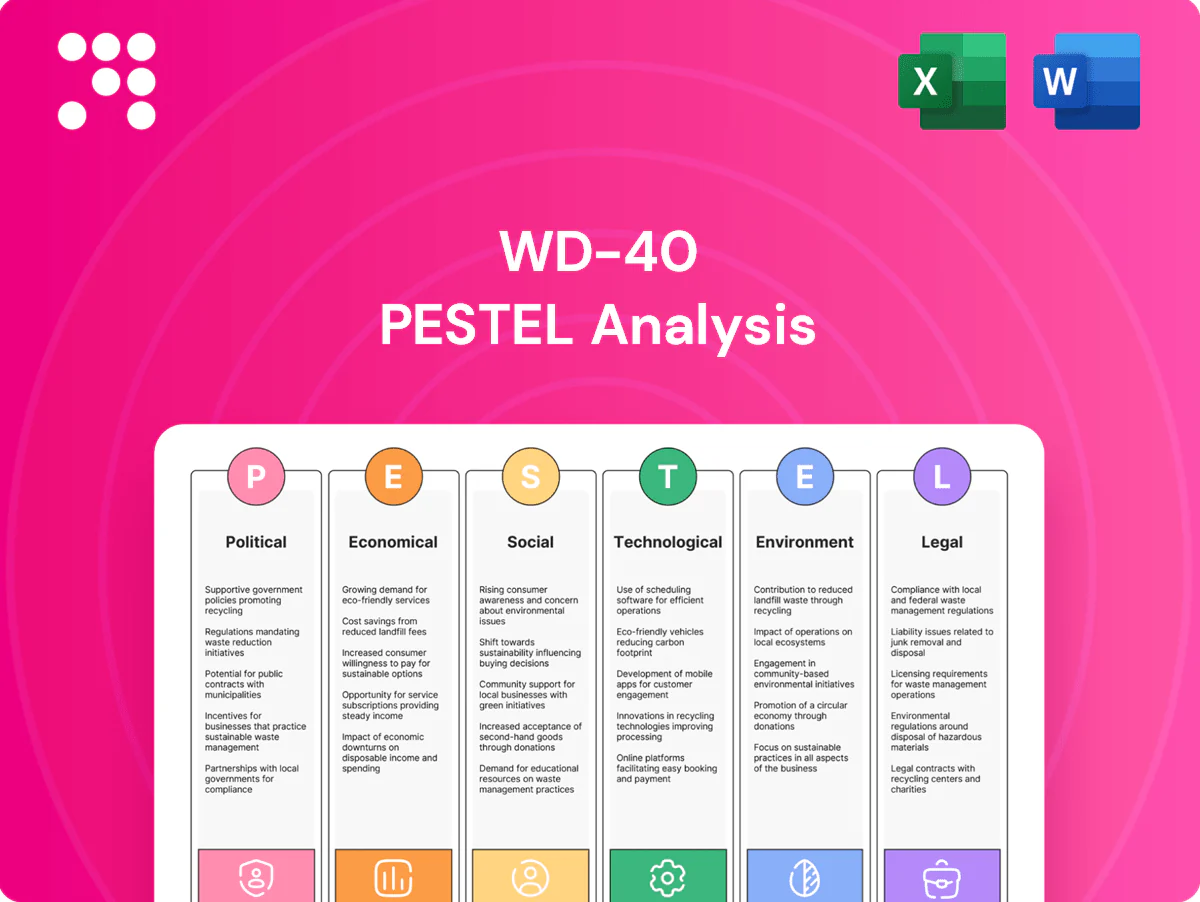

Explore how political regulation, economic cycles, social trends, technological innovation, legal shifts, and environmental pressures shape WD-40’s strategic outlook in our concise PESTLE snapshot. Perfect for investors and strategists, it highlights risks and opportunities you can act on. Purchase the full PESTLE for a complete, ready-to-use briefing and practical recommendations.

Political factors

Trade and tariff volatility

Geopolitical tensions and tariff shifts impact import costs for base oils, solvents and metal cans that WD-40 uses, with U.S. Section 232 tariffs still at 25% for steel and 10% for aluminum, raising aerosol packaging prices and squeezing margins. WD-40 may need to rebalance sourcing, hedge inputs and adjust pricing. Trade agreements or sanctions can quickly open or restrict key market access.

Regulatory nationalism

Local content rules and incentives are driving WD-40 to push regional manufacturing and sourcing to protect market access and margins; the brand is sold in 176 countries, increasing exposure to varying local rules. Aligning operations to qualify for subsidies can lower input costs but raises operational complexity and compliance overhead. Political drives for self-sufficiency strain cross-border supply reliability, so diversifying plants across regions mitigates country risk.

Public procurement priorities

Government maintenance budgets drive institutional demand for lubricants and cleaners, with public procurement accounting for roughly 12% of GDP (OECD). Policy shifts toward sustainability favor low-VOC, eco-label products, and over two-thirds of OECD countries now use environmental criteria in procurement. Vendor qualification and compliance standards create high barriers and onboarding costs. Long multi-year public contracts often stabilize volumes for suppliers.

Customs and border efficiency

Port delays and shifting customs rules have lengthened lead times for aerosols and chemicals, with hazardous-shipment inspections increasingly common and adding measurable per-shipment cost pressure; predictive logistics platforms and bonded warehousing are being adopted to cut friction and holding costs, while consistent, accurate documentation reduces detentions and rework.

- Inspections rise — increases handling costs

- Predictive logistics — lower variability

- Bonded warehousing — faster clearance

- Accurate docs — fewer detentions

Political stability in key markets

Strikes, unrest, or sudden policy changes can interrupt WD-40s distribution network in its operations across more than 176 countries, delaying deliveries and raising logistics costs; currency controls in markets such as Argentina and Nigeria have previously complicated cash repatriation for multinationals. Contingency inventory, multi-distributor models and regional stockpiles improve resilience, while political risk insurance and periodic country risk assessments hedge exposures and protect cash flows.

- Exposure: operations in 176+ countries

- Risk: strikes, unrest, currency controls hinder repatriation

- Mitigation: contingency inventory, multi-distributor model, political risk insurance

Tariffs 25%/10% squeeze aerosol margins; global sales in 176 countries raise regulatory risk

Geopolitical tariffs (US Section 232: steel 25%, aluminum 10%) raise aerosol packaging costs and squeeze margins; WD-40 sells in 176 countries, increasing regulatory exposure. Public procurement ~12% of GDP (OECD) and >66% of OECD countries use environmental criteria, boosting demand for low-VOC products. Currency controls (Argentina, Nigeria) and port inspections raise working capital needs; contingency stock and political-risk insurance are common mitigants.

| Factor | Metric | Impact |

|---|---|---|

| Tariffs | Steel 25% / Al 10% | Higher packaging costs |

| Markets | 176 countries | Regulatory exposure |

| Procurement | ~12% GDP / >66% env criteria | Demand shift to eco-products |

What is included in the product

Explores how macro-environmental forces uniquely affect WD-40 across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-backed trends and region-specific examples; designed to help executives, consultants, and entrepreneurs identify risks, opportunities, and scenario-driven strategic responses.

A concise, visually segmented WD‑40 PESTLE summary that relieves briefing pain points by enabling quick interpretation of external risks and market positioning, ready to drop into presentations for fast team alignment.

Economic factors

Commodity input swings

Base oils, solvents and propellants closely track petrochemical cycles—Brent crude averaged about $85/barrel in 2024, feeding raw-material cost swings that squeeze WD-40s gross margins. Volatility forces dynamic pricing and SKU-level margin management across consumer and industrial channels. Active hedging and supplier diversification have been used to smooth input costs, while rising packaging metal prices (aluminum up ~8% in 2024) add a separate inflation channel.

FX and global demand mix

WD-40 earns significant revenue overseas, so a stronger dollar (DXY ~105 in mid-2024) reduces reported sales and erodes price competitiveness versus local brands.

Costs tied to USD inputs exacerbate margin pressure, though local sourcing and production provide natural hedges that limit FX pass-through.

Robust emerging-market demand—IMF estimated EM growth ~4% in 2024—helps offset saturation in mature markets.

Retailer power and channel shifts

Big-box and e-commerce buyers exert strong price and placement pressure; Amazon accounted for about 40% of US e-commerce sales in 2024, sharpening retailer leverage over brands. Growing private-label penetration—store brands hold roughly 18% of US grocery sales—intensifies competition for WD-40. Direct-to-consumer can boost gross margins but requires marketing investment as global digital ad spend reached about $645 billion in 2024. Omni-channel execution helps protect shelf and online share.

Cycle sensitivity

Industrial maintenance demand tracks manufacturing cycles, so WD-40 sales are cyclical; the company reported fiscal 2024 net sales of about $548.9 million, reflecting sensitivity to end‑market activity. DIY and home‑improvement sales rise with housing turnover and renovations, supporting consumer segment volumes. In downturns repair‑and‑extend behavior cushions lubricant usage, though channel and product mix shifts can compress margins and alter profitability.

- Manufacturing-linked demand: cyclical

- Consumer DIY: propped by housing activity

- Downturns: repair‑and‑extend supports volumes

- Mix shifts: margin/ profit impact

Logistics and labor costs

Freight rates, warehousing and tight labor markets drive WD-40s delivered cost; US logistics ran about 7.6% of GDP in 2023 and manufacturing wage growth was ~5–6% YoY in 2024. Nearshoring trims transit time and risk but can raise unit costs roughly 5–15%. Automation lifts throughput and quality with typical payback of 2–4 years; network optimization can cut transport spend 5–12% while preserving service.

- Freight volatility: affects COGS and margins

- Warehousing: higher occupancy raises per-unit cost

- Nearshoring: +5–15% unit cost, lower lead time

- Automation/optimization: improves OEE, cuts transport 5–12%

Tariffs 25%/10% squeeze aerosol margins; global sales in 176 countries raise regulatory risk

Petrochemical-linked input swings (Brent ~$85/bbl in 2024) and aluminum +8% pressure gross margins, forcing dynamic pricing and hedging. FX (DXY ~105 mid‑2024) and USD‑priced inputs weigh on reported overseas revenue; FY2024 sales ~$548.9M. EM growth (~4% in 2024) and e‑commerce (Amazon ~40% of US e‑commerce) offset mature‑market softness.

| Metric | Value (2024) |

|---|---|

| Brent | $85/bbl |

| DXY | ~105 |

| Aluminum | +8% |

| FY Sales | $548.9M |

| EM GDP | ~4% |

| Amazon US e‑comm | ~40% |

Full Version Awaits

WD-40 PESTLE Analysis

The preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use. This WD-40 PESTLE Analysis provides concise political, economic, social, technological, legal and environmental insights to support strategic decisions and investment evaluation. The layout, content, and structure visible here are exactly what you’ll be able to download immediately after buying.

Your Shortcut to Market Insight Starts Here

Explore how political regulation, economic cycles, social trends, technological innovation, legal shifts, and environmental pressures shape WD-40’s strategic outlook in our concise PESTLE snapshot. Perfect for investors and strategists, it highlights risks and opportunities you can act on. Purchase the full PESTLE for a complete, ready-to-use briefing and practical recommendations.

Political factors

Trade and tariff volatility

Geopolitical tensions and tariff shifts impact import costs for base oils, solvents and metal cans that WD-40 uses, with U.S. Section 232 tariffs still at 25% for steel and 10% for aluminum, raising aerosol packaging prices and squeezing margins. WD-40 may need to rebalance sourcing, hedge inputs and adjust pricing. Trade agreements or sanctions can quickly open or restrict key market access.

Regulatory nationalism

Local content rules and incentives are driving WD-40 to push regional manufacturing and sourcing to protect market access and margins; the brand is sold in 176 countries, increasing exposure to varying local rules. Aligning operations to qualify for subsidies can lower input costs but raises operational complexity and compliance overhead. Political drives for self-sufficiency strain cross-border supply reliability, so diversifying plants across regions mitigates country risk.

Public procurement priorities

Government maintenance budgets drive institutional demand for lubricants and cleaners, with public procurement accounting for roughly 12% of GDP (OECD). Policy shifts toward sustainability favor low-VOC, eco-label products, and over two-thirds of OECD countries now use environmental criteria in procurement. Vendor qualification and compliance standards create high barriers and onboarding costs. Long multi-year public contracts often stabilize volumes for suppliers.

Customs and border efficiency

Port delays and shifting customs rules have lengthened lead times for aerosols and chemicals, with hazardous-shipment inspections increasingly common and adding measurable per-shipment cost pressure; predictive logistics platforms and bonded warehousing are being adopted to cut friction and holding costs, while consistent, accurate documentation reduces detentions and rework.

- Inspections rise — increases handling costs

- Predictive logistics — lower variability

- Bonded warehousing — faster clearance

- Accurate docs — fewer detentions

Political stability in key markets

Strikes, unrest, or sudden policy changes can interrupt WD-40s distribution network in its operations across more than 176 countries, delaying deliveries and raising logistics costs; currency controls in markets such as Argentina and Nigeria have previously complicated cash repatriation for multinationals. Contingency inventory, multi-distributor models and regional stockpiles improve resilience, while political risk insurance and periodic country risk assessments hedge exposures and protect cash flows.

- Exposure: operations in 176+ countries

- Risk: strikes, unrest, currency controls hinder repatriation

- Mitigation: contingency inventory, multi-distributor model, political risk insurance

Tariffs 25%/10% squeeze aerosol margins; global sales in 176 countries raise regulatory risk

Geopolitical tariffs (US Section 232: steel 25%, aluminum 10%) raise aerosol packaging costs and squeeze margins; WD-40 sells in 176 countries, increasing regulatory exposure. Public procurement ~12% of GDP (OECD) and >66% of OECD countries use environmental criteria, boosting demand for low-VOC products. Currency controls (Argentina, Nigeria) and port inspections raise working capital needs; contingency stock and political-risk insurance are common mitigants.

| Factor | Metric | Impact |

|---|---|---|

| Tariffs | Steel 25% / Al 10% | Higher packaging costs |

| Markets | 176 countries | Regulatory exposure |

| Procurement | ~12% GDP / >66% env criteria | Demand shift to eco-products |

What is included in the product

Explores how macro-environmental forces uniquely affect WD-40 across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-backed trends and region-specific examples; designed to help executives, consultants, and entrepreneurs identify risks, opportunities, and scenario-driven strategic responses.

A concise, visually segmented WD‑40 PESTLE summary that relieves briefing pain points by enabling quick interpretation of external risks and market positioning, ready to drop into presentations for fast team alignment.

Economic factors

Commodity input swings

Base oils, solvents and propellants closely track petrochemical cycles—Brent crude averaged about $85/barrel in 2024, feeding raw-material cost swings that squeeze WD-40s gross margins. Volatility forces dynamic pricing and SKU-level margin management across consumer and industrial channels. Active hedging and supplier diversification have been used to smooth input costs, while rising packaging metal prices (aluminum up ~8% in 2024) add a separate inflation channel.

FX and global demand mix

WD-40 earns significant revenue overseas, so a stronger dollar (DXY ~105 in mid-2024) reduces reported sales and erodes price competitiveness versus local brands.

Costs tied to USD inputs exacerbate margin pressure, though local sourcing and production provide natural hedges that limit FX pass-through.

Robust emerging-market demand—IMF estimated EM growth ~4% in 2024—helps offset saturation in mature markets.

Retailer power and channel shifts

Big-box and e-commerce buyers exert strong price and placement pressure; Amazon accounted for about 40% of US e-commerce sales in 2024, sharpening retailer leverage over brands. Growing private-label penetration—store brands hold roughly 18% of US grocery sales—intensifies competition for WD-40. Direct-to-consumer can boost gross margins but requires marketing investment as global digital ad spend reached about $645 billion in 2024. Omni-channel execution helps protect shelf and online share.

Cycle sensitivity

Industrial maintenance demand tracks manufacturing cycles, so WD-40 sales are cyclical; the company reported fiscal 2024 net sales of about $548.9 million, reflecting sensitivity to end‑market activity. DIY and home‑improvement sales rise with housing turnover and renovations, supporting consumer segment volumes. In downturns repair‑and‑extend behavior cushions lubricant usage, though channel and product mix shifts can compress margins and alter profitability.

- Manufacturing-linked demand: cyclical

- Consumer DIY: propped by housing activity

- Downturns: repair‑and‑extend supports volumes

- Mix shifts: margin/ profit impact

Logistics and labor costs

Freight rates, warehousing and tight labor markets drive WD-40s delivered cost; US logistics ran about 7.6% of GDP in 2023 and manufacturing wage growth was ~5–6% YoY in 2024. Nearshoring trims transit time and risk but can raise unit costs roughly 5–15%. Automation lifts throughput and quality with typical payback of 2–4 years; network optimization can cut transport spend 5–12% while preserving service.

- Freight volatility: affects COGS and margins

- Warehousing: higher occupancy raises per-unit cost

- Nearshoring: +5–15% unit cost, lower lead time

- Automation/optimization: improves OEE, cuts transport 5–12%

Tariffs 25%/10% squeeze aerosol margins; global sales in 176 countries raise regulatory risk

Petrochemical-linked input swings (Brent ~$85/bbl in 2024) and aluminum +8% pressure gross margins, forcing dynamic pricing and hedging. FX (DXY ~105 mid‑2024) and USD‑priced inputs weigh on reported overseas revenue; FY2024 sales ~$548.9M. EM growth (~4% in 2024) and e‑commerce (Amazon ~40% of US e‑commerce) offset mature‑market softness.

| Metric | Value (2024) |

|---|---|

| Brent | $85/bbl |

| DXY | ~105 |

| Aluminum | +8% |

| FY Sales | $548.9M |

| EM GDP | ~4% |

| Amazon US e‑comm | ~40% |

Full Version Awaits

WD-40 PESTLE Analysis

The preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use. This WD-40 PESTLE Analysis provides concise political, economic, social, technological, legal and environmental insights to support strategic decisions and investment evaluation. The layout, content, and structure visible here are exactly what you’ll be able to download immediately after buying.

Original: $10.00

-65%$10.00

$3.50Description

Your Shortcut to Market Insight Starts Here

Explore how political regulation, economic cycles, social trends, technological innovation, legal shifts, and environmental pressures shape WD-40’s strategic outlook in our concise PESTLE snapshot. Perfect for investors and strategists, it highlights risks and opportunities you can act on. Purchase the full PESTLE for a complete, ready-to-use briefing and practical recommendations.

Political factors

Trade and tariff volatility

Geopolitical tensions and tariff shifts impact import costs for base oils, solvents and metal cans that WD-40 uses, with U.S. Section 232 tariffs still at 25% for steel and 10% for aluminum, raising aerosol packaging prices and squeezing margins. WD-40 may need to rebalance sourcing, hedge inputs and adjust pricing. Trade agreements or sanctions can quickly open or restrict key market access.

Regulatory nationalism

Local content rules and incentives are driving WD-40 to push regional manufacturing and sourcing to protect market access and margins; the brand is sold in 176 countries, increasing exposure to varying local rules. Aligning operations to qualify for subsidies can lower input costs but raises operational complexity and compliance overhead. Political drives for self-sufficiency strain cross-border supply reliability, so diversifying plants across regions mitigates country risk.

Public procurement priorities

Government maintenance budgets drive institutional demand for lubricants and cleaners, with public procurement accounting for roughly 12% of GDP (OECD). Policy shifts toward sustainability favor low-VOC, eco-label products, and over two-thirds of OECD countries now use environmental criteria in procurement. Vendor qualification and compliance standards create high barriers and onboarding costs. Long multi-year public contracts often stabilize volumes for suppliers.

Customs and border efficiency

Port delays and shifting customs rules have lengthened lead times for aerosols and chemicals, with hazardous-shipment inspections increasingly common and adding measurable per-shipment cost pressure; predictive logistics platforms and bonded warehousing are being adopted to cut friction and holding costs, while consistent, accurate documentation reduces detentions and rework.

- Inspections rise — increases handling costs

- Predictive logistics — lower variability

- Bonded warehousing — faster clearance

- Accurate docs — fewer detentions

Political stability in key markets

Strikes, unrest, or sudden policy changes can interrupt WD-40s distribution network in its operations across more than 176 countries, delaying deliveries and raising logistics costs; currency controls in markets such as Argentina and Nigeria have previously complicated cash repatriation for multinationals. Contingency inventory, multi-distributor models and regional stockpiles improve resilience, while political risk insurance and periodic country risk assessments hedge exposures and protect cash flows.

- Exposure: operations in 176+ countries

- Risk: strikes, unrest, currency controls hinder repatriation

- Mitigation: contingency inventory, multi-distributor model, political risk insurance

Tariffs 25%/10% squeeze aerosol margins; global sales in 176 countries raise regulatory risk

Geopolitical tariffs (US Section 232: steel 25%, aluminum 10%) raise aerosol packaging costs and squeeze margins; WD-40 sells in 176 countries, increasing regulatory exposure. Public procurement ~12% of GDP (OECD) and >66% of OECD countries use environmental criteria, boosting demand for low-VOC products. Currency controls (Argentina, Nigeria) and port inspections raise working capital needs; contingency stock and political-risk insurance are common mitigants.

| Factor | Metric | Impact |

|---|---|---|

| Tariffs | Steel 25% / Al 10% | Higher packaging costs |

| Markets | 176 countries | Regulatory exposure |

| Procurement | ~12% GDP / >66% env criteria | Demand shift to eco-products |

What is included in the product

Explores how macro-environmental forces uniquely affect WD-40 across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-backed trends and region-specific examples; designed to help executives, consultants, and entrepreneurs identify risks, opportunities, and scenario-driven strategic responses.

A concise, visually segmented WD‑40 PESTLE summary that relieves briefing pain points by enabling quick interpretation of external risks and market positioning, ready to drop into presentations for fast team alignment.

Economic factors

Commodity input swings

Base oils, solvents and propellants closely track petrochemical cycles—Brent crude averaged about $85/barrel in 2024, feeding raw-material cost swings that squeeze WD-40s gross margins. Volatility forces dynamic pricing and SKU-level margin management across consumer and industrial channels. Active hedging and supplier diversification have been used to smooth input costs, while rising packaging metal prices (aluminum up ~8% in 2024) add a separate inflation channel.

FX and global demand mix

WD-40 earns significant revenue overseas, so a stronger dollar (DXY ~105 in mid-2024) reduces reported sales and erodes price competitiveness versus local brands.

Costs tied to USD inputs exacerbate margin pressure, though local sourcing and production provide natural hedges that limit FX pass-through.

Robust emerging-market demand—IMF estimated EM growth ~4% in 2024—helps offset saturation in mature markets.

Retailer power and channel shifts

Big-box and e-commerce buyers exert strong price and placement pressure; Amazon accounted for about 40% of US e-commerce sales in 2024, sharpening retailer leverage over brands. Growing private-label penetration—store brands hold roughly 18% of US grocery sales—intensifies competition for WD-40. Direct-to-consumer can boost gross margins but requires marketing investment as global digital ad spend reached about $645 billion in 2024. Omni-channel execution helps protect shelf and online share.

Cycle sensitivity

Industrial maintenance demand tracks manufacturing cycles, so WD-40 sales are cyclical; the company reported fiscal 2024 net sales of about $548.9 million, reflecting sensitivity to end‑market activity. DIY and home‑improvement sales rise with housing turnover and renovations, supporting consumer segment volumes. In downturns repair‑and‑extend behavior cushions lubricant usage, though channel and product mix shifts can compress margins and alter profitability.

- Manufacturing-linked demand: cyclical

- Consumer DIY: propped by housing activity

- Downturns: repair‑and‑extend supports volumes

- Mix shifts: margin/ profit impact

Logistics and labor costs

Freight rates, warehousing and tight labor markets drive WD-40s delivered cost; US logistics ran about 7.6% of GDP in 2023 and manufacturing wage growth was ~5–6% YoY in 2024. Nearshoring trims transit time and risk but can raise unit costs roughly 5–15%. Automation lifts throughput and quality with typical payback of 2–4 years; network optimization can cut transport spend 5–12% while preserving service.

- Freight volatility: affects COGS and margins

- Warehousing: higher occupancy raises per-unit cost

- Nearshoring: +5–15% unit cost, lower lead time

- Automation/optimization: improves OEE, cuts transport 5–12%

Tariffs 25%/10% squeeze aerosol margins; global sales in 176 countries raise regulatory risk

Petrochemical-linked input swings (Brent ~$85/bbl in 2024) and aluminum +8% pressure gross margins, forcing dynamic pricing and hedging. FX (DXY ~105 mid‑2024) and USD‑priced inputs weigh on reported overseas revenue; FY2024 sales ~$548.9M. EM growth (~4% in 2024) and e‑commerce (Amazon ~40% of US e‑commerce) offset mature‑market softness.

| Metric | Value (2024) |

|---|---|

| Brent | $85/bbl |

| DXY | ~105 |

| Aluminum | +8% |

| FY Sales | $548.9M |

| EM GDP | ~4% |

| Amazon US e‑comm | ~40% |

Full Version Awaits

WD-40 PESTLE Analysis

The preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use. This WD-40 PESTLE Analysis provides concise political, economic, social, technological, legal and environmental insights to support strategic decisions and investment evaluation. The layout, content, and structure visible here are exactly what you’ll be able to download immediately after buying.