WD-40 SWOT Analysis

Go Beyond the Preview—Access the Full Strategic Report

WD-40’s brand strength, global distribution and loyal customer base shield it from many competitors, but reliance on a narrow product range and exposure to commodity and currency swings present risks. Our detailed SWOT uncovers growth levers, competitive threats, and strategic options. Purchase the full SWOT for an editable, investor-ready report to guide decisions and planning.

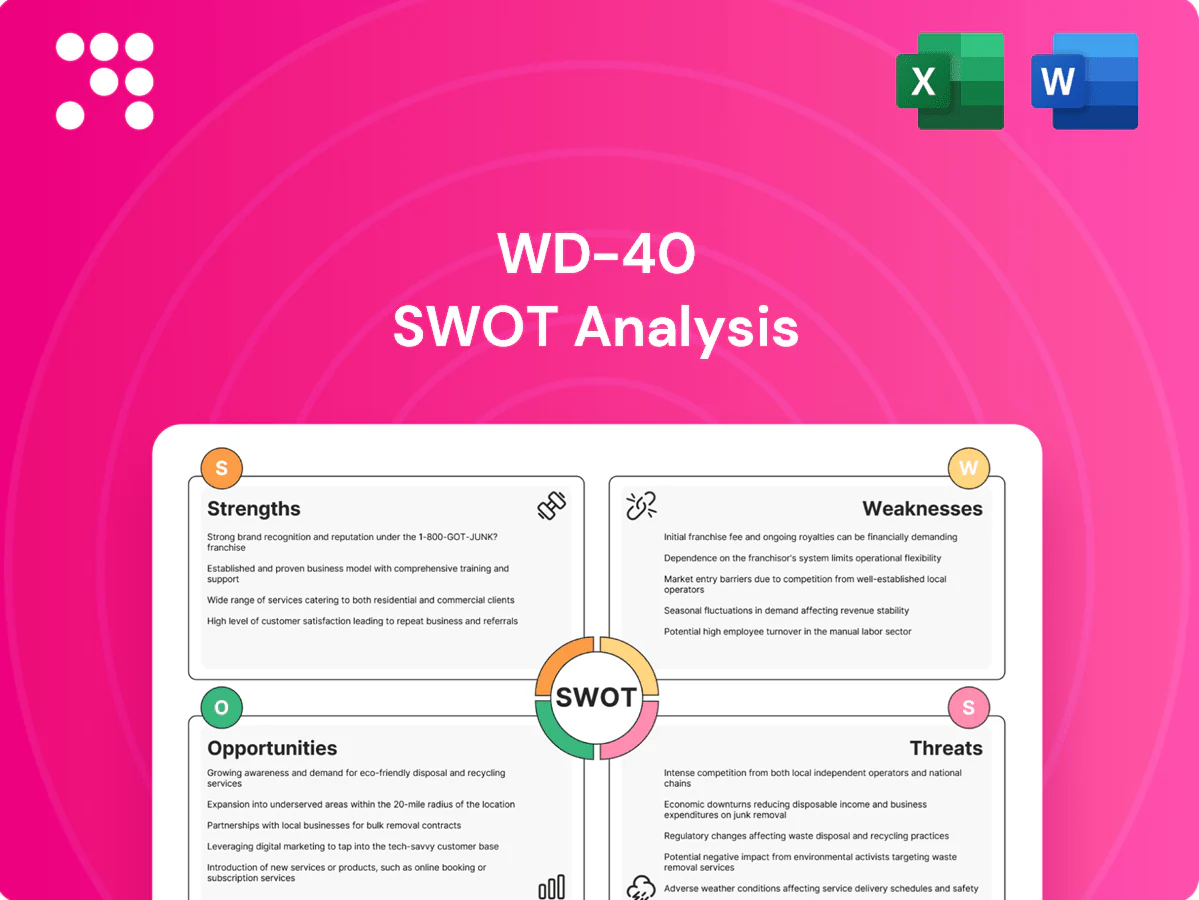

Strengths

Iconic brand equity

WD-40, founded in 1953, has a 72-year heritage and is sold in more than 176 countries, making it synonymous with multi-purpose lubrication and strong top-of-mind awareness. This iconic equity enables premium pricing and shelf prominence across retailers and lowers customer acquisition costs. High brand recall accelerates international market entry and distribution partnerships. Decades of consistent product performance and storytelling reinforce trust and repeat purchase.

Global distribution reach

Founded in 1953, WD-40 sells across developed and emerging markets via retail, e-commerce and professional channels, with products available in more than 176 countries. Long-standing distributor relationships secure resilient shelf space and consistent market access. Broad geographic exposure evens out regional and cyclical demand swings. This global footprint enables efficient rollouts of line extensions and channel-specific innovations.

Versatile hero product

WD-40's flagship spray addresses lubrication, rust prevention and moisture displacement, driving frequent repeat use and simplifying purchase decisions. Sold in over 176 countries since 1953, its multi-functionality reduces substitution and supports brand extensions into adjacent categories. This recurring utility contributes to strong unit economics and sustained pricing power.

Lean, asset-light model

Outsourced manufacturing and focused operations support healthy cash flow and strong return on invested capital by keeping capital expenditures low, enabling WD-40 to prioritize marketing and brand investment. The asset-light model allows rapid scaling of production to match demand and reduces operational fixed-cost exposure. Lower capital intensity also helps sustain shareholder returns and provides flexibility to manage risk during downturns.

- Outsourced manufacturing: lower CAPEX

- Agility: scalable production

- Returns: steady shareholder payouts

- Risk: better downside protection

Diverse portfolio adjacencies

Beyond its core lubricant, WD-40 offers cleaning and maintenance ranges serving DIY consumers and trade/professional users, available in more than 176 countries. Cross-selling across WD-40 Specialist and maintenance SKUs broadens basket size and increases stickiness with trade accounts. The portfolio supports channel breadth from mass retail to industrial supply and helps mitigate single-category seasonal swings.

- Channel reach: >176 countries

- Customer mix: consumer + professional trade

- Commercial stickiness: higher basket size via cross-sell

- Risk mitigation: reduces single-category seasonality

72-year multi-use spray, in 176+ countries

WD-40, founded in 1953, has a 72-year heritage and presence in more than 176 countries, driving premium pricing and top-of-mind awareness. Its flagship multi-use spray delivers frequent repeat purchases and enables cross-sell into Specialist and maintenance SKUs. An asset-light, outsourced manufacturing model keeps CAPEX low and supports steady returns.

| Metric | Value |

|---|---|

| Founded | 1953 |

| Global presence | 176+ countries |

| Heritage | 72 years (1953–2025) |

What is included in the product

Provides a concise SWOT analysis of WD-40, highlighting strong brand equity, global distribution and product-extension potential alongside vulnerabilities like reliance on core SKUs and commodity exposure; identifies growth opportunities in emerging markets and adjacent categories and threats from private-label competition, changing retail channels, and evolving consumer preferences.

Provides a concise SWOT matrix to quickly pinpoint WD‑40’s strategic pain points—strengths to leverage, weaknesses to fix, opportunities to pursue, and threats to mitigate for faster decision-making.

Weaknesses

Product concentration

Revenue is highly dependent on the flagship WD-40 Multi-Use SKU, with the company reporting fiscal 2024 net sales of about $558.6 million, concentrating risk in a single formula and brand. A disruption, recall, or reputation issue could disproportionately cut sales and margins. Concentration also limits negotiating leverage with large retailers. Meaningful diversification will require sustained R&D, M&A and marketing investment over multiple years.

Limited scale vs FMCG giants

Compared with FMCG giants, WD-40 operates with far smaller marketing budgets and weaker retail bargaining power, limiting national media reach and in‑store promotion frequency.

For context, Procter & Gamble spent about $8.1 billion on advertising in FY2023 and Unilever roughly €6–7 billion, sums WD-40 cannot match.

That gap allows competitors to outspend on innovation and shopper marketing and can translate into higher per‑unit procurement costs for WD-40.

Exposure to petrochemicals

Core WD-40 formulations rely on petroleum-derived inputs and aerosol propellants, leaving cost structure tied to hydrocarbon markets. Price volatility in 2024 squeezed industrial suppliers and can compress WD-40 margins and complicate pricing for distributors. Growing eco-conscious consumer segments increasingly view petrochemical-based aerosols negatively, risking demand shifts. Anticipated regulatory changes on VOCs and single-use aerosols could force reformulation and capital spending.

Narrow R&D pipeline

The brand’s success reduces urgency to innovate, with the Multi-Use Product still accounting for over half of WD-40 Company sales, which can limit breakthrough launches and keep R&D focused on incremental extensions.

Overreliance on the hero product slows category learning and diversification, making the company vulnerable to disruptive entrants with novel chemistries or business models.

- Concentration: hero product >50% sales

- R&D focus: incremental extensions

- Risk: exposure to disruptive entrants

Retailer dependence

Mass retail and hardware channels exert outsized control over WD-40 placement and pricing, pressuring promotional terms and contributing to margin compression as private-label share in U.S. grocery and consumables approached ~18% in 2023–24 (NielsenIQ). Slotting fees and trade spend are required to defend shelf space; shelf resets can erode visibility if not funded. Concentration in key accounts increases counterparty risk.

- Retailer influence on pricing/placement

- Private label pressure (~18% PL share 2023–24)

- Slotting fees/trade spend compress margins

- Key-account concentration = counterparty risk

Flagship SKU >50% of $558.6M; limited ad spend; VOC/hydrocarbon risk

WD-40 depends on its flagship SKU (>50% of fiscal 2024 sales; net sales $558.6M), concentrating operational and brand risk. Limited marketing spend versus FMCG giants (P&G $8.1B ad spend FY2023) reduces reach and retail leverage. Petroleum-based aerosols tie costs to hydrocarbon volatility and regulatory VOC exposure.

| Metric | Value |

|---|---|

| Net sales FY2024 | $558.6M |

| Hero SKU share | >50% |

| US private label | ~18% |

Preview the Actual Deliverable

WD-40 SWOT Analysis

This is the actual WD-40 SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full report you'll get, and purchase unlocks the complete, editable version. You’re viewing a live excerpt of the real file; the entire, detailed document becomes available immediately after checkout.

Go Beyond the Preview—Access the Full Strategic Report

WD-40’s brand strength, global distribution and loyal customer base shield it from many competitors, but reliance on a narrow product range and exposure to commodity and currency swings present risks. Our detailed SWOT uncovers growth levers, competitive threats, and strategic options. Purchase the full SWOT for an editable, investor-ready report to guide decisions and planning.

Strengths

Iconic brand equity

WD-40, founded in 1953, has a 72-year heritage and is sold in more than 176 countries, making it synonymous with multi-purpose lubrication and strong top-of-mind awareness. This iconic equity enables premium pricing and shelf prominence across retailers and lowers customer acquisition costs. High brand recall accelerates international market entry and distribution partnerships. Decades of consistent product performance and storytelling reinforce trust and repeat purchase.

Global distribution reach

Founded in 1953, WD-40 sells across developed and emerging markets via retail, e-commerce and professional channels, with products available in more than 176 countries. Long-standing distributor relationships secure resilient shelf space and consistent market access. Broad geographic exposure evens out regional and cyclical demand swings. This global footprint enables efficient rollouts of line extensions and channel-specific innovations.

Versatile hero product

WD-40's flagship spray addresses lubrication, rust prevention and moisture displacement, driving frequent repeat use and simplifying purchase decisions. Sold in over 176 countries since 1953, its multi-functionality reduces substitution and supports brand extensions into adjacent categories. This recurring utility contributes to strong unit economics and sustained pricing power.

Lean, asset-light model

Outsourced manufacturing and focused operations support healthy cash flow and strong return on invested capital by keeping capital expenditures low, enabling WD-40 to prioritize marketing and brand investment. The asset-light model allows rapid scaling of production to match demand and reduces operational fixed-cost exposure. Lower capital intensity also helps sustain shareholder returns and provides flexibility to manage risk during downturns.

- Outsourced manufacturing: lower CAPEX

- Agility: scalable production

- Returns: steady shareholder payouts

- Risk: better downside protection

Diverse portfolio adjacencies

Beyond its core lubricant, WD-40 offers cleaning and maintenance ranges serving DIY consumers and trade/professional users, available in more than 176 countries. Cross-selling across WD-40 Specialist and maintenance SKUs broadens basket size and increases stickiness with trade accounts. The portfolio supports channel breadth from mass retail to industrial supply and helps mitigate single-category seasonal swings.

- Channel reach: >176 countries

- Customer mix: consumer + professional trade

- Commercial stickiness: higher basket size via cross-sell

- Risk mitigation: reduces single-category seasonality

72-year multi-use spray, in 176+ countries

WD-40, founded in 1953, has a 72-year heritage and presence in more than 176 countries, driving premium pricing and top-of-mind awareness. Its flagship multi-use spray delivers frequent repeat purchases and enables cross-sell into Specialist and maintenance SKUs. An asset-light, outsourced manufacturing model keeps CAPEX low and supports steady returns.

| Metric | Value |

|---|---|

| Founded | 1953 |

| Global presence | 176+ countries |

| Heritage | 72 years (1953–2025) |

What is included in the product

Provides a concise SWOT analysis of WD-40, highlighting strong brand equity, global distribution and product-extension potential alongside vulnerabilities like reliance on core SKUs and commodity exposure; identifies growth opportunities in emerging markets and adjacent categories and threats from private-label competition, changing retail channels, and evolving consumer preferences.

Provides a concise SWOT matrix to quickly pinpoint WD‑40’s strategic pain points—strengths to leverage, weaknesses to fix, opportunities to pursue, and threats to mitigate for faster decision-making.

Weaknesses

Product concentration

Revenue is highly dependent on the flagship WD-40 Multi-Use SKU, with the company reporting fiscal 2024 net sales of about $558.6 million, concentrating risk in a single formula and brand. A disruption, recall, or reputation issue could disproportionately cut sales and margins. Concentration also limits negotiating leverage with large retailers. Meaningful diversification will require sustained R&D, M&A and marketing investment over multiple years.

Limited scale vs FMCG giants

Compared with FMCG giants, WD-40 operates with far smaller marketing budgets and weaker retail bargaining power, limiting national media reach and in‑store promotion frequency.

For context, Procter & Gamble spent about $8.1 billion on advertising in FY2023 and Unilever roughly €6–7 billion, sums WD-40 cannot match.

That gap allows competitors to outspend on innovation and shopper marketing and can translate into higher per‑unit procurement costs for WD-40.

Exposure to petrochemicals

Core WD-40 formulations rely on petroleum-derived inputs and aerosol propellants, leaving cost structure tied to hydrocarbon markets. Price volatility in 2024 squeezed industrial suppliers and can compress WD-40 margins and complicate pricing for distributors. Growing eco-conscious consumer segments increasingly view petrochemical-based aerosols negatively, risking demand shifts. Anticipated regulatory changes on VOCs and single-use aerosols could force reformulation and capital spending.

Narrow R&D pipeline

The brand’s success reduces urgency to innovate, with the Multi-Use Product still accounting for over half of WD-40 Company sales, which can limit breakthrough launches and keep R&D focused on incremental extensions.

Overreliance on the hero product slows category learning and diversification, making the company vulnerable to disruptive entrants with novel chemistries or business models.

- Concentration: hero product >50% sales

- R&D focus: incremental extensions

- Risk: exposure to disruptive entrants

Retailer dependence

Mass retail and hardware channels exert outsized control over WD-40 placement and pricing, pressuring promotional terms and contributing to margin compression as private-label share in U.S. grocery and consumables approached ~18% in 2023–24 (NielsenIQ). Slotting fees and trade spend are required to defend shelf space; shelf resets can erode visibility if not funded. Concentration in key accounts increases counterparty risk.

- Retailer influence on pricing/placement

- Private label pressure (~18% PL share 2023–24)

- Slotting fees/trade spend compress margins

- Key-account concentration = counterparty risk

Flagship SKU >50% of $558.6M; limited ad spend; VOC/hydrocarbon risk

WD-40 depends on its flagship SKU (>50% of fiscal 2024 sales; net sales $558.6M), concentrating operational and brand risk. Limited marketing spend versus FMCG giants (P&G $8.1B ad spend FY2023) reduces reach and retail leverage. Petroleum-based aerosols tie costs to hydrocarbon volatility and regulatory VOC exposure.

| Metric | Value |

|---|---|

| Net sales FY2024 | $558.6M |

| Hero SKU share | >50% |

| US private label | ~18% |

Preview the Actual Deliverable

WD-40 SWOT Analysis

This is the actual WD-40 SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full report you'll get, and purchase unlocks the complete, editable version. You’re viewing a live excerpt of the real file; the entire, detailed document becomes available immediately after checkout.

Original: $10.00

-65%$10.00

$3.50Description

Go Beyond the Preview—Access the Full Strategic Report

WD-40’s brand strength, global distribution and loyal customer base shield it from many competitors, but reliance on a narrow product range and exposure to commodity and currency swings present risks. Our detailed SWOT uncovers growth levers, competitive threats, and strategic options. Purchase the full SWOT for an editable, investor-ready report to guide decisions and planning.

Strengths

Iconic brand equity

WD-40, founded in 1953, has a 72-year heritage and is sold in more than 176 countries, making it synonymous with multi-purpose lubrication and strong top-of-mind awareness. This iconic equity enables premium pricing and shelf prominence across retailers and lowers customer acquisition costs. High brand recall accelerates international market entry and distribution partnerships. Decades of consistent product performance and storytelling reinforce trust and repeat purchase.

Global distribution reach

Founded in 1953, WD-40 sells across developed and emerging markets via retail, e-commerce and professional channels, with products available in more than 176 countries. Long-standing distributor relationships secure resilient shelf space and consistent market access. Broad geographic exposure evens out regional and cyclical demand swings. This global footprint enables efficient rollouts of line extensions and channel-specific innovations.

Versatile hero product

WD-40's flagship spray addresses lubrication, rust prevention and moisture displacement, driving frequent repeat use and simplifying purchase decisions. Sold in over 176 countries since 1953, its multi-functionality reduces substitution and supports brand extensions into adjacent categories. This recurring utility contributes to strong unit economics and sustained pricing power.

Lean, asset-light model

Outsourced manufacturing and focused operations support healthy cash flow and strong return on invested capital by keeping capital expenditures low, enabling WD-40 to prioritize marketing and brand investment. The asset-light model allows rapid scaling of production to match demand and reduces operational fixed-cost exposure. Lower capital intensity also helps sustain shareholder returns and provides flexibility to manage risk during downturns.

- Outsourced manufacturing: lower CAPEX

- Agility: scalable production

- Returns: steady shareholder payouts

- Risk: better downside protection

Diverse portfolio adjacencies

Beyond its core lubricant, WD-40 offers cleaning and maintenance ranges serving DIY consumers and trade/professional users, available in more than 176 countries. Cross-selling across WD-40 Specialist and maintenance SKUs broadens basket size and increases stickiness with trade accounts. The portfolio supports channel breadth from mass retail to industrial supply and helps mitigate single-category seasonal swings.

- Channel reach: >176 countries

- Customer mix: consumer + professional trade

- Commercial stickiness: higher basket size via cross-sell

- Risk mitigation: reduces single-category seasonality

72-year multi-use spray, in 176+ countries

WD-40, founded in 1953, has a 72-year heritage and presence in more than 176 countries, driving premium pricing and top-of-mind awareness. Its flagship multi-use spray delivers frequent repeat purchases and enables cross-sell into Specialist and maintenance SKUs. An asset-light, outsourced manufacturing model keeps CAPEX low and supports steady returns.

| Metric | Value |

|---|---|

| Founded | 1953 |

| Global presence | 176+ countries |

| Heritage | 72 years (1953–2025) |

What is included in the product

Provides a concise SWOT analysis of WD-40, highlighting strong brand equity, global distribution and product-extension potential alongside vulnerabilities like reliance on core SKUs and commodity exposure; identifies growth opportunities in emerging markets and adjacent categories and threats from private-label competition, changing retail channels, and evolving consumer preferences.

Provides a concise SWOT matrix to quickly pinpoint WD‑40’s strategic pain points—strengths to leverage, weaknesses to fix, opportunities to pursue, and threats to mitigate for faster decision-making.

Weaknesses

Product concentration

Revenue is highly dependent on the flagship WD-40 Multi-Use SKU, with the company reporting fiscal 2024 net sales of about $558.6 million, concentrating risk in a single formula and brand. A disruption, recall, or reputation issue could disproportionately cut sales and margins. Concentration also limits negotiating leverage with large retailers. Meaningful diversification will require sustained R&D, M&A and marketing investment over multiple years.

Limited scale vs FMCG giants

Compared with FMCG giants, WD-40 operates with far smaller marketing budgets and weaker retail bargaining power, limiting national media reach and in‑store promotion frequency.

For context, Procter & Gamble spent about $8.1 billion on advertising in FY2023 and Unilever roughly €6–7 billion, sums WD-40 cannot match.

That gap allows competitors to outspend on innovation and shopper marketing and can translate into higher per‑unit procurement costs for WD-40.

Exposure to petrochemicals

Core WD-40 formulations rely on petroleum-derived inputs and aerosol propellants, leaving cost structure tied to hydrocarbon markets. Price volatility in 2024 squeezed industrial suppliers and can compress WD-40 margins and complicate pricing for distributors. Growing eco-conscious consumer segments increasingly view petrochemical-based aerosols negatively, risking demand shifts. Anticipated regulatory changes on VOCs and single-use aerosols could force reformulation and capital spending.

Narrow R&D pipeline

The brand’s success reduces urgency to innovate, with the Multi-Use Product still accounting for over half of WD-40 Company sales, which can limit breakthrough launches and keep R&D focused on incremental extensions.

Overreliance on the hero product slows category learning and diversification, making the company vulnerable to disruptive entrants with novel chemistries or business models.

- Concentration: hero product >50% sales

- R&D focus: incremental extensions

- Risk: exposure to disruptive entrants

Retailer dependence

Mass retail and hardware channels exert outsized control over WD-40 placement and pricing, pressuring promotional terms and contributing to margin compression as private-label share in U.S. grocery and consumables approached ~18% in 2023–24 (NielsenIQ). Slotting fees and trade spend are required to defend shelf space; shelf resets can erode visibility if not funded. Concentration in key accounts increases counterparty risk.

- Retailer influence on pricing/placement

- Private label pressure (~18% PL share 2023–24)

- Slotting fees/trade spend compress margins

- Key-account concentration = counterparty risk

Flagship SKU >50% of $558.6M; limited ad spend; VOC/hydrocarbon risk

WD-40 depends on its flagship SKU (>50% of fiscal 2024 sales; net sales $558.6M), concentrating operational and brand risk. Limited marketing spend versus FMCG giants (P&G $8.1B ad spend FY2023) reduces reach and retail leverage. Petroleum-based aerosols tie costs to hydrocarbon volatility and regulatory VOC exposure.

| Metric | Value |

|---|---|

| Net sales FY2024 | $558.6M |

| Hero SKU share | >50% |

| US private label | ~18% |

Preview the Actual Deliverable

WD-40 SWOT Analysis

This is the actual WD-40 SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full report you'll get, and purchase unlocks the complete, editable version. You’re viewing a live excerpt of the real file; the entire, detailed document becomes available immediately after checkout.