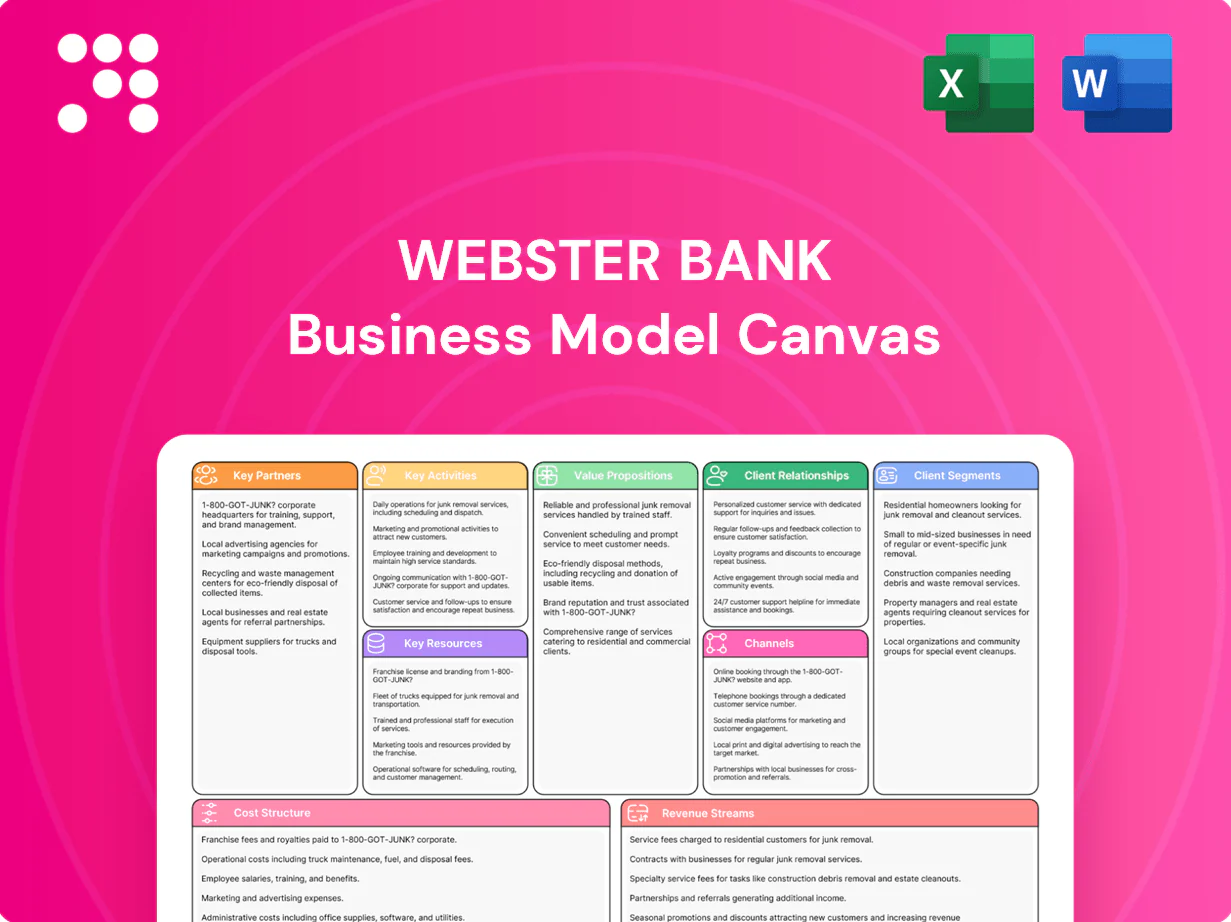

Webster Bank Business Model Canvas

Unlock a bank strategic playbook with a Business Model Canvas — download Word and Excel files

Unlock Webster Bank’s strategic playbook with the full Business Model Canvas — a concise, sector-tailored blueprint revealing customer segments, value propositions, revenue streams and cost drivers. Ideal for investors, consultants, and founders seeking actionable insights and ready-to-use Word and Excel files. Download the complete canvas to benchmark, plan, and scale with confidence.

Partnerships

Core banking and fintech vendors

Technology partners provide core banking platforms, digital onboarding, and cybersecurity solutions that enable continuous feature releases and regulatory-grade resilience.

Joint roadmaps with vendors help Webster tailor experiences for retail and commercial clients while vendor SLAs and co-innovation reduce time-to-market and total cost of ownership.

Payment networks and processors

Partnerships with card networks like Visa and Mastercard (acceptance in 200+ countries and territories) and ACH/wire processors (ACH handles 30+ billion annual transfers) power Webster Bank’s day-to-day transactions. These partners expand acceptance, accelerate settlement and layer fraud controls that materially curb losses. Co-branded card programs enhance rewards and can lift interchange economics by double-digit percentages, while tight integration ensures reliable payments for consumers and businesses.

Correspondent banks and liquidity providers

Correspondent banks and liquidity providers support Webster Bank’s FX, syndications and off‑balance‑sheet services, extending access to broader capital markets and specialty capabilities. In 2024 Webster Financial reported about $56.0 billion in total assets, diversifying funding and enhancing pricing. Clients receive seamless cross‑border execution and large‑ticket solutions backed by these alliances.

Investment, insurance, and wealth platforms

Third-party asset managers, custodians, and insurers expand Webster Bank’s advisory shelf, with open-architecture products addressing diverse risk/return profiles and platform fees averaging 25–50 basis points in 2024; revenue sharing and platform fees underpin economics while clients receive integrated planning through a single relationship.

- Third-party managers

- Open-architecture shelf

- Platform fees 25–50 bps (2024)

- Holistic client planning

Regulators and compliance advisors

Constructive engagement with regulators and retained compliance advisors ensure Webster Bank’s safety, soundness, and adherence to evolving rules, reducing regulatory risk and potential fines; Webster Financial reported roughly 50.7 billion in assets in 2024, underpinning the scale of oversight required.

External specialists bolster AML, KYC, and model-risk frameworks, strengthening franchise trust and reducing remediation costs and reputational loss.

- Regulatory engagement: reduces fines and enforcement risk

- Advisors: enhance AML/KYC and model risk controls

- Benefit: stronger trust and franchise value

Tech and partners accelerate digital banking, payments and liquidity for $56.0B; fees 25–50 bps

Technology, card networks, correspondent banks and asset managers enable Webster’s digital banking, payments, liquidity and advisory delivery while co‑innovation and SLAs lower time‑to‑market and TCO.

Card/ACH partners expand acceptance and settlement, boost fraud controls and interchange economics; platform fees 25–50 bps (2024).

Regulatory and specialist advisors strengthen AML/KYC, model risk and franchise trust across Webster Financial’s $56.0B assets (2024).

| Partner | Metric (2024) |

|---|---|

| Card networks | 200+ countries |

| ACH/wire | 30+B annual transfers |

| Platform fees | 25–50 bps |

| Assets | $56.0B |

What is included in the product

A comprehensive, pre-written Business Model Canvas for Webster Bank that maps customer segments, channels, value propositions, revenue streams and key resources across the 9 BMC blocks, reflecting real-world operations, competitive advantages, SWOT-linked insights and practical use for presentations, funding and strategic planning.

Clean, one-page Business Model Canvas that condenses Webster Bank’s strategy into editable cells, saving hours of structuring and making it easy to compare with peers or present to boards.

Activities

Deposit gathering and relationship banking

Attracting and retaining low-cost deposits anchors Webster Bank’s funding base, supporting lending and liquidity with over $50 billion in retail and commercial deposits as of 2024. Relationship managers deepen share of wallet across households and businesses, driving fee income and stronger balances. Data-driven outreach, using customer analytics, improves cross-sell and retention rates. A local presence of roughly 150 branches builds community trust and referral flow.

Lending and credit risk management

Underwriting covers consumer, mortgage and commercial credit with centralized underwriting standards and automated decisioning; in 2024 Webster continued segmented credit policies to limit concentration risk. Portfolio monitoring, stress testing and collections protect asset quality, with regular CECL-driven overlays and scenario tests. Prudent risk appetite balances growth and resilience, aligning pricing to risk-adjusted return targets and regulatory capital metrics in 2024.

Digital product development

Continuous enhancement of Webster Bank’s mobile and online banking drives engagement, reflecting over 70% US consumer mobile banking adoption in 2024; UX, security, and robust self-service flows are prioritized to reduce branch volume and lower support costs. APIs enable fintech and corporate ecosystem integrations, while analytics iterate features based on real customer behavior and conversion metrics.

Treasury and balance sheet management

ALM at Webster optimizes liquidity, capital and interest-rate risk to protect earnings and support lending growth; the securities portfolio and targeted hedge strategies stabilize net interest margin while limiting volatility; diversified funding sources (wholesale, deposits, brokered) strengthen balance-sheet resiliency; forward-looking scenario planning informs capital allocation and strategic choices.

- ALM: liquidity, capital, rate risk

- Securities & hedges: stabilize NIM

- Funding diversification: resiliency

- Scenario planning: strategic decisions

Compliance, security, and operations

Robust AML/KYC, privacy, and control processes at Webster Bank protect the franchise by preventing financial crime and ensuring regulatory compliance with ongoing transaction monitoring and client due diligence.

Layered cybersecurity and fraud prevention safeguards secure customer accounts and digital channels, reflecting 2024 industry focus as cyber losses remain a top risk.

Efficient back-office automation reduces operating costs and processing errors, while continuous staff training embeds a risk-aware culture across the bank.

- AML/KYC: ongoing transaction monitoring and enhanced due diligence

- Cybersecurity: multi-layer defenses and fraud detection

- Operations: automation to lower costs and errors

- Culture: continuous training and risk awareness

Bank: over $50B deposits, ~150 branches, over 70% mobile users

Webster anchors lending with over $50 billion in retail and commercial deposits and ~150 branches, while relationship managers and data-driven cross-sell lift fee income and balances. Segmented underwriting, CECL overlays and stress testing protect asset quality; ALM, securities and hedges stabilize NIM. Digital adoption exceeds 70% mobile users; strong AML/KYC and layered cybersecurity reduce fraud and compliance risk.

| Metric | 2024 |

|---|---|

| Deposits | $50B+ |

| Branches | ~150 |

| Mobile adoption | >70% |

| Risk controls | CECL, stress tests, AML/KYC |

What You See Is What You Get

Business Model Canvas

The document you're previewing is the exact Webster Bank Business Model Canvas you'll receive—no mockups or samples. After purchase you'll download this same fully formatted, editable file ready for presentation and analysis. What you see is the final deliverable.

Unlock a bank strategic playbook with a Business Model Canvas — download Word and Excel files

Unlock Webster Bank’s strategic playbook with the full Business Model Canvas — a concise, sector-tailored blueprint revealing customer segments, value propositions, revenue streams and cost drivers. Ideal for investors, consultants, and founders seeking actionable insights and ready-to-use Word and Excel files. Download the complete canvas to benchmark, plan, and scale with confidence.

Partnerships

Core banking and fintech vendors

Technology partners provide core banking platforms, digital onboarding, and cybersecurity solutions that enable continuous feature releases and regulatory-grade resilience.

Joint roadmaps with vendors help Webster tailor experiences for retail and commercial clients while vendor SLAs and co-innovation reduce time-to-market and total cost of ownership.

Payment networks and processors

Partnerships with card networks like Visa and Mastercard (acceptance in 200+ countries and territories) and ACH/wire processors (ACH handles 30+ billion annual transfers) power Webster Bank’s day-to-day transactions. These partners expand acceptance, accelerate settlement and layer fraud controls that materially curb losses. Co-branded card programs enhance rewards and can lift interchange economics by double-digit percentages, while tight integration ensures reliable payments for consumers and businesses.

Correspondent banks and liquidity providers

Correspondent banks and liquidity providers support Webster Bank’s FX, syndications and off‑balance‑sheet services, extending access to broader capital markets and specialty capabilities. In 2024 Webster Financial reported about $56.0 billion in total assets, diversifying funding and enhancing pricing. Clients receive seamless cross‑border execution and large‑ticket solutions backed by these alliances.

Investment, insurance, and wealth platforms

Third-party asset managers, custodians, and insurers expand Webster Bank’s advisory shelf, with open-architecture products addressing diverse risk/return profiles and platform fees averaging 25–50 basis points in 2024; revenue sharing and platform fees underpin economics while clients receive integrated planning through a single relationship.

- Third-party managers

- Open-architecture shelf

- Platform fees 25–50 bps (2024)

- Holistic client planning

Regulators and compliance advisors

Constructive engagement with regulators and retained compliance advisors ensure Webster Bank’s safety, soundness, and adherence to evolving rules, reducing regulatory risk and potential fines; Webster Financial reported roughly 50.7 billion in assets in 2024, underpinning the scale of oversight required.

External specialists bolster AML, KYC, and model-risk frameworks, strengthening franchise trust and reducing remediation costs and reputational loss.

- Regulatory engagement: reduces fines and enforcement risk

- Advisors: enhance AML/KYC and model risk controls

- Benefit: stronger trust and franchise value

Tech and partners accelerate digital banking, payments and liquidity for $56.0B; fees 25–50 bps

Technology, card networks, correspondent banks and asset managers enable Webster’s digital banking, payments, liquidity and advisory delivery while co‑innovation and SLAs lower time‑to‑market and TCO.

Card/ACH partners expand acceptance and settlement, boost fraud controls and interchange economics; platform fees 25–50 bps (2024).

Regulatory and specialist advisors strengthen AML/KYC, model risk and franchise trust across Webster Financial’s $56.0B assets (2024).

| Partner | Metric (2024) |

|---|---|

| Card networks | 200+ countries |

| ACH/wire | 30+B annual transfers |

| Platform fees | 25–50 bps |

| Assets | $56.0B |

What is included in the product

A comprehensive, pre-written Business Model Canvas for Webster Bank that maps customer segments, channels, value propositions, revenue streams and key resources across the 9 BMC blocks, reflecting real-world operations, competitive advantages, SWOT-linked insights and practical use for presentations, funding and strategic planning.

Clean, one-page Business Model Canvas that condenses Webster Bank’s strategy into editable cells, saving hours of structuring and making it easy to compare with peers or present to boards.

Activities

Deposit gathering and relationship banking

Attracting and retaining low-cost deposits anchors Webster Bank’s funding base, supporting lending and liquidity with over $50 billion in retail and commercial deposits as of 2024. Relationship managers deepen share of wallet across households and businesses, driving fee income and stronger balances. Data-driven outreach, using customer analytics, improves cross-sell and retention rates. A local presence of roughly 150 branches builds community trust and referral flow.

Lending and credit risk management

Underwriting covers consumer, mortgage and commercial credit with centralized underwriting standards and automated decisioning; in 2024 Webster continued segmented credit policies to limit concentration risk. Portfolio monitoring, stress testing and collections protect asset quality, with regular CECL-driven overlays and scenario tests. Prudent risk appetite balances growth and resilience, aligning pricing to risk-adjusted return targets and regulatory capital metrics in 2024.

Digital product development

Continuous enhancement of Webster Bank’s mobile and online banking drives engagement, reflecting over 70% US consumer mobile banking adoption in 2024; UX, security, and robust self-service flows are prioritized to reduce branch volume and lower support costs. APIs enable fintech and corporate ecosystem integrations, while analytics iterate features based on real customer behavior and conversion metrics.

Treasury and balance sheet management

ALM at Webster optimizes liquidity, capital and interest-rate risk to protect earnings and support lending growth; the securities portfolio and targeted hedge strategies stabilize net interest margin while limiting volatility; diversified funding sources (wholesale, deposits, brokered) strengthen balance-sheet resiliency; forward-looking scenario planning informs capital allocation and strategic choices.

- ALM: liquidity, capital, rate risk

- Securities & hedges: stabilize NIM

- Funding diversification: resiliency

- Scenario planning: strategic decisions

Compliance, security, and operations

Robust AML/KYC, privacy, and control processes at Webster Bank protect the franchise by preventing financial crime and ensuring regulatory compliance with ongoing transaction monitoring and client due diligence.

Layered cybersecurity and fraud prevention safeguards secure customer accounts and digital channels, reflecting 2024 industry focus as cyber losses remain a top risk.

Efficient back-office automation reduces operating costs and processing errors, while continuous staff training embeds a risk-aware culture across the bank.

- AML/KYC: ongoing transaction monitoring and enhanced due diligence

- Cybersecurity: multi-layer defenses and fraud detection

- Operations: automation to lower costs and errors

- Culture: continuous training and risk awareness

Bank: over $50B deposits, ~150 branches, over 70% mobile users

Webster anchors lending with over $50 billion in retail and commercial deposits and ~150 branches, while relationship managers and data-driven cross-sell lift fee income and balances. Segmented underwriting, CECL overlays and stress testing protect asset quality; ALM, securities and hedges stabilize NIM. Digital adoption exceeds 70% mobile users; strong AML/KYC and layered cybersecurity reduce fraud and compliance risk.

| Metric | 2024 |

|---|---|

| Deposits | $50B+ |

| Branches | ~150 |

| Mobile adoption | >70% |

| Risk controls | CECL, stress tests, AML/KYC |

What You See Is What You Get

Business Model Canvas

The document you're previewing is the exact Webster Bank Business Model Canvas you'll receive—no mockups or samples. After purchase you'll download this same fully formatted, editable file ready for presentation and analysis. What you see is the final deliverable.

Description

Unlock a bank strategic playbook with a Business Model Canvas — download Word and Excel files

Unlock Webster Bank’s strategic playbook with the full Business Model Canvas — a concise, sector-tailored blueprint revealing customer segments, value propositions, revenue streams and cost drivers. Ideal for investors, consultants, and founders seeking actionable insights and ready-to-use Word and Excel files. Download the complete canvas to benchmark, plan, and scale with confidence.

Partnerships

Core banking and fintech vendors

Technology partners provide core banking platforms, digital onboarding, and cybersecurity solutions that enable continuous feature releases and regulatory-grade resilience.

Joint roadmaps with vendors help Webster tailor experiences for retail and commercial clients while vendor SLAs and co-innovation reduce time-to-market and total cost of ownership.

Payment networks and processors

Partnerships with card networks like Visa and Mastercard (acceptance in 200+ countries and territories) and ACH/wire processors (ACH handles 30+ billion annual transfers) power Webster Bank’s day-to-day transactions. These partners expand acceptance, accelerate settlement and layer fraud controls that materially curb losses. Co-branded card programs enhance rewards and can lift interchange economics by double-digit percentages, while tight integration ensures reliable payments for consumers and businesses.

Correspondent banks and liquidity providers

Correspondent banks and liquidity providers support Webster Bank’s FX, syndications and off‑balance‑sheet services, extending access to broader capital markets and specialty capabilities. In 2024 Webster Financial reported about $56.0 billion in total assets, diversifying funding and enhancing pricing. Clients receive seamless cross‑border execution and large‑ticket solutions backed by these alliances.

Investment, insurance, and wealth platforms

Third-party asset managers, custodians, and insurers expand Webster Bank’s advisory shelf, with open-architecture products addressing diverse risk/return profiles and platform fees averaging 25–50 basis points in 2024; revenue sharing and platform fees underpin economics while clients receive integrated planning through a single relationship.

- Third-party managers

- Open-architecture shelf

- Platform fees 25–50 bps (2024)

- Holistic client planning

Regulators and compliance advisors

Constructive engagement with regulators and retained compliance advisors ensure Webster Bank’s safety, soundness, and adherence to evolving rules, reducing regulatory risk and potential fines; Webster Financial reported roughly 50.7 billion in assets in 2024, underpinning the scale of oversight required.

External specialists bolster AML, KYC, and model-risk frameworks, strengthening franchise trust and reducing remediation costs and reputational loss.

- Regulatory engagement: reduces fines and enforcement risk

- Advisors: enhance AML/KYC and model risk controls

- Benefit: stronger trust and franchise value

Tech and partners accelerate digital banking, payments and liquidity for $56.0B; fees 25–50 bps

Technology, card networks, correspondent banks and asset managers enable Webster’s digital banking, payments, liquidity and advisory delivery while co‑innovation and SLAs lower time‑to‑market and TCO.

Card/ACH partners expand acceptance and settlement, boost fraud controls and interchange economics; platform fees 25–50 bps (2024).

Regulatory and specialist advisors strengthen AML/KYC, model risk and franchise trust across Webster Financial’s $56.0B assets (2024).

| Partner | Metric (2024) |

|---|---|

| Card networks | 200+ countries |

| ACH/wire | 30+B annual transfers |

| Platform fees | 25–50 bps |

| Assets | $56.0B |

What is included in the product

A comprehensive, pre-written Business Model Canvas for Webster Bank that maps customer segments, channels, value propositions, revenue streams and key resources across the 9 BMC blocks, reflecting real-world operations, competitive advantages, SWOT-linked insights and practical use for presentations, funding and strategic planning.

Clean, one-page Business Model Canvas that condenses Webster Bank’s strategy into editable cells, saving hours of structuring and making it easy to compare with peers or present to boards.

Activities

Deposit gathering and relationship banking

Attracting and retaining low-cost deposits anchors Webster Bank’s funding base, supporting lending and liquidity with over $50 billion in retail and commercial deposits as of 2024. Relationship managers deepen share of wallet across households and businesses, driving fee income and stronger balances. Data-driven outreach, using customer analytics, improves cross-sell and retention rates. A local presence of roughly 150 branches builds community trust and referral flow.

Lending and credit risk management

Underwriting covers consumer, mortgage and commercial credit with centralized underwriting standards and automated decisioning; in 2024 Webster continued segmented credit policies to limit concentration risk. Portfolio monitoring, stress testing and collections protect asset quality, with regular CECL-driven overlays and scenario tests. Prudent risk appetite balances growth and resilience, aligning pricing to risk-adjusted return targets and regulatory capital metrics in 2024.

Digital product development

Continuous enhancement of Webster Bank’s mobile and online banking drives engagement, reflecting over 70% US consumer mobile banking adoption in 2024; UX, security, and robust self-service flows are prioritized to reduce branch volume and lower support costs. APIs enable fintech and corporate ecosystem integrations, while analytics iterate features based on real customer behavior and conversion metrics.

Treasury and balance sheet management

ALM at Webster optimizes liquidity, capital and interest-rate risk to protect earnings and support lending growth; the securities portfolio and targeted hedge strategies stabilize net interest margin while limiting volatility; diversified funding sources (wholesale, deposits, brokered) strengthen balance-sheet resiliency; forward-looking scenario planning informs capital allocation and strategic choices.

- ALM: liquidity, capital, rate risk

- Securities & hedges: stabilize NIM

- Funding diversification: resiliency

- Scenario planning: strategic decisions

Compliance, security, and operations

Robust AML/KYC, privacy, and control processes at Webster Bank protect the franchise by preventing financial crime and ensuring regulatory compliance with ongoing transaction monitoring and client due diligence.

Layered cybersecurity and fraud prevention safeguards secure customer accounts and digital channels, reflecting 2024 industry focus as cyber losses remain a top risk.

Efficient back-office automation reduces operating costs and processing errors, while continuous staff training embeds a risk-aware culture across the bank.

- AML/KYC: ongoing transaction monitoring and enhanced due diligence

- Cybersecurity: multi-layer defenses and fraud detection

- Operations: automation to lower costs and errors

- Culture: continuous training and risk awareness

Bank: over $50B deposits, ~150 branches, over 70% mobile users

Webster anchors lending with over $50 billion in retail and commercial deposits and ~150 branches, while relationship managers and data-driven cross-sell lift fee income and balances. Segmented underwriting, CECL overlays and stress testing protect asset quality; ALM, securities and hedges stabilize NIM. Digital adoption exceeds 70% mobile users; strong AML/KYC and layered cybersecurity reduce fraud and compliance risk.

| Metric | 2024 |

|---|---|

| Deposits | $50B+ |

| Branches | ~150 |

| Mobile adoption | >70% |

| Risk controls | CECL, stress tests, AML/KYC |

What You See Is What You Get

Business Model Canvas

The document you're previewing is the exact Webster Bank Business Model Canvas you'll receive—no mockups or samples. After purchase you'll download this same fully formatted, editable file ready for presentation and analysis. What you see is the final deliverable.