WELL Health Technologies Porter's Five Forces Analysis

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

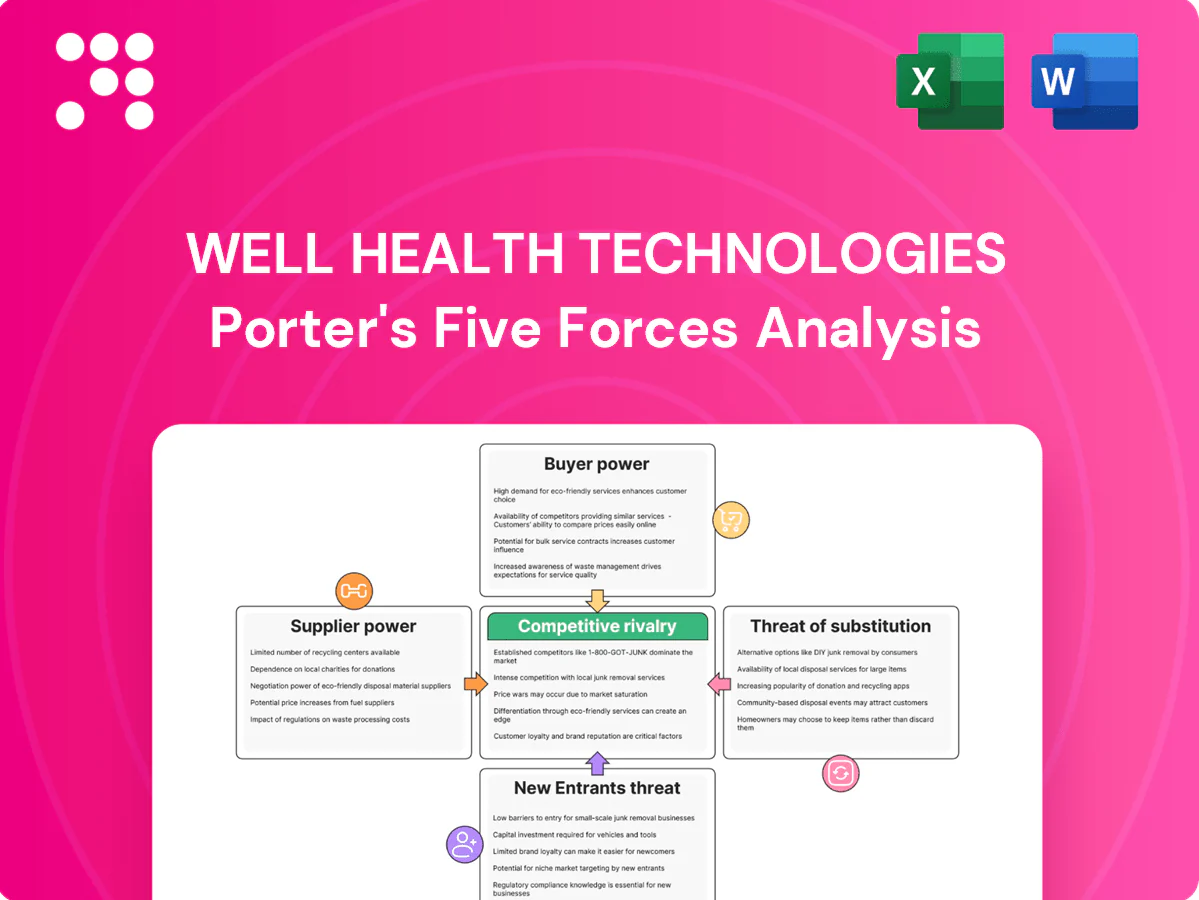

WELL Health’s Porter’s Five Forces highlights intense competitive rivalry from digital-health consolidators, moderate buyer power from payers and clinics, supplier leverage in tech partners, and regulatory & substitute threats from telehealth platforms. This snapshot teases strategic implications—unlock the full Porter’s Five Forces Analysis for force-by-force ratings, visuals, and actionable recommendations.

Suppliers Bargaining Power

Clinician labor as key input

WELL’s clinics rely on constrained pools of physicians, nurses and allied professionals, contributing to tight scheduling and higher wage pressure; WHO projects a global shortfall of about 18 million health workers by 2030. Scarcity in specialties gives physicians leverage to negotiate revenue splits and clinical autonomy. WELL’s recruiting and retention programs partially mitigate this supplier power.

Cloud and infrastructure vendors

Hosting WELL Health’s EMR and virtual-care stack depends on hyperscalers and critical SaaS tools; 2024 market-share estimates show AWS ~32%, Microsoft Azure ~23% and Google Cloud ~11%, concentrating supplier power. This concentration raises switching costs and risk of price escalation, especially with reserved-instance and multi-year SaaS contracts that lock pricing but reduce flexibility. Adopting multi-cloud and modular architectures mitigates dependence and enables negotiation leverage.

Medical devices and integrations

Clinic operations require certified devices and interfaces for labs, diagnostics and e-prescribing, and the global medical device market (~US$540B in 2023) concentrates supplier influence; proprietary standards and certification fees (often tens of thousands USD per device/certification) elevate supplier leverage. Vendor-specific integrations cause technical lock-in and high switching costs, while adoption of open standards and API-first design materially reduces that supplier power.

Data and interoperability networks

Access to health information exchanges, payer rails and e-referral networks is essential for WELL’s platform and often requires paid connectivity or compliance work from gatekeepers; these partners can levy per-connection fees or onboarding costs. Interoperability mandates (eg 21st Century Cures in the US) help but implementation and scope vary by province or state, creating uneven obligations. Strategic partnerships can secure preferred terms and lower supplier leverage.

- Gatekeeper fees: connectivity/onboarding costs

- Regulation: mandates vary by jurisdiction

- Mitigation: partnerships to lock favorable terms

Facilities and real estate

Prime clinic locations are limited and landlords in high-demand corridors can command higher rents and strict tenant-improvement demands, while long leases (common in healthcare real estate) increase fixed-cost exposure; WELL Health’s growing portfolio and expanded telehealth services reduce dependence on physical sites and provide offsetting flexibility.

- Limited prime sites

- Higher rents/TI in desirable corridors

- Long leases = fixed-cost risk

- Portfolio + telehealth lowers site dependence

Clinician shortage, cloud concentration and device costs raise supplier power; multi-cloud helps

WELL faces supplier power from scarce clinicians (WHO: 18M global shortfall by 2030), concentrated cloud providers (2024 share: AWS 32%, Azure 23%, GCP 11%), and a large medical-device market (~US$540B in 2023) with certification costs; long clinic leases also raise landlord leverage. Telehealth, multi-cloud, open APIs and strategic partnerships reduce supplier bargaining power.

| Supplier | Metric | Impact | Mitigation |

|---|---|---|---|

| Clinicians | 18M shortfall by 2030 | High wage/availability | Recruit/retention |

| Cloud | AWS 32%/Azure 23%/GCP 11% (2024) | Switching costs | Multi-cloud |

| Devices | ~US$540B (2023) | Certification lock-in | Open standards |

| Real estate | Long leases | Fixed-cost risk | Telehealth/portfolio |

What is included in the product

Analyzes competitive rivalry, buyer and supplier power, threat of new entrants and substitutes, and regulatory/technology pressures shaping WELL Health Technologies' profitability and strategic barriers.

A clear, one-sheet Porter’s Five Forces for WELL Health Technologies that relieves strategic analysis pain points by simplifying competitive pressures for rapid decisions; customize pressure levels with new data or swap in your own labels to reflect evolving healthcare market trends.

Customers Bargaining Power

Independent clinics and practitioners

Independent clinics and practitioners are highly cost-sensitive, actively comparing EMR plus virtual care bundles and seeking modular pricing and onboarding support to justify spend. Meaningful switching costs from data migration and workflow retraining make retention strong despite price pressure. Discounts, references, and industry-standard uptime SLAs (commonly 99.9%) materially reduce perceived risk.

Enterprise health systems

Enterprise health systems run formal RFPs in 2024 and demand deep integrations, security audits and steep volume pricing, giving buyers outsized negotiating leverage. Their scale drives multi-year deals (commonly 3–5 years) that cut churn but compress vendor margins. WELL’s robust compliance posture and clear ROI evidence are decisive in winning these large, procurement-led contracts.

Payers and government programs

Reimbursement policies drive demand and feature priorities for WELL, as public programs that finance roughly 70% of Canadian health spending (OECD) favor certified billing and interoperability. Public payers indirectly shape pricing through billing codes, certification and coverage rules, forcing product design trade-offs. Participation and certification add implementation cost but expand addressable market, while alignment with value-based care models—increasingly emphasized by payers—reduces adoption resistance.

Patients as clinic end-users

Patients prioritize access, convenience, and seamless digital experience when choosing clinics, with 2024 data showing sustained patient demand for virtual care and easier clinic switching than EMR changes, creating indirect pressure on service quality and availability.

Price transparency and virtual options increasingly affect retention, while NPS and wait-time metrics (reported in 2024 as key patient determinants) directly drive patient behavior and clinic selection.

- Access/convenience

- Virtual care penetration

- NPS & wait-time impact

Procurement transparency and comparability

WELL Health (TSX:WELL) faces high customer bargaining power because competing digital-health offerings are well-documented, enabling straightforward price and feature comparisons. Trials and pilots—common in enterprise procurement—increase buyer leverage by lowering uncertainty. Marketplace listings and peer reviews amplify scrutiny, while differentiated outcomes data can mitigate price pressure.

- Competing offerings: easy price/feature comparison

- Trials/pilots: reduce uncertainty, raise leverage

- Listings/reviews: amplify scrutiny

- Outcomes data: counteracts price pressure

Price-sensitive clinics face high switching costs; enterprises push 3-5yr deals; 70% public spend

Independent clinics exert price sensitivity but face meaningful switching costs; retention aided by 99.9% SLA norms and modular pricing. Enterprise systems use RFPs and volume discounts, driving 3–5 year contracts that compress margins. Public payers (≈70% of Canadian health spend in 2024) shape feature and pricing priorities; patient demand for virtual care raises service-quality pressure.

| Segment | Bargaining Power | 2024 Stat |

|---|---|---|

| Independent clinics | Moderate | High switching cost |

| Enterprises | High | 3–5 yr deals |

| Payers/Patients | High | 70% public spend |

Same Document Delivered

WELL Health Technologies Porter's Five Forces Analysis

This preview shows the exact Porter’s Five Forces analysis of WELL Health Technologies you’ll receive—no placeholders or summaries. The full, professionally formatted document available immediately after purchase contains the same detailed assessment of competitive rivalry, supplier and buyer power, threat of entrants, and substitutes. It’s ready for download and use the moment you buy.

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

WELL Health’s Porter’s Five Forces highlights intense competitive rivalry from digital-health consolidators, moderate buyer power from payers and clinics, supplier leverage in tech partners, and regulatory & substitute threats from telehealth platforms. This snapshot teases strategic implications—unlock the full Porter’s Five Forces Analysis for force-by-force ratings, visuals, and actionable recommendations.

Suppliers Bargaining Power

Clinician labor as key input

WELL’s clinics rely on constrained pools of physicians, nurses and allied professionals, contributing to tight scheduling and higher wage pressure; WHO projects a global shortfall of about 18 million health workers by 2030. Scarcity in specialties gives physicians leverage to negotiate revenue splits and clinical autonomy. WELL’s recruiting and retention programs partially mitigate this supplier power.

Cloud and infrastructure vendors

Hosting WELL Health’s EMR and virtual-care stack depends on hyperscalers and critical SaaS tools; 2024 market-share estimates show AWS ~32%, Microsoft Azure ~23% and Google Cloud ~11%, concentrating supplier power. This concentration raises switching costs and risk of price escalation, especially with reserved-instance and multi-year SaaS contracts that lock pricing but reduce flexibility. Adopting multi-cloud and modular architectures mitigates dependence and enables negotiation leverage.

Medical devices and integrations

Clinic operations require certified devices and interfaces for labs, diagnostics and e-prescribing, and the global medical device market (~US$540B in 2023) concentrates supplier influence; proprietary standards and certification fees (often tens of thousands USD per device/certification) elevate supplier leverage. Vendor-specific integrations cause technical lock-in and high switching costs, while adoption of open standards and API-first design materially reduces that supplier power.

Data and interoperability networks

Access to health information exchanges, payer rails and e-referral networks is essential for WELL’s platform and often requires paid connectivity or compliance work from gatekeepers; these partners can levy per-connection fees or onboarding costs. Interoperability mandates (eg 21st Century Cures in the US) help but implementation and scope vary by province or state, creating uneven obligations. Strategic partnerships can secure preferred terms and lower supplier leverage.

- Gatekeeper fees: connectivity/onboarding costs

- Regulation: mandates vary by jurisdiction

- Mitigation: partnerships to lock favorable terms

Facilities and real estate

Prime clinic locations are limited and landlords in high-demand corridors can command higher rents and strict tenant-improvement demands, while long leases (common in healthcare real estate) increase fixed-cost exposure; WELL Health’s growing portfolio and expanded telehealth services reduce dependence on physical sites and provide offsetting flexibility.

- Limited prime sites

- Higher rents/TI in desirable corridors

- Long leases = fixed-cost risk

- Portfolio + telehealth lowers site dependence

Clinician shortage, cloud concentration and device costs raise supplier power; multi-cloud helps

WELL faces supplier power from scarce clinicians (WHO: 18M global shortfall by 2030), concentrated cloud providers (2024 share: AWS 32%, Azure 23%, GCP 11%), and a large medical-device market (~US$540B in 2023) with certification costs; long clinic leases also raise landlord leverage. Telehealth, multi-cloud, open APIs and strategic partnerships reduce supplier bargaining power.

| Supplier | Metric | Impact | Mitigation |

|---|---|---|---|

| Clinicians | 18M shortfall by 2030 | High wage/availability | Recruit/retention |

| Cloud | AWS 32%/Azure 23%/GCP 11% (2024) | Switching costs | Multi-cloud |

| Devices | ~US$540B (2023) | Certification lock-in | Open standards |

| Real estate | Long leases | Fixed-cost risk | Telehealth/portfolio |

What is included in the product

Analyzes competitive rivalry, buyer and supplier power, threat of new entrants and substitutes, and regulatory/technology pressures shaping WELL Health Technologies' profitability and strategic barriers.

A clear, one-sheet Porter’s Five Forces for WELL Health Technologies that relieves strategic analysis pain points by simplifying competitive pressures for rapid decisions; customize pressure levels with new data or swap in your own labels to reflect evolving healthcare market trends.

Customers Bargaining Power

Independent clinics and practitioners

Independent clinics and practitioners are highly cost-sensitive, actively comparing EMR plus virtual care bundles and seeking modular pricing and onboarding support to justify spend. Meaningful switching costs from data migration and workflow retraining make retention strong despite price pressure. Discounts, references, and industry-standard uptime SLAs (commonly 99.9%) materially reduce perceived risk.

Enterprise health systems

Enterprise health systems run formal RFPs in 2024 and demand deep integrations, security audits and steep volume pricing, giving buyers outsized negotiating leverage. Their scale drives multi-year deals (commonly 3–5 years) that cut churn but compress vendor margins. WELL’s robust compliance posture and clear ROI evidence are decisive in winning these large, procurement-led contracts.

Payers and government programs

Reimbursement policies drive demand and feature priorities for WELL, as public programs that finance roughly 70% of Canadian health spending (OECD) favor certified billing and interoperability. Public payers indirectly shape pricing through billing codes, certification and coverage rules, forcing product design trade-offs. Participation and certification add implementation cost but expand addressable market, while alignment with value-based care models—increasingly emphasized by payers—reduces adoption resistance.

Patients as clinic end-users

Patients prioritize access, convenience, and seamless digital experience when choosing clinics, with 2024 data showing sustained patient demand for virtual care and easier clinic switching than EMR changes, creating indirect pressure on service quality and availability.

Price transparency and virtual options increasingly affect retention, while NPS and wait-time metrics (reported in 2024 as key patient determinants) directly drive patient behavior and clinic selection.

- Access/convenience

- Virtual care penetration

- NPS & wait-time impact

Procurement transparency and comparability

WELL Health (TSX:WELL) faces high customer bargaining power because competing digital-health offerings are well-documented, enabling straightforward price and feature comparisons. Trials and pilots—common in enterprise procurement—increase buyer leverage by lowering uncertainty. Marketplace listings and peer reviews amplify scrutiny, while differentiated outcomes data can mitigate price pressure.

- Competing offerings: easy price/feature comparison

- Trials/pilots: reduce uncertainty, raise leverage

- Listings/reviews: amplify scrutiny

- Outcomes data: counteracts price pressure

Price-sensitive clinics face high switching costs; enterprises push 3-5yr deals; 70% public spend

Independent clinics exert price sensitivity but face meaningful switching costs; retention aided by 99.9% SLA norms and modular pricing. Enterprise systems use RFPs and volume discounts, driving 3–5 year contracts that compress margins. Public payers (≈70% of Canadian health spend in 2024) shape feature and pricing priorities; patient demand for virtual care raises service-quality pressure.

| Segment | Bargaining Power | 2024 Stat |

|---|---|---|

| Independent clinics | Moderate | High switching cost |

| Enterprises | High | 3–5 yr deals |

| Payers/Patients | High | 70% public spend |

Same Document Delivered

WELL Health Technologies Porter's Five Forces Analysis

This preview shows the exact Porter’s Five Forces analysis of WELL Health Technologies you’ll receive—no placeholders or summaries. The full, professionally formatted document available immediately after purchase contains the same detailed assessment of competitive rivalry, supplier and buyer power, threat of entrants, and substitutes. It’s ready for download and use the moment you buy.

Original: $10.00

-65%$10.00

$3.50Description

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

WELL Health’s Porter’s Five Forces highlights intense competitive rivalry from digital-health consolidators, moderate buyer power from payers and clinics, supplier leverage in tech partners, and regulatory & substitute threats from telehealth platforms. This snapshot teases strategic implications—unlock the full Porter’s Five Forces Analysis for force-by-force ratings, visuals, and actionable recommendations.

Suppliers Bargaining Power

Clinician labor as key input

WELL’s clinics rely on constrained pools of physicians, nurses and allied professionals, contributing to tight scheduling and higher wage pressure; WHO projects a global shortfall of about 18 million health workers by 2030. Scarcity in specialties gives physicians leverage to negotiate revenue splits and clinical autonomy. WELL’s recruiting and retention programs partially mitigate this supplier power.

Cloud and infrastructure vendors

Hosting WELL Health’s EMR and virtual-care stack depends on hyperscalers and critical SaaS tools; 2024 market-share estimates show AWS ~32%, Microsoft Azure ~23% and Google Cloud ~11%, concentrating supplier power. This concentration raises switching costs and risk of price escalation, especially with reserved-instance and multi-year SaaS contracts that lock pricing but reduce flexibility. Adopting multi-cloud and modular architectures mitigates dependence and enables negotiation leverage.

Medical devices and integrations

Clinic operations require certified devices and interfaces for labs, diagnostics and e-prescribing, and the global medical device market (~US$540B in 2023) concentrates supplier influence; proprietary standards and certification fees (often tens of thousands USD per device/certification) elevate supplier leverage. Vendor-specific integrations cause technical lock-in and high switching costs, while adoption of open standards and API-first design materially reduces that supplier power.

Data and interoperability networks

Access to health information exchanges, payer rails and e-referral networks is essential for WELL’s platform and often requires paid connectivity or compliance work from gatekeepers; these partners can levy per-connection fees or onboarding costs. Interoperability mandates (eg 21st Century Cures in the US) help but implementation and scope vary by province or state, creating uneven obligations. Strategic partnerships can secure preferred terms and lower supplier leverage.

- Gatekeeper fees: connectivity/onboarding costs

- Regulation: mandates vary by jurisdiction

- Mitigation: partnerships to lock favorable terms

Facilities and real estate

Prime clinic locations are limited and landlords in high-demand corridors can command higher rents and strict tenant-improvement demands, while long leases (common in healthcare real estate) increase fixed-cost exposure; WELL Health’s growing portfolio and expanded telehealth services reduce dependence on physical sites and provide offsetting flexibility.

- Limited prime sites

- Higher rents/TI in desirable corridors

- Long leases = fixed-cost risk

- Portfolio + telehealth lowers site dependence

Clinician shortage, cloud concentration and device costs raise supplier power; multi-cloud helps

WELL faces supplier power from scarce clinicians (WHO: 18M global shortfall by 2030), concentrated cloud providers (2024 share: AWS 32%, Azure 23%, GCP 11%), and a large medical-device market (~US$540B in 2023) with certification costs; long clinic leases also raise landlord leverage. Telehealth, multi-cloud, open APIs and strategic partnerships reduce supplier bargaining power.

| Supplier | Metric | Impact | Mitigation |

|---|---|---|---|

| Clinicians | 18M shortfall by 2030 | High wage/availability | Recruit/retention |

| Cloud | AWS 32%/Azure 23%/GCP 11% (2024) | Switching costs | Multi-cloud |

| Devices | ~US$540B (2023) | Certification lock-in | Open standards |

| Real estate | Long leases | Fixed-cost risk | Telehealth/portfolio |

What is included in the product

Analyzes competitive rivalry, buyer and supplier power, threat of new entrants and substitutes, and regulatory/technology pressures shaping WELL Health Technologies' profitability and strategic barriers.

A clear, one-sheet Porter’s Five Forces for WELL Health Technologies that relieves strategic analysis pain points by simplifying competitive pressures for rapid decisions; customize pressure levels with new data or swap in your own labels to reflect evolving healthcare market trends.

Customers Bargaining Power

Independent clinics and practitioners

Independent clinics and practitioners are highly cost-sensitive, actively comparing EMR plus virtual care bundles and seeking modular pricing and onboarding support to justify spend. Meaningful switching costs from data migration and workflow retraining make retention strong despite price pressure. Discounts, references, and industry-standard uptime SLAs (commonly 99.9%) materially reduce perceived risk.

Enterprise health systems

Enterprise health systems run formal RFPs in 2024 and demand deep integrations, security audits and steep volume pricing, giving buyers outsized negotiating leverage. Their scale drives multi-year deals (commonly 3–5 years) that cut churn but compress vendor margins. WELL’s robust compliance posture and clear ROI evidence are decisive in winning these large, procurement-led contracts.

Payers and government programs

Reimbursement policies drive demand and feature priorities for WELL, as public programs that finance roughly 70% of Canadian health spending (OECD) favor certified billing and interoperability. Public payers indirectly shape pricing through billing codes, certification and coverage rules, forcing product design trade-offs. Participation and certification add implementation cost but expand addressable market, while alignment with value-based care models—increasingly emphasized by payers—reduces adoption resistance.

Patients as clinic end-users

Patients prioritize access, convenience, and seamless digital experience when choosing clinics, with 2024 data showing sustained patient demand for virtual care and easier clinic switching than EMR changes, creating indirect pressure on service quality and availability.

Price transparency and virtual options increasingly affect retention, while NPS and wait-time metrics (reported in 2024 as key patient determinants) directly drive patient behavior and clinic selection.

- Access/convenience

- Virtual care penetration

- NPS & wait-time impact

Procurement transparency and comparability

WELL Health (TSX:WELL) faces high customer bargaining power because competing digital-health offerings are well-documented, enabling straightforward price and feature comparisons. Trials and pilots—common in enterprise procurement—increase buyer leverage by lowering uncertainty. Marketplace listings and peer reviews amplify scrutiny, while differentiated outcomes data can mitigate price pressure.

- Competing offerings: easy price/feature comparison

- Trials/pilots: reduce uncertainty, raise leverage

- Listings/reviews: amplify scrutiny

- Outcomes data: counteracts price pressure

Price-sensitive clinics face high switching costs; enterprises push 3-5yr deals; 70% public spend

Independent clinics exert price sensitivity but face meaningful switching costs; retention aided by 99.9% SLA norms and modular pricing. Enterprise systems use RFPs and volume discounts, driving 3–5 year contracts that compress margins. Public payers (≈70% of Canadian health spend in 2024) shape feature and pricing priorities; patient demand for virtual care raises service-quality pressure.

| Segment | Bargaining Power | 2024 Stat |

|---|---|---|

| Independent clinics | Moderate | High switching cost |

| Enterprises | High | 3–5 yr deals |

| Payers/Patients | High | 70% public spend |

Same Document Delivered

WELL Health Technologies Porter's Five Forces Analysis

This preview shows the exact Porter’s Five Forces analysis of WELL Health Technologies you’ll receive—no placeholders or summaries. The full, professionally formatted document available immediately after purchase contains the same detailed assessment of competitive rivalry, supplier and buyer power, threat of entrants, and substitutes. It’s ready for download and use the moment you buy.