Western Energy Services Porter's Five Forces Analysis

From Overview to Strategy Blueprint

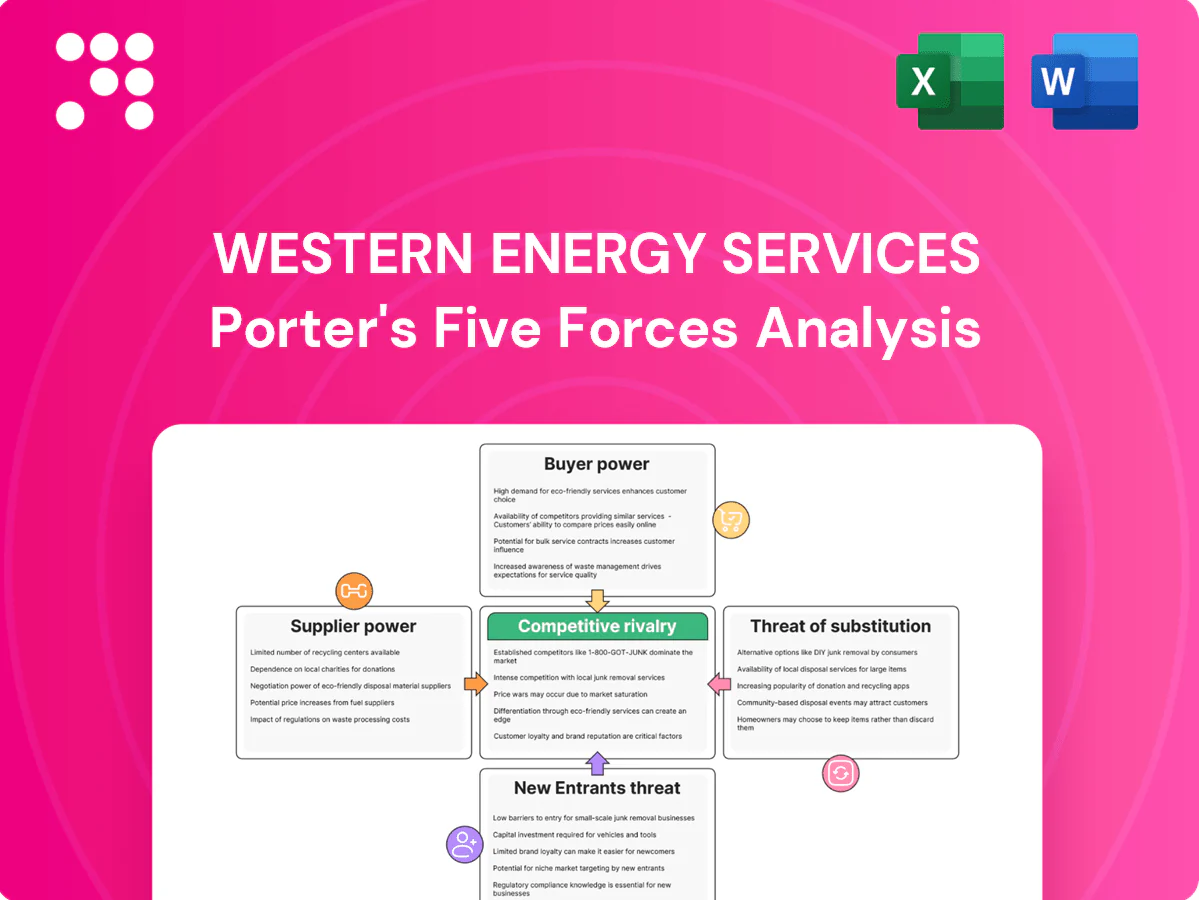

Western Energy Services faces moderate buyer power, concentrated suppliers, regulatory headwinds, substitution risks from alternative energy, and intense rivalry — factors compressing margins and shaping strategy. This snapshot highlights core competitive levers and vulnerabilities. Unlock the full Porter's Five Forces Analysis for force-by-force ratings, visuals, and actionable insights to guide investment or strategic decisions.

Suppliers Bargaining Power

Consolidated critical equipment

OEMs for rigs, top drives, snubbing units and control systems are relatively concentrated, giving a few suppliers outsized pricing and lead-time leverage for Western Energy Services. Proprietary parts and software lock-ins raise switching costs for maintenance and upgrades, effectively tying fleet economics to OEM service terms. Long build cycles for high-spec rigs, often 18–24 months, tighten supply during upswings and can compress margins unless multi-sourcing is secured.

Skilled labor scarcity

Experienced drillers, snubbing crews and HSE-certified operators remain finite, with the 2024 Baker Hughes rig count averaging about 620 rigs, concentrating demand during activity spikes and tightening supply.

Wage inflation and retention bonuses—reported industry-wide increases near 10% in 2024—push input costs and raise scheduling risk.

Training pipelines partially mitigate shortages but lag operational needs, while unions and regional labor dynamics further shift bargaining power to labor suppliers.

Consumables and energy volatility

Diesel, drilling mud, tubulars and chemicals are exposed to commodity swings—Brent averaged about $82/bbl in 2024 and U.S. retail diesel was near $3.88/gal (EIA July 2024), letting suppliers pass cost hikes faster than service dayrates. Fuel surcharges mitigate but lag can erode margins by several percentage points. Hedging and indexed supply contracts can partially neutralize volatility and stabilize cash flow.

Aftermarket parts dependence

Equipment uptime for Western Energy depends on timely access to specialized spares and certified service; 2024 industry data shows OEM-authorized channels can command 10–30% premiums and prioritize larger buyers, forcing smaller operators to either pay up or wait. Inventory buffering ties up an estimated 3–7% of working capital, and delays cascade into non-productive time penalties often in the $5,000–$20,000/day range.

- OEM premiums: 10–30%

- Working capital tied: 3–7%

- NPT penalties: $5k–$20k/day

Technology and data ecosystems

Supply bottlenecks lift OEM premiums 10-30%, tighten crews, raise NPT risk

Concentrated OEMs and vendor lock-ins give suppliers pricing and lead-time leverage, with OEM premiums of 10–30% and 3–5 year contract norms in 2024. Labor scarcity (Baker Hughes rig count ~620) and ~10% wage inflation tighten skilled crew supply. Commodity exposure (Brent ~$82/bbl, diesel ~$3.88/gal) and parts shortages tie up 3–7% working capital and risk NPT of $5k–$20k/day.

| Metric | 2024 Value |

|---|---|

| OEM premiums | 10–30% |

| Rig count (BH) | ~620 |

| Wage inflation | ~10% |

| Brent | $82/bbl |

| Diesel (US) | $3.88/gal |

| Working capital tied | 3–7% |

| NPT cost | $5k–$20k/day |

What is included in the product

Tailored Porter's Five Forces analysis for Western Energy Services that uncovers competitive drivers, supplier and buyer power, entry barriers, substitute threats, and strategic levers impacting pricing, margins, and market positioning.

A concise one-sheet Porter's Five Forces for Western Energy Services—instantly reveals supplier, buyer, entrant and rivalry pressures so management can prioritize actions and relieve strategic uncertainty.

Customers Bargaining Power

Concentrated E&P customers

Large operators and well-capitalized independents dominate demand and run competitive tenders, forcing Western Energy Services to bid aggressively. They leverage scale to pressure dayrates and contract terms, with preferred-vendor lists and performance scorecards amplifying buyer power. Deep relationships with key E&P clients improve utilization but do not eliminate pricing discipline.

Low switching costs

Customers can reassign work among comparable rigs and service providers with limited friction, compressing Western Energy Services pricing power. Standardized specifications and regulatory safety requirements make substitution straightforward across fleets. Short-duration jobs lasting days to weeks amplify this flexibility and buyer leverage. Contract renewals routinely reset dayrates to prevailing market levels, keeping margins exposed to spot competition.

Cyclical utilization leverage

When rig and service utilization is soft, buyers extract concessions and ancillary freebies; spot markets transmit pricing declines rapidly—Baker Hughes rig count volatility saw utilization dip below 75% in mid-2024, amplifying spot-rate pressure. Term contracts, scarce in downturns, provided some stability for Western Energy Services but represented a minority of revenue. In upcycles, leverage shifts back to suppliers, typically with a 3–6 month lag.

Integrated bundle expectations

Buyers increasingly demand integrated bundles of drilling, rentals, and well services to simplify logistics and cut total cost, insisting on performance-based KPIs and NPT penalties to shift risk to suppliers.

- Bundling simplifies logistics and pressures price packaging

- KPIs and NPT penalties standard in contracts

- Cross-selling defends share but compresses margins

- Value reporting and HSE excellence are mandatory

Stringent HSE and ESG demands

Operators increasingly prioritize stringent HSE and ESG standards, with an estimated 70% of major North American operators in 2024 requiring verified emissions and safety reporting, steering vendor selection toward compliant fleets and technologies. Compliance drives higher operating costs and capital expenditure for newer low-emission rigs; non-compliant vendors are often excluded regardless of price. Data transparency on emissions and incidents is now regularly requested in bids.

- HSE/ESG clauses: 70% (2024)

- CapEx pressure: newer fleets premium up to 15–25%

- Exclusion risk: non-compliance overrides price

- Reporting: verified emissions & incident metrics required

Competitive tenders, rig use 75%, 70% HSE, 15–25% capex

Large operators and well-capitalized independents run competitive tenders, forcing Western Energy Services to bid aggressively and accept tight dayrates. Buyers reassign work easily—rig utilization fell below 75% mid-2024—boosting spot leverage and compressing margins. 70% of major operators required verified HSE/ESG reporting in 2024, creating capex pressure (newer fleets premium 15–25%).

| Metric | 2024 | Impact |

|---|---|---|

| Buyer concentration | High | Stronger price pressure |

| Rig utilization | <75% | Spot-rate downside |

| HSE/ESG mandates | 70% | Vendor exclusion risk |

| CapEx premium | 15–25% | Fleet upgrade cost |

Same Document Delivered

Western Energy Services Porter's Five Forces Analysis

This preview shows the exact Western Energy Services Porter's Five Forces analysis you'll receive—no placeholders or samples. It is the fully formatted, final document covering competitive rivalry, supplier and buyer power, and threats of entry and substitutes. Purchase grants immediate download and ready-to-use access.

From Overview to Strategy Blueprint

Western Energy Services faces moderate buyer power, concentrated suppliers, regulatory headwinds, substitution risks from alternative energy, and intense rivalry — factors compressing margins and shaping strategy. This snapshot highlights core competitive levers and vulnerabilities. Unlock the full Porter's Five Forces Analysis for force-by-force ratings, visuals, and actionable insights to guide investment or strategic decisions.

Suppliers Bargaining Power

Consolidated critical equipment

OEMs for rigs, top drives, snubbing units and control systems are relatively concentrated, giving a few suppliers outsized pricing and lead-time leverage for Western Energy Services. Proprietary parts and software lock-ins raise switching costs for maintenance and upgrades, effectively tying fleet economics to OEM service terms. Long build cycles for high-spec rigs, often 18–24 months, tighten supply during upswings and can compress margins unless multi-sourcing is secured.

Skilled labor scarcity

Experienced drillers, snubbing crews and HSE-certified operators remain finite, with the 2024 Baker Hughes rig count averaging about 620 rigs, concentrating demand during activity spikes and tightening supply.

Wage inflation and retention bonuses—reported industry-wide increases near 10% in 2024—push input costs and raise scheduling risk.

Training pipelines partially mitigate shortages but lag operational needs, while unions and regional labor dynamics further shift bargaining power to labor suppliers.

Consumables and energy volatility

Diesel, drilling mud, tubulars and chemicals are exposed to commodity swings—Brent averaged about $82/bbl in 2024 and U.S. retail diesel was near $3.88/gal (EIA July 2024), letting suppliers pass cost hikes faster than service dayrates. Fuel surcharges mitigate but lag can erode margins by several percentage points. Hedging and indexed supply contracts can partially neutralize volatility and stabilize cash flow.

Aftermarket parts dependence

Equipment uptime for Western Energy depends on timely access to specialized spares and certified service; 2024 industry data shows OEM-authorized channels can command 10–30% premiums and prioritize larger buyers, forcing smaller operators to either pay up or wait. Inventory buffering ties up an estimated 3–7% of working capital, and delays cascade into non-productive time penalties often in the $5,000–$20,000/day range.

- OEM premiums: 10–30%

- Working capital tied: 3–7%

- NPT penalties: $5k–$20k/day

Technology and data ecosystems

Supply bottlenecks lift OEM premiums 10-30%, tighten crews, raise NPT risk

Concentrated OEMs and vendor lock-ins give suppliers pricing and lead-time leverage, with OEM premiums of 10–30% and 3–5 year contract norms in 2024. Labor scarcity (Baker Hughes rig count ~620) and ~10% wage inflation tighten skilled crew supply. Commodity exposure (Brent ~$82/bbl, diesel ~$3.88/gal) and parts shortages tie up 3–7% working capital and risk NPT of $5k–$20k/day.

| Metric | 2024 Value |

|---|---|

| OEM premiums | 10–30% |

| Rig count (BH) | ~620 |

| Wage inflation | ~10% |

| Brent | $82/bbl |

| Diesel (US) | $3.88/gal |

| Working capital tied | 3–7% |

| NPT cost | $5k–$20k/day |

What is included in the product

Tailored Porter's Five Forces analysis for Western Energy Services that uncovers competitive drivers, supplier and buyer power, entry barriers, substitute threats, and strategic levers impacting pricing, margins, and market positioning.

A concise one-sheet Porter's Five Forces for Western Energy Services—instantly reveals supplier, buyer, entrant and rivalry pressures so management can prioritize actions and relieve strategic uncertainty.

Customers Bargaining Power

Concentrated E&P customers

Large operators and well-capitalized independents dominate demand and run competitive tenders, forcing Western Energy Services to bid aggressively. They leverage scale to pressure dayrates and contract terms, with preferred-vendor lists and performance scorecards amplifying buyer power. Deep relationships with key E&P clients improve utilization but do not eliminate pricing discipline.

Low switching costs

Customers can reassign work among comparable rigs and service providers with limited friction, compressing Western Energy Services pricing power. Standardized specifications and regulatory safety requirements make substitution straightforward across fleets. Short-duration jobs lasting days to weeks amplify this flexibility and buyer leverage. Contract renewals routinely reset dayrates to prevailing market levels, keeping margins exposed to spot competition.

Cyclical utilization leverage

When rig and service utilization is soft, buyers extract concessions and ancillary freebies; spot markets transmit pricing declines rapidly—Baker Hughes rig count volatility saw utilization dip below 75% in mid-2024, amplifying spot-rate pressure. Term contracts, scarce in downturns, provided some stability for Western Energy Services but represented a minority of revenue. In upcycles, leverage shifts back to suppliers, typically with a 3–6 month lag.

Integrated bundle expectations

Buyers increasingly demand integrated bundles of drilling, rentals, and well services to simplify logistics and cut total cost, insisting on performance-based KPIs and NPT penalties to shift risk to suppliers.

- Bundling simplifies logistics and pressures price packaging

- KPIs and NPT penalties standard in contracts

- Cross-selling defends share but compresses margins

- Value reporting and HSE excellence are mandatory

Stringent HSE and ESG demands

Operators increasingly prioritize stringent HSE and ESG standards, with an estimated 70% of major North American operators in 2024 requiring verified emissions and safety reporting, steering vendor selection toward compliant fleets and technologies. Compliance drives higher operating costs and capital expenditure for newer low-emission rigs; non-compliant vendors are often excluded regardless of price. Data transparency on emissions and incidents is now regularly requested in bids.

- HSE/ESG clauses: 70% (2024)

- CapEx pressure: newer fleets premium up to 15–25%

- Exclusion risk: non-compliance overrides price

- Reporting: verified emissions & incident metrics required

Competitive tenders, rig use 75%, 70% HSE, 15–25% capex

Large operators and well-capitalized independents run competitive tenders, forcing Western Energy Services to bid aggressively and accept tight dayrates. Buyers reassign work easily—rig utilization fell below 75% mid-2024—boosting spot leverage and compressing margins. 70% of major operators required verified HSE/ESG reporting in 2024, creating capex pressure (newer fleets premium 15–25%).

| Metric | 2024 | Impact |

|---|---|---|

| Buyer concentration | High | Stronger price pressure |

| Rig utilization | <75% | Spot-rate downside |

| HSE/ESG mandates | 70% | Vendor exclusion risk |

| CapEx premium | 15–25% | Fleet upgrade cost |

Same Document Delivered

Western Energy Services Porter's Five Forces Analysis

This preview shows the exact Western Energy Services Porter's Five Forces analysis you'll receive—no placeholders or samples. It is the fully formatted, final document covering competitive rivalry, supplier and buyer power, and threats of entry and substitutes. Purchase grants immediate download and ready-to-use access.

Original: $10.00

-65%$10.00

$3.50Description

From Overview to Strategy Blueprint

Western Energy Services faces moderate buyer power, concentrated suppliers, regulatory headwinds, substitution risks from alternative energy, and intense rivalry — factors compressing margins and shaping strategy. This snapshot highlights core competitive levers and vulnerabilities. Unlock the full Porter's Five Forces Analysis for force-by-force ratings, visuals, and actionable insights to guide investment or strategic decisions.

Suppliers Bargaining Power

Consolidated critical equipment

OEMs for rigs, top drives, snubbing units and control systems are relatively concentrated, giving a few suppliers outsized pricing and lead-time leverage for Western Energy Services. Proprietary parts and software lock-ins raise switching costs for maintenance and upgrades, effectively tying fleet economics to OEM service terms. Long build cycles for high-spec rigs, often 18–24 months, tighten supply during upswings and can compress margins unless multi-sourcing is secured.

Skilled labor scarcity

Experienced drillers, snubbing crews and HSE-certified operators remain finite, with the 2024 Baker Hughes rig count averaging about 620 rigs, concentrating demand during activity spikes and tightening supply.

Wage inflation and retention bonuses—reported industry-wide increases near 10% in 2024—push input costs and raise scheduling risk.

Training pipelines partially mitigate shortages but lag operational needs, while unions and regional labor dynamics further shift bargaining power to labor suppliers.

Consumables and energy volatility

Diesel, drilling mud, tubulars and chemicals are exposed to commodity swings—Brent averaged about $82/bbl in 2024 and U.S. retail diesel was near $3.88/gal (EIA July 2024), letting suppliers pass cost hikes faster than service dayrates. Fuel surcharges mitigate but lag can erode margins by several percentage points. Hedging and indexed supply contracts can partially neutralize volatility and stabilize cash flow.

Aftermarket parts dependence

Equipment uptime for Western Energy depends on timely access to specialized spares and certified service; 2024 industry data shows OEM-authorized channels can command 10–30% premiums and prioritize larger buyers, forcing smaller operators to either pay up or wait. Inventory buffering ties up an estimated 3–7% of working capital, and delays cascade into non-productive time penalties often in the $5,000–$20,000/day range.

- OEM premiums: 10–30%

- Working capital tied: 3–7%

- NPT penalties: $5k–$20k/day

Technology and data ecosystems

Supply bottlenecks lift OEM premiums 10-30%, tighten crews, raise NPT risk

Concentrated OEMs and vendor lock-ins give suppliers pricing and lead-time leverage, with OEM premiums of 10–30% and 3–5 year contract norms in 2024. Labor scarcity (Baker Hughes rig count ~620) and ~10% wage inflation tighten skilled crew supply. Commodity exposure (Brent ~$82/bbl, diesel ~$3.88/gal) and parts shortages tie up 3–7% working capital and risk NPT of $5k–$20k/day.

| Metric | 2024 Value |

|---|---|

| OEM premiums | 10–30% |

| Rig count (BH) | ~620 |

| Wage inflation | ~10% |

| Brent | $82/bbl |

| Diesel (US) | $3.88/gal |

| Working capital tied | 3–7% |

| NPT cost | $5k–$20k/day |

What is included in the product

Tailored Porter's Five Forces analysis for Western Energy Services that uncovers competitive drivers, supplier and buyer power, entry barriers, substitute threats, and strategic levers impacting pricing, margins, and market positioning.

A concise one-sheet Porter's Five Forces for Western Energy Services—instantly reveals supplier, buyer, entrant and rivalry pressures so management can prioritize actions and relieve strategic uncertainty.

Customers Bargaining Power

Concentrated E&P customers

Large operators and well-capitalized independents dominate demand and run competitive tenders, forcing Western Energy Services to bid aggressively. They leverage scale to pressure dayrates and contract terms, with preferred-vendor lists and performance scorecards amplifying buyer power. Deep relationships with key E&P clients improve utilization but do not eliminate pricing discipline.

Low switching costs

Customers can reassign work among comparable rigs and service providers with limited friction, compressing Western Energy Services pricing power. Standardized specifications and regulatory safety requirements make substitution straightforward across fleets. Short-duration jobs lasting days to weeks amplify this flexibility and buyer leverage. Contract renewals routinely reset dayrates to prevailing market levels, keeping margins exposed to spot competition.

Cyclical utilization leverage

When rig and service utilization is soft, buyers extract concessions and ancillary freebies; spot markets transmit pricing declines rapidly—Baker Hughes rig count volatility saw utilization dip below 75% in mid-2024, amplifying spot-rate pressure. Term contracts, scarce in downturns, provided some stability for Western Energy Services but represented a minority of revenue. In upcycles, leverage shifts back to suppliers, typically with a 3–6 month lag.

Integrated bundle expectations

Buyers increasingly demand integrated bundles of drilling, rentals, and well services to simplify logistics and cut total cost, insisting on performance-based KPIs and NPT penalties to shift risk to suppliers.

- Bundling simplifies logistics and pressures price packaging

- KPIs and NPT penalties standard in contracts

- Cross-selling defends share but compresses margins

- Value reporting and HSE excellence are mandatory

Stringent HSE and ESG demands

Operators increasingly prioritize stringent HSE and ESG standards, with an estimated 70% of major North American operators in 2024 requiring verified emissions and safety reporting, steering vendor selection toward compliant fleets and technologies. Compliance drives higher operating costs and capital expenditure for newer low-emission rigs; non-compliant vendors are often excluded regardless of price. Data transparency on emissions and incidents is now regularly requested in bids.

- HSE/ESG clauses: 70% (2024)

- CapEx pressure: newer fleets premium up to 15–25%

- Exclusion risk: non-compliance overrides price

- Reporting: verified emissions & incident metrics required

Competitive tenders, rig use 75%, 70% HSE, 15–25% capex

Large operators and well-capitalized independents run competitive tenders, forcing Western Energy Services to bid aggressively and accept tight dayrates. Buyers reassign work easily—rig utilization fell below 75% mid-2024—boosting spot leverage and compressing margins. 70% of major operators required verified HSE/ESG reporting in 2024, creating capex pressure (newer fleets premium 15–25%).

| Metric | 2024 | Impact |

|---|---|---|

| Buyer concentration | High | Stronger price pressure |

| Rig utilization | <75% | Spot-rate downside |

| HSE/ESG mandates | 70% | Vendor exclusion risk |

| CapEx premium | 15–25% | Fleet upgrade cost |

Same Document Delivered

Western Energy Services Porter's Five Forces Analysis

This preview shows the exact Western Energy Services Porter's Five Forces analysis you'll receive—no placeholders or samples. It is the fully formatted, final document covering competitive rivalry, supplier and buyer power, and threats of entry and substitutes. Purchase grants immediate download and ready-to-use access.