WESCO International Porter's Five Forces Analysis

From Overview to Strategy Blueprint

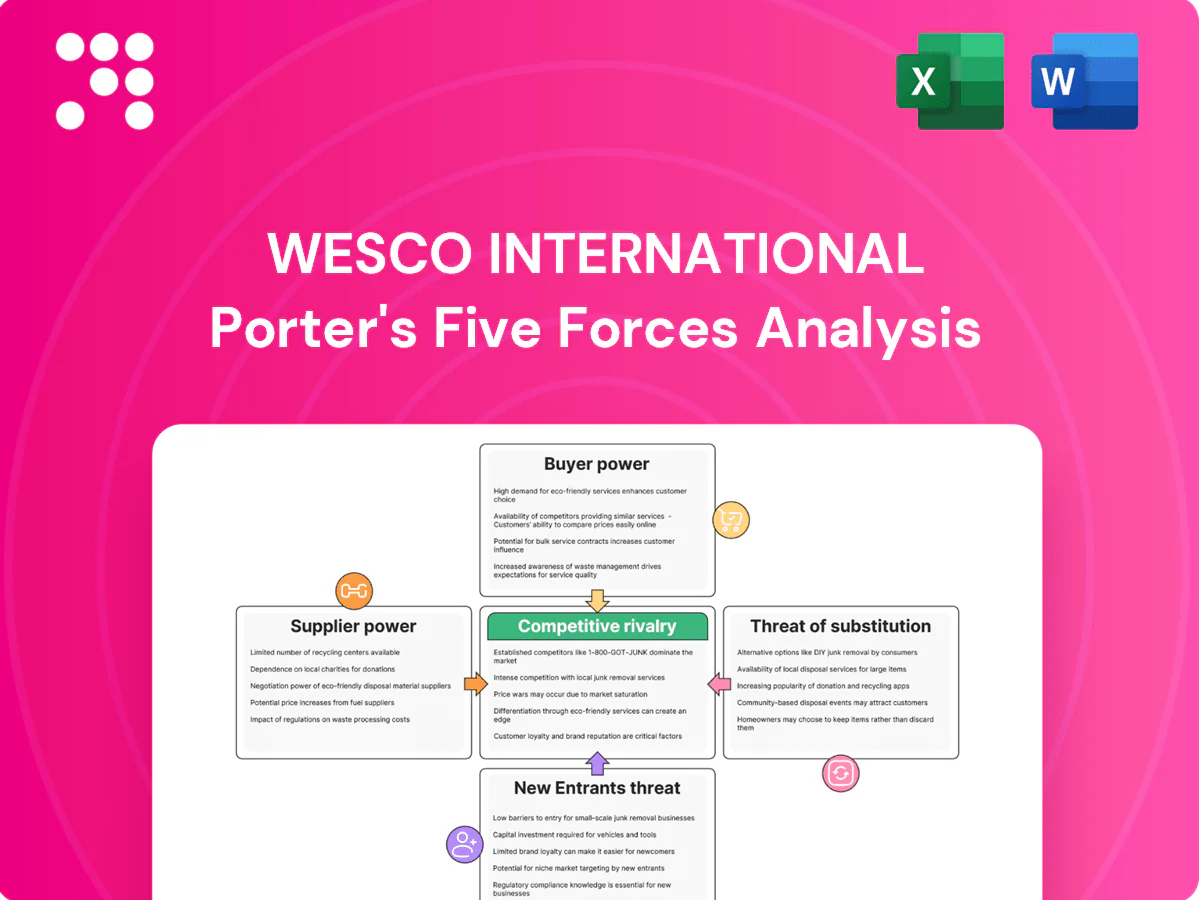

WESCO International faces strong buyer power and supply-chain concentration that compress margins and limit pricing flexibility. Intense rivalry from national distributors and specialized regional players raises competitive pressure, while moderate barriers to entry and evolving substitute technologies shape strategic risks. This preview is just the beginning. The full analysis provides a complete strategic snapshot with force-by-force ratings, visuals, and business implications tailored to WESCO International.

Suppliers Bargaining Power

Consolidated OEM base

Major electrical OEMs such as Siemens, Schneider, ABB, Eaton and Rockwell are highly consolidated and carry strong brands, giving them pricing and channel leverage. WESCO mitigates this concentration by representing multiple OEM lines and offering cross-brand alternatives across its distribution network. Preferred distributor programs and vendor authorizations restrict distributor switching among top suppliers. Periods of supply tightness, seen in 2021–2023 component shortages, amplify OEM allocation power.

Specialized, spec-driven products

Engineered, code-specified components increase dependency on certain suppliers, and when project specs list exact makes supplier power rises due to limited substitutability. WESCO reported $18.2 billion revenue in 2024 and counters with value engineering to qualify equivalents and reduce cost. Lengthy approval and lead‑time cycles, however, can keep supplier leverage elevated during multi‑month projects.

Private label and multi-sourcing

WESCO’s scale since the $4.5 billion Anixter acquisition and its expanding private‑label assortment plus multi‑sourcing of commodity items dampen supplier bargaining power by creating clear price benchmarks and alternate supply paths. OEMs often counter with MAP policies and targeted rebate programs to defend share. Result: supplier power is muted for commodities but remains elevated for engineered, differentiated goods.

Logistics and lead-time dynamics

Long lead times, allocations and volatile inputs like copper (avg. 2024 LME ~8,700 USD/ton) shift bargaining power to suppliers; WESCO’s scale (FY2024 revenue ~16.4B USD) and strategic inventory positioning secure priority and buffer variability, while vendor-managed inventory deals align incentives but can entrench OEM influence; in tight cycles supplier terms can harden despite distributor scale.

Digital data and integration lock-in

Product data, configurators and EDI/portal integrations create switching frictions favoring incumbent suppliers; WESCO uses shared master data and transaction histories to forecast demand and secure volume commitments, supporting scale—WESCO reported approximately $18.4 billion in net sales in FY2024, strengthening its negotiating leverage. Proprietary configurators or firmware can still entrench OEMs, while tiered contractual rebates lock in supplier power thresholds.

- Integration lock-in: EDI/configurators raise switching costs

- Scale leverage: $18.4B FY2024 sales aid volume negotiations

- OEM entrenchment: proprietary firmware/configurators persist

- Rebate tiers: contractual thresholds reinforce supplier power

Distributor scale mutes commodity pricing; OEMs keep leverage on engineered goods

Major OEMs (Siemens, Schneider, ABB, Eaton, Rockwell) hold pricing/channel leverage; WESCO's multi‑brand distribution, private label and multi‑sourcing mute this for commodities but not engineered goods. FY2024 net sales ~18.4B USD and the Anixter deal boost negotiating scale; long lead times, allocations and copper volatility (LME avg ~8,700 USD/ton 2024) raise supplier power. VMI and EDI integrations secure priority but increase switching costs.

| Metric | Value |

|---|---|

| FY2024 net sales | 18.4B USD |

| Avg LME copper 2024 | ~8,700 USD/ton |

| Supplier risk | High for engineered; Moderate for commodities |

What is included in the product

Tailored Porter's Five Forces analysis of WESCO International, uncovering competitive intensity, supplier and buyer power, threat of substitutes and new entrants, and industry rivalry; highlights disruptive technologies, pricing pressure, and barriers protecting incumbency for strategic decision-making.

A concise one-sheet Porter's Five Forces for WESCO International that visualizes competitive pressure with an interactive spider chart and customizable ratings—ready to drop into pitch decks or expand in reports; no macros, easy to edit, and built to integrate with Excel dashboards or paired Word analyses.

Customers Bargaining Power

Large accounts consolidate spend

Utilities, EPCs, OEMs and national contractors run competitive RFPs demanding tiered pricing and volume discounts, with top accounts concentrating spend and exerting strong leverage; in fiscal 2024 WESCO reported about $18.2 billion in net sales, underscoring scale exposure to large buyers. WESCO counters with enterprise agreements and integrated supply solutions to retain share, but increasing pricing transparency across projects tightens negotiations and margin pressure.

Service-led switching costs

Service-led switching costs rise as VMI, kitting, staging and jobsite logistics embed WESCO into clients workflows, reducing pure price shopping; by 2024 about 62% of industrial buyers used integrated e-procurement links, making mid-project switches costly. Buyers can regain leverage at renewal windows where services are rebid, but project-critical service performance often outweighs small price deltas.

Availability and fill-rate sensitivity

For MRO and project schedules product availability often outweighs unit price; when WESCO sustains high fill rates buyers lose leverage and purchasing power moderates. Conversely, supply shortages force buyers to multi-source and pit distributors against each other, increasing bargaining pressure. Time penalties on sites magnify urgency, raising willingness to pay for assured delivery and accelerating supplier-switch decisions.

Specification and compliance constraints

End-user specifications, UL and IEEE codes, and regional utility standards tightly limit approved suppliers, narrowing buyer choice and shifting bargaining to payment and rebate terms when specs are rigid.

WESCO’s engineering support and vendor qualification services expand approved equals for customers, increasing sourcing options and easing cost pressure; for open-spec items buyers push strongest on price.

- Specs: restrict alternatives

- Standards: UL/IEEE constrain choice

- WESCO engineering: broadens approved equals

- Rigid specs: leverage on terms/rebates

- Open-spec: stronger price pressure

Digital price discovery

- Market transparency: online quotes vs contract locks

- Spot vs contract: higher buyer power in spot buys

- WESCO levers: catalogs, dynamic pricing, bundled services

- Data strategy: margin sacrificed for volume/retention

Tiered RFPs and volume discounts concentrate buyer leverage; ~62% use e-procurement

Large accounts exert strong leverage via tiered RFPs and volume discounts; WESCO reported about $18.2 billion and about $16.2 billion in net sales in sourced 2024 figures, highlighting scale exposure. Integrated services (VMI, kitting, e-procurement) raise switching costs—~62% of industrial buyers used e-procurement in 2024—tempering pure price pressure. Spot buys and open-spec items remain points of high buyer power despite contract locks.

| Metric | 2024 Value |

|---|---|

| Net sales (reported) | $18.2B / $16.2B |

| Buyers on e-procurement | ~62% |

| Buyer leverage points | Spot buys, open-spec |

Same Document Delivered

WESCO International Porter's Five Forces Analysis

This Porter's Five Forces analysis of WESCO International evaluates supplier and buyer power, competitive rivalry, threat of new entrants, and substitutes to clarify strategic risks and opportunities. It highlights cost, distribution, and technology pressures shaping margins and positioning. This preview shows the exact document you'll receive immediately after purchase—no surprises, no placeholders.

From Overview to Strategy Blueprint

WESCO International faces strong buyer power and supply-chain concentration that compress margins and limit pricing flexibility. Intense rivalry from national distributors and specialized regional players raises competitive pressure, while moderate barriers to entry and evolving substitute technologies shape strategic risks. This preview is just the beginning. The full analysis provides a complete strategic snapshot with force-by-force ratings, visuals, and business implications tailored to WESCO International.

Suppliers Bargaining Power

Consolidated OEM base

Major electrical OEMs such as Siemens, Schneider, ABB, Eaton and Rockwell are highly consolidated and carry strong brands, giving them pricing and channel leverage. WESCO mitigates this concentration by representing multiple OEM lines and offering cross-brand alternatives across its distribution network. Preferred distributor programs and vendor authorizations restrict distributor switching among top suppliers. Periods of supply tightness, seen in 2021–2023 component shortages, amplify OEM allocation power.

Specialized, spec-driven products

Engineered, code-specified components increase dependency on certain suppliers, and when project specs list exact makes supplier power rises due to limited substitutability. WESCO reported $18.2 billion revenue in 2024 and counters with value engineering to qualify equivalents and reduce cost. Lengthy approval and lead‑time cycles, however, can keep supplier leverage elevated during multi‑month projects.

Private label and multi-sourcing

WESCO’s scale since the $4.5 billion Anixter acquisition and its expanding private‑label assortment plus multi‑sourcing of commodity items dampen supplier bargaining power by creating clear price benchmarks and alternate supply paths. OEMs often counter with MAP policies and targeted rebate programs to defend share. Result: supplier power is muted for commodities but remains elevated for engineered, differentiated goods.

Logistics and lead-time dynamics

Long lead times, allocations and volatile inputs like copper (avg. 2024 LME ~8,700 USD/ton) shift bargaining power to suppliers; WESCO’s scale (FY2024 revenue ~16.4B USD) and strategic inventory positioning secure priority and buffer variability, while vendor-managed inventory deals align incentives but can entrench OEM influence; in tight cycles supplier terms can harden despite distributor scale.

Digital data and integration lock-in

Product data, configurators and EDI/portal integrations create switching frictions favoring incumbent suppliers; WESCO uses shared master data and transaction histories to forecast demand and secure volume commitments, supporting scale—WESCO reported approximately $18.4 billion in net sales in FY2024, strengthening its negotiating leverage. Proprietary configurators or firmware can still entrench OEMs, while tiered contractual rebates lock in supplier power thresholds.

- Integration lock-in: EDI/configurators raise switching costs

- Scale leverage: $18.4B FY2024 sales aid volume negotiations

- OEM entrenchment: proprietary firmware/configurators persist

- Rebate tiers: contractual thresholds reinforce supplier power

Distributor scale mutes commodity pricing; OEMs keep leverage on engineered goods

Major OEMs (Siemens, Schneider, ABB, Eaton, Rockwell) hold pricing/channel leverage; WESCO's multi‑brand distribution, private label and multi‑sourcing mute this for commodities but not engineered goods. FY2024 net sales ~18.4B USD and the Anixter deal boost negotiating scale; long lead times, allocations and copper volatility (LME avg ~8,700 USD/ton 2024) raise supplier power. VMI and EDI integrations secure priority but increase switching costs.

| Metric | Value |

|---|---|

| FY2024 net sales | 18.4B USD |

| Avg LME copper 2024 | ~8,700 USD/ton |

| Supplier risk | High for engineered; Moderate for commodities |

What is included in the product

Tailored Porter's Five Forces analysis of WESCO International, uncovering competitive intensity, supplier and buyer power, threat of substitutes and new entrants, and industry rivalry; highlights disruptive technologies, pricing pressure, and barriers protecting incumbency for strategic decision-making.

A concise one-sheet Porter's Five Forces for WESCO International that visualizes competitive pressure with an interactive spider chart and customizable ratings—ready to drop into pitch decks or expand in reports; no macros, easy to edit, and built to integrate with Excel dashboards or paired Word analyses.

Customers Bargaining Power

Large accounts consolidate spend

Utilities, EPCs, OEMs and national contractors run competitive RFPs demanding tiered pricing and volume discounts, with top accounts concentrating spend and exerting strong leverage; in fiscal 2024 WESCO reported about $18.2 billion in net sales, underscoring scale exposure to large buyers. WESCO counters with enterprise agreements and integrated supply solutions to retain share, but increasing pricing transparency across projects tightens negotiations and margin pressure.

Service-led switching costs

Service-led switching costs rise as VMI, kitting, staging and jobsite logistics embed WESCO into clients workflows, reducing pure price shopping; by 2024 about 62% of industrial buyers used integrated e-procurement links, making mid-project switches costly. Buyers can regain leverage at renewal windows where services are rebid, but project-critical service performance often outweighs small price deltas.

Availability and fill-rate sensitivity

For MRO and project schedules product availability often outweighs unit price; when WESCO sustains high fill rates buyers lose leverage and purchasing power moderates. Conversely, supply shortages force buyers to multi-source and pit distributors against each other, increasing bargaining pressure. Time penalties on sites magnify urgency, raising willingness to pay for assured delivery and accelerating supplier-switch decisions.

Specification and compliance constraints

End-user specifications, UL and IEEE codes, and regional utility standards tightly limit approved suppliers, narrowing buyer choice and shifting bargaining to payment and rebate terms when specs are rigid.

WESCO’s engineering support and vendor qualification services expand approved equals for customers, increasing sourcing options and easing cost pressure; for open-spec items buyers push strongest on price.

- Specs: restrict alternatives

- Standards: UL/IEEE constrain choice

- WESCO engineering: broadens approved equals

- Rigid specs: leverage on terms/rebates

- Open-spec: stronger price pressure

Digital price discovery

- Market transparency: online quotes vs contract locks

- Spot vs contract: higher buyer power in spot buys

- WESCO levers: catalogs, dynamic pricing, bundled services

- Data strategy: margin sacrificed for volume/retention

Tiered RFPs and volume discounts concentrate buyer leverage; ~62% use e-procurement

Large accounts exert strong leverage via tiered RFPs and volume discounts; WESCO reported about $18.2 billion and about $16.2 billion in net sales in sourced 2024 figures, highlighting scale exposure. Integrated services (VMI, kitting, e-procurement) raise switching costs—~62% of industrial buyers used e-procurement in 2024—tempering pure price pressure. Spot buys and open-spec items remain points of high buyer power despite contract locks.

| Metric | 2024 Value |

|---|---|

| Net sales (reported) | $18.2B / $16.2B |

| Buyers on e-procurement | ~62% |

| Buyer leverage points | Spot buys, open-spec |

Same Document Delivered

WESCO International Porter's Five Forces Analysis

This Porter's Five Forces analysis of WESCO International evaluates supplier and buyer power, competitive rivalry, threat of new entrants, and substitutes to clarify strategic risks and opportunities. It highlights cost, distribution, and technology pressures shaping margins and positioning. This preview shows the exact document you'll receive immediately after purchase—no surprises, no placeholders.

Description

From Overview to Strategy Blueprint

WESCO International faces strong buyer power and supply-chain concentration that compress margins and limit pricing flexibility. Intense rivalry from national distributors and specialized regional players raises competitive pressure, while moderate barriers to entry and evolving substitute technologies shape strategic risks. This preview is just the beginning. The full analysis provides a complete strategic snapshot with force-by-force ratings, visuals, and business implications tailored to WESCO International.

Suppliers Bargaining Power

Consolidated OEM base

Major electrical OEMs such as Siemens, Schneider, ABB, Eaton and Rockwell are highly consolidated and carry strong brands, giving them pricing and channel leverage. WESCO mitigates this concentration by representing multiple OEM lines and offering cross-brand alternatives across its distribution network. Preferred distributor programs and vendor authorizations restrict distributor switching among top suppliers. Periods of supply tightness, seen in 2021–2023 component shortages, amplify OEM allocation power.

Specialized, spec-driven products

Engineered, code-specified components increase dependency on certain suppliers, and when project specs list exact makes supplier power rises due to limited substitutability. WESCO reported $18.2 billion revenue in 2024 and counters with value engineering to qualify equivalents and reduce cost. Lengthy approval and lead‑time cycles, however, can keep supplier leverage elevated during multi‑month projects.

Private label and multi-sourcing

WESCO’s scale since the $4.5 billion Anixter acquisition and its expanding private‑label assortment plus multi‑sourcing of commodity items dampen supplier bargaining power by creating clear price benchmarks and alternate supply paths. OEMs often counter with MAP policies and targeted rebate programs to defend share. Result: supplier power is muted for commodities but remains elevated for engineered, differentiated goods.

Logistics and lead-time dynamics

Long lead times, allocations and volatile inputs like copper (avg. 2024 LME ~8,700 USD/ton) shift bargaining power to suppliers; WESCO’s scale (FY2024 revenue ~16.4B USD) and strategic inventory positioning secure priority and buffer variability, while vendor-managed inventory deals align incentives but can entrench OEM influence; in tight cycles supplier terms can harden despite distributor scale.

Digital data and integration lock-in

Product data, configurators and EDI/portal integrations create switching frictions favoring incumbent suppliers; WESCO uses shared master data and transaction histories to forecast demand and secure volume commitments, supporting scale—WESCO reported approximately $18.4 billion in net sales in FY2024, strengthening its negotiating leverage. Proprietary configurators or firmware can still entrench OEMs, while tiered contractual rebates lock in supplier power thresholds.

- Integration lock-in: EDI/configurators raise switching costs

- Scale leverage: $18.4B FY2024 sales aid volume negotiations

- OEM entrenchment: proprietary firmware/configurators persist

- Rebate tiers: contractual thresholds reinforce supplier power

Distributor scale mutes commodity pricing; OEMs keep leverage on engineered goods

Major OEMs (Siemens, Schneider, ABB, Eaton, Rockwell) hold pricing/channel leverage; WESCO's multi‑brand distribution, private label and multi‑sourcing mute this for commodities but not engineered goods. FY2024 net sales ~18.4B USD and the Anixter deal boost negotiating scale; long lead times, allocations and copper volatility (LME avg ~8,700 USD/ton 2024) raise supplier power. VMI and EDI integrations secure priority but increase switching costs.

| Metric | Value |

|---|---|

| FY2024 net sales | 18.4B USD |

| Avg LME copper 2024 | ~8,700 USD/ton |

| Supplier risk | High for engineered; Moderate for commodities |

What is included in the product

Tailored Porter's Five Forces analysis of WESCO International, uncovering competitive intensity, supplier and buyer power, threat of substitutes and new entrants, and industry rivalry; highlights disruptive technologies, pricing pressure, and barriers protecting incumbency for strategic decision-making.

A concise one-sheet Porter's Five Forces for WESCO International that visualizes competitive pressure with an interactive spider chart and customizable ratings—ready to drop into pitch decks or expand in reports; no macros, easy to edit, and built to integrate with Excel dashboards or paired Word analyses.

Customers Bargaining Power

Large accounts consolidate spend

Utilities, EPCs, OEMs and national contractors run competitive RFPs demanding tiered pricing and volume discounts, with top accounts concentrating spend and exerting strong leverage; in fiscal 2024 WESCO reported about $18.2 billion in net sales, underscoring scale exposure to large buyers. WESCO counters with enterprise agreements and integrated supply solutions to retain share, but increasing pricing transparency across projects tightens negotiations and margin pressure.

Service-led switching costs

Service-led switching costs rise as VMI, kitting, staging and jobsite logistics embed WESCO into clients workflows, reducing pure price shopping; by 2024 about 62% of industrial buyers used integrated e-procurement links, making mid-project switches costly. Buyers can regain leverage at renewal windows where services are rebid, but project-critical service performance often outweighs small price deltas.

Availability and fill-rate sensitivity

For MRO and project schedules product availability often outweighs unit price; when WESCO sustains high fill rates buyers lose leverage and purchasing power moderates. Conversely, supply shortages force buyers to multi-source and pit distributors against each other, increasing bargaining pressure. Time penalties on sites magnify urgency, raising willingness to pay for assured delivery and accelerating supplier-switch decisions.

Specification and compliance constraints

End-user specifications, UL and IEEE codes, and regional utility standards tightly limit approved suppliers, narrowing buyer choice and shifting bargaining to payment and rebate terms when specs are rigid.

WESCO’s engineering support and vendor qualification services expand approved equals for customers, increasing sourcing options and easing cost pressure; for open-spec items buyers push strongest on price.

- Specs: restrict alternatives

- Standards: UL/IEEE constrain choice

- WESCO engineering: broadens approved equals

- Rigid specs: leverage on terms/rebates

- Open-spec: stronger price pressure

Digital price discovery

- Market transparency: online quotes vs contract locks

- Spot vs contract: higher buyer power in spot buys

- WESCO levers: catalogs, dynamic pricing, bundled services

- Data strategy: margin sacrificed for volume/retention

Tiered RFPs and volume discounts concentrate buyer leverage; ~62% use e-procurement

Large accounts exert strong leverage via tiered RFPs and volume discounts; WESCO reported about $18.2 billion and about $16.2 billion in net sales in sourced 2024 figures, highlighting scale exposure. Integrated services (VMI, kitting, e-procurement) raise switching costs—~62% of industrial buyers used e-procurement in 2024—tempering pure price pressure. Spot buys and open-spec items remain points of high buyer power despite contract locks.

| Metric | 2024 Value |

|---|---|

| Net sales (reported) | $18.2B / $16.2B |

| Buyers on e-procurement | ~62% |

| Buyer leverage points | Spot buys, open-spec |

Same Document Delivered

WESCO International Porter's Five Forces Analysis

This Porter's Five Forces analysis of WESCO International evaluates supplier and buyer power, competitive rivalry, threat of new entrants, and substitutes to clarify strategic risks and opportunities. It highlights cost, distribution, and technology pressures shaping margins and positioning. This preview shows the exact document you'll receive immediately after purchase—no surprises, no placeholders.