WESCO International PESTLE Analysis

Skip the Research. Get the Strategy.

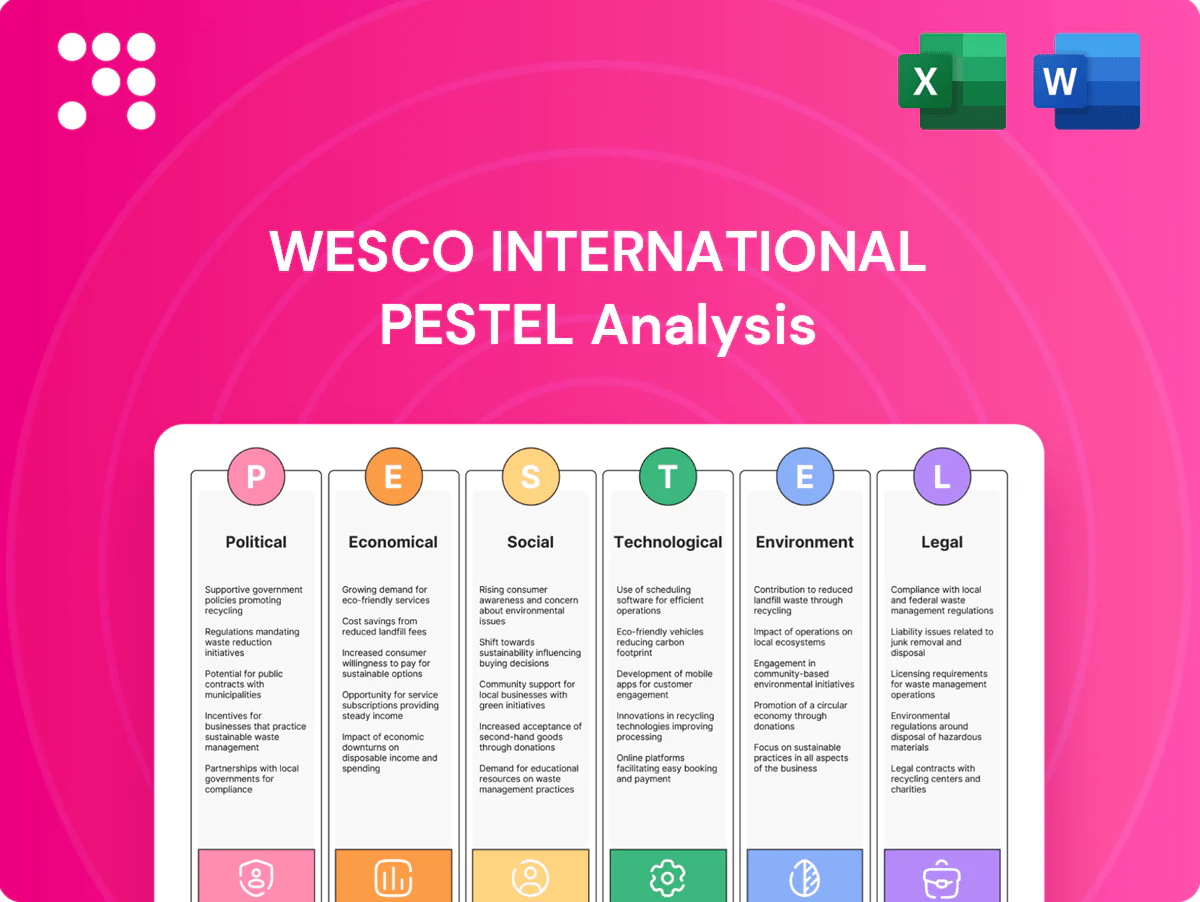

Discover how political shifts, economic cycles, social trends, technological advances, legal changes, and environmental pressures shape WESCO International’s strategic outlook in this concise PESTLE snapshot. Our full analysis dives deeper into risk exposures and growth levers to inform investment and planning decisions. Purchase the complete PESTLE report for actionable, ready-to-use insights and downloadable templates.

Political factors

Infrastructure spending priorities

The $1.2 trillion Bipartisan Infrastructure Law, including roughly $550 billion in new federal investment, plus $65 billion BEAD broadband funding and $110 billion for roads and bridges, directly expands demand for WESCO’s electrical and communications products. Policy cycles and election outcomes can accelerate or delay project starts and fund releases, creating revenue timing variance. Public–private partnership models open channels but add compliance and reporting overhead. Monitoring federal and state appropriations helps align inventory and sales focus.

Trade policy and tariffs

Tariffs on electrical components, metals and electronics—notably U.S. steel (25%) and aluminum (10%) duties and Section 301 levies covering roughly $360 billion of Chinese goods—raise WESCO’s input costs and compress pricing flexibility. Shifts in U.S.–China and other bilateral policies have lengthened lead times and increased freight volatility. Preferential trade agreements such as USMCA and regional FTAs can lower cost-to-serve in targeted markets. Diversifying suppliers across Asia, Europe and the Americas mitigates political trade shocks.

Government procurement rules

Buy American preferences, the Trade Agreements Act threshold tied to the simplified acquisition threshold of $250,000, and small‑business set‑aside programs (statutory federal small business contracting goal 23%) shape WESCO International’s eligibility and product mix for public contracts. Compliance adds documentation and supplier qualification overhead, raising bid preparation costs. Lengthy federal procurement cycles delay revenue recognition and cash flow. Securing approved vendor status boosts win rates and long‑term positioning.

Geopolitical supply chain risks

Geopolitical shocks since 2022 have interrupted component flows and logistics corridors, while sanctions increase customs scrutiny and delay deliveries; port congestion spikes during tensions raise lead times for electrical and network components. Multi-region inventory buffers and nearshoring implemented in 2023–2024 reduce exposure, and scenario planning supports service continuity for critical infrastructure clients.

Energy and electrification policy

Inflation Reduction Act expansions and federal incentives (EV tax credit up to $7,500) are enlarging renewables, EV and grid-hardening markets; tightening emissions rules drive demand for industrial efficiency and power-quality upgrades, and policy stability shapes long-horizon customer CAPEX, enabling WESCO to align product and services with funded electrification programs.

- Incentives expand addressable market

- Emissions rules boost upgrade demand

- Policy stability affects CAPEX timing

- WESCO can link to funded programs

Federal funding, IRA EV credits and tariffs force nearshoring, raising timing and compliance risk

Federal programs (Bipartisan Infrastructure Law $1.2T; ~$550B new; BEAD $65B) and IRA incentives (EV credit up to $7,500) expand WESCO’s addressable market but create timing risk tied to appropriations and election cycles. Tariffs (U.S. steel 25%, aluminum 10%; Section 301 ≈$360B) raise input costs and lengthen lead times, driving nearshoring and inventory buffers. Buy American, TAA thresholds ($250,000) and 23% small‑business contracting goal increase compliance and bid overhead.

| Issue | 2024–25 Impact |

|---|---|

| Infrastructure funding | $1.2T; ~$550B new |

| BEAD | $65B |

| Tariffs | Steel 25% / Al 10% / Sect301 ≈$360B |

| Procurement | TAA $250k; 23% goal |

What is included in the product

Explores how macro-environmental factors uniquely affect WESCO International across Political, Economic, Social, Technological, Environmental and Legal dimensions, with data-backed trends and forward-looking insights to help executives, consultants and investors identify risks, opportunities and strategic responses.

Concise PESTLE summary of WESCO International that’s visually segmented for quick reference during meetings, easily dropped into presentations, and editable for region- or business-specific notes to streamline risk discussions and strategic planning.

Economic factors

Construction and industrial cycles

Non-residential construction spending near $1.0 trillion in 2023 and a modest 1.2% rise in U.S. industrial production through 2024 drive WESCO order volumes, with MRO demand proving more resilient than OEM replacement cycles but still following cyclicality. WESCO reported a backlog around $1.1 billion in FY2024 that smooths near-term volatility yet can unwind quickly in downturns. Diversification across utilities, data centers, and industrial end markets reduces exposure to any single sector and lowers beta.

Interest rates and credit

Higher interest rates (US policy rate 5.25–5.50% in 2024–25) raise WESCO's inventory carrying costs and make customer financing harder, leading to more project deferrals as borrowing costs climb. With 10-year Treasury yields near 4% in 2024, working-capital discipline preserves liquidity and flexibility during tightening cycles. Vendor financing programs and captive credit lines can sustain sales momentum by easing customer purchase hurdles.

Commodity price pass-through

Copper (~$9,500/t), aluminum (~$2,300/t) and resin (~$1,100/t) swings in 2024–25 materially move WESCO product pricing and margins, with effective pass-through protecting gross margin but often dampening end-market volume. Volatility has triggered customer forward-buying and periodic destocking, amplifying working-capital swings. Transparent surcharge mechanisms and selective hedging reduce earnings surprises and stabilize margin trajectory.

FX and international exposure

Currency movements materially affect WESCO International’s reported results and cross-border sourcing economics, compressing margins when the US dollar strengthens against purchasing currencies; localized pricing and regional procurement create natural hedges that blunt this effect. The company’s hedging policies aim to smooth quarterly earnings variability and protect margins during volatile FX periods.

- FX affects reported revenue and sourcing costs

- Localized pricing mitigates margin compression

- Regional procurement provides natural hedge

- Active hedging policies reduce earnings volatility

Industry consolidation dynamics

- scale: procurement leverage, network density

- integration: drives cost synergies & continuity

- competition: pricing/service pressure from large peers

- M&A: targeted deals to close capability/geography gaps

Federal funding, IRA EV credits and tariffs force nearshoring, raising timing and compliance risk

Non-residential construction ~$1.0T (2023) and 1.2% industrial-prod. growth thru 2024 support demand; WESCO backlog ~$1.1B (FY2024) smooths near-term volatility. US policy rate 5.25–5.50% (2024–25) and 10y ~4% raise financing and inventory costs, pressuring project timing. Commodity swings (copper ~$9,500/t; aluminum ~$2,300/t; resin ~$1,100/t) drive pricing, margin pass-through and working-capital swings.

| Metric | Value |

|---|---|

| Construction spend (2023) | $1.0T |

| WESCO backlog (FY2024) | $1.1B |

| US policy rate (2024–25) | 5.25–5.50% |

| Copper (2024) | $9,500/t |

Same Document Delivered

WESCO International PESTLE Analysis

The preview shown here is the exact WESCO International PESTLE Analysis you’ll receive after purchase—fully formatted and ready to use. The layout, content, and structure visible here are exactly what you’ll download immediately after buying. No placeholders or teasers; this is the final, professionally structured file.

Skip the Research. Get the Strategy.

Discover how political shifts, economic cycles, social trends, technological advances, legal changes, and environmental pressures shape WESCO International’s strategic outlook in this concise PESTLE snapshot. Our full analysis dives deeper into risk exposures and growth levers to inform investment and planning decisions. Purchase the complete PESTLE report for actionable, ready-to-use insights and downloadable templates.

Political factors

Infrastructure spending priorities

The $1.2 trillion Bipartisan Infrastructure Law, including roughly $550 billion in new federal investment, plus $65 billion BEAD broadband funding and $110 billion for roads and bridges, directly expands demand for WESCO’s electrical and communications products. Policy cycles and election outcomes can accelerate or delay project starts and fund releases, creating revenue timing variance. Public–private partnership models open channels but add compliance and reporting overhead. Monitoring federal and state appropriations helps align inventory and sales focus.

Trade policy and tariffs

Tariffs on electrical components, metals and electronics—notably U.S. steel (25%) and aluminum (10%) duties and Section 301 levies covering roughly $360 billion of Chinese goods—raise WESCO’s input costs and compress pricing flexibility. Shifts in U.S.–China and other bilateral policies have lengthened lead times and increased freight volatility. Preferential trade agreements such as USMCA and regional FTAs can lower cost-to-serve in targeted markets. Diversifying suppliers across Asia, Europe and the Americas mitigates political trade shocks.

Government procurement rules

Buy American preferences, the Trade Agreements Act threshold tied to the simplified acquisition threshold of $250,000, and small‑business set‑aside programs (statutory federal small business contracting goal 23%) shape WESCO International’s eligibility and product mix for public contracts. Compliance adds documentation and supplier qualification overhead, raising bid preparation costs. Lengthy federal procurement cycles delay revenue recognition and cash flow. Securing approved vendor status boosts win rates and long‑term positioning.

Geopolitical supply chain risks

Geopolitical shocks since 2022 have interrupted component flows and logistics corridors, while sanctions increase customs scrutiny and delay deliveries; port congestion spikes during tensions raise lead times for electrical and network components. Multi-region inventory buffers and nearshoring implemented in 2023–2024 reduce exposure, and scenario planning supports service continuity for critical infrastructure clients.

Energy and electrification policy

Inflation Reduction Act expansions and federal incentives (EV tax credit up to $7,500) are enlarging renewables, EV and grid-hardening markets; tightening emissions rules drive demand for industrial efficiency and power-quality upgrades, and policy stability shapes long-horizon customer CAPEX, enabling WESCO to align product and services with funded electrification programs.

- Incentives expand addressable market

- Emissions rules boost upgrade demand

- Policy stability affects CAPEX timing

- WESCO can link to funded programs

Federal funding, IRA EV credits and tariffs force nearshoring, raising timing and compliance risk

Federal programs (Bipartisan Infrastructure Law $1.2T; ~$550B new; BEAD $65B) and IRA incentives (EV credit up to $7,500) expand WESCO’s addressable market but create timing risk tied to appropriations and election cycles. Tariffs (U.S. steel 25%, aluminum 10%; Section 301 ≈$360B) raise input costs and lengthen lead times, driving nearshoring and inventory buffers. Buy American, TAA thresholds ($250,000) and 23% small‑business contracting goal increase compliance and bid overhead.

| Issue | 2024–25 Impact |

|---|---|

| Infrastructure funding | $1.2T; ~$550B new |

| BEAD | $65B |

| Tariffs | Steel 25% / Al 10% / Sect301 ≈$360B |

| Procurement | TAA $250k; 23% goal |

What is included in the product

Explores how macro-environmental factors uniquely affect WESCO International across Political, Economic, Social, Technological, Environmental and Legal dimensions, with data-backed trends and forward-looking insights to help executives, consultants and investors identify risks, opportunities and strategic responses.

Concise PESTLE summary of WESCO International that’s visually segmented for quick reference during meetings, easily dropped into presentations, and editable for region- or business-specific notes to streamline risk discussions and strategic planning.

Economic factors

Construction and industrial cycles

Non-residential construction spending near $1.0 trillion in 2023 and a modest 1.2% rise in U.S. industrial production through 2024 drive WESCO order volumes, with MRO demand proving more resilient than OEM replacement cycles but still following cyclicality. WESCO reported a backlog around $1.1 billion in FY2024 that smooths near-term volatility yet can unwind quickly in downturns. Diversification across utilities, data centers, and industrial end markets reduces exposure to any single sector and lowers beta.

Interest rates and credit

Higher interest rates (US policy rate 5.25–5.50% in 2024–25) raise WESCO's inventory carrying costs and make customer financing harder, leading to more project deferrals as borrowing costs climb. With 10-year Treasury yields near 4% in 2024, working-capital discipline preserves liquidity and flexibility during tightening cycles. Vendor financing programs and captive credit lines can sustain sales momentum by easing customer purchase hurdles.

Commodity price pass-through

Copper (~$9,500/t), aluminum (~$2,300/t) and resin (~$1,100/t) swings in 2024–25 materially move WESCO product pricing and margins, with effective pass-through protecting gross margin but often dampening end-market volume. Volatility has triggered customer forward-buying and periodic destocking, amplifying working-capital swings. Transparent surcharge mechanisms and selective hedging reduce earnings surprises and stabilize margin trajectory.

FX and international exposure

Currency movements materially affect WESCO International’s reported results and cross-border sourcing economics, compressing margins when the US dollar strengthens against purchasing currencies; localized pricing and regional procurement create natural hedges that blunt this effect. The company’s hedging policies aim to smooth quarterly earnings variability and protect margins during volatile FX periods.

- FX affects reported revenue and sourcing costs

- Localized pricing mitigates margin compression

- Regional procurement provides natural hedge

- Active hedging policies reduce earnings volatility

Industry consolidation dynamics

- scale: procurement leverage, network density

- integration: drives cost synergies & continuity

- competition: pricing/service pressure from large peers

- M&A: targeted deals to close capability/geography gaps

Federal funding, IRA EV credits and tariffs force nearshoring, raising timing and compliance risk

Non-residential construction ~$1.0T (2023) and 1.2% industrial-prod. growth thru 2024 support demand; WESCO backlog ~$1.1B (FY2024) smooths near-term volatility. US policy rate 5.25–5.50% (2024–25) and 10y ~4% raise financing and inventory costs, pressuring project timing. Commodity swings (copper ~$9,500/t; aluminum ~$2,300/t; resin ~$1,100/t) drive pricing, margin pass-through and working-capital swings.

| Metric | Value |

|---|---|

| Construction spend (2023) | $1.0T |

| WESCO backlog (FY2024) | $1.1B |

| US policy rate (2024–25) | 5.25–5.50% |

| Copper (2024) | $9,500/t |

Same Document Delivered

WESCO International PESTLE Analysis

The preview shown here is the exact WESCO International PESTLE Analysis you’ll receive after purchase—fully formatted and ready to use. The layout, content, and structure visible here are exactly what you’ll download immediately after buying. No placeholders or teasers; this is the final, professionally structured file.

Original: $10.00

-65%$10.00

$3.50Description

Skip the Research. Get the Strategy.

Discover how political shifts, economic cycles, social trends, technological advances, legal changes, and environmental pressures shape WESCO International’s strategic outlook in this concise PESTLE snapshot. Our full analysis dives deeper into risk exposures and growth levers to inform investment and planning decisions. Purchase the complete PESTLE report for actionable, ready-to-use insights and downloadable templates.

Political factors

Infrastructure spending priorities

The $1.2 trillion Bipartisan Infrastructure Law, including roughly $550 billion in new federal investment, plus $65 billion BEAD broadband funding and $110 billion for roads and bridges, directly expands demand for WESCO’s electrical and communications products. Policy cycles and election outcomes can accelerate or delay project starts and fund releases, creating revenue timing variance. Public–private partnership models open channels but add compliance and reporting overhead. Monitoring federal and state appropriations helps align inventory and sales focus.

Trade policy and tariffs

Tariffs on electrical components, metals and electronics—notably U.S. steel (25%) and aluminum (10%) duties and Section 301 levies covering roughly $360 billion of Chinese goods—raise WESCO’s input costs and compress pricing flexibility. Shifts in U.S.–China and other bilateral policies have lengthened lead times and increased freight volatility. Preferential trade agreements such as USMCA and regional FTAs can lower cost-to-serve in targeted markets. Diversifying suppliers across Asia, Europe and the Americas mitigates political trade shocks.

Government procurement rules

Buy American preferences, the Trade Agreements Act threshold tied to the simplified acquisition threshold of $250,000, and small‑business set‑aside programs (statutory federal small business contracting goal 23%) shape WESCO International’s eligibility and product mix for public contracts. Compliance adds documentation and supplier qualification overhead, raising bid preparation costs. Lengthy federal procurement cycles delay revenue recognition and cash flow. Securing approved vendor status boosts win rates and long‑term positioning.

Geopolitical supply chain risks

Geopolitical shocks since 2022 have interrupted component flows and logistics corridors, while sanctions increase customs scrutiny and delay deliveries; port congestion spikes during tensions raise lead times for electrical and network components. Multi-region inventory buffers and nearshoring implemented in 2023–2024 reduce exposure, and scenario planning supports service continuity for critical infrastructure clients.

Energy and electrification policy

Inflation Reduction Act expansions and federal incentives (EV tax credit up to $7,500) are enlarging renewables, EV and grid-hardening markets; tightening emissions rules drive demand for industrial efficiency and power-quality upgrades, and policy stability shapes long-horizon customer CAPEX, enabling WESCO to align product and services with funded electrification programs.

- Incentives expand addressable market

- Emissions rules boost upgrade demand

- Policy stability affects CAPEX timing

- WESCO can link to funded programs

Federal funding, IRA EV credits and tariffs force nearshoring, raising timing and compliance risk

Federal programs (Bipartisan Infrastructure Law $1.2T; ~$550B new; BEAD $65B) and IRA incentives (EV credit up to $7,500) expand WESCO’s addressable market but create timing risk tied to appropriations and election cycles. Tariffs (U.S. steel 25%, aluminum 10%; Section 301 ≈$360B) raise input costs and lengthen lead times, driving nearshoring and inventory buffers. Buy American, TAA thresholds ($250,000) and 23% small‑business contracting goal increase compliance and bid overhead.

| Issue | 2024–25 Impact |

|---|---|

| Infrastructure funding | $1.2T; ~$550B new |

| BEAD | $65B |

| Tariffs | Steel 25% / Al 10% / Sect301 ≈$360B |

| Procurement | TAA $250k; 23% goal |

What is included in the product

Explores how macro-environmental factors uniquely affect WESCO International across Political, Economic, Social, Technological, Environmental and Legal dimensions, with data-backed trends and forward-looking insights to help executives, consultants and investors identify risks, opportunities and strategic responses.

Concise PESTLE summary of WESCO International that’s visually segmented for quick reference during meetings, easily dropped into presentations, and editable for region- or business-specific notes to streamline risk discussions and strategic planning.

Economic factors

Construction and industrial cycles

Non-residential construction spending near $1.0 trillion in 2023 and a modest 1.2% rise in U.S. industrial production through 2024 drive WESCO order volumes, with MRO demand proving more resilient than OEM replacement cycles but still following cyclicality. WESCO reported a backlog around $1.1 billion in FY2024 that smooths near-term volatility yet can unwind quickly in downturns. Diversification across utilities, data centers, and industrial end markets reduces exposure to any single sector and lowers beta.

Interest rates and credit

Higher interest rates (US policy rate 5.25–5.50% in 2024–25) raise WESCO's inventory carrying costs and make customer financing harder, leading to more project deferrals as borrowing costs climb. With 10-year Treasury yields near 4% in 2024, working-capital discipline preserves liquidity and flexibility during tightening cycles. Vendor financing programs and captive credit lines can sustain sales momentum by easing customer purchase hurdles.

Commodity price pass-through

Copper (~$9,500/t), aluminum (~$2,300/t) and resin (~$1,100/t) swings in 2024–25 materially move WESCO product pricing and margins, with effective pass-through protecting gross margin but often dampening end-market volume. Volatility has triggered customer forward-buying and periodic destocking, amplifying working-capital swings. Transparent surcharge mechanisms and selective hedging reduce earnings surprises and stabilize margin trajectory.

FX and international exposure

Currency movements materially affect WESCO International’s reported results and cross-border sourcing economics, compressing margins when the US dollar strengthens against purchasing currencies; localized pricing and regional procurement create natural hedges that blunt this effect. The company’s hedging policies aim to smooth quarterly earnings variability and protect margins during volatile FX periods.

- FX affects reported revenue and sourcing costs

- Localized pricing mitigates margin compression

- Regional procurement provides natural hedge

- Active hedging policies reduce earnings volatility

Industry consolidation dynamics

- scale: procurement leverage, network density

- integration: drives cost synergies & continuity

- competition: pricing/service pressure from large peers

- M&A: targeted deals to close capability/geography gaps

Federal funding, IRA EV credits and tariffs force nearshoring, raising timing and compliance risk

Non-residential construction ~$1.0T (2023) and 1.2% industrial-prod. growth thru 2024 support demand; WESCO backlog ~$1.1B (FY2024) smooths near-term volatility. US policy rate 5.25–5.50% (2024–25) and 10y ~4% raise financing and inventory costs, pressuring project timing. Commodity swings (copper ~$9,500/t; aluminum ~$2,300/t; resin ~$1,100/t) drive pricing, margin pass-through and working-capital swings.

| Metric | Value |

|---|---|

| Construction spend (2023) | $1.0T |

| WESCO backlog (FY2024) | $1.1B |

| US policy rate (2024–25) | 5.25–5.50% |

| Copper (2024) | $9,500/t |

Same Document Delivered

WESCO International PESTLE Analysis

The preview shown here is the exact WESCO International PESTLE Analysis you’ll receive after purchase—fully formatted and ready to use. The layout, content, and structure visible here are exactly what you’ll download immediately after buying. No placeholders or teasers; this is the final, professionally structured file.