Westamerica Bank Porter's Five Forces Analysis

Go Beyond the Preview—Access the Full Strategic Report

Westamerica Bank operates in a niche regional banking market with stable customer relationships, moderate regulatory pressure, and competitive threats from larger banks and fintechs. Its loan portfolio strength counters some substitution risk but limits scale benefits. This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis to explore force-by-force ratings, visuals, and actionable strategy insights.

Suppliers Bargaining Power

Concentrated core tech vendors

Westamerica relies on a few core banking platforms, payments processors, and ATM networks, concentrating supplier power and giving vendors leverage over pricing and contract terms.

High switching costs, complex integrations, and regulatory validation make vendor changes rare, allowing vendors to dictate upgrade roadmaps and squeeze margins.

Vendor outages or implementation delays can directly harm customer experience and operational continuity, increasing reputational and compliance risk.

Funding providers and depositors

Depositors are Westamerica’s primary funding suppliers and became more rate-sensitive as the fed funds rate stayed at 5.25–5.50% through 2024, so greater yield demands push Westamerica’s cost of funds and compress NIM. Wholesale alternatives such as FHLB advances can replace deposits but generally carry higher, more volatile funding costs. Maintaining a stable core deposit mix reduces supplier bargaining power.

Skilled labor and compliance talent

Experienced bankers, credit underwriters, and compliance officers remain scarce in California, where the 2024 unemployment rate averaged about 4.4%, tightening labor supply for financial services.

Wage inflation in 2024 saw financial-sector pay rise roughly 4% year-over-year, increasing employees’ bargaining power and raising recruitment costs.

Higher retention and hiring expenses have pushed operating costs up for regional banks like Westamerica, while talent shortages can delay growth and risk-management initiatives.

Regulators as gatekeepers

Regulators act as gatekeepers: banking licenses, capital rules and supervisory expectations effectively supply permission to operate for Westamerica, and 2024 supervisory scrutiny after industry stress raised compliance and systems upgrade costs that compress margins.

Examination findings can limit growth or strategy, giving regulators indirect supplier power over branch expansion, lending limits and product offerings.

- Regulatory permission is a de facto input

- 2024-era compliance upgrades raise operating costs

- Examinations can constrain strategy and growth

Data, cybersecurity, and cloud providers

Specialized data feeds, fraud tools, and cloud infrastructure are essential for Westamerica Bank; top cloud vendors hold concentrated share (AWS ~32%, Azure ~23%, Google ~11% in 2024 per Synergy Research), narrowing alternatives and raising supplier pricing power. High security and uptime requirements increase switching costs, while vendor outages or poor performance directly raise regulatory, risk, and compliance impact.

- Limited vendors

- High switching cost

- Direct compliance risk

- Cloud market concentration

Suppliers exert moderate-high power; top-three cloud share 66%

Suppliers (core platforms, cloud, payments, talent, regulators, depositors) hold moderate-to-high power: cloud concentration (AWS 32%, Azure 23%, Google 11% in 2024) and integration costs raise switching barriers; depositors pushed yields as fed funds sat at 5.25–5.50% in 2024; CA unemployment 4.4% and 4% y/y wage growth tightened labor supply.

| Supplier | 2024 metric |

|---|---|

| Cloud share | AWS 32% / Azure 23% / GCP 11% |

| Fed funds | 5.25–5.50% |

| CA unemployment | 4.4% |

| Wage growth | ~4% y/y |

What is included in the product

Tailored Porter's Five Forces analysis for Westamerica Bank that uncovers key drivers of competition, customer bargaining power, and market entry risks while identifying disruptive threats and substitutes; evaluates supplier/buyer influence on pricing and profitability and highlights dynamics that protect incumbents. Fully editable for reports and strategy decks.

Clear one-sheet Porter's Five Forces for Westamerica Bank—instantly visualize competitive pressures with a radar chart, customize force levels with your data, and drop a clean, no-macro sheet straight into pitch decks or executive reports.

Customers Bargaining Power

Rate-shopping retail depositors

Consumers can compare deposit rates instantly via apps and aggregators, boosting bargaining power. In 2024 money market and 1-year CD yields near 4–4.5% versus median savings APY ~0.4%, prompting rapid fund shifts. Westamerica must match pricing or add value to retain deposits. That squeezes net interest margins and raises acquisition costs.

SMB and commercial clients

SMB and commercial clients exert moderate bargaining power at Westamerica Bank: roughly 70% of SMBs multi-bank (2024 surveys), enabling negotiation on lending rates, covenants and fees. Treasury services create stickiness—client retention for payment/treasury products averages over 80% industry-wide in 2024—tempering price pressure. Deep relationships and high service quality reduce buyer leverage despite ongoing rate competition.

Affluent clients with alternatives

Affluent clients can move high balances into brokered sweep accounts or 3-month T-bills, which averaged about 5% in 2024, increasing pressure on Westamerica to match yield and service. Their mobility raises bargaining power and losing a few large accounts can materially affect funding and liquidity. Westamerica must segment these clients and tailor competitive yield, sweep options, and concierge service to retain them.

Digital expectations and low switching friction

Enhanced digital capabilities across competitors have reduced perceived switching costs; by 2024 about 80% of U.S. consumers used mobile banking, enabling rapid online migrations when features lag. Customers can move accounts with minimal effort, increasing buyer leverage over features and fees and pressuring margins. Continuous UX and feature investment is required to dampen this power and retain deposits.

- 2024 mobile banking adoption ~80%

- Low digital switching friction increases fee/feature pressure

- Ongoing UX spend needed to defend deposits

Credit customers’ negotiation leverage

Creditworthy borrowers can pit lenders against each other for better rates and structures, with Westamerica Bancorporation (WABC) reporting about $6.3B in assets in 2024, increasing competitive pressure on yields. Collateral-rich loans face aggressive bidding in stable markets, and covenant-light trends have risen, compressing risk-adjusted returns. Underwriting discipline must balance share retention and credit quality to avoid margin erosion.

- Debt shopping: higher borrower leverage on pricing

- Collateral bidding: tighter spreads in stable cycles

- Covenant-light: pressure on protections and returns

- Underwriting trade-off: growth versus credit discipline

Customers wield pricing power: mobile ~80%, MM/CD 4–4.5%, 3-mo T-bill ~5%

Customers hold elevated bargaining power: retail can chase 4–4.5% money‑market/1‑yr CD yields vs median savings APY ~0.4% (2024), mobile banking adoption ~80% lowers switching friction, and affluent balances can shift into 3‑month T‑bills ~5% (2024). SMBs (~70% multi‑bank) and $6.3B WABC asset base force competitive pricing and tailored service to retain deposits.

| Metric | 2024 Value |

|---|---|

| Mobile adoption | ~80% |

| Money‑market/1yr CD | 4–4.5% |

| Median savings APY | ~0.4% |

| 3‑month T‑bill | ~5% |

| SMB multi‑bank | ~70% |

| WABC assets | $6.3B |

Preview the Actual Deliverable

Westamerica Bank Porter's Five Forces Analysis

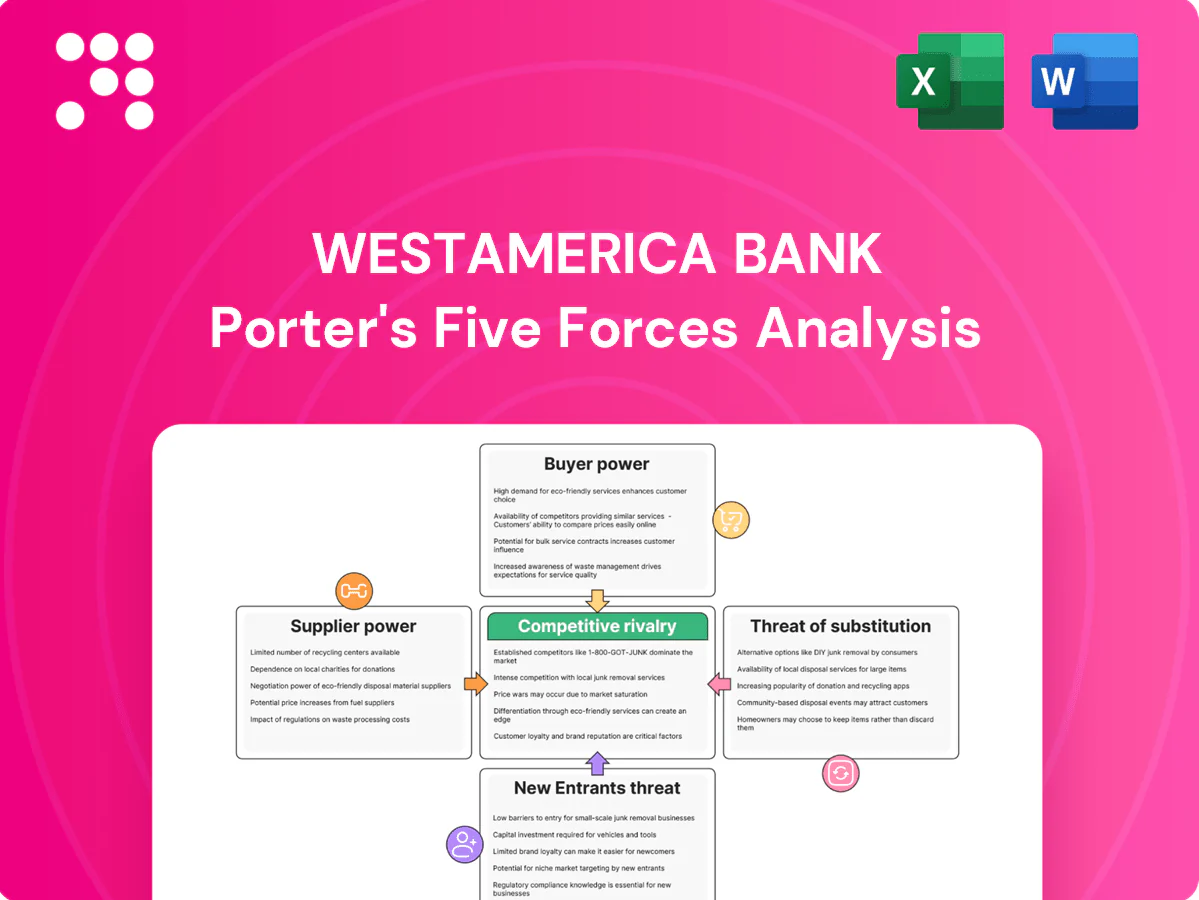

This preview is the exact Westamerica Bank Porter's Five Forces Analysis you'll receive—no samples or placeholders. It contains the full, professionally formatted assessment of competitive rivalry, supplier and buyer power, threats of entry and substitution, and strategic implications. Purchase grants immediate download of this identical file, ready for use.

Go Beyond the Preview—Access the Full Strategic Report

Westamerica Bank operates in a niche regional banking market with stable customer relationships, moderate regulatory pressure, and competitive threats from larger banks and fintechs. Its loan portfolio strength counters some substitution risk but limits scale benefits. This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis to explore force-by-force ratings, visuals, and actionable strategy insights.

Suppliers Bargaining Power

Concentrated core tech vendors

Westamerica relies on a few core banking platforms, payments processors, and ATM networks, concentrating supplier power and giving vendors leverage over pricing and contract terms.

High switching costs, complex integrations, and regulatory validation make vendor changes rare, allowing vendors to dictate upgrade roadmaps and squeeze margins.

Vendor outages or implementation delays can directly harm customer experience and operational continuity, increasing reputational and compliance risk.

Funding providers and depositors

Depositors are Westamerica’s primary funding suppliers and became more rate-sensitive as the fed funds rate stayed at 5.25–5.50% through 2024, so greater yield demands push Westamerica’s cost of funds and compress NIM. Wholesale alternatives such as FHLB advances can replace deposits but generally carry higher, more volatile funding costs. Maintaining a stable core deposit mix reduces supplier bargaining power.

Skilled labor and compliance talent

Experienced bankers, credit underwriters, and compliance officers remain scarce in California, where the 2024 unemployment rate averaged about 4.4%, tightening labor supply for financial services.

Wage inflation in 2024 saw financial-sector pay rise roughly 4% year-over-year, increasing employees’ bargaining power and raising recruitment costs.

Higher retention and hiring expenses have pushed operating costs up for regional banks like Westamerica, while talent shortages can delay growth and risk-management initiatives.

Regulators as gatekeepers

Regulators act as gatekeepers: banking licenses, capital rules and supervisory expectations effectively supply permission to operate for Westamerica, and 2024 supervisory scrutiny after industry stress raised compliance and systems upgrade costs that compress margins.

Examination findings can limit growth or strategy, giving regulators indirect supplier power over branch expansion, lending limits and product offerings.

- Regulatory permission is a de facto input

- 2024-era compliance upgrades raise operating costs

- Examinations can constrain strategy and growth

Data, cybersecurity, and cloud providers

Specialized data feeds, fraud tools, and cloud infrastructure are essential for Westamerica Bank; top cloud vendors hold concentrated share (AWS ~32%, Azure ~23%, Google ~11% in 2024 per Synergy Research), narrowing alternatives and raising supplier pricing power. High security and uptime requirements increase switching costs, while vendor outages or poor performance directly raise regulatory, risk, and compliance impact.

- Limited vendors

- High switching cost

- Direct compliance risk

- Cloud market concentration

Suppliers exert moderate-high power; top-three cloud share 66%

Suppliers (core platforms, cloud, payments, talent, regulators, depositors) hold moderate-to-high power: cloud concentration (AWS 32%, Azure 23%, Google 11% in 2024) and integration costs raise switching barriers; depositors pushed yields as fed funds sat at 5.25–5.50% in 2024; CA unemployment 4.4% and 4% y/y wage growth tightened labor supply.

| Supplier | 2024 metric |

|---|---|

| Cloud share | AWS 32% / Azure 23% / GCP 11% |

| Fed funds | 5.25–5.50% |

| CA unemployment | 4.4% |

| Wage growth | ~4% y/y |

What is included in the product

Tailored Porter's Five Forces analysis for Westamerica Bank that uncovers key drivers of competition, customer bargaining power, and market entry risks while identifying disruptive threats and substitutes; evaluates supplier/buyer influence on pricing and profitability and highlights dynamics that protect incumbents. Fully editable for reports and strategy decks.

Clear one-sheet Porter's Five Forces for Westamerica Bank—instantly visualize competitive pressures with a radar chart, customize force levels with your data, and drop a clean, no-macro sheet straight into pitch decks or executive reports.

Customers Bargaining Power

Rate-shopping retail depositors

Consumers can compare deposit rates instantly via apps and aggregators, boosting bargaining power. In 2024 money market and 1-year CD yields near 4–4.5% versus median savings APY ~0.4%, prompting rapid fund shifts. Westamerica must match pricing or add value to retain deposits. That squeezes net interest margins and raises acquisition costs.

SMB and commercial clients

SMB and commercial clients exert moderate bargaining power at Westamerica Bank: roughly 70% of SMBs multi-bank (2024 surveys), enabling negotiation on lending rates, covenants and fees. Treasury services create stickiness—client retention for payment/treasury products averages over 80% industry-wide in 2024—tempering price pressure. Deep relationships and high service quality reduce buyer leverage despite ongoing rate competition.

Affluent clients with alternatives

Affluent clients can move high balances into brokered sweep accounts or 3-month T-bills, which averaged about 5% in 2024, increasing pressure on Westamerica to match yield and service. Their mobility raises bargaining power and losing a few large accounts can materially affect funding and liquidity. Westamerica must segment these clients and tailor competitive yield, sweep options, and concierge service to retain them.

Digital expectations and low switching friction

Enhanced digital capabilities across competitors have reduced perceived switching costs; by 2024 about 80% of U.S. consumers used mobile banking, enabling rapid online migrations when features lag. Customers can move accounts with minimal effort, increasing buyer leverage over features and fees and pressuring margins. Continuous UX and feature investment is required to dampen this power and retain deposits.

- 2024 mobile banking adoption ~80%

- Low digital switching friction increases fee/feature pressure

- Ongoing UX spend needed to defend deposits

Credit customers’ negotiation leverage

Creditworthy borrowers can pit lenders against each other for better rates and structures, with Westamerica Bancorporation (WABC) reporting about $6.3B in assets in 2024, increasing competitive pressure on yields. Collateral-rich loans face aggressive bidding in stable markets, and covenant-light trends have risen, compressing risk-adjusted returns. Underwriting discipline must balance share retention and credit quality to avoid margin erosion.

- Debt shopping: higher borrower leverage on pricing

- Collateral bidding: tighter spreads in stable cycles

- Covenant-light: pressure on protections and returns

- Underwriting trade-off: growth versus credit discipline

Customers wield pricing power: mobile ~80%, MM/CD 4–4.5%, 3-mo T-bill ~5%

Customers hold elevated bargaining power: retail can chase 4–4.5% money‑market/1‑yr CD yields vs median savings APY ~0.4% (2024), mobile banking adoption ~80% lowers switching friction, and affluent balances can shift into 3‑month T‑bills ~5% (2024). SMBs (~70% multi‑bank) and $6.3B WABC asset base force competitive pricing and tailored service to retain deposits.

| Metric | 2024 Value |

|---|---|

| Mobile adoption | ~80% |

| Money‑market/1yr CD | 4–4.5% |

| Median savings APY | ~0.4% |

| 3‑month T‑bill | ~5% |

| SMB multi‑bank | ~70% |

| WABC assets | $6.3B |

Preview the Actual Deliverable

Westamerica Bank Porter's Five Forces Analysis

This preview is the exact Westamerica Bank Porter's Five Forces Analysis you'll receive—no samples or placeholders. It contains the full, professionally formatted assessment of competitive rivalry, supplier and buyer power, threats of entry and substitution, and strategic implications. Purchase grants immediate download of this identical file, ready for use.

Original: $10.00

-65%$10.00

$3.50Description

Go Beyond the Preview—Access the Full Strategic Report

Westamerica Bank operates in a niche regional banking market with stable customer relationships, moderate regulatory pressure, and competitive threats from larger banks and fintechs. Its loan portfolio strength counters some substitution risk but limits scale benefits. This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis to explore force-by-force ratings, visuals, and actionable strategy insights.

Suppliers Bargaining Power

Concentrated core tech vendors

Westamerica relies on a few core banking platforms, payments processors, and ATM networks, concentrating supplier power and giving vendors leverage over pricing and contract terms.

High switching costs, complex integrations, and regulatory validation make vendor changes rare, allowing vendors to dictate upgrade roadmaps and squeeze margins.

Vendor outages or implementation delays can directly harm customer experience and operational continuity, increasing reputational and compliance risk.

Funding providers and depositors

Depositors are Westamerica’s primary funding suppliers and became more rate-sensitive as the fed funds rate stayed at 5.25–5.50% through 2024, so greater yield demands push Westamerica’s cost of funds and compress NIM. Wholesale alternatives such as FHLB advances can replace deposits but generally carry higher, more volatile funding costs. Maintaining a stable core deposit mix reduces supplier bargaining power.

Skilled labor and compliance talent

Experienced bankers, credit underwriters, and compliance officers remain scarce in California, where the 2024 unemployment rate averaged about 4.4%, tightening labor supply for financial services.

Wage inflation in 2024 saw financial-sector pay rise roughly 4% year-over-year, increasing employees’ bargaining power and raising recruitment costs.

Higher retention and hiring expenses have pushed operating costs up for regional banks like Westamerica, while talent shortages can delay growth and risk-management initiatives.

Regulators as gatekeepers

Regulators act as gatekeepers: banking licenses, capital rules and supervisory expectations effectively supply permission to operate for Westamerica, and 2024 supervisory scrutiny after industry stress raised compliance and systems upgrade costs that compress margins.

Examination findings can limit growth or strategy, giving regulators indirect supplier power over branch expansion, lending limits and product offerings.

- Regulatory permission is a de facto input

- 2024-era compliance upgrades raise operating costs

- Examinations can constrain strategy and growth

Data, cybersecurity, and cloud providers

Specialized data feeds, fraud tools, and cloud infrastructure are essential for Westamerica Bank; top cloud vendors hold concentrated share (AWS ~32%, Azure ~23%, Google ~11% in 2024 per Synergy Research), narrowing alternatives and raising supplier pricing power. High security and uptime requirements increase switching costs, while vendor outages or poor performance directly raise regulatory, risk, and compliance impact.

- Limited vendors

- High switching cost

- Direct compliance risk

- Cloud market concentration

Suppliers exert moderate-high power; top-three cloud share 66%

Suppliers (core platforms, cloud, payments, talent, regulators, depositors) hold moderate-to-high power: cloud concentration (AWS 32%, Azure 23%, Google 11% in 2024) and integration costs raise switching barriers; depositors pushed yields as fed funds sat at 5.25–5.50% in 2024; CA unemployment 4.4% and 4% y/y wage growth tightened labor supply.

| Supplier | 2024 metric |

|---|---|

| Cloud share | AWS 32% / Azure 23% / GCP 11% |

| Fed funds | 5.25–5.50% |

| CA unemployment | 4.4% |

| Wage growth | ~4% y/y |

What is included in the product

Tailored Porter's Five Forces analysis for Westamerica Bank that uncovers key drivers of competition, customer bargaining power, and market entry risks while identifying disruptive threats and substitutes; evaluates supplier/buyer influence on pricing and profitability and highlights dynamics that protect incumbents. Fully editable for reports and strategy decks.

Clear one-sheet Porter's Five Forces for Westamerica Bank—instantly visualize competitive pressures with a radar chart, customize force levels with your data, and drop a clean, no-macro sheet straight into pitch decks or executive reports.

Customers Bargaining Power

Rate-shopping retail depositors

Consumers can compare deposit rates instantly via apps and aggregators, boosting bargaining power. In 2024 money market and 1-year CD yields near 4–4.5% versus median savings APY ~0.4%, prompting rapid fund shifts. Westamerica must match pricing or add value to retain deposits. That squeezes net interest margins and raises acquisition costs.

SMB and commercial clients

SMB and commercial clients exert moderate bargaining power at Westamerica Bank: roughly 70% of SMBs multi-bank (2024 surveys), enabling negotiation on lending rates, covenants and fees. Treasury services create stickiness—client retention for payment/treasury products averages over 80% industry-wide in 2024—tempering price pressure. Deep relationships and high service quality reduce buyer leverage despite ongoing rate competition.

Affluent clients with alternatives

Affluent clients can move high balances into brokered sweep accounts or 3-month T-bills, which averaged about 5% in 2024, increasing pressure on Westamerica to match yield and service. Their mobility raises bargaining power and losing a few large accounts can materially affect funding and liquidity. Westamerica must segment these clients and tailor competitive yield, sweep options, and concierge service to retain them.

Digital expectations and low switching friction

Enhanced digital capabilities across competitors have reduced perceived switching costs; by 2024 about 80% of U.S. consumers used mobile banking, enabling rapid online migrations when features lag. Customers can move accounts with minimal effort, increasing buyer leverage over features and fees and pressuring margins. Continuous UX and feature investment is required to dampen this power and retain deposits.

- 2024 mobile banking adoption ~80%

- Low digital switching friction increases fee/feature pressure

- Ongoing UX spend needed to defend deposits

Credit customers’ negotiation leverage

Creditworthy borrowers can pit lenders against each other for better rates and structures, with Westamerica Bancorporation (WABC) reporting about $6.3B in assets in 2024, increasing competitive pressure on yields. Collateral-rich loans face aggressive bidding in stable markets, and covenant-light trends have risen, compressing risk-adjusted returns. Underwriting discipline must balance share retention and credit quality to avoid margin erosion.

- Debt shopping: higher borrower leverage on pricing

- Collateral bidding: tighter spreads in stable cycles

- Covenant-light: pressure on protections and returns

- Underwriting trade-off: growth versus credit discipline

Customers wield pricing power: mobile ~80%, MM/CD 4–4.5%, 3-mo T-bill ~5%

Customers hold elevated bargaining power: retail can chase 4–4.5% money‑market/1‑yr CD yields vs median savings APY ~0.4% (2024), mobile banking adoption ~80% lowers switching friction, and affluent balances can shift into 3‑month T‑bills ~5% (2024). SMBs (~70% multi‑bank) and $6.3B WABC asset base force competitive pricing and tailored service to retain deposits.

| Metric | 2024 Value |

|---|---|

| Mobile adoption | ~80% |

| Money‑market/1yr CD | 4–4.5% |

| Median savings APY | ~0.4% |

| 3‑month T‑bill | ~5% |

| SMB multi‑bank | ~70% |

| WABC assets | $6.3B |

Preview the Actual Deliverable

Westamerica Bank Porter's Five Forces Analysis

This preview is the exact Westamerica Bank Porter's Five Forces Analysis you'll receive—no samples or placeholders. It contains the full, professionally formatted assessment of competitive rivalry, supplier and buyer power, threats of entry and substitution, and strategic implications. Purchase grants immediate download of this identical file, ready for use.