Western Midstream Partners Porter's Five Forces Analysis

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

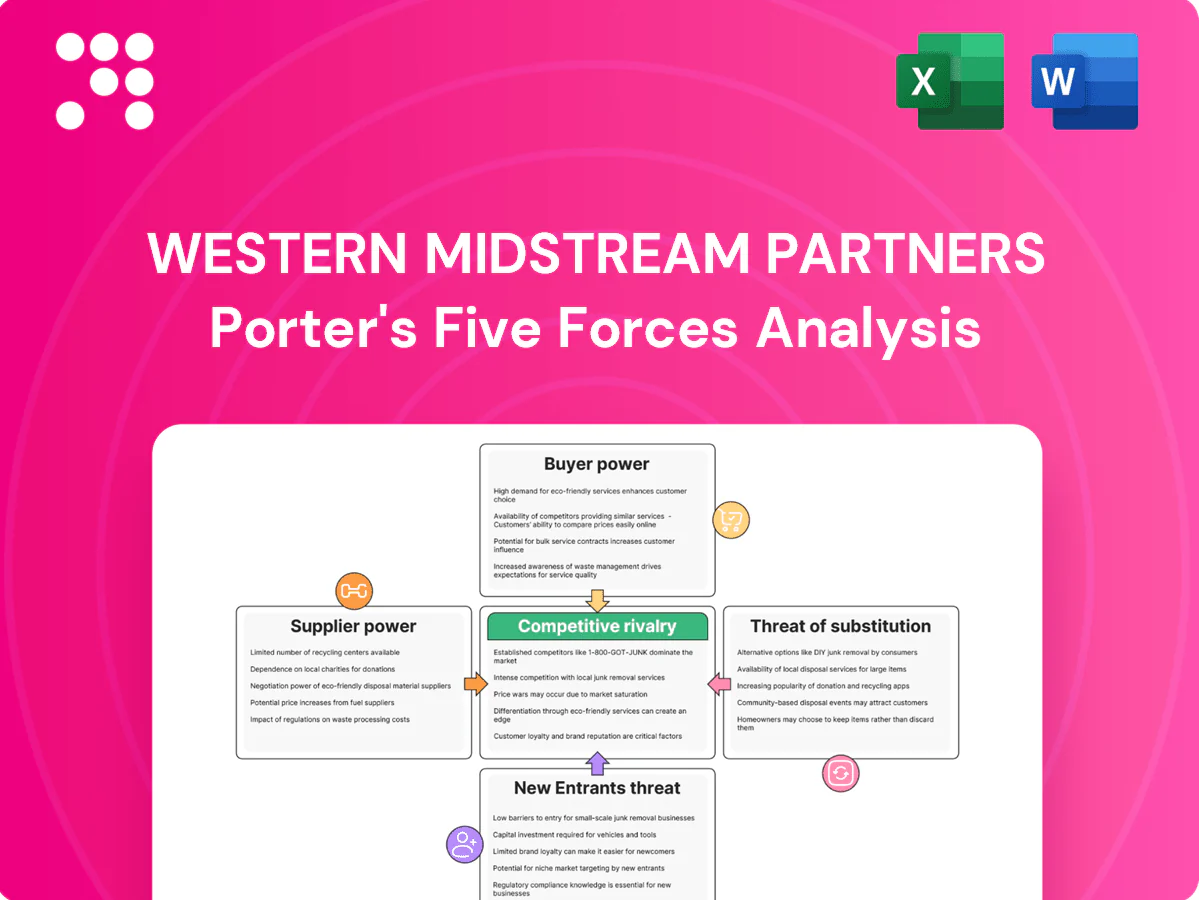

Western Midstream Partners faces moderate buyer power and high supplier leverage due to concentrated pipeline assets and contract structures. Entry barriers and capital intensity limit new entrants, yet commodity cycles and asset overlap keep rivalry intense. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Western Midstream Partners’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentrated upstream volume providers

Hydrocarbon volumes are the critical input and a handful of large E&P players in the Permian, Rockies and Appalachia can press on fees, specs and contract terms; the Permian produced about 5.5 million b/d in 2024 (EIA), boosting producer bargaining clout. Producer consolidation across these basins amplifies leverage, though long-term acreage dedications and minimum volume commitments (multi-year MVCs) curb immediate renegotiation risk. Basin-specific pipeline and processing alternatives remain limited, constraining near-term switching for Western Midstream.

Specialized equipment and services

Compressors, cryogenic units, SCADA and specialty maintenance vendors are relatively concentrated—OEMs like Siemens, GE and Honeywell dominate—giving suppliers pricing power as compressor lead times often reach 12–18 months and cryogenic skids can cost millions per unit. Multi-year service agreements (commonly 3–5 years) and equipment standardization reduce switching costs, while Western Midstream’s scale purchasing and 2024 capex discipline help offset vendor leverage.

Land, ROW, and power providers

Access to rights-of-way and grid power are chokepoints for Western Midstream, with permitting-driven delays averaging about 18 months in 2024, letting local utilities and landowners extract favorable terms or cause hold-ups. Early corridor control cuts holdout risk and transaction costs, while long-dated power and ROW agreements stabilize cashflow but lock in rates and reduce operational flexibility.

Environmental and compliance inputs

Emissions controls, treating chemicals and specialized environmental services are essential to meet evolving regulations; limited qualified providers can raise procurement costs and reduce flexibility. Regulatory shifts—notably tighter EPA methane and VOC enforcement in 2024—increase dependence on niche compliance suppliers. Long-term supplier contracts improve availability and price predictability.

- Emissions controls: higher capex/O&M pressure

- Limited providers: upward cost pressure

- 2024 EPA methane/VOC enforcement: heightens supplier reliance

- Long-term contracts: secure supply and price predictability

Labor and contractor availability

Skilled field labor and certified contractors are essential for Western Midstream’s safe operations and expansions; tight regional labor markets in 2024 pushed field technician wages up about 6% year‑over‑year and increased scheduling risk. Strong safety records and a steady project pipeline improve Western Midstream’s bargaining position with contractors, while automation and remote monitoring investments are reducing labor intensity over time.

- Labor cost rise ~6% (2024)

- Hiring difficulty: majority of energy firms cited workforce shortages in 2024

- Automation spend cuts recurring field hours over project lifecycle

Suppliers tighten terms: 12–18 month lead times, ~18 month permits, +6% wages

Suppliers exert moderate-to-high power: large E&P producers (Permian ~5.5m b/d in 2024) and concentrated OEMs (compressor lead times 12–18 months) pressure fees and terms, while long-term MVCs, scale purchasing and multi-year service contracts mitigate risk; permitting delays (~18 months in 2024) and rising field wages (+6% y/y) raise supplier leverage.

| Metric | 2024 |

|---|---|

| Permian production | ~5.5m b/d |

| Compressor lead time | 12–18 months |

| Permitting delay | ~18 months |

| Field wages | +6% y/y |

What is included in the product

Tailored Porter's Five Forces analysis of Western Midstream Partners uncovering competitive drivers, buyer and supplier power, entry barriers, substitutes and emerging threats to its midstream energy position.

A concise Porter's Five Forces one-sheet for Western Midstream Partners that highlights supplier/customer bargaining, threat of entrants, substitutes, and competitive rivalry—adjustable pressure sliders and a radar chart simplify scenario analysis for fast, board-ready decisions.

Customers Bargaining Power

Large anchor producers

Major producers in WES’s DJ, Permian and Eagle Ford basins command meaningful bargaining power due to concentrated volumes and can negotiate tariff structures, service bundling and optionality. Acreage dedications and minimum volume commitments provide throughput visibility and partly offset this leverage. Deep operational integration and longstanding commercial relationships further reduce churn and lock in flow economics as of 2024.

Limited basin alternatives

In 2024 intra-basin gathering/processing alternatives for Western Midstream customers are often limited to one or two providers, curbing buyer leverage. Where parallel systems exist, producers use competitive quotes to pressure fees, but interconnectivity and downstream takeaway access—notably access to Gulf Coast and midstream hubs—remain decisive differentiators. Switching requires substantial capex and 12–24 months lead time, moderating immediate price concessions.

Contractual protections

Take-or-pay and deficiency payments create predictable cash flows and materially dampen volume and price volatility for Western Midstream, while fee escalators indexed to CPI (US CPI ~3.4% in 2024) help limit long-term margin erosion; however contract renewal windows can reintroduce buyer leverage, and service-quality SLAs support customer retention by preserving volumes despite disciplined pricing.

Commodity price pass-through

Predominantly fee-based structures at Western Midstream limit customers' ability to push commodity price risk upstream, reducing WES's exposure. Where keep-whole or percent-of-proceeds contracts exist, shippers can press for favorable revenue sharing. A portfolio tilt toward fixed-fee agreements improves WES's stance, but market downturns still heighten customer pushback at renewal.

- Fee-based contracts reduce pass-through

- Keep-whole/POP enable customer pressure

- Fixed-fee mix strengthens negotiating power

- Downturns increase renewal leverage

Downstream access and quality specs

Buyers prize Western Midstream’s downstream access to NGL takeaway, residue gas markets and crude hubs, which in 2024 helped preserve superior netbacks and limited renegotiation pressure. Consistent tight-spec adherence and low downtime raise switching costs for shippers, while transient bottlenecks in other corridors can briefly restore buyer leverage.

- Downstream connectivity: supports stronger netbacks

- Spec adherence: increases switching costs

- Low downtime: reduces renegotiation risk

- Bottlenecks elsewhere: can temporarily boost buyer leverage

WES producers hold leverage; switching 12–24 months, CPI 3.4%

Large producers in WES basins retain notable leverage via concentrated volumes and optionality, though acreage dedications and 12–24 month switching lead times limit immediate pressure. Fee-based and take-or-pay contracts (with CPI ~3.4% in 2024) stabilize cash flows and reduce pass-through risk, while keep-whole/POP arrangements amplify customer bargaining at renewals.

| Metric | 2024 |

|---|---|

| Switching lead time | 12–24 months |

| US CPI | 3.4% |

Full Version Awaits

Western Midstream Partners Porter's Five Forces Analysis

This preview shows the complete Porter's Five Forces analysis for Western Midstream Partners, covering supplier power, buyer power, competitive rivalry, threat of substitutes, and barriers to entry. The document displayed here is the exact file you'll receive after purchase—fully formatted and ready to use. No samples or placeholders; buy and download instantly.

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Western Midstream Partners faces moderate buyer power and high supplier leverage due to concentrated pipeline assets and contract structures. Entry barriers and capital intensity limit new entrants, yet commodity cycles and asset overlap keep rivalry intense. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Western Midstream Partners’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentrated upstream volume providers

Hydrocarbon volumes are the critical input and a handful of large E&P players in the Permian, Rockies and Appalachia can press on fees, specs and contract terms; the Permian produced about 5.5 million b/d in 2024 (EIA), boosting producer bargaining clout. Producer consolidation across these basins amplifies leverage, though long-term acreage dedications and minimum volume commitments (multi-year MVCs) curb immediate renegotiation risk. Basin-specific pipeline and processing alternatives remain limited, constraining near-term switching for Western Midstream.

Specialized equipment and services

Compressors, cryogenic units, SCADA and specialty maintenance vendors are relatively concentrated—OEMs like Siemens, GE and Honeywell dominate—giving suppliers pricing power as compressor lead times often reach 12–18 months and cryogenic skids can cost millions per unit. Multi-year service agreements (commonly 3–5 years) and equipment standardization reduce switching costs, while Western Midstream’s scale purchasing and 2024 capex discipline help offset vendor leverage.

Land, ROW, and power providers

Access to rights-of-way and grid power are chokepoints for Western Midstream, with permitting-driven delays averaging about 18 months in 2024, letting local utilities and landowners extract favorable terms or cause hold-ups. Early corridor control cuts holdout risk and transaction costs, while long-dated power and ROW agreements stabilize cashflow but lock in rates and reduce operational flexibility.

Environmental and compliance inputs

Emissions controls, treating chemicals and specialized environmental services are essential to meet evolving regulations; limited qualified providers can raise procurement costs and reduce flexibility. Regulatory shifts—notably tighter EPA methane and VOC enforcement in 2024—increase dependence on niche compliance suppliers. Long-term supplier contracts improve availability and price predictability.

- Emissions controls: higher capex/O&M pressure

- Limited providers: upward cost pressure

- 2024 EPA methane/VOC enforcement: heightens supplier reliance

- Long-term contracts: secure supply and price predictability

Labor and contractor availability

Skilled field labor and certified contractors are essential for Western Midstream’s safe operations and expansions; tight regional labor markets in 2024 pushed field technician wages up about 6% year‑over‑year and increased scheduling risk. Strong safety records and a steady project pipeline improve Western Midstream’s bargaining position with contractors, while automation and remote monitoring investments are reducing labor intensity over time.

- Labor cost rise ~6% (2024)

- Hiring difficulty: majority of energy firms cited workforce shortages in 2024

- Automation spend cuts recurring field hours over project lifecycle

Suppliers tighten terms: 12–18 month lead times, ~18 month permits, +6% wages

Suppliers exert moderate-to-high power: large E&P producers (Permian ~5.5m b/d in 2024) and concentrated OEMs (compressor lead times 12–18 months) pressure fees and terms, while long-term MVCs, scale purchasing and multi-year service contracts mitigate risk; permitting delays (~18 months in 2024) and rising field wages (+6% y/y) raise supplier leverage.

| Metric | 2024 |

|---|---|

| Permian production | ~5.5m b/d |

| Compressor lead time | 12–18 months |

| Permitting delay | ~18 months |

| Field wages | +6% y/y |

What is included in the product

Tailored Porter's Five Forces analysis of Western Midstream Partners uncovering competitive drivers, buyer and supplier power, entry barriers, substitutes and emerging threats to its midstream energy position.

A concise Porter's Five Forces one-sheet for Western Midstream Partners that highlights supplier/customer bargaining, threat of entrants, substitutes, and competitive rivalry—adjustable pressure sliders and a radar chart simplify scenario analysis for fast, board-ready decisions.

Customers Bargaining Power

Large anchor producers

Major producers in WES’s DJ, Permian and Eagle Ford basins command meaningful bargaining power due to concentrated volumes and can negotiate tariff structures, service bundling and optionality. Acreage dedications and minimum volume commitments provide throughput visibility and partly offset this leverage. Deep operational integration and longstanding commercial relationships further reduce churn and lock in flow economics as of 2024.

Limited basin alternatives

In 2024 intra-basin gathering/processing alternatives for Western Midstream customers are often limited to one or two providers, curbing buyer leverage. Where parallel systems exist, producers use competitive quotes to pressure fees, but interconnectivity and downstream takeaway access—notably access to Gulf Coast and midstream hubs—remain decisive differentiators. Switching requires substantial capex and 12–24 months lead time, moderating immediate price concessions.

Contractual protections

Take-or-pay and deficiency payments create predictable cash flows and materially dampen volume and price volatility for Western Midstream, while fee escalators indexed to CPI (US CPI ~3.4% in 2024) help limit long-term margin erosion; however contract renewal windows can reintroduce buyer leverage, and service-quality SLAs support customer retention by preserving volumes despite disciplined pricing.

Commodity price pass-through

Predominantly fee-based structures at Western Midstream limit customers' ability to push commodity price risk upstream, reducing WES's exposure. Where keep-whole or percent-of-proceeds contracts exist, shippers can press for favorable revenue sharing. A portfolio tilt toward fixed-fee agreements improves WES's stance, but market downturns still heighten customer pushback at renewal.

- Fee-based contracts reduce pass-through

- Keep-whole/POP enable customer pressure

- Fixed-fee mix strengthens negotiating power

- Downturns increase renewal leverage

Downstream access and quality specs

Buyers prize Western Midstream’s downstream access to NGL takeaway, residue gas markets and crude hubs, which in 2024 helped preserve superior netbacks and limited renegotiation pressure. Consistent tight-spec adherence and low downtime raise switching costs for shippers, while transient bottlenecks in other corridors can briefly restore buyer leverage.

- Downstream connectivity: supports stronger netbacks

- Spec adherence: increases switching costs

- Low downtime: reduces renegotiation risk

- Bottlenecks elsewhere: can temporarily boost buyer leverage

WES producers hold leverage; switching 12–24 months, CPI 3.4%

Large producers in WES basins retain notable leverage via concentrated volumes and optionality, though acreage dedications and 12–24 month switching lead times limit immediate pressure. Fee-based and take-or-pay contracts (with CPI ~3.4% in 2024) stabilize cash flows and reduce pass-through risk, while keep-whole/POP arrangements amplify customer bargaining at renewals.

| Metric | 2024 |

|---|---|

| Switching lead time | 12–24 months |

| US CPI | 3.4% |

Full Version Awaits

Western Midstream Partners Porter's Five Forces Analysis

This preview shows the complete Porter's Five Forces analysis for Western Midstream Partners, covering supplier power, buyer power, competitive rivalry, threat of substitutes, and barriers to entry. The document displayed here is the exact file you'll receive after purchase—fully formatted and ready to use. No samples or placeholders; buy and download instantly.

Original: $10.00

-65%$10.00

$3.50Description

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Western Midstream Partners faces moderate buyer power and high supplier leverage due to concentrated pipeline assets and contract structures. Entry barriers and capital intensity limit new entrants, yet commodity cycles and asset overlap keep rivalry intense. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Western Midstream Partners’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentrated upstream volume providers

Hydrocarbon volumes are the critical input and a handful of large E&P players in the Permian, Rockies and Appalachia can press on fees, specs and contract terms; the Permian produced about 5.5 million b/d in 2024 (EIA), boosting producer bargaining clout. Producer consolidation across these basins amplifies leverage, though long-term acreage dedications and minimum volume commitments (multi-year MVCs) curb immediate renegotiation risk. Basin-specific pipeline and processing alternatives remain limited, constraining near-term switching for Western Midstream.

Specialized equipment and services

Compressors, cryogenic units, SCADA and specialty maintenance vendors are relatively concentrated—OEMs like Siemens, GE and Honeywell dominate—giving suppliers pricing power as compressor lead times often reach 12–18 months and cryogenic skids can cost millions per unit. Multi-year service agreements (commonly 3–5 years) and equipment standardization reduce switching costs, while Western Midstream’s scale purchasing and 2024 capex discipline help offset vendor leverage.

Land, ROW, and power providers

Access to rights-of-way and grid power are chokepoints for Western Midstream, with permitting-driven delays averaging about 18 months in 2024, letting local utilities and landowners extract favorable terms or cause hold-ups. Early corridor control cuts holdout risk and transaction costs, while long-dated power and ROW agreements stabilize cashflow but lock in rates and reduce operational flexibility.

Environmental and compliance inputs

Emissions controls, treating chemicals and specialized environmental services are essential to meet evolving regulations; limited qualified providers can raise procurement costs and reduce flexibility. Regulatory shifts—notably tighter EPA methane and VOC enforcement in 2024—increase dependence on niche compliance suppliers. Long-term supplier contracts improve availability and price predictability.

- Emissions controls: higher capex/O&M pressure

- Limited providers: upward cost pressure

- 2024 EPA methane/VOC enforcement: heightens supplier reliance

- Long-term contracts: secure supply and price predictability

Labor and contractor availability

Skilled field labor and certified contractors are essential for Western Midstream’s safe operations and expansions; tight regional labor markets in 2024 pushed field technician wages up about 6% year‑over‑year and increased scheduling risk. Strong safety records and a steady project pipeline improve Western Midstream’s bargaining position with contractors, while automation and remote monitoring investments are reducing labor intensity over time.

- Labor cost rise ~6% (2024)

- Hiring difficulty: majority of energy firms cited workforce shortages in 2024

- Automation spend cuts recurring field hours over project lifecycle

Suppliers tighten terms: 12–18 month lead times, ~18 month permits, +6% wages

Suppliers exert moderate-to-high power: large E&P producers (Permian ~5.5m b/d in 2024) and concentrated OEMs (compressor lead times 12–18 months) pressure fees and terms, while long-term MVCs, scale purchasing and multi-year service contracts mitigate risk; permitting delays (~18 months in 2024) and rising field wages (+6% y/y) raise supplier leverage.

| Metric | 2024 |

|---|---|

| Permian production | ~5.5m b/d |

| Compressor lead time | 12–18 months |

| Permitting delay | ~18 months |

| Field wages | +6% y/y |

What is included in the product

Tailored Porter's Five Forces analysis of Western Midstream Partners uncovering competitive drivers, buyer and supplier power, entry barriers, substitutes and emerging threats to its midstream energy position.

A concise Porter's Five Forces one-sheet for Western Midstream Partners that highlights supplier/customer bargaining, threat of entrants, substitutes, and competitive rivalry—adjustable pressure sliders and a radar chart simplify scenario analysis for fast, board-ready decisions.

Customers Bargaining Power

Large anchor producers

Major producers in WES’s DJ, Permian and Eagle Ford basins command meaningful bargaining power due to concentrated volumes and can negotiate tariff structures, service bundling and optionality. Acreage dedications and minimum volume commitments provide throughput visibility and partly offset this leverage. Deep operational integration and longstanding commercial relationships further reduce churn and lock in flow economics as of 2024.

Limited basin alternatives

In 2024 intra-basin gathering/processing alternatives for Western Midstream customers are often limited to one or two providers, curbing buyer leverage. Where parallel systems exist, producers use competitive quotes to pressure fees, but interconnectivity and downstream takeaway access—notably access to Gulf Coast and midstream hubs—remain decisive differentiators. Switching requires substantial capex and 12–24 months lead time, moderating immediate price concessions.

Contractual protections

Take-or-pay and deficiency payments create predictable cash flows and materially dampen volume and price volatility for Western Midstream, while fee escalators indexed to CPI (US CPI ~3.4% in 2024) help limit long-term margin erosion; however contract renewal windows can reintroduce buyer leverage, and service-quality SLAs support customer retention by preserving volumes despite disciplined pricing.

Commodity price pass-through

Predominantly fee-based structures at Western Midstream limit customers' ability to push commodity price risk upstream, reducing WES's exposure. Where keep-whole or percent-of-proceeds contracts exist, shippers can press for favorable revenue sharing. A portfolio tilt toward fixed-fee agreements improves WES's stance, but market downturns still heighten customer pushback at renewal.

- Fee-based contracts reduce pass-through

- Keep-whole/POP enable customer pressure

- Fixed-fee mix strengthens negotiating power

- Downturns increase renewal leverage

Downstream access and quality specs

Buyers prize Western Midstream’s downstream access to NGL takeaway, residue gas markets and crude hubs, which in 2024 helped preserve superior netbacks and limited renegotiation pressure. Consistent tight-spec adherence and low downtime raise switching costs for shippers, while transient bottlenecks in other corridors can briefly restore buyer leverage.

- Downstream connectivity: supports stronger netbacks

- Spec adherence: increases switching costs

- Low downtime: reduces renegotiation risk

- Bottlenecks elsewhere: can temporarily boost buyer leverage

WES producers hold leverage; switching 12–24 months, CPI 3.4%

Large producers in WES basins retain notable leverage via concentrated volumes and optionality, though acreage dedications and 12–24 month switching lead times limit immediate pressure. Fee-based and take-or-pay contracts (with CPI ~3.4% in 2024) stabilize cash flows and reduce pass-through risk, while keep-whole/POP arrangements amplify customer bargaining at renewals.

| Metric | 2024 |

|---|---|

| Switching lead time | 12–24 months |

| US CPI | 3.4% |

Full Version Awaits

Western Midstream Partners Porter's Five Forces Analysis

This preview shows the complete Porter's Five Forces analysis for Western Midstream Partners, covering supplier power, buyer power, competitive rivalry, threat of substitutes, and barriers to entry. The document displayed here is the exact file you'll receive after purchase—fully formatted and ready to use. No samples or placeholders; buy and download instantly.