West Fraser Porter's Five Forces Analysis

From Overview to Strategy Blueprint

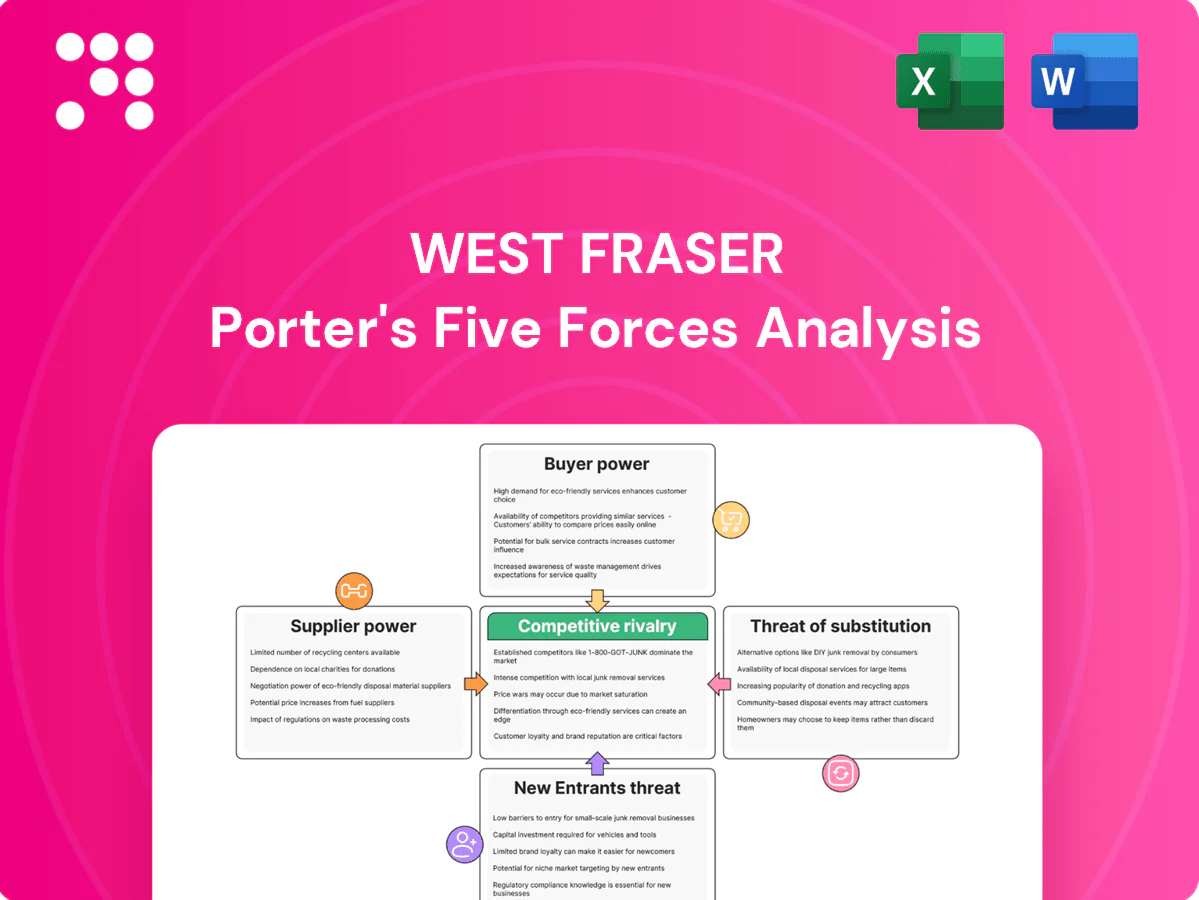

West Fraser faces intense cyclical demand, concentrated supplier influence for key inputs, moderate buyer power, and growing substitute pressures from engineered wood and recycling trends; barriers to entry remain high but climate regulations add risk. This snapshot highlights key forces—unlock the full Porter's Five Forces Analysis for force-by-force ratings, visuals, and actionable strategy to inform investment decisions.

Suppliers Bargaining Power

Concentrated timberland and stumpage sources

Wood fiber, the critical input for West Fraser, is sourced from Crown timber tenures in Western Canada and private timberland in the U.S. South, where access is governed by quotas, auctions and long-term licenses that concentrate supplier power. In 2024 wildfires, drought and beetle outbreaks continued to tighten availability and raise supplier leverage. Securing multi-year fiber agreements and investing in silviculture reduce this risk by stabilizing supply.

Log price volatility and fiber mix constraints

Log prices swing with housing demand and harvest conditions—US housing starts averaged about 1.4 million units in 2024, driving mill margin volatility. Mills are optimized for specific diameters and species, limiting rapid fiber switching and raising supplier leverage. When markets heat up suppliers can extract premiums for tight grade/spec lots; diversifying into residual chips and recycled fiber has reduced exposure but not eliminated price sensitivity.

Equipment, chemicals, and resin vendor leverage

Engineered wood and pulp operations depend on specialized resins, pulping chemicals, and OEM parts from a small supplier base, creating concentrated vendor leverage; West Fraser cited supplier tightness in its 2024 filings. Switching qualified suppliers requires certification and downtime, often running weeks to months and raising costs. In 2023–24 supply shocks, vendors passed through cost increases materially (vendor price uplifts in the sector averaged double digits). West Fraser mitigates risk via strategic sourcing and dual-qualification programs to reduce single-supplier exposure.

Energy and fuel cost pass-through

Mills are energy intensive and exposed to electricity, natural gas and diesel price swings; in 2024 Henry Hub averaged about 2.8 USD/MMBtu and US diesel averaged near 3.7 USD/gal, increasing supplier leverage where alternatives are limited. Cogeneration and biomass use reduce but do not eliminate exposure. Long-term energy contracts and onsite generation materially stabilize costs and negotiating power.

- High exposure: energy a material input

- Mitigation: cogeneration/biomass lowers spot risk

- Stability: long-term contracts shift bargaining power

Transportation and rail capacity bottlenecks

Transportation and rail capacity bottlenecks raise supplier power for West Fraser because logs, lumber and pulp depend on finite rail and trucking corridors; car shortages, labor disputes and terminal congestion increased freight rates by approximately 12% year-over-year in 2024, giving carriers pricing leverage. Remote mill locations intensify dependence on a few carriers, while multimodal options and origin diversification provide partial buffers.

- Finite corridors: concentrated carrier control

- 2024 freight rates: ≈12% YoY increase

- Remote mills: higher switching costs

- Mitigants: multimodal transport, sourcing diversification

Wood fiber scarcity, rising fuel and freight squeeze building-materials margins

Wood fiber scarcity from wildfire, beetles and quotaed tenures tightened supplier leverage in 2024; housing starts ~1.4M raised log price volatility. Chemical/OEM suppliers remained concentrated with double-digit vendor uplifts in 2023–24. Energy (Henry Hub ~2.8 USD/MMBtu; diesel ~3.7 USD/gal) and freight (+≈12% YoY) further elevate supplier power; cogeneration, long-term contracts and sourcing reduce but do not eliminate risk.

| Supplier | 2024 metric | Impact |

|---|---|---|

| Fiber | Housing starts 1.4M | Price volatility |

| Energy | HH 2.8 USD/MMBtu | Cost exposure |

| Freight | +12% YoY | Logistics bottleneck |

What is included in the product

Tailored Porter’s Five Forces analysis for West Fraser that uncovers competitive drivers, supplier and buyer power, threat of substitutes and entrants, and emerging disruptions, with strategic commentary to assess pricing leverage and long‑term profitability.

A concise one-sheet Porter's Five Forces for West Fraser that maps supplier, buyer, rivalry, substitutes, and entry pressures—ideal for quick strategic decisions. Customize scores and radar visuals to model scenarios like timber price shocks, mill capacity changes, or regulatory shifts.

Customers Bargaining Power

Large retailers and builders concentrate demand

Big-box retailers (Home Depot, Lowe's) accounted for roughly 70% of US home‑improvement retail sales in 2024, while truss/OSB distributors and large builders (top builders deliver hundreds of thousands of homes annually) concentrate volume, enabling aggressive price negotiation, vendor scorecards and service demands. Losing a key account can dent mill utilization and margins; multi‑year supply agreements with service differentiation (dedicated trucks, JIT scheduling) help temper that leverage.

High price sensitivity in commodity lumber

Lumber and OSB trade off transparent Random Lengths indices, letting buyers time purchases and extract index-linked discounts; in 2024 softwood lumber averaged roughly 30% below 2021 peaks, amplifying buyer leverage in weak markets. Commoditization boosts price sensitivity and bargaining power, while West Fraser can protect margins via value-added grades and reliable logistics that sustain small premiums.

Low switching costs across mills

Buyers can readily switch among mills and producers when grades meet spec, so bargaining power stays high across most regions; freight differentials, which often represent roughly 5–15% of delivered price, are usually the main switching hurdle. Proximity and reliable on-time performance create soft frictions that modestly reduce buyer leverage in local markets.

Certification and sustainability requirements

Customers increasingly mandate FSC/PEFC/SFI certification and chain-of-custody; FSC+PEFC cover about 500 million hectares globally in 2024. Compliance raises supplier costs but is table stakes, letting buyers shift volumes rapidly to certified suppliers. West Fraser’s strong sustainable-forestry footprint helps defend share and pricing.

- Certification required by many large buyers

- FSC+PEFC ≈500M ha (2024)

- Raises supplier costs; increases buyer switching power

- West Fraser's certified holdings defend volumes/pricing

Export and pulp customers’ cyclical purchasing

Export and pulp customers shift volumes quickly in response to currency swings and end-market cycles, increasing spot purchases when prices fall and reducing long-term commitments; this cyclicality raised buyer leverage for West Fraser during recent downturns. A balanced contract versus spot mix — historically used to stabilize cash flow — helps smooth volume and price exposure across cycles.

- Spot buying rises in downturns

- Currency/end-market sensitivity

- Buyer leverage increases when prices drop

- Contract/spot balance mitigates volatility

Retail concentration, certification and price pressure reshape lumber margins and share

Large retailers/distributors concentrate volumes (big-box ≈70% US DIY sales 2024), giving customers price and service leverage; losing key accounts hurts utilization and margins. Commoditization and Random Lengths transparency (softwood lumber ≈30% below 2021 peaks in 2024) boost switching; certification (FSC+PEFC ≈500M ha 2024) is table stakes, raising costs but West Fraser's certified supply defends share.

| Metric | 2024 | Implication |

|---|---|---|

| Big-box US DIY share | ≈70% | High buyer concentration |

| Softwood lumber vs 2021 | ≈−30% | Increases buyer leverage |

| Certification area | FSC+PEFC ≈500M ha | Table stakes; raises supplier costs |

| Freight as % of price | ≈5–15% | Switching friction |

Same Document Delivered

West Fraser Porter's Five Forces Analysis

This preview shows the exact Porter's Five Forces analysis of West Fraser you'll receive—no surprises, no placeholders. The document provides a full assessment of competitive rivalry, supplier and buyer power, threat of substitutes, and barriers to entry. It's fully formatted and ready for immediate download after purchase.

From Overview to Strategy Blueprint

West Fraser faces intense cyclical demand, concentrated supplier influence for key inputs, moderate buyer power, and growing substitute pressures from engineered wood and recycling trends; barriers to entry remain high but climate regulations add risk. This snapshot highlights key forces—unlock the full Porter's Five Forces Analysis for force-by-force ratings, visuals, and actionable strategy to inform investment decisions.

Suppliers Bargaining Power

Concentrated timberland and stumpage sources

Wood fiber, the critical input for West Fraser, is sourced from Crown timber tenures in Western Canada and private timberland in the U.S. South, where access is governed by quotas, auctions and long-term licenses that concentrate supplier power. In 2024 wildfires, drought and beetle outbreaks continued to tighten availability and raise supplier leverage. Securing multi-year fiber agreements and investing in silviculture reduce this risk by stabilizing supply.

Log price volatility and fiber mix constraints

Log prices swing with housing demand and harvest conditions—US housing starts averaged about 1.4 million units in 2024, driving mill margin volatility. Mills are optimized for specific diameters and species, limiting rapid fiber switching and raising supplier leverage. When markets heat up suppliers can extract premiums for tight grade/spec lots; diversifying into residual chips and recycled fiber has reduced exposure but not eliminated price sensitivity.

Equipment, chemicals, and resin vendor leverage

Engineered wood and pulp operations depend on specialized resins, pulping chemicals, and OEM parts from a small supplier base, creating concentrated vendor leverage; West Fraser cited supplier tightness in its 2024 filings. Switching qualified suppliers requires certification and downtime, often running weeks to months and raising costs. In 2023–24 supply shocks, vendors passed through cost increases materially (vendor price uplifts in the sector averaged double digits). West Fraser mitigates risk via strategic sourcing and dual-qualification programs to reduce single-supplier exposure.

Energy and fuel cost pass-through

Mills are energy intensive and exposed to electricity, natural gas and diesel price swings; in 2024 Henry Hub averaged about 2.8 USD/MMBtu and US diesel averaged near 3.7 USD/gal, increasing supplier leverage where alternatives are limited. Cogeneration and biomass use reduce but do not eliminate exposure. Long-term energy contracts and onsite generation materially stabilize costs and negotiating power.

- High exposure: energy a material input

- Mitigation: cogeneration/biomass lowers spot risk

- Stability: long-term contracts shift bargaining power

Transportation and rail capacity bottlenecks

Transportation and rail capacity bottlenecks raise supplier power for West Fraser because logs, lumber and pulp depend on finite rail and trucking corridors; car shortages, labor disputes and terminal congestion increased freight rates by approximately 12% year-over-year in 2024, giving carriers pricing leverage. Remote mill locations intensify dependence on a few carriers, while multimodal options and origin diversification provide partial buffers.

- Finite corridors: concentrated carrier control

- 2024 freight rates: ≈12% YoY increase

- Remote mills: higher switching costs

- Mitigants: multimodal transport, sourcing diversification

Wood fiber scarcity, rising fuel and freight squeeze building-materials margins

Wood fiber scarcity from wildfire, beetles and quotaed tenures tightened supplier leverage in 2024; housing starts ~1.4M raised log price volatility. Chemical/OEM suppliers remained concentrated with double-digit vendor uplifts in 2023–24. Energy (Henry Hub ~2.8 USD/MMBtu; diesel ~3.7 USD/gal) and freight (+≈12% YoY) further elevate supplier power; cogeneration, long-term contracts and sourcing reduce but do not eliminate risk.

| Supplier | 2024 metric | Impact |

|---|---|---|

| Fiber | Housing starts 1.4M | Price volatility |

| Energy | HH 2.8 USD/MMBtu | Cost exposure |

| Freight | +12% YoY | Logistics bottleneck |

What is included in the product

Tailored Porter’s Five Forces analysis for West Fraser that uncovers competitive drivers, supplier and buyer power, threat of substitutes and entrants, and emerging disruptions, with strategic commentary to assess pricing leverage and long‑term profitability.

A concise one-sheet Porter's Five Forces for West Fraser that maps supplier, buyer, rivalry, substitutes, and entry pressures—ideal for quick strategic decisions. Customize scores and radar visuals to model scenarios like timber price shocks, mill capacity changes, or regulatory shifts.

Customers Bargaining Power

Large retailers and builders concentrate demand

Big-box retailers (Home Depot, Lowe's) accounted for roughly 70% of US home‑improvement retail sales in 2024, while truss/OSB distributors and large builders (top builders deliver hundreds of thousands of homes annually) concentrate volume, enabling aggressive price negotiation, vendor scorecards and service demands. Losing a key account can dent mill utilization and margins; multi‑year supply agreements with service differentiation (dedicated trucks, JIT scheduling) help temper that leverage.

High price sensitivity in commodity lumber

Lumber and OSB trade off transparent Random Lengths indices, letting buyers time purchases and extract index-linked discounts; in 2024 softwood lumber averaged roughly 30% below 2021 peaks, amplifying buyer leverage in weak markets. Commoditization boosts price sensitivity and bargaining power, while West Fraser can protect margins via value-added grades and reliable logistics that sustain small premiums.

Low switching costs across mills

Buyers can readily switch among mills and producers when grades meet spec, so bargaining power stays high across most regions; freight differentials, which often represent roughly 5–15% of delivered price, are usually the main switching hurdle. Proximity and reliable on-time performance create soft frictions that modestly reduce buyer leverage in local markets.

Certification and sustainability requirements

Customers increasingly mandate FSC/PEFC/SFI certification and chain-of-custody; FSC+PEFC cover about 500 million hectares globally in 2024. Compliance raises supplier costs but is table stakes, letting buyers shift volumes rapidly to certified suppliers. West Fraser’s strong sustainable-forestry footprint helps defend share and pricing.

- Certification required by many large buyers

- FSC+PEFC ≈500M ha (2024)

- Raises supplier costs; increases buyer switching power

- West Fraser's certified holdings defend volumes/pricing

Export and pulp customers’ cyclical purchasing

Export and pulp customers shift volumes quickly in response to currency swings and end-market cycles, increasing spot purchases when prices fall and reducing long-term commitments; this cyclicality raised buyer leverage for West Fraser during recent downturns. A balanced contract versus spot mix — historically used to stabilize cash flow — helps smooth volume and price exposure across cycles.

- Spot buying rises in downturns

- Currency/end-market sensitivity

- Buyer leverage increases when prices drop

- Contract/spot balance mitigates volatility

Retail concentration, certification and price pressure reshape lumber margins and share

Large retailers/distributors concentrate volumes (big-box ≈70% US DIY sales 2024), giving customers price and service leverage; losing key accounts hurts utilization and margins. Commoditization and Random Lengths transparency (softwood lumber ≈30% below 2021 peaks in 2024) boost switching; certification (FSC+PEFC ≈500M ha 2024) is table stakes, raising costs but West Fraser's certified supply defends share.

| Metric | 2024 | Implication |

|---|---|---|

| Big-box US DIY share | ≈70% | High buyer concentration |

| Softwood lumber vs 2021 | ≈−30% | Increases buyer leverage |

| Certification area | FSC+PEFC ≈500M ha | Table stakes; raises supplier costs |

| Freight as % of price | ≈5–15% | Switching friction |

Same Document Delivered

West Fraser Porter's Five Forces Analysis

This preview shows the exact Porter's Five Forces analysis of West Fraser you'll receive—no surprises, no placeholders. The document provides a full assessment of competitive rivalry, supplier and buyer power, threat of substitutes, and barriers to entry. It's fully formatted and ready for immediate download after purchase.

Description

From Overview to Strategy Blueprint

West Fraser faces intense cyclical demand, concentrated supplier influence for key inputs, moderate buyer power, and growing substitute pressures from engineered wood and recycling trends; barriers to entry remain high but climate regulations add risk. This snapshot highlights key forces—unlock the full Porter's Five Forces Analysis for force-by-force ratings, visuals, and actionable strategy to inform investment decisions.

Suppliers Bargaining Power

Concentrated timberland and stumpage sources

Wood fiber, the critical input for West Fraser, is sourced from Crown timber tenures in Western Canada and private timberland in the U.S. South, where access is governed by quotas, auctions and long-term licenses that concentrate supplier power. In 2024 wildfires, drought and beetle outbreaks continued to tighten availability and raise supplier leverage. Securing multi-year fiber agreements and investing in silviculture reduce this risk by stabilizing supply.

Log price volatility and fiber mix constraints

Log prices swing with housing demand and harvest conditions—US housing starts averaged about 1.4 million units in 2024, driving mill margin volatility. Mills are optimized for specific diameters and species, limiting rapid fiber switching and raising supplier leverage. When markets heat up suppliers can extract premiums for tight grade/spec lots; diversifying into residual chips and recycled fiber has reduced exposure but not eliminated price sensitivity.

Equipment, chemicals, and resin vendor leverage

Engineered wood and pulp operations depend on specialized resins, pulping chemicals, and OEM parts from a small supplier base, creating concentrated vendor leverage; West Fraser cited supplier tightness in its 2024 filings. Switching qualified suppliers requires certification and downtime, often running weeks to months and raising costs. In 2023–24 supply shocks, vendors passed through cost increases materially (vendor price uplifts in the sector averaged double digits). West Fraser mitigates risk via strategic sourcing and dual-qualification programs to reduce single-supplier exposure.

Energy and fuel cost pass-through

Mills are energy intensive and exposed to electricity, natural gas and diesel price swings; in 2024 Henry Hub averaged about 2.8 USD/MMBtu and US diesel averaged near 3.7 USD/gal, increasing supplier leverage where alternatives are limited. Cogeneration and biomass use reduce but do not eliminate exposure. Long-term energy contracts and onsite generation materially stabilize costs and negotiating power.

- High exposure: energy a material input

- Mitigation: cogeneration/biomass lowers spot risk

- Stability: long-term contracts shift bargaining power

Transportation and rail capacity bottlenecks

Transportation and rail capacity bottlenecks raise supplier power for West Fraser because logs, lumber and pulp depend on finite rail and trucking corridors; car shortages, labor disputes and terminal congestion increased freight rates by approximately 12% year-over-year in 2024, giving carriers pricing leverage. Remote mill locations intensify dependence on a few carriers, while multimodal options and origin diversification provide partial buffers.

- Finite corridors: concentrated carrier control

- 2024 freight rates: ≈12% YoY increase

- Remote mills: higher switching costs

- Mitigants: multimodal transport, sourcing diversification

Wood fiber scarcity, rising fuel and freight squeeze building-materials margins

Wood fiber scarcity from wildfire, beetles and quotaed tenures tightened supplier leverage in 2024; housing starts ~1.4M raised log price volatility. Chemical/OEM suppliers remained concentrated with double-digit vendor uplifts in 2023–24. Energy (Henry Hub ~2.8 USD/MMBtu; diesel ~3.7 USD/gal) and freight (+≈12% YoY) further elevate supplier power; cogeneration, long-term contracts and sourcing reduce but do not eliminate risk.

| Supplier | 2024 metric | Impact |

|---|---|---|

| Fiber | Housing starts 1.4M | Price volatility |

| Energy | HH 2.8 USD/MMBtu | Cost exposure |

| Freight | +12% YoY | Logistics bottleneck |

What is included in the product

Tailored Porter’s Five Forces analysis for West Fraser that uncovers competitive drivers, supplier and buyer power, threat of substitutes and entrants, and emerging disruptions, with strategic commentary to assess pricing leverage and long‑term profitability.

A concise one-sheet Porter's Five Forces for West Fraser that maps supplier, buyer, rivalry, substitutes, and entry pressures—ideal for quick strategic decisions. Customize scores and radar visuals to model scenarios like timber price shocks, mill capacity changes, or regulatory shifts.

Customers Bargaining Power

Large retailers and builders concentrate demand

Big-box retailers (Home Depot, Lowe's) accounted for roughly 70% of US home‑improvement retail sales in 2024, while truss/OSB distributors and large builders (top builders deliver hundreds of thousands of homes annually) concentrate volume, enabling aggressive price negotiation, vendor scorecards and service demands. Losing a key account can dent mill utilization and margins; multi‑year supply agreements with service differentiation (dedicated trucks, JIT scheduling) help temper that leverage.

High price sensitivity in commodity lumber

Lumber and OSB trade off transparent Random Lengths indices, letting buyers time purchases and extract index-linked discounts; in 2024 softwood lumber averaged roughly 30% below 2021 peaks, amplifying buyer leverage in weak markets. Commoditization boosts price sensitivity and bargaining power, while West Fraser can protect margins via value-added grades and reliable logistics that sustain small premiums.

Low switching costs across mills

Buyers can readily switch among mills and producers when grades meet spec, so bargaining power stays high across most regions; freight differentials, which often represent roughly 5–15% of delivered price, are usually the main switching hurdle. Proximity and reliable on-time performance create soft frictions that modestly reduce buyer leverage in local markets.

Certification and sustainability requirements

Customers increasingly mandate FSC/PEFC/SFI certification and chain-of-custody; FSC+PEFC cover about 500 million hectares globally in 2024. Compliance raises supplier costs but is table stakes, letting buyers shift volumes rapidly to certified suppliers. West Fraser’s strong sustainable-forestry footprint helps defend share and pricing.

- Certification required by many large buyers

- FSC+PEFC ≈500M ha (2024)

- Raises supplier costs; increases buyer switching power

- West Fraser's certified holdings defend volumes/pricing

Export and pulp customers’ cyclical purchasing

Export and pulp customers shift volumes quickly in response to currency swings and end-market cycles, increasing spot purchases when prices fall and reducing long-term commitments; this cyclicality raised buyer leverage for West Fraser during recent downturns. A balanced contract versus spot mix — historically used to stabilize cash flow — helps smooth volume and price exposure across cycles.

- Spot buying rises in downturns

- Currency/end-market sensitivity

- Buyer leverage increases when prices drop

- Contract/spot balance mitigates volatility

Retail concentration, certification and price pressure reshape lumber margins and share

Large retailers/distributors concentrate volumes (big-box ≈70% US DIY sales 2024), giving customers price and service leverage; losing key accounts hurts utilization and margins. Commoditization and Random Lengths transparency (softwood lumber ≈30% below 2021 peaks in 2024) boost switching; certification (FSC+PEFC ≈500M ha 2024) is table stakes, raising costs but West Fraser's certified supply defends share.

| Metric | 2024 | Implication |

|---|---|---|

| Big-box US DIY share | ≈70% | High buyer concentration |

| Softwood lumber vs 2021 | ≈−30% | Increases buyer leverage |

| Certification area | FSC+PEFC ≈500M ha | Table stakes; raises supplier costs |

| Freight as % of price | ≈5–15% | Switching friction |

Same Document Delivered

West Fraser Porter's Five Forces Analysis

This preview shows the exact Porter's Five Forces analysis of West Fraser you'll receive—no surprises, no placeholders. The document provides a full assessment of competitive rivalry, supplier and buyer power, threat of substitutes, and barriers to entry. It's fully formatted and ready for immediate download after purchase.