West Fraser SWOT Analysis

Dive Deeper Into the Company’s Strategic Blueprint

Explore West Fraser’s competitive edge in forestry and engineered wood, its exposure to cyclical housing markets, and the operational and sustainability risks shaping future margins. Want the full story behind strengths, vulnerabilities, and growth levers? Purchase the complete SWOT analysis to receive a research-backed, editable Word report plus Excel tools to support investment, strategy, and pitch-ready planning.

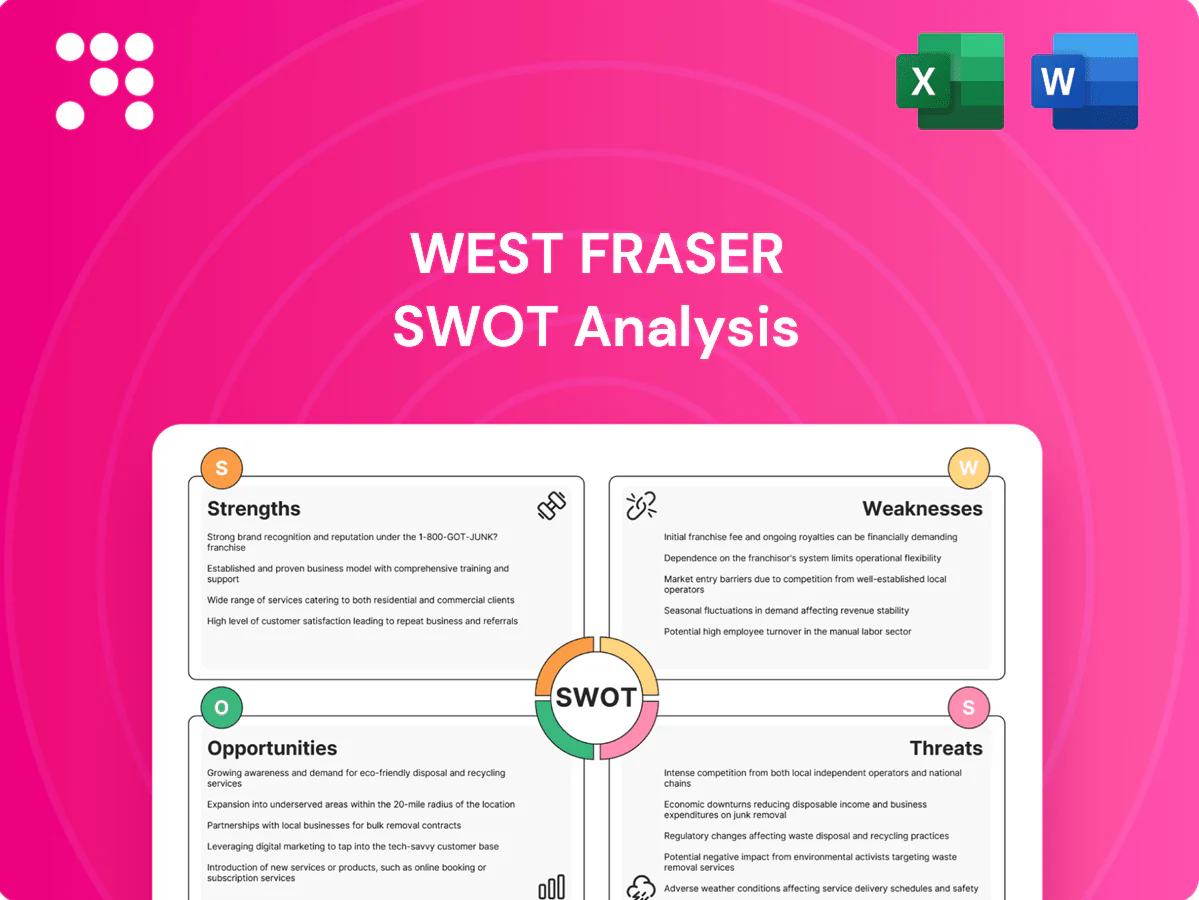

Strengths

Diversified wood product portfolio

West Fraser's portfolio spans five product lines — lumber, engineered wood, pulp, newsprint and chips — reducing reliance on any single cycle.

This mix helps buffer margins when one segment softens by shifting sales and capacity across categories.

Integrated operations enable cross-segment utilization of residuals, enhancing yield and lowering unit costs. Customers gain one-stop sourcing, strengthening long-term relationships.

Scale and operational footprint

West Fraser’s scale—operating about 58 facilities across Western Canada and the U.S. South—delivers high volume, purchasing power and logistics advantages that supported CAD 9.9 billion revenue in 2024.

Vertically integrated fiber management

Vertically integrated fiber management—West Fraser manages about 6.6 million hectares of timberland—secures supply from stump to finished product, reducing procurement risk. Integrated planning raises fiber recovery and cost predictability and supports FSC, SFI and PEFC certifications that customers demand. Strong stewardship helps dampen raw material price volatility and underpins sustainable claims.

Engineered wood capabilities

Engineered wood expands West Fraser beyond commodity lumber into higher‑margin, value‑added products aligned with structural, industrial and offsite construction trends, improving mix and pricing power. Product specifications and customization drive stickier customer relationships and repeat contracts, supporting more predictable sales. This diversification helps smooth earnings through housing cycles and supports long‑term margin resiliency.

- Value‑add exposure: higher margins vs commodity lumber

- Market fit: aligned with offsite, mass timber and industrial trends

- Customer stickiness: spec-driven repeat business

- Volatility mitigation: smoother earnings across housing cycles

Strong sustainability positioning

West Fraser’s focus on certified forestry and renewable materials (FSC, SFI across operations) aligns with growing low-carbon construction demand; mass timber can cut lifecycle emissions ~40–60% versus steel/concrete. Wood’s carbon storage resonates with builders and policymakers pursuing net-zero targets, helping West Fraser win large project bids while mitigating regulatory and reputational risk.

- Certifications: FSC, SFI across operations

- Emissions: mass timber ≈40–60% lower lifecycle CO2 vs steel/concrete

- Commercial: stronger bid success on large low-carbon projects

- Risk: reduces regulatory and reputational exposure

Diversified forest products, CAD 9.9B, ~58 facilities, ≈6.6M ha, ≈40–60% CO2

Broad product diversity (lumber, engineered wood, pulp, newsprint, chips) reduces single‑cycle exposure and aids margin resilience. Scale and integration—CAD 9.9B revenue in 2024, ~58 facilities—drive purchasing, logistics and cost advantages. Vertically managed fiber (≈6.6M ha) plus FSC/SFI/PEFC certification secures supply and supports mass‑timber demand (≈40–60% lifecycle CO2 reduction).

| Metric | Value |

|---|---|

| 2024 Revenue | CAD 9.9B |

| Facilities | ~58 |

| Timberland | ≈6.6M ha |

| Certifications | FSC, SFI, PEFC |

| Mass timber CO2 reduction | ≈40–60% |

What is included in the product

Provides a concise SWOT assessment of West Fraser’s internal capabilities, market opportunities, and external risks to inform strategic decision-making.

Provides a concise West Fraser SWOT matrix that relieves analysis bottlenecks by clearly aligning mill, supply chain, regulatory and sustainability risks and opportunities for fast executive decision-making.

Weaknesses

High cyclical exposure

High cyclical exposure leaves West Fraser revenue and margins tightly linked to housing starts, renovations and industrial activity; US housing starts ran around 1.4 million annualized in 2024, amplifying sensitivity to construction demand. Downturns compress volumes and prices quickly, pressuring lumber realizations and EBITDA margins within quarters. Inventory and working capital can swing materially, complicating cash flow, and forecasting remains challenging in late-cycle conditions.

Commodity price volatility

Benchmark Random Lengths softwood lumber peaked near 1,670 USD/mbf in May 2021 and fell to roughly 400 USD/mbf by 2023, while NBSK pulp rallied above 1,200 USD/ton in 2021–22 before retreating toward ~800–900 USD/ton in 2023–24; such swings driven by supply-demand and macro shocks make West Fraser earnings highly variable quarter to quarter. Hedging programs are limited and imperfect, leaving residual price exposure, and investors often apply a lower valuation multiple to commoditized, volatile cash flows.

Capital intensity and maintenance needs

West Fraser operates over 50 sawmills and multiple pulp facilities, which require continuous capital expenditure to sustain efficiency and regulatory compliance, with large periodic shutdowns for maintenance that materially disrupt throughput. Payback on major upgrades often hinges on stable lumber and pulp prices, exposing multi-year projects to market volatility. This capital intensity can limit financial and operational flexibility during weak cycles.

Trade and duty exposure

North American softwood lumber disputes expose West Fraser to duties and policy uncertainty, with administrative proceedings often stretching beyond a year and periodically altering access to major US and global markets.

Cash deposit requirements during anti-dumping and countervailing duty cases can strain liquidity and compress realized pricing, forcing working capital adjustments and impacting margins.

Shifts in trade policy can either advantage or penalize market access quickly, making strategic planning and pricing volatile.

Geographic concentration

Operations concentrated in Western Canada and the U.S. South heighten exposure to localized weather events, regional regulatory shifts and timber supply variability; this geographic clustering means fiber or transport disruptions can quickly cascade through mills and disrupt production. Heavy reliance on North American construction demand and limited global diversification reduce resilience to international demand shocks.

- Regional concentration: Western Canada + U.S. South

- Supply-chain vulnerability: cascading mill impact

- Market exposure: tied to North American construction

- Diversification: limited global buffer

Cyclical lumber and pulp margins swing with housing (1.4M) and trade shocks

High cyclical exposure ties revenue and margins to housing starts (~1.4M annualized in 2024), causing rapid price and EBITDA swings; Random Lengths lumber ranged from ~1,670 USD/mbf (May 2021) to ~400 USD/mbf (2023) and NBSK pulp ~800–900 USD/ton in 2023–24. Capital intensity (over 50 sawmills) and periodic shutdowns raise capex and cash-flow risk. Trade disputes (often >1 year) and cash-deposit duties strain liquidity and market access.

| Metric | Value |

|---|---|

| US housing starts (2024) | ~1.4M |

| RL lumber peak/fall | 1,670 → ~400 USD/mbf |

| NBSK pulp (2023–24) | ~800–900 USD/ton |

| Sawmills | >50 |

| Trade dispute timelines | >1 year |

Preview Before You Purchase

West Fraser SWOT Analysis

This is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full SWOT report you'll get; purchase unlocks the entire in-depth version. The file shown is the real report available after checkout.

Dive Deeper Into the Company’s Strategic Blueprint

Explore West Fraser’s competitive edge in forestry and engineered wood, its exposure to cyclical housing markets, and the operational and sustainability risks shaping future margins. Want the full story behind strengths, vulnerabilities, and growth levers? Purchase the complete SWOT analysis to receive a research-backed, editable Word report plus Excel tools to support investment, strategy, and pitch-ready planning.

Strengths

Diversified wood product portfolio

West Fraser's portfolio spans five product lines — lumber, engineered wood, pulp, newsprint and chips — reducing reliance on any single cycle.

This mix helps buffer margins when one segment softens by shifting sales and capacity across categories.

Integrated operations enable cross-segment utilization of residuals, enhancing yield and lowering unit costs. Customers gain one-stop sourcing, strengthening long-term relationships.

Scale and operational footprint

West Fraser’s scale—operating about 58 facilities across Western Canada and the U.S. South—delivers high volume, purchasing power and logistics advantages that supported CAD 9.9 billion revenue in 2024.

Vertically integrated fiber management

Vertically integrated fiber management—West Fraser manages about 6.6 million hectares of timberland—secures supply from stump to finished product, reducing procurement risk. Integrated planning raises fiber recovery and cost predictability and supports FSC, SFI and PEFC certifications that customers demand. Strong stewardship helps dampen raw material price volatility and underpins sustainable claims.

Engineered wood capabilities

Engineered wood expands West Fraser beyond commodity lumber into higher‑margin, value‑added products aligned with structural, industrial and offsite construction trends, improving mix and pricing power. Product specifications and customization drive stickier customer relationships and repeat contracts, supporting more predictable sales. This diversification helps smooth earnings through housing cycles and supports long‑term margin resiliency.

- Value‑add exposure: higher margins vs commodity lumber

- Market fit: aligned with offsite, mass timber and industrial trends

- Customer stickiness: spec-driven repeat business

- Volatility mitigation: smoother earnings across housing cycles

Strong sustainability positioning

West Fraser’s focus on certified forestry and renewable materials (FSC, SFI across operations) aligns with growing low-carbon construction demand; mass timber can cut lifecycle emissions ~40–60% versus steel/concrete. Wood’s carbon storage resonates with builders and policymakers pursuing net-zero targets, helping West Fraser win large project bids while mitigating regulatory and reputational risk.

- Certifications: FSC, SFI across operations

- Emissions: mass timber ≈40–60% lower lifecycle CO2 vs steel/concrete

- Commercial: stronger bid success on large low-carbon projects

- Risk: reduces regulatory and reputational exposure

Diversified forest products, CAD 9.9B, ~58 facilities, ≈6.6M ha, ≈40–60% CO2

Broad product diversity (lumber, engineered wood, pulp, newsprint, chips) reduces single‑cycle exposure and aids margin resilience. Scale and integration—CAD 9.9B revenue in 2024, ~58 facilities—drive purchasing, logistics and cost advantages. Vertically managed fiber (≈6.6M ha) plus FSC/SFI/PEFC certification secures supply and supports mass‑timber demand (≈40–60% lifecycle CO2 reduction).

| Metric | Value |

|---|---|

| 2024 Revenue | CAD 9.9B |

| Facilities | ~58 |

| Timberland | ≈6.6M ha |

| Certifications | FSC, SFI, PEFC |

| Mass timber CO2 reduction | ≈40–60% |

What is included in the product

Provides a concise SWOT assessment of West Fraser’s internal capabilities, market opportunities, and external risks to inform strategic decision-making.

Provides a concise West Fraser SWOT matrix that relieves analysis bottlenecks by clearly aligning mill, supply chain, regulatory and sustainability risks and opportunities for fast executive decision-making.

Weaknesses

High cyclical exposure

High cyclical exposure leaves West Fraser revenue and margins tightly linked to housing starts, renovations and industrial activity; US housing starts ran around 1.4 million annualized in 2024, amplifying sensitivity to construction demand. Downturns compress volumes and prices quickly, pressuring lumber realizations and EBITDA margins within quarters. Inventory and working capital can swing materially, complicating cash flow, and forecasting remains challenging in late-cycle conditions.

Commodity price volatility

Benchmark Random Lengths softwood lumber peaked near 1,670 USD/mbf in May 2021 and fell to roughly 400 USD/mbf by 2023, while NBSK pulp rallied above 1,200 USD/ton in 2021–22 before retreating toward ~800–900 USD/ton in 2023–24; such swings driven by supply-demand and macro shocks make West Fraser earnings highly variable quarter to quarter. Hedging programs are limited and imperfect, leaving residual price exposure, and investors often apply a lower valuation multiple to commoditized, volatile cash flows.

Capital intensity and maintenance needs

West Fraser operates over 50 sawmills and multiple pulp facilities, which require continuous capital expenditure to sustain efficiency and regulatory compliance, with large periodic shutdowns for maintenance that materially disrupt throughput. Payback on major upgrades often hinges on stable lumber and pulp prices, exposing multi-year projects to market volatility. This capital intensity can limit financial and operational flexibility during weak cycles.

Trade and duty exposure

North American softwood lumber disputes expose West Fraser to duties and policy uncertainty, with administrative proceedings often stretching beyond a year and periodically altering access to major US and global markets.

Cash deposit requirements during anti-dumping and countervailing duty cases can strain liquidity and compress realized pricing, forcing working capital adjustments and impacting margins.

Shifts in trade policy can either advantage or penalize market access quickly, making strategic planning and pricing volatile.

Geographic concentration

Operations concentrated in Western Canada and the U.S. South heighten exposure to localized weather events, regional regulatory shifts and timber supply variability; this geographic clustering means fiber or transport disruptions can quickly cascade through mills and disrupt production. Heavy reliance on North American construction demand and limited global diversification reduce resilience to international demand shocks.

- Regional concentration: Western Canada + U.S. South

- Supply-chain vulnerability: cascading mill impact

- Market exposure: tied to North American construction

- Diversification: limited global buffer

Cyclical lumber and pulp margins swing with housing (1.4M) and trade shocks

High cyclical exposure ties revenue and margins to housing starts (~1.4M annualized in 2024), causing rapid price and EBITDA swings; Random Lengths lumber ranged from ~1,670 USD/mbf (May 2021) to ~400 USD/mbf (2023) and NBSK pulp ~800–900 USD/ton in 2023–24. Capital intensity (over 50 sawmills) and periodic shutdowns raise capex and cash-flow risk. Trade disputes (often >1 year) and cash-deposit duties strain liquidity and market access.

| Metric | Value |

|---|---|

| US housing starts (2024) | ~1.4M |

| RL lumber peak/fall | 1,670 → ~400 USD/mbf |

| NBSK pulp (2023–24) | ~800–900 USD/ton |

| Sawmills | >50 |

| Trade dispute timelines | >1 year |

Preview Before You Purchase

West Fraser SWOT Analysis

This is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full SWOT report you'll get; purchase unlocks the entire in-depth version. The file shown is the real report available after checkout.

Description

Dive Deeper Into the Company’s Strategic Blueprint

Explore West Fraser’s competitive edge in forestry and engineered wood, its exposure to cyclical housing markets, and the operational and sustainability risks shaping future margins. Want the full story behind strengths, vulnerabilities, and growth levers? Purchase the complete SWOT analysis to receive a research-backed, editable Word report plus Excel tools to support investment, strategy, and pitch-ready planning.

Strengths

Diversified wood product portfolio

West Fraser's portfolio spans five product lines — lumber, engineered wood, pulp, newsprint and chips — reducing reliance on any single cycle.

This mix helps buffer margins when one segment softens by shifting sales and capacity across categories.

Integrated operations enable cross-segment utilization of residuals, enhancing yield and lowering unit costs. Customers gain one-stop sourcing, strengthening long-term relationships.

Scale and operational footprint

West Fraser’s scale—operating about 58 facilities across Western Canada and the U.S. South—delivers high volume, purchasing power and logistics advantages that supported CAD 9.9 billion revenue in 2024.

Vertically integrated fiber management

Vertically integrated fiber management—West Fraser manages about 6.6 million hectares of timberland—secures supply from stump to finished product, reducing procurement risk. Integrated planning raises fiber recovery and cost predictability and supports FSC, SFI and PEFC certifications that customers demand. Strong stewardship helps dampen raw material price volatility and underpins sustainable claims.

Engineered wood capabilities

Engineered wood expands West Fraser beyond commodity lumber into higher‑margin, value‑added products aligned with structural, industrial and offsite construction trends, improving mix and pricing power. Product specifications and customization drive stickier customer relationships and repeat contracts, supporting more predictable sales. This diversification helps smooth earnings through housing cycles and supports long‑term margin resiliency.

- Value‑add exposure: higher margins vs commodity lumber

- Market fit: aligned with offsite, mass timber and industrial trends

- Customer stickiness: spec-driven repeat business

- Volatility mitigation: smoother earnings across housing cycles

Strong sustainability positioning

West Fraser’s focus on certified forestry and renewable materials (FSC, SFI across operations) aligns with growing low-carbon construction demand; mass timber can cut lifecycle emissions ~40–60% versus steel/concrete. Wood’s carbon storage resonates with builders and policymakers pursuing net-zero targets, helping West Fraser win large project bids while mitigating regulatory and reputational risk.

- Certifications: FSC, SFI across operations

- Emissions: mass timber ≈40–60% lower lifecycle CO2 vs steel/concrete

- Commercial: stronger bid success on large low-carbon projects

- Risk: reduces regulatory and reputational exposure

Diversified forest products, CAD 9.9B, ~58 facilities, ≈6.6M ha, ≈40–60% CO2

Broad product diversity (lumber, engineered wood, pulp, newsprint, chips) reduces single‑cycle exposure and aids margin resilience. Scale and integration—CAD 9.9B revenue in 2024, ~58 facilities—drive purchasing, logistics and cost advantages. Vertically managed fiber (≈6.6M ha) plus FSC/SFI/PEFC certification secures supply and supports mass‑timber demand (≈40–60% lifecycle CO2 reduction).

| Metric | Value |

|---|---|

| 2024 Revenue | CAD 9.9B |

| Facilities | ~58 |

| Timberland | ≈6.6M ha |

| Certifications | FSC, SFI, PEFC |

| Mass timber CO2 reduction | ≈40–60% |

What is included in the product

Provides a concise SWOT assessment of West Fraser’s internal capabilities, market opportunities, and external risks to inform strategic decision-making.

Provides a concise West Fraser SWOT matrix that relieves analysis bottlenecks by clearly aligning mill, supply chain, regulatory and sustainability risks and opportunities for fast executive decision-making.

Weaknesses

High cyclical exposure

High cyclical exposure leaves West Fraser revenue and margins tightly linked to housing starts, renovations and industrial activity; US housing starts ran around 1.4 million annualized in 2024, amplifying sensitivity to construction demand. Downturns compress volumes and prices quickly, pressuring lumber realizations and EBITDA margins within quarters. Inventory and working capital can swing materially, complicating cash flow, and forecasting remains challenging in late-cycle conditions.

Commodity price volatility

Benchmark Random Lengths softwood lumber peaked near 1,670 USD/mbf in May 2021 and fell to roughly 400 USD/mbf by 2023, while NBSK pulp rallied above 1,200 USD/ton in 2021–22 before retreating toward ~800–900 USD/ton in 2023–24; such swings driven by supply-demand and macro shocks make West Fraser earnings highly variable quarter to quarter. Hedging programs are limited and imperfect, leaving residual price exposure, and investors often apply a lower valuation multiple to commoditized, volatile cash flows.

Capital intensity and maintenance needs

West Fraser operates over 50 sawmills and multiple pulp facilities, which require continuous capital expenditure to sustain efficiency and regulatory compliance, with large periodic shutdowns for maintenance that materially disrupt throughput. Payback on major upgrades often hinges on stable lumber and pulp prices, exposing multi-year projects to market volatility. This capital intensity can limit financial and operational flexibility during weak cycles.

Trade and duty exposure

North American softwood lumber disputes expose West Fraser to duties and policy uncertainty, with administrative proceedings often stretching beyond a year and periodically altering access to major US and global markets.

Cash deposit requirements during anti-dumping and countervailing duty cases can strain liquidity and compress realized pricing, forcing working capital adjustments and impacting margins.

Shifts in trade policy can either advantage or penalize market access quickly, making strategic planning and pricing volatile.

Geographic concentration

Operations concentrated in Western Canada and the U.S. South heighten exposure to localized weather events, regional regulatory shifts and timber supply variability; this geographic clustering means fiber or transport disruptions can quickly cascade through mills and disrupt production. Heavy reliance on North American construction demand and limited global diversification reduce resilience to international demand shocks.

- Regional concentration: Western Canada + U.S. South

- Supply-chain vulnerability: cascading mill impact

- Market exposure: tied to North American construction

- Diversification: limited global buffer

Cyclical lumber and pulp margins swing with housing (1.4M) and trade shocks

High cyclical exposure ties revenue and margins to housing starts (~1.4M annualized in 2024), causing rapid price and EBITDA swings; Random Lengths lumber ranged from ~1,670 USD/mbf (May 2021) to ~400 USD/mbf (2023) and NBSK pulp ~800–900 USD/ton in 2023–24. Capital intensity (over 50 sawmills) and periodic shutdowns raise capex and cash-flow risk. Trade disputes (often >1 year) and cash-deposit duties strain liquidity and market access.

| Metric | Value |

|---|---|

| US housing starts (2024) | ~1.4M |

| RL lumber peak/fall | 1,670 → ~400 USD/mbf |

| NBSK pulp (2023–24) | ~800–900 USD/ton |

| Sawmills | >50 |

| Trade dispute timelines | >1 year |

Preview Before You Purchase

West Fraser SWOT Analysis

This is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full SWOT report you'll get; purchase unlocks the entire in-depth version. The file shown is the real report available after checkout.