George Weston Porter's Five Forces Analysis

From Overview to Strategy Blueprint

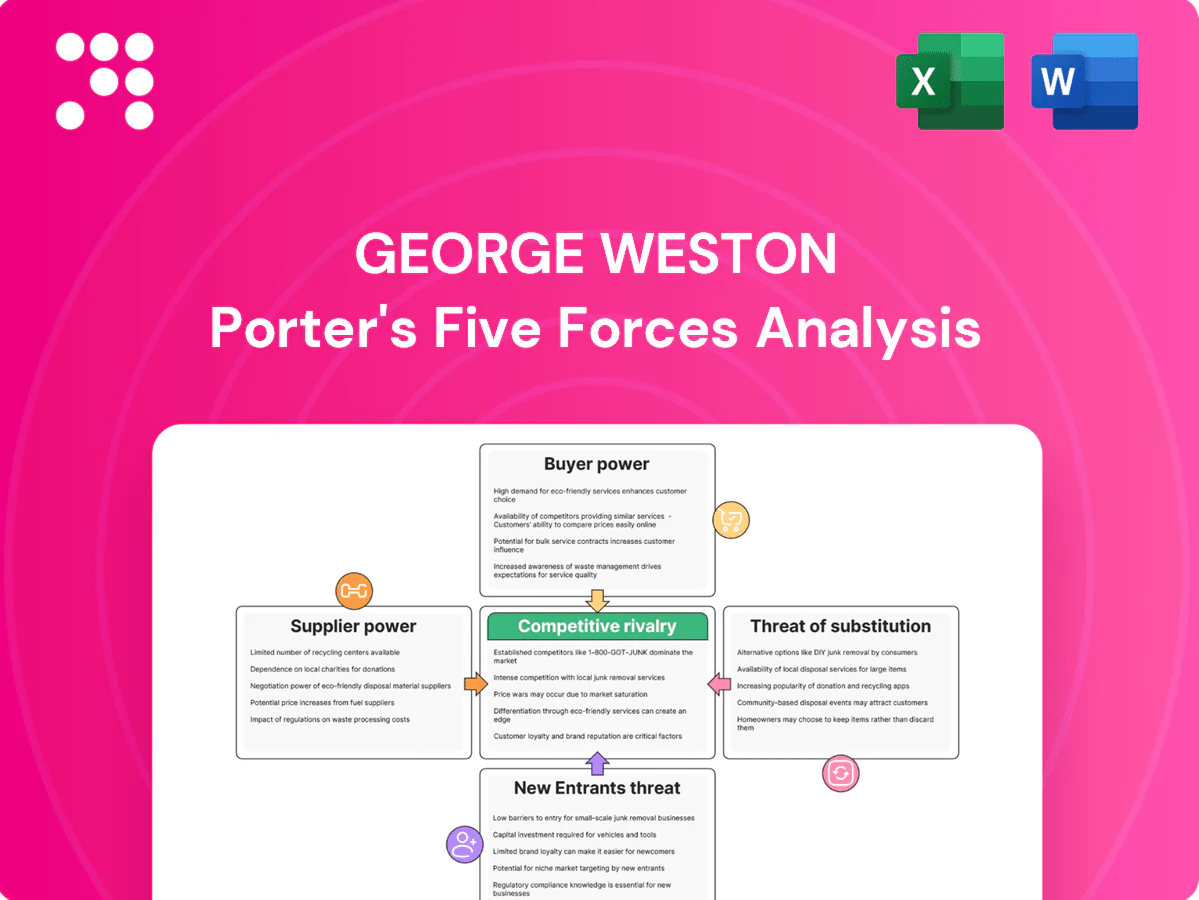

George Weston's Porter’s Five Forces snapshot highlights competitive rivalry, supplier and buyer power, and threats from substitutes and new entrants, showing where strategic levers may lie. This brief overview surfaces key pressures but omits force-by-force ratings, visuals, and tactical implications. Unlock the full Porter's Five Forces Analysis to explore George Weston’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Scale dampens vendor leverage

George Weston’s majority ownership of Loblaw concentrates purchasing across over 2,400 stores (2024), sharply curbing branded suppliers’ pricing power.

Centralized procurement, long-term contracts and data-driven category management secure favorable terms and margins for Weston.

Supplier consolidation in fresh and meat can still raise leverage, but strong private-label penetration (President’s Choice leadership) provides a credible counterweight.

Private label as a counterbalance

President’s Choice and No Name give Weston credible negotiation leverage against CPG brands, with private-label penetration in Canada at about 26% in 2024 enhancing bargaining position. Own brands reduce dependence on any single manufacturer and enable rapid price-pack architecture changes. They capture margin and shelf space, structurally lowering supplier power. Reliance on a few co-packers, however, creates pockets of exposure.

Perishables and local sourcing constraints

Fresh produce, meat and bakery sourcing for George Weston/Loblaw depends heavily on regional and seasonal suppliers, limiting alternatives and increasing supplier leverage. Weather shocks and biosecurity events in 2024 drove short-term input cost spikes, shifting bargaining power toward suppliers. Loblaw’s extensive distribution network and cold-chain reduce but do not remove this volatility; Loblaw reported CAD 58.1 billion revenue in fiscal 2024, highlighting exposure scale. Certification and strict quality standards further narrow viable supplier pools.

Pharma and regulated categories

Brand-name manufacturers retain strong supplier power via IP and formulary placement, shaping price and access. Canadian generics account for ~80% of prescriptions by volume but price controls cap prices and limit switching. Pharmacy reimbursement compresses retail margins to low single digits; Shoppers Drug Mart’s scale (~1,300 stores) improves purchasing leverage but upstream imbalance persists.

- Brand IP and formulary control

- Generics ~80% of prescriptions (volume)

- Retail margins compressed to low single digits

- Shoppers Drug Mart ~1,300 stores

Real estate and infrastructure inputs

Choice Properties relies on construction, utilities and maintenance vendors that face capacity bottlenecks; tight trades markets and rising materials costs have increased supplier leverage and can extend development timelines.

- Multi-year service agreements reduce short-term disruption risk

- Preferred-vendor programs lower procurement volatility

- Geographic diversification mitigates localized supplier pressures

Centralized buying and scale CAD 58.1bn, ~2,400 stores curb supplier pricing power

George Weston’s centralized buying across ~2,400 Loblaw stores (2024) and CAD 58.1bn revenue (FY2024) materially suppress supplier pricing power.

Private-label penetration ~26% (2024) and President’s Choice scale provide strong countervailing leverage versus CPG brands.

Fresh/meat seasonal constraints and reliance on co-packers create localized supplier pockets of power; pharmacy margins remain compressed.

| Metric | 2024 |

|---|---|

| Loblaw stores | ~2,400 |

| Revenue | CAD 58.1bn |

| Private-label share | ~26% |

| Shoppers stores | ~1,300 |

What is included in the product

Comprehensive Porter's Five Forces analysis of George Weston that uncovers competitive drivers, supplier and buyer power, threat of substitutes and new entrants, and identifies disruptive trends affecting pricing, margins, and market position.

A one-sheet Porter's Five Forces for George Weston—visualizes supplier/buyer power, entrant/substitute threats and competitive rivalry to pinpoint pain points and prioritize tactical responses for faster, data-driven strategy decisions.

Customers Bargaining Power

Price-sensitive grocery consumers

Canadian shoppers are highly value focused, amplified by the 8.1% CPI peak in 2022 and lingering cost pressure into 2024, raising price sensitivity. Low switching costs across banners and widespread promotions, price matching and EDLP erode margins. Loblaw (≈27% market share) offsets this with broad assortments and multi-tier private labels such as President's Choice and no-name to protect margins.

Loyalty and ecosystem stickiness

PC Optimum exceeded 20 million members in 2024 and Loblaw's digital apps register millions of monthly active users, creating switching frictions and rich transaction data advantages. Points, targeted offers and PC Financial credit integrations temper raw buyer power by personalizing value and raising switching costs. Nevertheless high value expectations keep price pressure alive—loyalty reduces but does not eliminate it. The broad ecosystem functions as a defensive moat.

Format and channel alternatives

Customers can shift among discounters, supermarkets, clubs, dollar stores and e-grocery, increasing switching options and price transparency. Walmart (FY2024 revenue $611.3 billion) and Costco anchor strong cross-category value perceptions that amplify buyer expectations. This plurality strengthens negotiating power via easy comparison, though convenience and store proximity still often determine final choice.

Pharmacy patient choice

Patients can shift between chains and independents subject to location and insurer networks; prescriptions drive ~55% of pharmacy revenue in 2024, anchoring stickiness while OTCs face ~15% online substitution, increasing buyer leverage. Professional consultations and script fulfillment add retention but are partly commoditized; service quality and wait times materially influence churn.

- Chains vs independents: network/location constrained

- Rx revenue ~55% (2024)

- OTC online substitution ~15% (2024)

- Consults add stickiness; wait times affect retention

Tenants as B2B customers

Tenants negotiate rents, tenant-improvement allowances and lease terms with Choice Properties as B2B customers; in 2024 Choice reported portfolio occupancy near 98%, limiting tenant exit leverage while keeping renewal bargaining focused on concessions and TI levels. Loblaw remains the dominant anchor tenant, underpinning demand and reducing overall tenant bargaining power, though soft retail markets in 2023–24 increased concessioning. Lease maturities create episodic negotiation windows when tenants can extract better terms or request higher TIs.

- Anchor strength: Loblaw largest tenant, stabilizes occupancy

- Occupancy: ~98% in 2024, constrains tenant leverage

- Concessions: rose in soft retail markets 2023–24

- Maturities: concentrate negotiation opportunities

Price-sensitive Canadian shoppers favor private labels and online OTC, squeezing retailer margins

Canadian shoppers are highly price sensitive after an 8.1% CPI peak in 2022 and persistent 2024 cost pressure, while low switching costs and widespread promotions erode margins. Loblaw (~27% market share) and PC Optimum (>20M members in 2024) raise switching frictions via private labels and targeted offers. Cross-channel competition (Walmart FY2024 revenue $611.3B, Costco) and 15% OTC online substitution (2024) sustain buyer leverage.

| Metric | Value (2024) |

|---|---|

| CPI peak | 8.1% (2022) |

| Loblaw market share | ~27% |

| PC Optimum members | >20M |

| Walmart revenue | $611.3B |

| Rx revenue | ~55% |

| OTC online substitution | ~15% |

Preview the Actual Deliverable

George Weston Porter's Five Forces Analysis

This preview shows the exact George Weston Porter's Five Forces analysis you'll receive immediately after purchase—no surprises or placeholders. The document displayed is fully formatted and ready for download and use the moment you buy. You’ll get instant access to this same file.

From Overview to Strategy Blueprint

George Weston's Porter’s Five Forces snapshot highlights competitive rivalry, supplier and buyer power, and threats from substitutes and new entrants, showing where strategic levers may lie. This brief overview surfaces key pressures but omits force-by-force ratings, visuals, and tactical implications. Unlock the full Porter's Five Forces Analysis to explore George Weston’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Scale dampens vendor leverage

George Weston’s majority ownership of Loblaw concentrates purchasing across over 2,400 stores (2024), sharply curbing branded suppliers’ pricing power.

Centralized procurement, long-term contracts and data-driven category management secure favorable terms and margins for Weston.

Supplier consolidation in fresh and meat can still raise leverage, but strong private-label penetration (President’s Choice leadership) provides a credible counterweight.

Private label as a counterbalance

President’s Choice and No Name give Weston credible negotiation leverage against CPG brands, with private-label penetration in Canada at about 26% in 2024 enhancing bargaining position. Own brands reduce dependence on any single manufacturer and enable rapid price-pack architecture changes. They capture margin and shelf space, structurally lowering supplier power. Reliance on a few co-packers, however, creates pockets of exposure.

Perishables and local sourcing constraints

Fresh produce, meat and bakery sourcing for George Weston/Loblaw depends heavily on regional and seasonal suppliers, limiting alternatives and increasing supplier leverage. Weather shocks and biosecurity events in 2024 drove short-term input cost spikes, shifting bargaining power toward suppliers. Loblaw’s extensive distribution network and cold-chain reduce but do not remove this volatility; Loblaw reported CAD 58.1 billion revenue in fiscal 2024, highlighting exposure scale. Certification and strict quality standards further narrow viable supplier pools.

Pharma and regulated categories

Brand-name manufacturers retain strong supplier power via IP and formulary placement, shaping price and access. Canadian generics account for ~80% of prescriptions by volume but price controls cap prices and limit switching. Pharmacy reimbursement compresses retail margins to low single digits; Shoppers Drug Mart’s scale (~1,300 stores) improves purchasing leverage but upstream imbalance persists.

- Brand IP and formulary control

- Generics ~80% of prescriptions (volume)

- Retail margins compressed to low single digits

- Shoppers Drug Mart ~1,300 stores

Real estate and infrastructure inputs

Choice Properties relies on construction, utilities and maintenance vendors that face capacity bottlenecks; tight trades markets and rising materials costs have increased supplier leverage and can extend development timelines.

- Multi-year service agreements reduce short-term disruption risk

- Preferred-vendor programs lower procurement volatility

- Geographic diversification mitigates localized supplier pressures

Centralized buying and scale CAD 58.1bn, ~2,400 stores curb supplier pricing power

George Weston’s centralized buying across ~2,400 Loblaw stores (2024) and CAD 58.1bn revenue (FY2024) materially suppress supplier pricing power.

Private-label penetration ~26% (2024) and President’s Choice scale provide strong countervailing leverage versus CPG brands.

Fresh/meat seasonal constraints and reliance on co-packers create localized supplier pockets of power; pharmacy margins remain compressed.

| Metric | 2024 |

|---|---|

| Loblaw stores | ~2,400 |

| Revenue | CAD 58.1bn |

| Private-label share | ~26% |

| Shoppers stores | ~1,300 |

What is included in the product

Comprehensive Porter's Five Forces analysis of George Weston that uncovers competitive drivers, supplier and buyer power, threat of substitutes and new entrants, and identifies disruptive trends affecting pricing, margins, and market position.

A one-sheet Porter's Five Forces for George Weston—visualizes supplier/buyer power, entrant/substitute threats and competitive rivalry to pinpoint pain points and prioritize tactical responses for faster, data-driven strategy decisions.

Customers Bargaining Power

Price-sensitive grocery consumers

Canadian shoppers are highly value focused, amplified by the 8.1% CPI peak in 2022 and lingering cost pressure into 2024, raising price sensitivity. Low switching costs across banners and widespread promotions, price matching and EDLP erode margins. Loblaw (≈27% market share) offsets this with broad assortments and multi-tier private labels such as President's Choice and no-name to protect margins.

Loyalty and ecosystem stickiness

PC Optimum exceeded 20 million members in 2024 and Loblaw's digital apps register millions of monthly active users, creating switching frictions and rich transaction data advantages. Points, targeted offers and PC Financial credit integrations temper raw buyer power by personalizing value and raising switching costs. Nevertheless high value expectations keep price pressure alive—loyalty reduces but does not eliminate it. The broad ecosystem functions as a defensive moat.

Format and channel alternatives

Customers can shift among discounters, supermarkets, clubs, dollar stores and e-grocery, increasing switching options and price transparency. Walmart (FY2024 revenue $611.3 billion) and Costco anchor strong cross-category value perceptions that amplify buyer expectations. This plurality strengthens negotiating power via easy comparison, though convenience and store proximity still often determine final choice.

Pharmacy patient choice

Patients can shift between chains and independents subject to location and insurer networks; prescriptions drive ~55% of pharmacy revenue in 2024, anchoring stickiness while OTCs face ~15% online substitution, increasing buyer leverage. Professional consultations and script fulfillment add retention but are partly commoditized; service quality and wait times materially influence churn.

- Chains vs independents: network/location constrained

- Rx revenue ~55% (2024)

- OTC online substitution ~15% (2024)

- Consults add stickiness; wait times affect retention

Tenants as B2B customers

Tenants negotiate rents, tenant-improvement allowances and lease terms with Choice Properties as B2B customers; in 2024 Choice reported portfolio occupancy near 98%, limiting tenant exit leverage while keeping renewal bargaining focused on concessions and TI levels. Loblaw remains the dominant anchor tenant, underpinning demand and reducing overall tenant bargaining power, though soft retail markets in 2023–24 increased concessioning. Lease maturities create episodic negotiation windows when tenants can extract better terms or request higher TIs.

- Anchor strength: Loblaw largest tenant, stabilizes occupancy

- Occupancy: ~98% in 2024, constrains tenant leverage

- Concessions: rose in soft retail markets 2023–24

- Maturities: concentrate negotiation opportunities

Price-sensitive Canadian shoppers favor private labels and online OTC, squeezing retailer margins

Canadian shoppers are highly price sensitive after an 8.1% CPI peak in 2022 and persistent 2024 cost pressure, while low switching costs and widespread promotions erode margins. Loblaw (~27% market share) and PC Optimum (>20M members in 2024) raise switching frictions via private labels and targeted offers. Cross-channel competition (Walmart FY2024 revenue $611.3B, Costco) and 15% OTC online substitution (2024) sustain buyer leverage.

| Metric | Value (2024) |

|---|---|

| CPI peak | 8.1% (2022) |

| Loblaw market share | ~27% |

| PC Optimum members | >20M |

| Walmart revenue | $611.3B |

| Rx revenue | ~55% |

| OTC online substitution | ~15% |

Preview the Actual Deliverable

George Weston Porter's Five Forces Analysis

This preview shows the exact George Weston Porter's Five Forces analysis you'll receive immediately after purchase—no surprises or placeholders. The document displayed is fully formatted and ready for download and use the moment you buy. You’ll get instant access to this same file.

Description

From Overview to Strategy Blueprint

George Weston's Porter’s Five Forces snapshot highlights competitive rivalry, supplier and buyer power, and threats from substitutes and new entrants, showing where strategic levers may lie. This brief overview surfaces key pressures but omits force-by-force ratings, visuals, and tactical implications. Unlock the full Porter's Five Forces Analysis to explore George Weston’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Scale dampens vendor leverage

George Weston’s majority ownership of Loblaw concentrates purchasing across over 2,400 stores (2024), sharply curbing branded suppliers’ pricing power.

Centralized procurement, long-term contracts and data-driven category management secure favorable terms and margins for Weston.

Supplier consolidation in fresh and meat can still raise leverage, but strong private-label penetration (President’s Choice leadership) provides a credible counterweight.

Private label as a counterbalance

President’s Choice and No Name give Weston credible negotiation leverage against CPG brands, with private-label penetration in Canada at about 26% in 2024 enhancing bargaining position. Own brands reduce dependence on any single manufacturer and enable rapid price-pack architecture changes. They capture margin and shelf space, structurally lowering supplier power. Reliance on a few co-packers, however, creates pockets of exposure.

Perishables and local sourcing constraints

Fresh produce, meat and bakery sourcing for George Weston/Loblaw depends heavily on regional and seasonal suppliers, limiting alternatives and increasing supplier leverage. Weather shocks and biosecurity events in 2024 drove short-term input cost spikes, shifting bargaining power toward suppliers. Loblaw’s extensive distribution network and cold-chain reduce but do not remove this volatility; Loblaw reported CAD 58.1 billion revenue in fiscal 2024, highlighting exposure scale. Certification and strict quality standards further narrow viable supplier pools.

Pharma and regulated categories

Brand-name manufacturers retain strong supplier power via IP and formulary placement, shaping price and access. Canadian generics account for ~80% of prescriptions by volume but price controls cap prices and limit switching. Pharmacy reimbursement compresses retail margins to low single digits; Shoppers Drug Mart’s scale (~1,300 stores) improves purchasing leverage but upstream imbalance persists.

- Brand IP and formulary control

- Generics ~80% of prescriptions (volume)

- Retail margins compressed to low single digits

- Shoppers Drug Mart ~1,300 stores

Real estate and infrastructure inputs

Choice Properties relies on construction, utilities and maintenance vendors that face capacity bottlenecks; tight trades markets and rising materials costs have increased supplier leverage and can extend development timelines.

- Multi-year service agreements reduce short-term disruption risk

- Preferred-vendor programs lower procurement volatility

- Geographic diversification mitigates localized supplier pressures

Centralized buying and scale CAD 58.1bn, ~2,400 stores curb supplier pricing power

George Weston’s centralized buying across ~2,400 Loblaw stores (2024) and CAD 58.1bn revenue (FY2024) materially suppress supplier pricing power.

Private-label penetration ~26% (2024) and President’s Choice scale provide strong countervailing leverage versus CPG brands.

Fresh/meat seasonal constraints and reliance on co-packers create localized supplier pockets of power; pharmacy margins remain compressed.

| Metric | 2024 |

|---|---|

| Loblaw stores | ~2,400 |

| Revenue | CAD 58.1bn |

| Private-label share | ~26% |

| Shoppers stores | ~1,300 |

What is included in the product

Comprehensive Porter's Five Forces analysis of George Weston that uncovers competitive drivers, supplier and buyer power, threat of substitutes and new entrants, and identifies disruptive trends affecting pricing, margins, and market position.

A one-sheet Porter's Five Forces for George Weston—visualizes supplier/buyer power, entrant/substitute threats and competitive rivalry to pinpoint pain points and prioritize tactical responses for faster, data-driven strategy decisions.

Customers Bargaining Power

Price-sensitive grocery consumers

Canadian shoppers are highly value focused, amplified by the 8.1% CPI peak in 2022 and lingering cost pressure into 2024, raising price sensitivity. Low switching costs across banners and widespread promotions, price matching and EDLP erode margins. Loblaw (≈27% market share) offsets this with broad assortments and multi-tier private labels such as President's Choice and no-name to protect margins.

Loyalty and ecosystem stickiness

PC Optimum exceeded 20 million members in 2024 and Loblaw's digital apps register millions of monthly active users, creating switching frictions and rich transaction data advantages. Points, targeted offers and PC Financial credit integrations temper raw buyer power by personalizing value and raising switching costs. Nevertheless high value expectations keep price pressure alive—loyalty reduces but does not eliminate it. The broad ecosystem functions as a defensive moat.

Format and channel alternatives

Customers can shift among discounters, supermarkets, clubs, dollar stores and e-grocery, increasing switching options and price transparency. Walmart (FY2024 revenue $611.3 billion) and Costco anchor strong cross-category value perceptions that amplify buyer expectations. This plurality strengthens negotiating power via easy comparison, though convenience and store proximity still often determine final choice.

Pharmacy patient choice

Patients can shift between chains and independents subject to location and insurer networks; prescriptions drive ~55% of pharmacy revenue in 2024, anchoring stickiness while OTCs face ~15% online substitution, increasing buyer leverage. Professional consultations and script fulfillment add retention but are partly commoditized; service quality and wait times materially influence churn.

- Chains vs independents: network/location constrained

- Rx revenue ~55% (2024)

- OTC online substitution ~15% (2024)

- Consults add stickiness; wait times affect retention

Tenants as B2B customers

Tenants negotiate rents, tenant-improvement allowances and lease terms with Choice Properties as B2B customers; in 2024 Choice reported portfolio occupancy near 98%, limiting tenant exit leverage while keeping renewal bargaining focused on concessions and TI levels. Loblaw remains the dominant anchor tenant, underpinning demand and reducing overall tenant bargaining power, though soft retail markets in 2023–24 increased concessioning. Lease maturities create episodic negotiation windows when tenants can extract better terms or request higher TIs.

- Anchor strength: Loblaw largest tenant, stabilizes occupancy

- Occupancy: ~98% in 2024, constrains tenant leverage

- Concessions: rose in soft retail markets 2023–24

- Maturities: concentrate negotiation opportunities

Price-sensitive Canadian shoppers favor private labels and online OTC, squeezing retailer margins

Canadian shoppers are highly price sensitive after an 8.1% CPI peak in 2022 and persistent 2024 cost pressure, while low switching costs and widespread promotions erode margins. Loblaw (~27% market share) and PC Optimum (>20M members in 2024) raise switching frictions via private labels and targeted offers. Cross-channel competition (Walmart FY2024 revenue $611.3B, Costco) and 15% OTC online substitution (2024) sustain buyer leverage.

| Metric | Value (2024) |

|---|---|

| CPI peak | 8.1% (2022) |

| Loblaw market share | ~27% |

| PC Optimum members | >20M |

| Walmart revenue | $611.3B |

| Rx revenue | ~55% |

| OTC online substitution | ~15% |

Preview the Actual Deliverable

George Weston Porter's Five Forces Analysis

This preview shows the exact George Weston Porter's Five Forces analysis you'll receive immediately after purchase—no surprises or placeholders. The document displayed is fully formatted and ready for download and use the moment you buy. You’ll get instant access to this same file.