Westpac Bank Boston Consulting Group Matrix

Actionable Strategy Starts Here

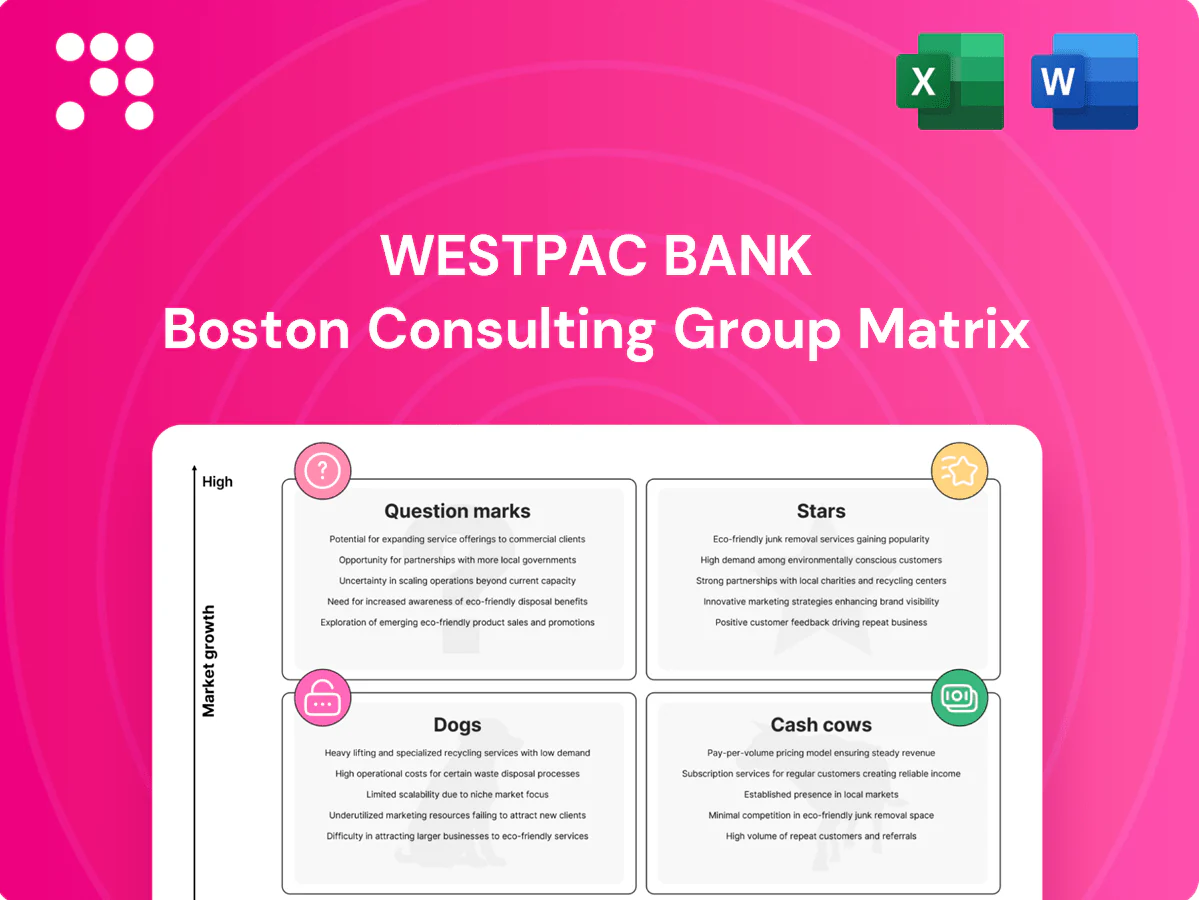

Curious where Westpac’s businesses sit—Stars, Cash Cows, Dogs or Question Marks? This quick peek hints at momentum and risk, but the full BCG Matrix gives you quadrant-by-quadrant clarity, tailored recommendations and ready-to-use visuals. Purchase the complete report for a downloadable Word analysis plus an Excel summary you can plug into board decks and planning sessions. Get it now and stop guessing where to invest your next dollar.

Stars

Digital consumer banking (mobile + online)

Westpac's digital consumer banking sees high daily usage and strong brand trust, with over 5 million active digital customers reported in 2024 and growing adoption as Australia shifts fast to mobile-first banking. Continuous investment in UX, features and security is required to stay ahead, keeping pace with real-time payments and NPP-driven instant transfers. Ongoing personalisation and spend secures market share now and lets this star mature into a cash cow later.

Real-time payments and data-led services

Westpac's exposure to real-time rails — NPP and PayID — matters: over 18 million PayIDs in Australia by 2024 and rapidly rising adoption in NZ. Delivering richer data at scale requires heavy investment in reliability, fraud controls and partner integrations. Monetisation leans on value-added services (data analytics, liquidity tools), not interchange fees. Winning here anchors account primacy and cross-sell economics.

SME digital lending and onboarding

SME digital lending and onboarding at Westpac sits in a high-growth quadrant as SME demand rebounded in 2024 with Australian business credit growth around 5% year-on-year and online applications rising sharply. The space is crowded, so faster decisioning and advanced risk models are critical to win share. Keep acquisition costs tight while improving straight-through processing to lift lifetime value. Scale now to lock in cohort retention and cross-sell revenue.

Sustainable finance and green lending

Sustainable finance and green lending sit in Stars: corporate and retail ESG lending demand is climbing rapidly, supported by product innovation like green mortgages and transition finance that drive share gains; global sustainable debt issuance exceeded US$1 trillion in 2023, underscoring market scale. Verification, reporting and pricing sophistication require material investment; executed well, this becomes a growth engine feeding Westpac’s franchise.

- ESG demand

- Product innovation

- Verification & reporting

- Pricing sophistication

- Growth engine

New Zealand retail and business franchise (digital-first)

New Zealand retail and business franchise (digital-first) sits in Stars: strong brand recognition in NZ and a market still shifting to digital experiences; growth in 2024 outpaces some mature AU segments. Continue investing in mobile, payments, and small-business tools to capture digital share. Hold via service quality while scaling deposits and everyday banking.

- Tag: digital-first

- Tag: 2024 outperformance vs AU mature segments

- Tag: invest mobile, payments, SMB tools

- Tag: retain share through service, scale deposits

5M+ digital users, 18M PayIDs, SME +5% — invest in UX & fraud

Westpac Stars: 5.0M+ active digital customers (2024) and rising mobile-first usage; 18M+ PayIDs in AU underscores real-time rails reliance. SME credit growth ~5% YoY (2024) demands faster decisioning; sustainable lending taps >US$1T sustainable debt market (2023). NZ digital franchise outperformed AU mature segments in 2024—invest in UX, fraud controls and productisation to scale.

| Segment | 2024 metric | Key action |

|---|---|---|

| Digital consumers | 5.0M+ | UX, personalisation |

| PayID/NPP | 18M+ | Reliability, fraud |

| SME lending | 5% YoY | Auto decisioning |

| Sustainable finance | US$1T+ | Verification, pricing |

| NZ franchise | Outperform 2024 | Scale deposits |

What is included in the product

BCG Matrix analysis of Westpac’s units: Stars, Cash Cows, Question Marks and Dogs with investment, hold or divest guidance.

One-page BCG Matrix placing Westpac business units in quadrants, clarifies priorities and eases board decisions.

Cash Cows

Australian home lending (prime mortgages)

Westpac's Australian prime mortgage portfolio remains a large cash cow, with a roughly A$300bn book and about 15% share of owner-occupier lending in 2024 amid slower market growth of ~3% p.a.

Disciplined margin management and low arrears (around 0.3% 90+ days in 2024) generate strong cash; focus is on retention, simplified pricing and broker efficiency to defend share.

Strategy: milk efficiency gains and operational automation but avoid heavy investment in unproven, new-to-world features.

Everyday transaction accounts and term deposits

Everyday transaction accounts and term deposits form Westpac’s stable funding base, with customer deposits of A$395 billion at 30 September 2024 underpinning low-growth, sticky balances. Scale drives low unit funding costs and steady fee income from accounts and card fees, supporting net interest margins. Prioritise investment in reliability and simple features only, and divert surplus cash to higher-growth digital and business lending bets.

Corporate and institutional transaction banking

Corporate and institutional transaction banking holds high share with entrenched client relationships, but operates in a mature Australian market with low growth; sticky cash management and trade flows create persistent fee float that stabilises revenue.

Incremental investments in APIs and connectivity in 2024 improved straight-through processing and reduced operational costs, lifting efficiency and margins on transaction volumes.

As a reliable cash generator, this business funds Westpac’s risk buffers and targeted innovation spend, underpinning capital allocation across strategic initiatives.

Credit cards and personal loans (prime segments)

Credit cards and personal loans (prime segments)

Market growth is modest, roughly 3% in 2024 amid debit and BNPL pressure, while existing Westpac prime portfolios continue to generate solid net interest and fee income. Management should tighten credit risk, optimise rewards economics and keep acquisition costs efficient. Harvest cash flows; avoid chasing marginal volumes that dilute returns.- Net yield focus

- Tighten risk

- Efficient acquisition

BT superannuation and wealth platforms (core)

BT superannuation and wealth platforms (core) sit on a large installed base—supporting over A$80bn–A$100bn in FUA in 2024—so growth is modest while fee compression persists; scale still delivers positive margins and predictable cash flow that funds group priorities. Prioritise compliance, cost-to-serve cuts and platform efficiency over new flashy features to protect margins.

- Scale: high FUA, low growth

- Margin: fee compression real, scale offsets

- Capex: focus on compliance & efficiency

- Strategic role: reliable cash flow for group

A$300bn mortgage engine funds A$395bn deposits, A$90bn FUA, digital bets & capital buffers

Westpac cash cows: A$300bn owner-occupier mortgages (~15% market share, ~3% market growth in 2024) with 90+ days arrears ~0.3%. Customer deposits A$395bn (30 Sep 2024) provide low-cost funding. BT FUA ~A$90bn; cards/personal loans grow ~3% with tight risk focus. Surplus cash funds digital bets and capital buffers.

| Segment | 2024 metric | Role |

|---|---|---|

| Mortgages | A$300bn; 15% share; 0.3% arrears | Primary cash generator |

| Deposits | A$395bn | Stable funding |

| BT | A$90bn FUA | Fee cash flow |

What You’re Viewing Is Included

Westpac Bank BCG Matrix

The file you're previewing is the exact Westpac BCG Matrix report you'll receive after purchase—no watermarks, no demo text, just the finished document. It's formatted for clarity and action, ready to drop into board decks or strategy sessions. Once bought, the full file is yours to download, edit, print or share immediately. Built by strategy pros with market-backed inputs, there are no surprises—just work you can use straight away.

Actionable Strategy Starts Here

Curious where Westpac’s businesses sit—Stars, Cash Cows, Dogs or Question Marks? This quick peek hints at momentum and risk, but the full BCG Matrix gives you quadrant-by-quadrant clarity, tailored recommendations and ready-to-use visuals. Purchase the complete report for a downloadable Word analysis plus an Excel summary you can plug into board decks and planning sessions. Get it now and stop guessing where to invest your next dollar.

Stars

Digital consumer banking (mobile + online)

Westpac's digital consumer banking sees high daily usage and strong brand trust, with over 5 million active digital customers reported in 2024 and growing adoption as Australia shifts fast to mobile-first banking. Continuous investment in UX, features and security is required to stay ahead, keeping pace with real-time payments and NPP-driven instant transfers. Ongoing personalisation and spend secures market share now and lets this star mature into a cash cow later.

Real-time payments and data-led services

Westpac's exposure to real-time rails — NPP and PayID — matters: over 18 million PayIDs in Australia by 2024 and rapidly rising adoption in NZ. Delivering richer data at scale requires heavy investment in reliability, fraud controls and partner integrations. Monetisation leans on value-added services (data analytics, liquidity tools), not interchange fees. Winning here anchors account primacy and cross-sell economics.

SME digital lending and onboarding

SME digital lending and onboarding at Westpac sits in a high-growth quadrant as SME demand rebounded in 2024 with Australian business credit growth around 5% year-on-year and online applications rising sharply. The space is crowded, so faster decisioning and advanced risk models are critical to win share. Keep acquisition costs tight while improving straight-through processing to lift lifetime value. Scale now to lock in cohort retention and cross-sell revenue.

Sustainable finance and green lending

Sustainable finance and green lending sit in Stars: corporate and retail ESG lending demand is climbing rapidly, supported by product innovation like green mortgages and transition finance that drive share gains; global sustainable debt issuance exceeded US$1 trillion in 2023, underscoring market scale. Verification, reporting and pricing sophistication require material investment; executed well, this becomes a growth engine feeding Westpac’s franchise.

- ESG demand

- Product innovation

- Verification & reporting

- Pricing sophistication

- Growth engine

New Zealand retail and business franchise (digital-first)

New Zealand retail and business franchise (digital-first) sits in Stars: strong brand recognition in NZ and a market still shifting to digital experiences; growth in 2024 outpaces some mature AU segments. Continue investing in mobile, payments, and small-business tools to capture digital share. Hold via service quality while scaling deposits and everyday banking.

- Tag: digital-first

- Tag: 2024 outperformance vs AU mature segments

- Tag: invest mobile, payments, SMB tools

- Tag: retain share through service, scale deposits

5M+ digital users, 18M PayIDs, SME +5% — invest in UX & fraud

Westpac Stars: 5.0M+ active digital customers (2024) and rising mobile-first usage; 18M+ PayIDs in AU underscores real-time rails reliance. SME credit growth ~5% YoY (2024) demands faster decisioning; sustainable lending taps >US$1T sustainable debt market (2023). NZ digital franchise outperformed AU mature segments in 2024—invest in UX, fraud controls and productisation to scale.

| Segment | 2024 metric | Key action |

|---|---|---|

| Digital consumers | 5.0M+ | UX, personalisation |

| PayID/NPP | 18M+ | Reliability, fraud |

| SME lending | 5% YoY | Auto decisioning |

| Sustainable finance | US$1T+ | Verification, pricing |

| NZ franchise | Outperform 2024 | Scale deposits |

What is included in the product

BCG Matrix analysis of Westpac’s units: Stars, Cash Cows, Question Marks and Dogs with investment, hold or divest guidance.

One-page BCG Matrix placing Westpac business units in quadrants, clarifies priorities and eases board decisions.

Cash Cows

Australian home lending (prime mortgages)

Westpac's Australian prime mortgage portfolio remains a large cash cow, with a roughly A$300bn book and about 15% share of owner-occupier lending in 2024 amid slower market growth of ~3% p.a.

Disciplined margin management and low arrears (around 0.3% 90+ days in 2024) generate strong cash; focus is on retention, simplified pricing and broker efficiency to defend share.

Strategy: milk efficiency gains and operational automation but avoid heavy investment in unproven, new-to-world features.

Everyday transaction accounts and term deposits

Everyday transaction accounts and term deposits form Westpac’s stable funding base, with customer deposits of A$395 billion at 30 September 2024 underpinning low-growth, sticky balances. Scale drives low unit funding costs and steady fee income from accounts and card fees, supporting net interest margins. Prioritise investment in reliability and simple features only, and divert surplus cash to higher-growth digital and business lending bets.

Corporate and institutional transaction banking

Corporate and institutional transaction banking holds high share with entrenched client relationships, but operates in a mature Australian market with low growth; sticky cash management and trade flows create persistent fee float that stabilises revenue.

Incremental investments in APIs and connectivity in 2024 improved straight-through processing and reduced operational costs, lifting efficiency and margins on transaction volumes.

As a reliable cash generator, this business funds Westpac’s risk buffers and targeted innovation spend, underpinning capital allocation across strategic initiatives.

Credit cards and personal loans (prime segments)

Credit cards and personal loans (prime segments)

Market growth is modest, roughly 3% in 2024 amid debit and BNPL pressure, while existing Westpac prime portfolios continue to generate solid net interest and fee income. Management should tighten credit risk, optimise rewards economics and keep acquisition costs efficient. Harvest cash flows; avoid chasing marginal volumes that dilute returns.- Net yield focus

- Tighten risk

- Efficient acquisition

BT superannuation and wealth platforms (core)

BT superannuation and wealth platforms (core) sit on a large installed base—supporting over A$80bn–A$100bn in FUA in 2024—so growth is modest while fee compression persists; scale still delivers positive margins and predictable cash flow that funds group priorities. Prioritise compliance, cost-to-serve cuts and platform efficiency over new flashy features to protect margins.

- Scale: high FUA, low growth

- Margin: fee compression real, scale offsets

- Capex: focus on compliance & efficiency

- Strategic role: reliable cash flow for group

A$300bn mortgage engine funds A$395bn deposits, A$90bn FUA, digital bets & capital buffers

Westpac cash cows: A$300bn owner-occupier mortgages (~15% market share, ~3% market growth in 2024) with 90+ days arrears ~0.3%. Customer deposits A$395bn (30 Sep 2024) provide low-cost funding. BT FUA ~A$90bn; cards/personal loans grow ~3% with tight risk focus. Surplus cash funds digital bets and capital buffers.

| Segment | 2024 metric | Role |

|---|---|---|

| Mortgages | A$300bn; 15% share; 0.3% arrears | Primary cash generator |

| Deposits | A$395bn | Stable funding |

| BT | A$90bn FUA | Fee cash flow |

What You’re Viewing Is Included

Westpac Bank BCG Matrix

The file you're previewing is the exact Westpac BCG Matrix report you'll receive after purchase—no watermarks, no demo text, just the finished document. It's formatted for clarity and action, ready to drop into board decks or strategy sessions. Once bought, the full file is yours to download, edit, print or share immediately. Built by strategy pros with market-backed inputs, there are no surprises—just work you can use straight away.

Description

Actionable Strategy Starts Here

Curious where Westpac’s businesses sit—Stars, Cash Cows, Dogs or Question Marks? This quick peek hints at momentum and risk, but the full BCG Matrix gives you quadrant-by-quadrant clarity, tailored recommendations and ready-to-use visuals. Purchase the complete report for a downloadable Word analysis plus an Excel summary you can plug into board decks and planning sessions. Get it now and stop guessing where to invest your next dollar.

Stars

Digital consumer banking (mobile + online)

Westpac's digital consumer banking sees high daily usage and strong brand trust, with over 5 million active digital customers reported in 2024 and growing adoption as Australia shifts fast to mobile-first banking. Continuous investment in UX, features and security is required to stay ahead, keeping pace with real-time payments and NPP-driven instant transfers. Ongoing personalisation and spend secures market share now and lets this star mature into a cash cow later.

Real-time payments and data-led services

Westpac's exposure to real-time rails — NPP and PayID — matters: over 18 million PayIDs in Australia by 2024 and rapidly rising adoption in NZ. Delivering richer data at scale requires heavy investment in reliability, fraud controls and partner integrations. Monetisation leans on value-added services (data analytics, liquidity tools), not interchange fees. Winning here anchors account primacy and cross-sell economics.

SME digital lending and onboarding

SME digital lending and onboarding at Westpac sits in a high-growth quadrant as SME demand rebounded in 2024 with Australian business credit growth around 5% year-on-year and online applications rising sharply. The space is crowded, so faster decisioning and advanced risk models are critical to win share. Keep acquisition costs tight while improving straight-through processing to lift lifetime value. Scale now to lock in cohort retention and cross-sell revenue.

Sustainable finance and green lending

Sustainable finance and green lending sit in Stars: corporate and retail ESG lending demand is climbing rapidly, supported by product innovation like green mortgages and transition finance that drive share gains; global sustainable debt issuance exceeded US$1 trillion in 2023, underscoring market scale. Verification, reporting and pricing sophistication require material investment; executed well, this becomes a growth engine feeding Westpac’s franchise.

- ESG demand

- Product innovation

- Verification & reporting

- Pricing sophistication

- Growth engine

New Zealand retail and business franchise (digital-first)

New Zealand retail and business franchise (digital-first) sits in Stars: strong brand recognition in NZ and a market still shifting to digital experiences; growth in 2024 outpaces some mature AU segments. Continue investing in mobile, payments, and small-business tools to capture digital share. Hold via service quality while scaling deposits and everyday banking.

- Tag: digital-first

- Tag: 2024 outperformance vs AU mature segments

- Tag: invest mobile, payments, SMB tools

- Tag: retain share through service, scale deposits

5M+ digital users, 18M PayIDs, SME +5% — invest in UX & fraud

Westpac Stars: 5.0M+ active digital customers (2024) and rising mobile-first usage; 18M+ PayIDs in AU underscores real-time rails reliance. SME credit growth ~5% YoY (2024) demands faster decisioning; sustainable lending taps >US$1T sustainable debt market (2023). NZ digital franchise outperformed AU mature segments in 2024—invest in UX, fraud controls and productisation to scale.

| Segment | 2024 metric | Key action |

|---|---|---|

| Digital consumers | 5.0M+ | UX, personalisation |

| PayID/NPP | 18M+ | Reliability, fraud |

| SME lending | 5% YoY | Auto decisioning |

| Sustainable finance | US$1T+ | Verification, pricing |

| NZ franchise | Outperform 2024 | Scale deposits |

What is included in the product

BCG Matrix analysis of Westpac’s units: Stars, Cash Cows, Question Marks and Dogs with investment, hold or divest guidance.

One-page BCG Matrix placing Westpac business units in quadrants, clarifies priorities and eases board decisions.

Cash Cows

Australian home lending (prime mortgages)

Westpac's Australian prime mortgage portfolio remains a large cash cow, with a roughly A$300bn book and about 15% share of owner-occupier lending in 2024 amid slower market growth of ~3% p.a.

Disciplined margin management and low arrears (around 0.3% 90+ days in 2024) generate strong cash; focus is on retention, simplified pricing and broker efficiency to defend share.

Strategy: milk efficiency gains and operational automation but avoid heavy investment in unproven, new-to-world features.

Everyday transaction accounts and term deposits

Everyday transaction accounts and term deposits form Westpac’s stable funding base, with customer deposits of A$395 billion at 30 September 2024 underpinning low-growth, sticky balances. Scale drives low unit funding costs and steady fee income from accounts and card fees, supporting net interest margins. Prioritise investment in reliability and simple features only, and divert surplus cash to higher-growth digital and business lending bets.

Corporate and institutional transaction banking

Corporate and institutional transaction banking holds high share with entrenched client relationships, but operates in a mature Australian market with low growth; sticky cash management and trade flows create persistent fee float that stabilises revenue.

Incremental investments in APIs and connectivity in 2024 improved straight-through processing and reduced operational costs, lifting efficiency and margins on transaction volumes.

As a reliable cash generator, this business funds Westpac’s risk buffers and targeted innovation spend, underpinning capital allocation across strategic initiatives.

Credit cards and personal loans (prime segments)

Credit cards and personal loans (prime segments)

Market growth is modest, roughly 3% in 2024 amid debit and BNPL pressure, while existing Westpac prime portfolios continue to generate solid net interest and fee income. Management should tighten credit risk, optimise rewards economics and keep acquisition costs efficient. Harvest cash flows; avoid chasing marginal volumes that dilute returns.- Net yield focus

- Tighten risk

- Efficient acquisition

BT superannuation and wealth platforms (core)

BT superannuation and wealth platforms (core) sit on a large installed base—supporting over A$80bn–A$100bn in FUA in 2024—so growth is modest while fee compression persists; scale still delivers positive margins and predictable cash flow that funds group priorities. Prioritise compliance, cost-to-serve cuts and platform efficiency over new flashy features to protect margins.

- Scale: high FUA, low growth

- Margin: fee compression real, scale offsets

- Capex: focus on compliance & efficiency

- Strategic role: reliable cash flow for group

A$300bn mortgage engine funds A$395bn deposits, A$90bn FUA, digital bets & capital buffers

Westpac cash cows: A$300bn owner-occupier mortgages (~15% market share, ~3% market growth in 2024) with 90+ days arrears ~0.3%. Customer deposits A$395bn (30 Sep 2024) provide low-cost funding. BT FUA ~A$90bn; cards/personal loans grow ~3% with tight risk focus. Surplus cash funds digital bets and capital buffers.

| Segment | 2024 metric | Role |

|---|---|---|

| Mortgages | A$300bn; 15% share; 0.3% arrears | Primary cash generator |

| Deposits | A$395bn | Stable funding |

| BT | A$90bn FUA | Fee cash flow |

What You’re Viewing Is Included

Westpac Bank BCG Matrix

The file you're previewing is the exact Westpac BCG Matrix report you'll receive after purchase—no watermarks, no demo text, just the finished document. It's formatted for clarity and action, ready to drop into board decks or strategy sessions. Once bought, the full file is yours to download, edit, print or share immediately. Built by strategy pros with market-backed inputs, there are no surprises—just work you can use straight away.