Weyerhaeuser PESTLE Analysis

Your Competitive Advantage Starts with This Report

Discover how political shifts, economic cycles, and environmental regulations shape Weyerhaeuser’s timber and real estate businesses in our concise PESTLE overview; it highlights risks and opportunities for investors and strategists. Buy the full analysis to access detailed, actionable insights and ready-to-use charts for decision-making.

Political factors

US-Canada forestry and trade policy

US-Canada softwood lumber disputes, including the expiry of the Softwood Lumber Agreement in 2015, drive tariffs, quotas and export access that materially shape realized prices. Policy shifts can widen price spreads and volatility, affecting margin cycles for producers. Weyerhaeuser hedges exposure through product mix and contract structures and factors ongoing diplomacy into planning horizons and capital allocation.

Federal and state forest management priorities

Federal and state budgeting for wildfire mitigation, thinning and reforestation directly raises Weyerhaeuser operating costs as wildfire response now consumes over 50% of USFS discretionary spending, pressuring matching and program funds. Expanded state incentives for fuel reduction in 2024 unlocked commercial thinning and logging opportunities that lower landscape risk and liability. Changes in state best-management practices and political leadership shifts can accelerate or delay program funding and harvesting schedules, affecting cash flow timing.

Rural development and infrastructure funding

Road, rail and port investments from the Bipartisan Infrastructure Law (roughly $110B for roads/bridges, $66B for rail and $17B for ports) directly lower Weyerhaeuser delivered log costs and expand market reach by shortening haul distances and enabling larger vessels/railcars. Public funding cycles and multi-year grant timelines can compress or expand logistics bottlenecks, driving volatility in transit lead times. Improved infrastructure raises mill utilization and reduces freight exposure, while policy or permitting delays increase working capital tied up in transit and inventory.

Tribal and local government relations

Collaborations and permitting with tribal nations and counties materially affect access and timelines for Weyerhaeuser, which manages roughly 11 million acres of timberland in the US; negotiated permits can shorten project timelines while disputes cause stoppages and legal costs. Shared stewardship agreements have improved social license to operate in several regions, and unresolved conflicts risk regulatory delays and litigation expenses. Constructive engagement with tribes and local governments underpins long-term harvesting stability and supply predictability.

- Permitting impact: access and timelines

- Shared stewardship: stronger social license

- Disputes: delays + legal costs

- Engagement: long-term harvesting stability

Energy and biomass policy incentives

Renewable standards and biomass credit programs materially affect Weyerhaeuser by increasing byproduct monetization; the company reported roughly $8.1 billion in 2024 net sales, so incremental energy revenue from pellets and black liquor can meaningfully boost margins. Supportive state RPS and biomass credits improve mill economics via cogeneration, while policy retrenchment can cut expected IRR on energy capex by several percentage points. Clear federal and state policy signals through 2024–25 are driving selective investment in bio-based initiatives.

- RPS influence: biomass eligible in ~29 states

- Cogeneration impact: can offset 20–30% of mill energy costs

- Capex risk: policy rollback may reduce IRR by 3–6 pts

- Revenue context: Weyerhaeuser ~8.1B 2024 net sales

Softwood disputes, wildfires and tariffs squeeze margins; infrastructure trims log costs

Softwood disputes, tariffs and export rules drive price volatility and margins; Weyerhaeuser hedges via mix/contracting. Wildfire response now >50% of USFS discretionary spend, raising operating and mitigation costs. Bipartisan Infrastructure (roads $110B, rail $66B, ports $17B) lowers delivered log costs; Weyerhaeuser manages ~11M acres and reported $8.1B 2024 sales.

| Metric | Value |

|---|---|

| USFS wildfire share | >50% |

| Infrastructure funding | Roads $110B / Rail $66B / Ports $17B |

| Timberland | ~11M acres |

| 2024 net sales | $8.1B |

What is included in the product

Provides a focused PESTLE analysis showing how political, economic, social, technological, environmental, and legal forces uniquely impact Weyerhaeuser’s timber, wood products, and land-management operations, with data-backed trends and forward-looking insights to inform strategy, risk mitigation, and investor-ready reporting.

A concise, visually segmented Weyerhaeuser PESTLE summary that relieves preparation pain by providing an editable, easy-to-drop-into-presentations brief for quick team alignment and strategy discussions on external risks and market positioning.

Economic factors

Housing starts and repair/remodel demand

U.S. housing starts averaged about 1.45 million annualized in 2024, with single-family housing roughly a 66% share, directly driving Weyerhaeuser lumber and panel volumes and pricing; single-family favors dimensional lumber while multi-family shifts demand toward panels and engineered products. Strong DIY spending—around $450 billion in 2024—buffers cycles differently than pro channels, and demand elasticity directly impacts mill run rates and inventory strategies.

Interest rates and mortgage affordability

Higher interest rates (federal funds around 5.25–5.50% through mid‑2025) and a 30‑year mortgage averaging about 7% in 2024 compressed affordability and delayed new home starts, weighing on demand for lumber. Rate cuts typically spark restocking and price rebounds. Sensitivity differs by region and grade, and Fed signals drive Weyerhaeuser production and inventory planning.

Commodity price volatility

Lumber and OSB prices have swung wildly—softwood lumber futures ranged roughly from $300/mbf in 2023 lows to over $1,200/mbf at 2021 peaks—so price spikes boost Weyerhaeuser’s cash flow but strain homebuilder customers. Downcycles compress margins and test working-capital discipline and cost positions. Weyerhaeuser uses hedging and index-linked contracts to smooth earnings volatility.

Exchange rates (USD/CAD)

Exchange-rate moves (USD/CAD ~1.36 in July 2025) affect Weyerhaeuser's cross-border competitiveness and input costs: a strong USD pressures lumber exports while lowering imported equipment and capital costs. CAD volatility alters Canadian timber valuations and operating cash flow; natural hedges from North American sales and USD-denominated contracts partially offset volatility.

- USD/CAD ~1.36 (Jul 2025)

- Strong USD: export pressure, cheaper imports

- CAD swings: timber valuation & cash-flow impact

- Natural hedges: partial offset

Labor, fuel, and logistics costs

Truck availability, diesel prices, and rail service materially shape Weyerhaeuser’s delivered costs; U.S. diesel averaged about $3.79/gal in 2024 (EIA) while rail car cycle times rose roughly 5% y/y in 2024, increasing dwell costs. Tight labor markets lifted mill and forestry wages ~6% in 2024, pressuring margins. Efficiency gains, modal shifts to rail, and contracting strategies mitigate inflation and service risk.

- Truck availability → spot rate volatility, capacity risk

- Diesel ~$3.79/gal (2024) → direct fuel cost impact

- Rail delays +5% cycle time (2024) → higher delivered cost

- Wages +~6% (2024) → labor inflation; contracts & modal shifts mitigate

Softwood disputes, wildfires and tariffs squeeze margins; infrastructure trims log costs

Housing starts ~1.45M (2024) drive lumber/panel demand; DIY ~$450B cushions cycles. Fed funds 5.25–5.50% and 30‑yr ~7% (2024) constrain affordability; rate cuts spur restocking. Lumber/OSB price volatility and hedging shape margins; USD/CAD ~1.36 (Jul 2025) and diesel ~$3.79/gal (2024) affect costs and export competitiveness.

| Metric | Value |

|---|---|

| Housing starts (2024) | ~1.45M |

| Fed funds / 30‑yr (2024/25) | 5.25–5.50% / ~7% |

| USD/CAD (Jul 2025) | ~1.36 |

What You See Is What You Get

Weyerhaeuser PESTLE Analysis

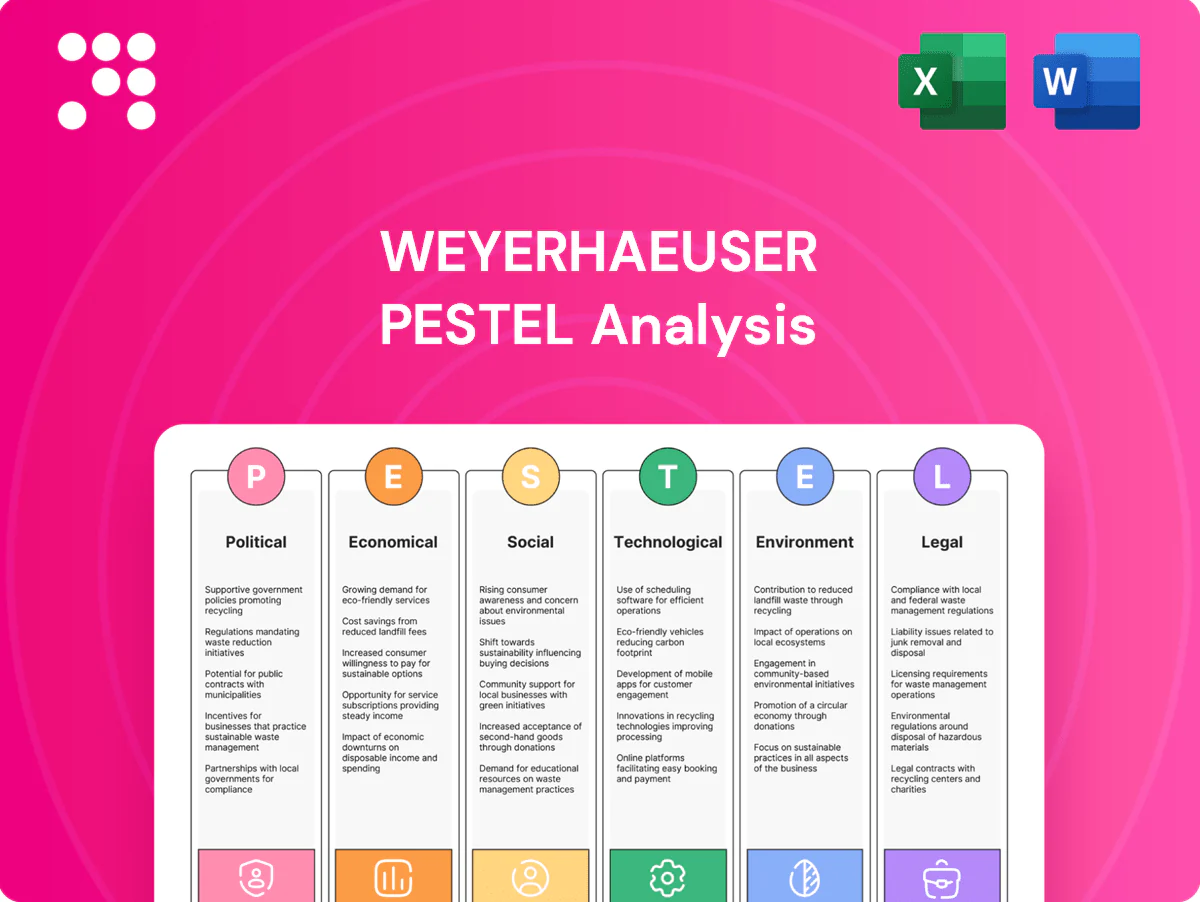

The Weyerhaeuser PESTLE Analysis provides a concise, professionally structured review of political, economic, social, technological, legal, and environmental factors affecting the company. The preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use. No placeholders or teasers; the content, layout, and structure visible are what you’ll download instantly.

Your Competitive Advantage Starts with This Report

Discover how political shifts, economic cycles, and environmental regulations shape Weyerhaeuser’s timber and real estate businesses in our concise PESTLE overview; it highlights risks and opportunities for investors and strategists. Buy the full analysis to access detailed, actionable insights and ready-to-use charts for decision-making.

Political factors

US-Canada forestry and trade policy

US-Canada softwood lumber disputes, including the expiry of the Softwood Lumber Agreement in 2015, drive tariffs, quotas and export access that materially shape realized prices. Policy shifts can widen price spreads and volatility, affecting margin cycles for producers. Weyerhaeuser hedges exposure through product mix and contract structures and factors ongoing diplomacy into planning horizons and capital allocation.

Federal and state forest management priorities

Federal and state budgeting for wildfire mitigation, thinning and reforestation directly raises Weyerhaeuser operating costs as wildfire response now consumes over 50% of USFS discretionary spending, pressuring matching and program funds. Expanded state incentives for fuel reduction in 2024 unlocked commercial thinning and logging opportunities that lower landscape risk and liability. Changes in state best-management practices and political leadership shifts can accelerate or delay program funding and harvesting schedules, affecting cash flow timing.

Rural development and infrastructure funding

Road, rail and port investments from the Bipartisan Infrastructure Law (roughly $110B for roads/bridges, $66B for rail and $17B for ports) directly lower Weyerhaeuser delivered log costs and expand market reach by shortening haul distances and enabling larger vessels/railcars. Public funding cycles and multi-year grant timelines can compress or expand logistics bottlenecks, driving volatility in transit lead times. Improved infrastructure raises mill utilization and reduces freight exposure, while policy or permitting delays increase working capital tied up in transit and inventory.

Tribal and local government relations

Collaborations and permitting with tribal nations and counties materially affect access and timelines for Weyerhaeuser, which manages roughly 11 million acres of timberland in the US; negotiated permits can shorten project timelines while disputes cause stoppages and legal costs. Shared stewardship agreements have improved social license to operate in several regions, and unresolved conflicts risk regulatory delays and litigation expenses. Constructive engagement with tribes and local governments underpins long-term harvesting stability and supply predictability.

- Permitting impact: access and timelines

- Shared stewardship: stronger social license

- Disputes: delays + legal costs

- Engagement: long-term harvesting stability

Energy and biomass policy incentives

Renewable standards and biomass credit programs materially affect Weyerhaeuser by increasing byproduct monetization; the company reported roughly $8.1 billion in 2024 net sales, so incremental energy revenue from pellets and black liquor can meaningfully boost margins. Supportive state RPS and biomass credits improve mill economics via cogeneration, while policy retrenchment can cut expected IRR on energy capex by several percentage points. Clear federal and state policy signals through 2024–25 are driving selective investment in bio-based initiatives.

- RPS influence: biomass eligible in ~29 states

- Cogeneration impact: can offset 20–30% of mill energy costs

- Capex risk: policy rollback may reduce IRR by 3–6 pts

- Revenue context: Weyerhaeuser ~8.1B 2024 net sales

Softwood disputes, wildfires and tariffs squeeze margins; infrastructure trims log costs

Softwood disputes, tariffs and export rules drive price volatility and margins; Weyerhaeuser hedges via mix/contracting. Wildfire response now >50% of USFS discretionary spend, raising operating and mitigation costs. Bipartisan Infrastructure (roads $110B, rail $66B, ports $17B) lowers delivered log costs; Weyerhaeuser manages ~11M acres and reported $8.1B 2024 sales.

| Metric | Value |

|---|---|

| USFS wildfire share | >50% |

| Infrastructure funding | Roads $110B / Rail $66B / Ports $17B |

| Timberland | ~11M acres |

| 2024 net sales | $8.1B |

What is included in the product

Provides a focused PESTLE analysis showing how political, economic, social, technological, environmental, and legal forces uniquely impact Weyerhaeuser’s timber, wood products, and land-management operations, with data-backed trends and forward-looking insights to inform strategy, risk mitigation, and investor-ready reporting.

A concise, visually segmented Weyerhaeuser PESTLE summary that relieves preparation pain by providing an editable, easy-to-drop-into-presentations brief for quick team alignment and strategy discussions on external risks and market positioning.

Economic factors

Housing starts and repair/remodel demand

U.S. housing starts averaged about 1.45 million annualized in 2024, with single-family housing roughly a 66% share, directly driving Weyerhaeuser lumber and panel volumes and pricing; single-family favors dimensional lumber while multi-family shifts demand toward panels and engineered products. Strong DIY spending—around $450 billion in 2024—buffers cycles differently than pro channels, and demand elasticity directly impacts mill run rates and inventory strategies.

Interest rates and mortgage affordability

Higher interest rates (federal funds around 5.25–5.50% through mid‑2025) and a 30‑year mortgage averaging about 7% in 2024 compressed affordability and delayed new home starts, weighing on demand for lumber. Rate cuts typically spark restocking and price rebounds. Sensitivity differs by region and grade, and Fed signals drive Weyerhaeuser production and inventory planning.

Commodity price volatility

Lumber and OSB prices have swung wildly—softwood lumber futures ranged roughly from $300/mbf in 2023 lows to over $1,200/mbf at 2021 peaks—so price spikes boost Weyerhaeuser’s cash flow but strain homebuilder customers. Downcycles compress margins and test working-capital discipline and cost positions. Weyerhaeuser uses hedging and index-linked contracts to smooth earnings volatility.

Exchange rates (USD/CAD)

Exchange-rate moves (USD/CAD ~1.36 in July 2025) affect Weyerhaeuser's cross-border competitiveness and input costs: a strong USD pressures lumber exports while lowering imported equipment and capital costs. CAD volatility alters Canadian timber valuations and operating cash flow; natural hedges from North American sales and USD-denominated contracts partially offset volatility.

- USD/CAD ~1.36 (Jul 2025)

- Strong USD: export pressure, cheaper imports

- CAD swings: timber valuation & cash-flow impact

- Natural hedges: partial offset

Labor, fuel, and logistics costs

Truck availability, diesel prices, and rail service materially shape Weyerhaeuser’s delivered costs; U.S. diesel averaged about $3.79/gal in 2024 (EIA) while rail car cycle times rose roughly 5% y/y in 2024, increasing dwell costs. Tight labor markets lifted mill and forestry wages ~6% in 2024, pressuring margins. Efficiency gains, modal shifts to rail, and contracting strategies mitigate inflation and service risk.

- Truck availability → spot rate volatility, capacity risk

- Diesel ~$3.79/gal (2024) → direct fuel cost impact

- Rail delays +5% cycle time (2024) → higher delivered cost

- Wages +~6% (2024) → labor inflation; contracts & modal shifts mitigate

Softwood disputes, wildfires and tariffs squeeze margins; infrastructure trims log costs

Housing starts ~1.45M (2024) drive lumber/panel demand; DIY ~$450B cushions cycles. Fed funds 5.25–5.50% and 30‑yr ~7% (2024) constrain affordability; rate cuts spur restocking. Lumber/OSB price volatility and hedging shape margins; USD/CAD ~1.36 (Jul 2025) and diesel ~$3.79/gal (2024) affect costs and export competitiveness.

| Metric | Value |

|---|---|

| Housing starts (2024) | ~1.45M |

| Fed funds / 30‑yr (2024/25) | 5.25–5.50% / ~7% |

| USD/CAD (Jul 2025) | ~1.36 |

What You See Is What You Get

Weyerhaeuser PESTLE Analysis

The Weyerhaeuser PESTLE Analysis provides a concise, professionally structured review of political, economic, social, technological, legal, and environmental factors affecting the company. The preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use. No placeholders or teasers; the content, layout, and structure visible are what you’ll download instantly.

Description

Your Competitive Advantage Starts with This Report

Discover how political shifts, economic cycles, and environmental regulations shape Weyerhaeuser’s timber and real estate businesses in our concise PESTLE overview; it highlights risks and opportunities for investors and strategists. Buy the full analysis to access detailed, actionable insights and ready-to-use charts for decision-making.

Political factors

US-Canada forestry and trade policy

US-Canada softwood lumber disputes, including the expiry of the Softwood Lumber Agreement in 2015, drive tariffs, quotas and export access that materially shape realized prices. Policy shifts can widen price spreads and volatility, affecting margin cycles for producers. Weyerhaeuser hedges exposure through product mix and contract structures and factors ongoing diplomacy into planning horizons and capital allocation.

Federal and state forest management priorities

Federal and state budgeting for wildfire mitigation, thinning and reforestation directly raises Weyerhaeuser operating costs as wildfire response now consumes over 50% of USFS discretionary spending, pressuring matching and program funds. Expanded state incentives for fuel reduction in 2024 unlocked commercial thinning and logging opportunities that lower landscape risk and liability. Changes in state best-management practices and political leadership shifts can accelerate or delay program funding and harvesting schedules, affecting cash flow timing.

Rural development and infrastructure funding

Road, rail and port investments from the Bipartisan Infrastructure Law (roughly $110B for roads/bridges, $66B for rail and $17B for ports) directly lower Weyerhaeuser delivered log costs and expand market reach by shortening haul distances and enabling larger vessels/railcars. Public funding cycles and multi-year grant timelines can compress or expand logistics bottlenecks, driving volatility in transit lead times. Improved infrastructure raises mill utilization and reduces freight exposure, while policy or permitting delays increase working capital tied up in transit and inventory.

Tribal and local government relations

Collaborations and permitting with tribal nations and counties materially affect access and timelines for Weyerhaeuser, which manages roughly 11 million acres of timberland in the US; negotiated permits can shorten project timelines while disputes cause stoppages and legal costs. Shared stewardship agreements have improved social license to operate in several regions, and unresolved conflicts risk regulatory delays and litigation expenses. Constructive engagement with tribes and local governments underpins long-term harvesting stability and supply predictability.

- Permitting impact: access and timelines

- Shared stewardship: stronger social license

- Disputes: delays + legal costs

- Engagement: long-term harvesting stability

Energy and biomass policy incentives

Renewable standards and biomass credit programs materially affect Weyerhaeuser by increasing byproduct monetization; the company reported roughly $8.1 billion in 2024 net sales, so incremental energy revenue from pellets and black liquor can meaningfully boost margins. Supportive state RPS and biomass credits improve mill economics via cogeneration, while policy retrenchment can cut expected IRR on energy capex by several percentage points. Clear federal and state policy signals through 2024–25 are driving selective investment in bio-based initiatives.

- RPS influence: biomass eligible in ~29 states

- Cogeneration impact: can offset 20–30% of mill energy costs

- Capex risk: policy rollback may reduce IRR by 3–6 pts

- Revenue context: Weyerhaeuser ~8.1B 2024 net sales

Softwood disputes, wildfires and tariffs squeeze margins; infrastructure trims log costs

Softwood disputes, tariffs and export rules drive price volatility and margins; Weyerhaeuser hedges via mix/contracting. Wildfire response now >50% of USFS discretionary spend, raising operating and mitigation costs. Bipartisan Infrastructure (roads $110B, rail $66B, ports $17B) lowers delivered log costs; Weyerhaeuser manages ~11M acres and reported $8.1B 2024 sales.

| Metric | Value |

|---|---|

| USFS wildfire share | >50% |

| Infrastructure funding | Roads $110B / Rail $66B / Ports $17B |

| Timberland | ~11M acres |

| 2024 net sales | $8.1B |

What is included in the product

Provides a focused PESTLE analysis showing how political, economic, social, technological, environmental, and legal forces uniquely impact Weyerhaeuser’s timber, wood products, and land-management operations, with data-backed trends and forward-looking insights to inform strategy, risk mitigation, and investor-ready reporting.

A concise, visually segmented Weyerhaeuser PESTLE summary that relieves preparation pain by providing an editable, easy-to-drop-into-presentations brief for quick team alignment and strategy discussions on external risks and market positioning.

Economic factors

Housing starts and repair/remodel demand

U.S. housing starts averaged about 1.45 million annualized in 2024, with single-family housing roughly a 66% share, directly driving Weyerhaeuser lumber and panel volumes and pricing; single-family favors dimensional lumber while multi-family shifts demand toward panels and engineered products. Strong DIY spending—around $450 billion in 2024—buffers cycles differently than pro channels, and demand elasticity directly impacts mill run rates and inventory strategies.

Interest rates and mortgage affordability

Higher interest rates (federal funds around 5.25–5.50% through mid‑2025) and a 30‑year mortgage averaging about 7% in 2024 compressed affordability and delayed new home starts, weighing on demand for lumber. Rate cuts typically spark restocking and price rebounds. Sensitivity differs by region and grade, and Fed signals drive Weyerhaeuser production and inventory planning.

Commodity price volatility

Lumber and OSB prices have swung wildly—softwood lumber futures ranged roughly from $300/mbf in 2023 lows to over $1,200/mbf at 2021 peaks—so price spikes boost Weyerhaeuser’s cash flow but strain homebuilder customers. Downcycles compress margins and test working-capital discipline and cost positions. Weyerhaeuser uses hedging and index-linked contracts to smooth earnings volatility.

Exchange rates (USD/CAD)

Exchange-rate moves (USD/CAD ~1.36 in July 2025) affect Weyerhaeuser's cross-border competitiveness and input costs: a strong USD pressures lumber exports while lowering imported equipment and capital costs. CAD volatility alters Canadian timber valuations and operating cash flow; natural hedges from North American sales and USD-denominated contracts partially offset volatility.

- USD/CAD ~1.36 (Jul 2025)

- Strong USD: export pressure, cheaper imports

- CAD swings: timber valuation & cash-flow impact

- Natural hedges: partial offset

Labor, fuel, and logistics costs

Truck availability, diesel prices, and rail service materially shape Weyerhaeuser’s delivered costs; U.S. diesel averaged about $3.79/gal in 2024 (EIA) while rail car cycle times rose roughly 5% y/y in 2024, increasing dwell costs. Tight labor markets lifted mill and forestry wages ~6% in 2024, pressuring margins. Efficiency gains, modal shifts to rail, and contracting strategies mitigate inflation and service risk.

- Truck availability → spot rate volatility, capacity risk

- Diesel ~$3.79/gal (2024) → direct fuel cost impact

- Rail delays +5% cycle time (2024) → higher delivered cost

- Wages +~6% (2024) → labor inflation; contracts & modal shifts mitigate

Softwood disputes, wildfires and tariffs squeeze margins; infrastructure trims log costs

Housing starts ~1.45M (2024) drive lumber/panel demand; DIY ~$450B cushions cycles. Fed funds 5.25–5.50% and 30‑yr ~7% (2024) constrain affordability; rate cuts spur restocking. Lumber/OSB price volatility and hedging shape margins; USD/CAD ~1.36 (Jul 2025) and diesel ~$3.79/gal (2024) affect costs and export competitiveness.

| Metric | Value |

|---|---|

| Housing starts (2024) | ~1.45M |

| Fed funds / 30‑yr (2024/25) | 5.25–5.50% / ~7% |

| USD/CAD (Jul 2025) | ~1.36 |

What You See Is What You Get

Weyerhaeuser PESTLE Analysis

The Weyerhaeuser PESTLE Analysis provides a concise, professionally structured review of political, economic, social, technological, legal, and environmental factors affecting the company. The preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use. No placeholders or teasers; the content, layout, and structure visible are what you’ll download instantly.