Wharf (Holdings) Boston Consulting Group Matrix

Unlock Strategic Clarity

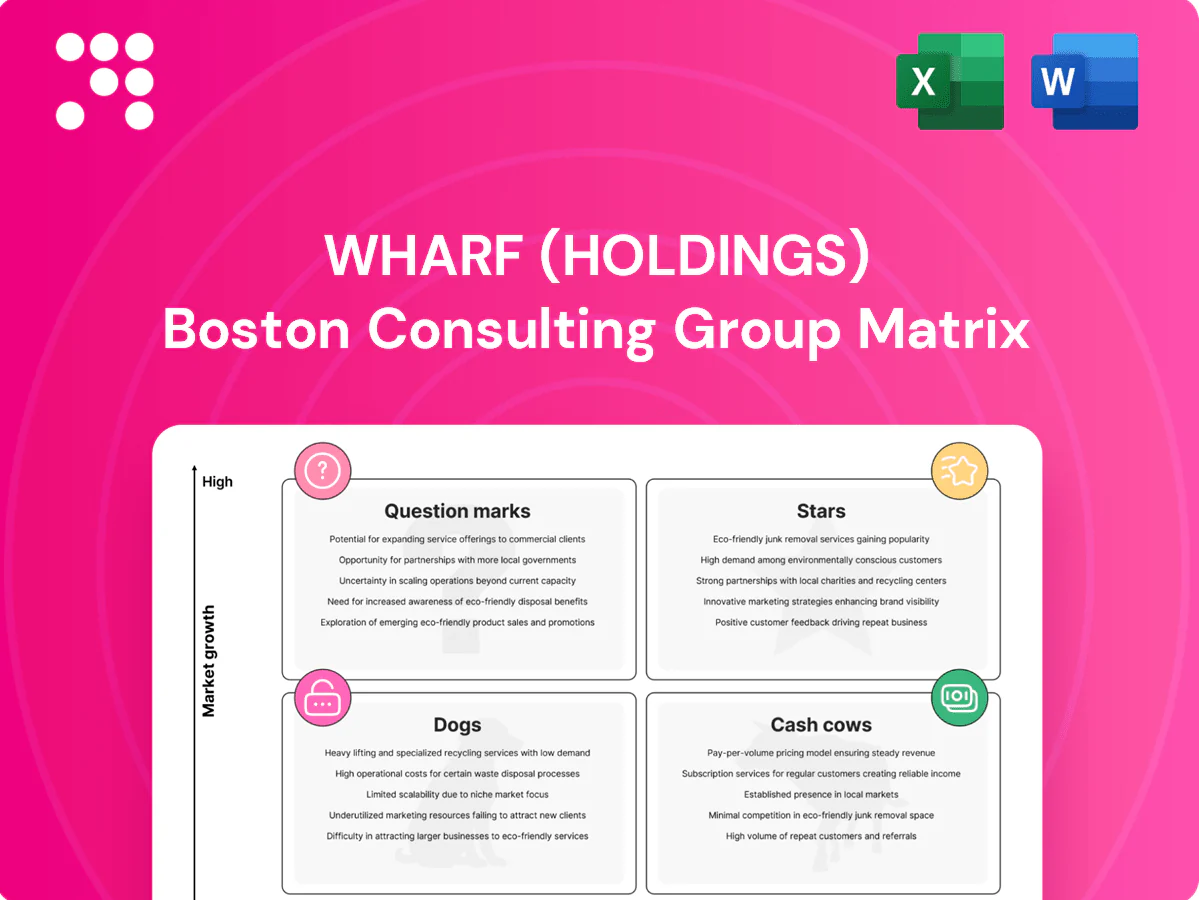

The Wharf (Holdings) BCG Matrix snapshot shows where its ports, property and retail assets land amid shifting demand—some are clear Cash Cows, others sit in the Question Mark corner begging for decisions. Want the quadrant-by-quadrant data, revenue momentum scores and pragmatic moves we’d actually use to reallocate capital? Purchase the full BCG Matrix for a complete Word report plus an editable Excel summary with tactical recommendations you can act on tomorrow. Skip the guesswork—get clarity and a ready plan.

Stars

Mainland China Grade-A commercial hubs

Mainland China Grade-A commercial hubs in tier-1 and strong tier-2 markets continue adding premium office and retail stock, and Wharf’s quality pipeline consistently wins blue-chip tenants, driving rapid occupancy and rental uplift. Achieving this requires heavy capex and leasing firepower, but tenant mix and rising rents compound returns over time. Management should keep feeding the pipeline to defend market share and ride the updraft.

Premium mixed-use developments (live-work-shop)

Premium mixed-use projects lock in footfall and pricing across retail, office and residential, creating cross-subsidy resilience; in fast-urbanizing nodes they scale rapidly and become local benchmarks. They consume cash during build-out and ramp-up but set market tempo; Wharf should stay on offense to convert growth into dominance.

Mainland e-commerce-ready warehouses

Mainland e-commerce-ready warehouses near demand centers benefit from secular omni-channel tailwinds as e-commerce penetration reached about 35% in 2024, boosting demand for last-mile logistics. High pre-let rates and vacancy under 5% in key markets have driven rising rents, but ongoing expansion capital is required to scale capacity. Speed to market matters more than perfection for capturing market share. Invest to keep the operational flywheel turning.

Flagship lifestyle retail precincts

Flagship lifestyle precincts combine luxury, F&B and experience-led retail and remain resilient in growth corridors; Harbour City (Wharf) hosts over 450 shops across ~2.1 million sq ft (Wharf 2024), sustaining strong footfall and spend. Strong brands track strong landlords, keeping core occupancy above 90–95% in 2024. Ongoing capex on curation and activation is continuous, turning mature precincts into stable cash engines.

- Destination retail mix drives premium spend

- Brands follow landlord strength — high occupancy 2024

- Capex on curation/activation is ongoing

- Maturation yields predictable cashflow

Top-tier residential launches in core cities

Top-tier residential launches in Hong Kong and major Chinese gateway cities consistently sell through even in choppy cycles; well-located, well-designed units command premium PSF, reinforcing Wharf (Holdings) market share and brand reputation.

Accelerated marketing and bespoke financing packages are essential to sustain velocity; scale projects only while absorption remains strong to optimize returns and capital turnover.

- Sell-through: location + design = premium PSF

- Marketing & financing: indispensable fuel

- Fast absorption enables scale

- Reputation drives repeat demand

Grade-A offices, mixed-use and last-mile logistics drive 90–95% occupancy, rental gains

Mainland Grade-A offices, premium mixed-use and last-mile logistics are Stars for Wharf, driving rapid rental/occupancy uplift (office/retail core occupancy 90–95% in 2024) but require heavy capex and leasing firepower. Ecommerce penetration ~35% in 2024 lifts logistics demand; vacancy <5% in key hubs. Harbour City (2024) ~450 shops, ~2.1m sq ft, anchors retail resilience and premium pricing.

| Asset | 2024 Metric | Implication |

|---|---|---|

| Offices/Retail | Occupancy 90–95% | High cashflow, needs capex |

| Logistics | E‑commerce 35%; vacancy <5% | Scale needed |

| Harbour City | ~450 shops; ~2.1m sq ft | Stable spend |

What is included in the product

In-depth BCG review of Wharf Holdings' portfolio, identifying Stars, Cash Cows, Question Marks and Dogs with strategic recommendations.

One-page Wharf BCG map placing every business in a quadrant — highlights pain points, export-ready for C-level decks and prints.

Cash Cows

Hong Kong investment properties (stable rentals)

Mature, high-occupancy Hong Kong investment properties such as Harbour City and Times Square generate steady rental cash flows. Renewal cycles and ancillary retail and F&B income keep margins healthy. Low organic growth reduces promotional spend, making these assets reliable dividend engines. Cash is routinely recycled to fund selective growth bets and capital projects.

Container terminals with entrenched share

Container terminals with entrenched share benefit from incumbency, scale and long-term customer ties that anchor throughput; Hong Kong remains a top-10 global port as of 2024, supporting steady volumes. Pricing is disciplined and opex efficiencies drop straight to cash, boosting free cash flow. Not a sprint market but dependable—focus on asset optimization, operational digitization and banking the cash.

Long-lease office towers

Long-lease office towers at Wharf benefit from blue-chip covenants that smooth volatility and materially lower re-leasing risk, with portfolio office occupancy around 95% in 2024. Capex is predictable and low-frequency, making NOI sticky across cycles. In 2024 reported yields exceeded estimated WACC by roughly 250 basis points, a durable spread that supports value. Maintain, don’t over-engineer; prioritize upkeep and tenant retention.

Legacy urban warehouses in HK

Legacy urban warehouses in HK function as cash cows for Wharf: occupancy >95% in 2024, alternatives scarce, and steady logistics demand keeps churn low. Incremental fit-outs historically lift achievable rents ~5% with light capex (typically <2% of asset value), so growth is muted but cash generation is clean. Sweat assets, limit tenant turnover and prioritize low-cost yield enhancements.

- Occupancy: >95% (2024)

- Typical rent uplift from light upgrades: ~5%

- Capex intensity: <2% of asset value

- Cash yield: 6-8%

Property management and recurring services

Property management and recurring services provide Wharf stable, captive fee streams with high revenue visibility; 2024 interim reporting showed year‑on‑year growth in recurring income supporting operating cash flow. Efficiency gains and tech platforms quietly widen margins, while low capital intensity keeps ROIC resilient. Surplus cash is redeployed to incubate the next growth segments.

- Stable fees: captive portfolio, predictable cash

- Margin levers: operational efficiency + tech

- Low capex, high visibility

- Surplus funds: finance new winners

City + port assets: 6–8% yields, 250bps spread

Mature Wharf assets (Harbour City, Times Square, container terminals, offices, warehouses) delivered high occupancy (~95%+ in 2024), 6–8% cash yields, ~5% light-upgrade rent uplift, capex <2% of value; reported yields ~250bps above WACC; surplus cash funds selective growth.

| Asset | Occupancy 2024 | Cash yield | Rent uplift | Capex | Spread vs WACC |

|---|---|---|---|---|---|

| Retail/Offices | ~95%+ | 6–8% | ~5% | <2% | ~250bps |

| Terminals/Warehouses | >95% | 6–8% | ~5% | <2% | ~250bps |

Full Transparency, Always

Wharf (Holdings) BCG Matrix

The file you're previewing is the final Wharf (Holdings) BCG Matrix you'll receive after purchase. No watermarks or demo text—just a fully formatted, strategy-ready report built around Wharf's portfolio, market share and growth insights. After buying, the exact same file is yours to download, edit, print or present. Clean, professional and ready for immediate use.

Unlock Strategic Clarity

The Wharf (Holdings) BCG Matrix snapshot shows where its ports, property and retail assets land amid shifting demand—some are clear Cash Cows, others sit in the Question Mark corner begging for decisions. Want the quadrant-by-quadrant data, revenue momentum scores and pragmatic moves we’d actually use to reallocate capital? Purchase the full BCG Matrix for a complete Word report plus an editable Excel summary with tactical recommendations you can act on tomorrow. Skip the guesswork—get clarity and a ready plan.

Stars

Mainland China Grade-A commercial hubs

Mainland China Grade-A commercial hubs in tier-1 and strong tier-2 markets continue adding premium office and retail stock, and Wharf’s quality pipeline consistently wins blue-chip tenants, driving rapid occupancy and rental uplift. Achieving this requires heavy capex and leasing firepower, but tenant mix and rising rents compound returns over time. Management should keep feeding the pipeline to defend market share and ride the updraft.

Premium mixed-use developments (live-work-shop)

Premium mixed-use projects lock in footfall and pricing across retail, office and residential, creating cross-subsidy resilience; in fast-urbanizing nodes they scale rapidly and become local benchmarks. They consume cash during build-out and ramp-up but set market tempo; Wharf should stay on offense to convert growth into dominance.

Mainland e-commerce-ready warehouses

Mainland e-commerce-ready warehouses near demand centers benefit from secular omni-channel tailwinds as e-commerce penetration reached about 35% in 2024, boosting demand for last-mile logistics. High pre-let rates and vacancy under 5% in key markets have driven rising rents, but ongoing expansion capital is required to scale capacity. Speed to market matters more than perfection for capturing market share. Invest to keep the operational flywheel turning.

Flagship lifestyle retail precincts

Flagship lifestyle precincts combine luxury, F&B and experience-led retail and remain resilient in growth corridors; Harbour City (Wharf) hosts over 450 shops across ~2.1 million sq ft (Wharf 2024), sustaining strong footfall and spend. Strong brands track strong landlords, keeping core occupancy above 90–95% in 2024. Ongoing capex on curation and activation is continuous, turning mature precincts into stable cash engines.

- Destination retail mix drives premium spend

- Brands follow landlord strength — high occupancy 2024

- Capex on curation/activation is ongoing

- Maturation yields predictable cashflow

Top-tier residential launches in core cities

Top-tier residential launches in Hong Kong and major Chinese gateway cities consistently sell through even in choppy cycles; well-located, well-designed units command premium PSF, reinforcing Wharf (Holdings) market share and brand reputation.

Accelerated marketing and bespoke financing packages are essential to sustain velocity; scale projects only while absorption remains strong to optimize returns and capital turnover.

- Sell-through: location + design = premium PSF

- Marketing & financing: indispensable fuel

- Fast absorption enables scale

- Reputation drives repeat demand

Grade-A offices, mixed-use and last-mile logistics drive 90–95% occupancy, rental gains

Mainland Grade-A offices, premium mixed-use and last-mile logistics are Stars for Wharf, driving rapid rental/occupancy uplift (office/retail core occupancy 90–95% in 2024) but require heavy capex and leasing firepower. Ecommerce penetration ~35% in 2024 lifts logistics demand; vacancy <5% in key hubs. Harbour City (2024) ~450 shops, ~2.1m sq ft, anchors retail resilience and premium pricing.

| Asset | 2024 Metric | Implication |

|---|---|---|

| Offices/Retail | Occupancy 90–95% | High cashflow, needs capex |

| Logistics | E‑commerce 35%; vacancy <5% | Scale needed |

| Harbour City | ~450 shops; ~2.1m sq ft | Stable spend |

What is included in the product

In-depth BCG review of Wharf Holdings' portfolio, identifying Stars, Cash Cows, Question Marks and Dogs with strategic recommendations.

One-page Wharf BCG map placing every business in a quadrant — highlights pain points, export-ready for C-level decks and prints.

Cash Cows

Hong Kong investment properties (stable rentals)

Mature, high-occupancy Hong Kong investment properties such as Harbour City and Times Square generate steady rental cash flows. Renewal cycles and ancillary retail and F&B income keep margins healthy. Low organic growth reduces promotional spend, making these assets reliable dividend engines. Cash is routinely recycled to fund selective growth bets and capital projects.

Container terminals with entrenched share

Container terminals with entrenched share benefit from incumbency, scale and long-term customer ties that anchor throughput; Hong Kong remains a top-10 global port as of 2024, supporting steady volumes. Pricing is disciplined and opex efficiencies drop straight to cash, boosting free cash flow. Not a sprint market but dependable—focus on asset optimization, operational digitization and banking the cash.

Long-lease office towers

Long-lease office towers at Wharf benefit from blue-chip covenants that smooth volatility and materially lower re-leasing risk, with portfolio office occupancy around 95% in 2024. Capex is predictable and low-frequency, making NOI sticky across cycles. In 2024 reported yields exceeded estimated WACC by roughly 250 basis points, a durable spread that supports value. Maintain, don’t over-engineer; prioritize upkeep and tenant retention.

Legacy urban warehouses in HK

Legacy urban warehouses in HK function as cash cows for Wharf: occupancy >95% in 2024, alternatives scarce, and steady logistics demand keeps churn low. Incremental fit-outs historically lift achievable rents ~5% with light capex (typically <2% of asset value), so growth is muted but cash generation is clean. Sweat assets, limit tenant turnover and prioritize low-cost yield enhancements.

- Occupancy: >95% (2024)

- Typical rent uplift from light upgrades: ~5%

- Capex intensity: <2% of asset value

- Cash yield: 6-8%

Property management and recurring services

Property management and recurring services provide Wharf stable, captive fee streams with high revenue visibility; 2024 interim reporting showed year‑on‑year growth in recurring income supporting operating cash flow. Efficiency gains and tech platforms quietly widen margins, while low capital intensity keeps ROIC resilient. Surplus cash is redeployed to incubate the next growth segments.

- Stable fees: captive portfolio, predictable cash

- Margin levers: operational efficiency + tech

- Low capex, high visibility

- Surplus funds: finance new winners

City + port assets: 6–8% yields, 250bps spread

Mature Wharf assets (Harbour City, Times Square, container terminals, offices, warehouses) delivered high occupancy (~95%+ in 2024), 6–8% cash yields, ~5% light-upgrade rent uplift, capex <2% of value; reported yields ~250bps above WACC; surplus cash funds selective growth.

| Asset | Occupancy 2024 | Cash yield | Rent uplift | Capex | Spread vs WACC |

|---|---|---|---|---|---|

| Retail/Offices | ~95%+ | 6–8% | ~5% | <2% | ~250bps |

| Terminals/Warehouses | >95% | 6–8% | ~5% | <2% | ~250bps |

Full Transparency, Always

Wharf (Holdings) BCG Matrix

The file you're previewing is the final Wharf (Holdings) BCG Matrix you'll receive after purchase. No watermarks or demo text—just a fully formatted, strategy-ready report built around Wharf's portfolio, market share and growth insights. After buying, the exact same file is yours to download, edit, print or present. Clean, professional and ready for immediate use.

Original: $10.00

-65%$10.00

$3.50Description

Unlock Strategic Clarity

The Wharf (Holdings) BCG Matrix snapshot shows where its ports, property and retail assets land amid shifting demand—some are clear Cash Cows, others sit in the Question Mark corner begging for decisions. Want the quadrant-by-quadrant data, revenue momentum scores and pragmatic moves we’d actually use to reallocate capital? Purchase the full BCG Matrix for a complete Word report plus an editable Excel summary with tactical recommendations you can act on tomorrow. Skip the guesswork—get clarity and a ready plan.

Stars

Mainland China Grade-A commercial hubs

Mainland China Grade-A commercial hubs in tier-1 and strong tier-2 markets continue adding premium office and retail stock, and Wharf’s quality pipeline consistently wins blue-chip tenants, driving rapid occupancy and rental uplift. Achieving this requires heavy capex and leasing firepower, but tenant mix and rising rents compound returns over time. Management should keep feeding the pipeline to defend market share and ride the updraft.

Premium mixed-use developments (live-work-shop)

Premium mixed-use projects lock in footfall and pricing across retail, office and residential, creating cross-subsidy resilience; in fast-urbanizing nodes they scale rapidly and become local benchmarks. They consume cash during build-out and ramp-up but set market tempo; Wharf should stay on offense to convert growth into dominance.

Mainland e-commerce-ready warehouses

Mainland e-commerce-ready warehouses near demand centers benefit from secular omni-channel tailwinds as e-commerce penetration reached about 35% in 2024, boosting demand for last-mile logistics. High pre-let rates and vacancy under 5% in key markets have driven rising rents, but ongoing expansion capital is required to scale capacity. Speed to market matters more than perfection for capturing market share. Invest to keep the operational flywheel turning.

Flagship lifestyle retail precincts

Flagship lifestyle precincts combine luxury, F&B and experience-led retail and remain resilient in growth corridors; Harbour City (Wharf) hosts over 450 shops across ~2.1 million sq ft (Wharf 2024), sustaining strong footfall and spend. Strong brands track strong landlords, keeping core occupancy above 90–95% in 2024. Ongoing capex on curation and activation is continuous, turning mature precincts into stable cash engines.

- Destination retail mix drives premium spend

- Brands follow landlord strength — high occupancy 2024

- Capex on curation/activation is ongoing

- Maturation yields predictable cashflow

Top-tier residential launches in core cities

Top-tier residential launches in Hong Kong and major Chinese gateway cities consistently sell through even in choppy cycles; well-located, well-designed units command premium PSF, reinforcing Wharf (Holdings) market share and brand reputation.

Accelerated marketing and bespoke financing packages are essential to sustain velocity; scale projects only while absorption remains strong to optimize returns and capital turnover.

- Sell-through: location + design = premium PSF

- Marketing & financing: indispensable fuel

- Fast absorption enables scale

- Reputation drives repeat demand

Grade-A offices, mixed-use and last-mile logistics drive 90–95% occupancy, rental gains

Mainland Grade-A offices, premium mixed-use and last-mile logistics are Stars for Wharf, driving rapid rental/occupancy uplift (office/retail core occupancy 90–95% in 2024) but require heavy capex and leasing firepower. Ecommerce penetration ~35% in 2024 lifts logistics demand; vacancy <5% in key hubs. Harbour City (2024) ~450 shops, ~2.1m sq ft, anchors retail resilience and premium pricing.

| Asset | 2024 Metric | Implication |

|---|---|---|

| Offices/Retail | Occupancy 90–95% | High cashflow, needs capex |

| Logistics | E‑commerce 35%; vacancy <5% | Scale needed |

| Harbour City | ~450 shops; ~2.1m sq ft | Stable spend |

What is included in the product

In-depth BCG review of Wharf Holdings' portfolio, identifying Stars, Cash Cows, Question Marks and Dogs with strategic recommendations.

One-page Wharf BCG map placing every business in a quadrant — highlights pain points, export-ready for C-level decks and prints.

Cash Cows

Hong Kong investment properties (stable rentals)

Mature, high-occupancy Hong Kong investment properties such as Harbour City and Times Square generate steady rental cash flows. Renewal cycles and ancillary retail and F&B income keep margins healthy. Low organic growth reduces promotional spend, making these assets reliable dividend engines. Cash is routinely recycled to fund selective growth bets and capital projects.

Container terminals with entrenched share

Container terminals with entrenched share benefit from incumbency, scale and long-term customer ties that anchor throughput; Hong Kong remains a top-10 global port as of 2024, supporting steady volumes. Pricing is disciplined and opex efficiencies drop straight to cash, boosting free cash flow. Not a sprint market but dependable—focus on asset optimization, operational digitization and banking the cash.

Long-lease office towers

Long-lease office towers at Wharf benefit from blue-chip covenants that smooth volatility and materially lower re-leasing risk, with portfolio office occupancy around 95% in 2024. Capex is predictable and low-frequency, making NOI sticky across cycles. In 2024 reported yields exceeded estimated WACC by roughly 250 basis points, a durable spread that supports value. Maintain, don’t over-engineer; prioritize upkeep and tenant retention.

Legacy urban warehouses in HK

Legacy urban warehouses in HK function as cash cows for Wharf: occupancy >95% in 2024, alternatives scarce, and steady logistics demand keeps churn low. Incremental fit-outs historically lift achievable rents ~5% with light capex (typically <2% of asset value), so growth is muted but cash generation is clean. Sweat assets, limit tenant turnover and prioritize low-cost yield enhancements.

- Occupancy: >95% (2024)

- Typical rent uplift from light upgrades: ~5%

- Capex intensity: <2% of asset value

- Cash yield: 6-8%

Property management and recurring services

Property management and recurring services provide Wharf stable, captive fee streams with high revenue visibility; 2024 interim reporting showed year‑on‑year growth in recurring income supporting operating cash flow. Efficiency gains and tech platforms quietly widen margins, while low capital intensity keeps ROIC resilient. Surplus cash is redeployed to incubate the next growth segments.

- Stable fees: captive portfolio, predictable cash

- Margin levers: operational efficiency + tech

- Low capex, high visibility

- Surplus funds: finance new winners

City + port assets: 6–8% yields, 250bps spread

Mature Wharf assets (Harbour City, Times Square, container terminals, offices, warehouses) delivered high occupancy (~95%+ in 2024), 6–8% cash yields, ~5% light-upgrade rent uplift, capex <2% of value; reported yields ~250bps above WACC; surplus cash funds selective growth.

| Asset | Occupancy 2024 | Cash yield | Rent uplift | Capex | Spread vs WACC |

|---|---|---|---|---|---|

| Retail/Offices | ~95%+ | 6–8% | ~5% | <2% | ~250bps |

| Terminals/Warehouses | >95% | 6–8% | ~5% | <2% | ~250bps |

Full Transparency, Always

Wharf (Holdings) BCG Matrix

The file you're previewing is the final Wharf (Holdings) BCG Matrix you'll receive after purchase. No watermarks or demo text—just a fully formatted, strategy-ready report built around Wharf's portfolio, market share and growth insights. After buying, the exact same file is yours to download, edit, print or present. Clean, professional and ready for immediate use.