Whitbread SWOT Analysis

Elevate Your Analysis with the Complete SWOT Report

Whitbread’s Premier Inn brand and large UK footprint drive strong revenue resilience and scale advantages, while cost pressure, labour shortages and heavy UK exposure pose clear risks; digitalisation and international expansion offer growth levers. Purchase the full SWOT analysis for a professionally formatted Word and Excel report to strategize, present, and invest with confidence.

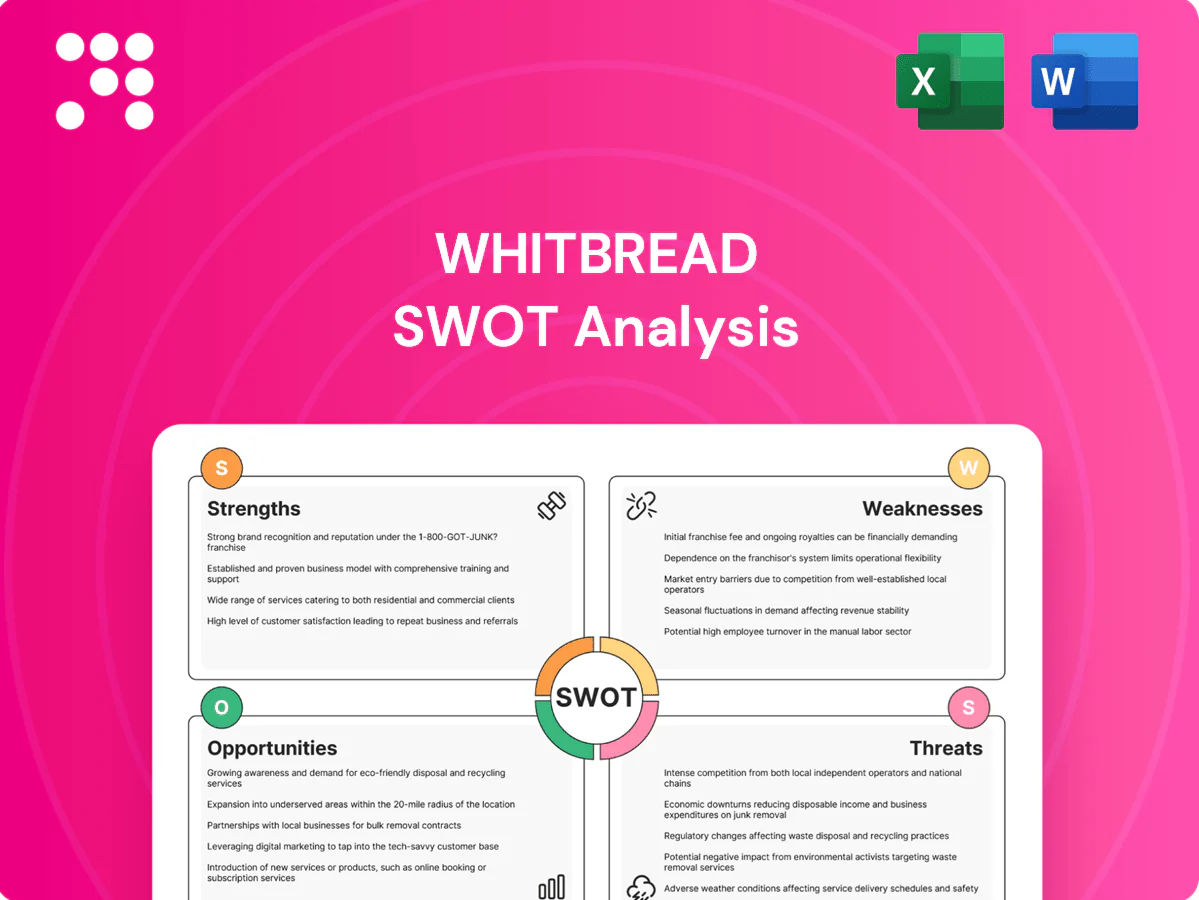

Strengths

Premier Inn market leadership

Premier Inn is the UKs leading budget/midscale brand with over 800 hotels, driving strong brand recognition and customer trust. Consistently high occupancy and RevPAR resilience in the value segment underpins steady cash flows. Scale enables superior procurement, marketing efficiency and standardized service delivery, creating meaningful barriers to entry for smaller rivals.

Integrated hotel-restaurant model

Co-located Brewers Fayre, Beefeater and Bar + Block alongside Premier Inn — the UK’s largest hotel brand — boost guest convenience and capture ancillary spend. Shared sites lift asset utilisation and margins via operational synergies, while F&B broadens family and corporate appeal. The integrated model is flexed by market to optimise returns.

Value-driven positioning

Affordable, consistent quality resonates with price-sensitive leisure and business travellers; Premier Inn’s value proposition is supported by scale—over 800 hotels and c.70,000 rooms—widening the addressable market across the UK and Germany. In downturns customers often trade down into this segment, enabling dynamic pricing that preserves trust. Whitbread reported group revenue of c.£3.8bn in FY24, underlining the model’s resilience.

Robust digital and direct channels

Whitbread’s strong app, website and booking engine drive high direct bookings, lowering OTA commission exposure while enabling personalized upsells and ancillary revenue through streamlined check-in and offers. Advanced digital tools support dynamic yield management and refine pricing and occupancy mix via real-time data, improving marketing ROI. Seamless digital journeys boost guest satisfaction and retention across Premier Inn and other brands.

- Direct bookings reduce OTA fees and increase margin

- Dynamic pricing and upsells raise RevPAR

- Data-driven marketing improves acquisition ROI

- Integrated UX elevates NPS and repeat stays

Disciplined expansion capability

Whitbread’s disciplined expansion — backed by a c.840 Premier Inn UK estate (≈85,000 rooms) — is powered by proven site selection, standardized builds and efficient operations, enabling scalable network growth. The Germany rollout leverages the UK playbook to accelerate openings; centralized procurement and modular design cut timelines and costs, while active portfolio management prunes underperformers.

- c.840 UK hotels

- ≈85,000 rooms

- Centralized procurement

- Modular builds shorten timelines

- Portfolio pruning

UK budget hotel scale drives robust cash flows, strong RevPAR and margin uplift from direct bookings

Premier Inn scale drives strong cashflows: c.840 UK hotels, ≈85,000 rooms; group revenue c.£3.8bn (FY24); high occupancy/RevPAR resilience in the value segment; digital-first direct bookings reduce OTA fees and boost margins.

| Metric | Value |

|---|---|

| UK hotels | c.840 |

| Rooms | ≈85,000 |

| Group revenue (FY24) | c.£3.8bn |

What is included in the product

Delivers a strategic overview of Whitbread’s internal and external business factors, outlining strengths, weaknesses, opportunities and threats to assess its competitive position, growth drivers and key risks.

Provides a concise, Whitbread-specific SWOT matrix for fast strategic alignment and executive snapshots, enabling quick updates to reflect operational shifts and competitive pressures.

Weaknesses

UK revenue concentration

Whitbread remains highly concentrated in the UK, with over 80% of group revenue generated there, making performance highly sensitive to UK macro cycles and consumer confidence swings. Regional demand shocks or changes in UK policy, taxation or business rates can therefore disproportionately affect results. Expansion in Germany is accelerating but still small relative to the UK footprint, leaving currency and geographic balance limited.

Capital-intensive estate

Whitbread's owned and long-lease estate—over 800 hotels and c.80,000 rooms—requires significant upfront and ongoing capex, with FY2024 maintenance and development spend in the mid-hundreds of millions; construction cost inflation has compressed project IRRs and extended payback periods, while the heavy asset base lowers returns versus asset-light peers and long-term commitments constrain rapid strategic pivots.

Restaurant brand variability

Performance across Brewers Fayre, Beefeater and Bar + Block can be uneven by location, dragging on Whitbread group revenue (reported ~£3.6bn in FY24) as F&B faces intense competition and food cost volatility—food inflation peaked around 15% in 2022–23—pressuring margins. Turnaround or rebranding often needs multi-million-pound investment and 12–24 months, and underperforming restaurants dilute hotel economics at co-located Premier Inn sites.

Limited presence in premium segments

Whitbread’s heavy focus on budget and midscale Premier Inn caps ADR upside and leaves it underexposed to higher-margin luxury and lifestyle niches, reducing revenue diversification and margin resilience. Brand-stretch risk constrains moving upmarket under the Premier Inn banner, while competitors targeting upscale demand may capture growth and higher returns Whitbread cannot fully access.

- Concentration: limited luxury/lifestyle exposure

- ADR constraint: midscale pricing ceiling

- Brand-stretch: Premier Inn limits upmarket moves

- Competitive loss: upscale opportunities ceded

Exposure to business travel cycles

UK-heavy hotel operator: >80% UK revenue, ~833 hotels, midweek stays 8-12% below 2019

High UK concentration (>80% revenue) and ~833 hotels/≈82,000 rooms (FY24) leave Whitbread exposed to UK demand and policy shocks. Large owned estate drives mid-hundreds of millions in annual capex, compressing returns versus asset-light peers. Midweek stays remain ~8–12% below 2019, limiting ADR upside and margin resilience.

| Metric | Value |

|---|---|

| Group revenue FY24 | £3.6bn |

| UK revenue share | >80% |

| Hotels/rooms | ~833 / ~82,000 |

| Midweek gap vs 2019 | 8–12% |

Preview Before You Purchase

Whitbread SWOT Analysis

This is the actual Whitbread SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full report you'll get; buy to unlock the complete, editable version. The file shown is the real analysis you'll download after payment, ready to use in presentations or strategy work.

Elevate Your Analysis with the Complete SWOT Report

Whitbread’s Premier Inn brand and large UK footprint drive strong revenue resilience and scale advantages, while cost pressure, labour shortages and heavy UK exposure pose clear risks; digitalisation and international expansion offer growth levers. Purchase the full SWOT analysis for a professionally formatted Word and Excel report to strategize, present, and invest with confidence.

Strengths

Premier Inn market leadership

Premier Inn is the UKs leading budget/midscale brand with over 800 hotels, driving strong brand recognition and customer trust. Consistently high occupancy and RevPAR resilience in the value segment underpins steady cash flows. Scale enables superior procurement, marketing efficiency and standardized service delivery, creating meaningful barriers to entry for smaller rivals.

Integrated hotel-restaurant model

Co-located Brewers Fayre, Beefeater and Bar + Block alongside Premier Inn — the UK’s largest hotel brand — boost guest convenience and capture ancillary spend. Shared sites lift asset utilisation and margins via operational synergies, while F&B broadens family and corporate appeal. The integrated model is flexed by market to optimise returns.

Value-driven positioning

Affordable, consistent quality resonates with price-sensitive leisure and business travellers; Premier Inn’s value proposition is supported by scale—over 800 hotels and c.70,000 rooms—widening the addressable market across the UK and Germany. In downturns customers often trade down into this segment, enabling dynamic pricing that preserves trust. Whitbread reported group revenue of c.£3.8bn in FY24, underlining the model’s resilience.

Robust digital and direct channels

Whitbread’s strong app, website and booking engine drive high direct bookings, lowering OTA commission exposure while enabling personalized upsells and ancillary revenue through streamlined check-in and offers. Advanced digital tools support dynamic yield management and refine pricing and occupancy mix via real-time data, improving marketing ROI. Seamless digital journeys boost guest satisfaction and retention across Premier Inn and other brands.

- Direct bookings reduce OTA fees and increase margin

- Dynamic pricing and upsells raise RevPAR

- Data-driven marketing improves acquisition ROI

- Integrated UX elevates NPS and repeat stays

Disciplined expansion capability

Whitbread’s disciplined expansion — backed by a c.840 Premier Inn UK estate (≈85,000 rooms) — is powered by proven site selection, standardized builds and efficient operations, enabling scalable network growth. The Germany rollout leverages the UK playbook to accelerate openings; centralized procurement and modular design cut timelines and costs, while active portfolio management prunes underperformers.

- c.840 UK hotels

- ≈85,000 rooms

- Centralized procurement

- Modular builds shorten timelines

- Portfolio pruning

UK budget hotel scale drives robust cash flows, strong RevPAR and margin uplift from direct bookings

Premier Inn scale drives strong cashflows: c.840 UK hotels, ≈85,000 rooms; group revenue c.£3.8bn (FY24); high occupancy/RevPAR resilience in the value segment; digital-first direct bookings reduce OTA fees and boost margins.

| Metric | Value |

|---|---|

| UK hotels | c.840 |

| Rooms | ≈85,000 |

| Group revenue (FY24) | c.£3.8bn |

What is included in the product

Delivers a strategic overview of Whitbread’s internal and external business factors, outlining strengths, weaknesses, opportunities and threats to assess its competitive position, growth drivers and key risks.

Provides a concise, Whitbread-specific SWOT matrix for fast strategic alignment and executive snapshots, enabling quick updates to reflect operational shifts and competitive pressures.

Weaknesses

UK revenue concentration

Whitbread remains highly concentrated in the UK, with over 80% of group revenue generated there, making performance highly sensitive to UK macro cycles and consumer confidence swings. Regional demand shocks or changes in UK policy, taxation or business rates can therefore disproportionately affect results. Expansion in Germany is accelerating but still small relative to the UK footprint, leaving currency and geographic balance limited.

Capital-intensive estate

Whitbread's owned and long-lease estate—over 800 hotels and c.80,000 rooms—requires significant upfront and ongoing capex, with FY2024 maintenance and development spend in the mid-hundreds of millions; construction cost inflation has compressed project IRRs and extended payback periods, while the heavy asset base lowers returns versus asset-light peers and long-term commitments constrain rapid strategic pivots.

Restaurant brand variability

Performance across Brewers Fayre, Beefeater and Bar + Block can be uneven by location, dragging on Whitbread group revenue (reported ~£3.6bn in FY24) as F&B faces intense competition and food cost volatility—food inflation peaked around 15% in 2022–23—pressuring margins. Turnaround or rebranding often needs multi-million-pound investment and 12–24 months, and underperforming restaurants dilute hotel economics at co-located Premier Inn sites.

Limited presence in premium segments

Whitbread’s heavy focus on budget and midscale Premier Inn caps ADR upside and leaves it underexposed to higher-margin luxury and lifestyle niches, reducing revenue diversification and margin resilience. Brand-stretch risk constrains moving upmarket under the Premier Inn banner, while competitors targeting upscale demand may capture growth and higher returns Whitbread cannot fully access.

- Concentration: limited luxury/lifestyle exposure

- ADR constraint: midscale pricing ceiling

- Brand-stretch: Premier Inn limits upmarket moves

- Competitive loss: upscale opportunities ceded

Exposure to business travel cycles

UK-heavy hotel operator: >80% UK revenue, ~833 hotels, midweek stays 8-12% below 2019

High UK concentration (>80% revenue) and ~833 hotels/≈82,000 rooms (FY24) leave Whitbread exposed to UK demand and policy shocks. Large owned estate drives mid-hundreds of millions in annual capex, compressing returns versus asset-light peers. Midweek stays remain ~8–12% below 2019, limiting ADR upside and margin resilience.

| Metric | Value |

|---|---|

| Group revenue FY24 | £3.6bn |

| UK revenue share | >80% |

| Hotels/rooms | ~833 / ~82,000 |

| Midweek gap vs 2019 | 8–12% |

Preview Before You Purchase

Whitbread SWOT Analysis

This is the actual Whitbread SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full report you'll get; buy to unlock the complete, editable version. The file shown is the real analysis you'll download after payment, ready to use in presentations or strategy work.

Description

Elevate Your Analysis with the Complete SWOT Report

Whitbread’s Premier Inn brand and large UK footprint drive strong revenue resilience and scale advantages, while cost pressure, labour shortages and heavy UK exposure pose clear risks; digitalisation and international expansion offer growth levers. Purchase the full SWOT analysis for a professionally formatted Word and Excel report to strategize, present, and invest with confidence.

Strengths

Premier Inn market leadership

Premier Inn is the UKs leading budget/midscale brand with over 800 hotels, driving strong brand recognition and customer trust. Consistently high occupancy and RevPAR resilience in the value segment underpins steady cash flows. Scale enables superior procurement, marketing efficiency and standardized service delivery, creating meaningful barriers to entry for smaller rivals.

Integrated hotel-restaurant model

Co-located Brewers Fayre, Beefeater and Bar + Block alongside Premier Inn — the UK’s largest hotel brand — boost guest convenience and capture ancillary spend. Shared sites lift asset utilisation and margins via operational synergies, while F&B broadens family and corporate appeal. The integrated model is flexed by market to optimise returns.

Value-driven positioning

Affordable, consistent quality resonates with price-sensitive leisure and business travellers; Premier Inn’s value proposition is supported by scale—over 800 hotels and c.70,000 rooms—widening the addressable market across the UK and Germany. In downturns customers often trade down into this segment, enabling dynamic pricing that preserves trust. Whitbread reported group revenue of c.£3.8bn in FY24, underlining the model’s resilience.

Robust digital and direct channels

Whitbread’s strong app, website and booking engine drive high direct bookings, lowering OTA commission exposure while enabling personalized upsells and ancillary revenue through streamlined check-in and offers. Advanced digital tools support dynamic yield management and refine pricing and occupancy mix via real-time data, improving marketing ROI. Seamless digital journeys boost guest satisfaction and retention across Premier Inn and other brands.

- Direct bookings reduce OTA fees and increase margin

- Dynamic pricing and upsells raise RevPAR

- Data-driven marketing improves acquisition ROI

- Integrated UX elevates NPS and repeat stays

Disciplined expansion capability

Whitbread’s disciplined expansion — backed by a c.840 Premier Inn UK estate (≈85,000 rooms) — is powered by proven site selection, standardized builds and efficient operations, enabling scalable network growth. The Germany rollout leverages the UK playbook to accelerate openings; centralized procurement and modular design cut timelines and costs, while active portfolio management prunes underperformers.

- c.840 UK hotels

- ≈85,000 rooms

- Centralized procurement

- Modular builds shorten timelines

- Portfolio pruning

UK budget hotel scale drives robust cash flows, strong RevPAR and margin uplift from direct bookings

Premier Inn scale drives strong cashflows: c.840 UK hotels, ≈85,000 rooms; group revenue c.£3.8bn (FY24); high occupancy/RevPAR resilience in the value segment; digital-first direct bookings reduce OTA fees and boost margins.

| Metric | Value |

|---|---|

| UK hotels | c.840 |

| Rooms | ≈85,000 |

| Group revenue (FY24) | c.£3.8bn |

What is included in the product

Delivers a strategic overview of Whitbread’s internal and external business factors, outlining strengths, weaknesses, opportunities and threats to assess its competitive position, growth drivers and key risks.

Provides a concise, Whitbread-specific SWOT matrix for fast strategic alignment and executive snapshots, enabling quick updates to reflect operational shifts and competitive pressures.

Weaknesses

UK revenue concentration

Whitbread remains highly concentrated in the UK, with over 80% of group revenue generated there, making performance highly sensitive to UK macro cycles and consumer confidence swings. Regional demand shocks or changes in UK policy, taxation or business rates can therefore disproportionately affect results. Expansion in Germany is accelerating but still small relative to the UK footprint, leaving currency and geographic balance limited.

Capital-intensive estate

Whitbread's owned and long-lease estate—over 800 hotels and c.80,000 rooms—requires significant upfront and ongoing capex, with FY2024 maintenance and development spend in the mid-hundreds of millions; construction cost inflation has compressed project IRRs and extended payback periods, while the heavy asset base lowers returns versus asset-light peers and long-term commitments constrain rapid strategic pivots.

Restaurant brand variability

Performance across Brewers Fayre, Beefeater and Bar + Block can be uneven by location, dragging on Whitbread group revenue (reported ~£3.6bn in FY24) as F&B faces intense competition and food cost volatility—food inflation peaked around 15% in 2022–23—pressuring margins. Turnaround or rebranding often needs multi-million-pound investment and 12–24 months, and underperforming restaurants dilute hotel economics at co-located Premier Inn sites.

Limited presence in premium segments

Whitbread’s heavy focus on budget and midscale Premier Inn caps ADR upside and leaves it underexposed to higher-margin luxury and lifestyle niches, reducing revenue diversification and margin resilience. Brand-stretch risk constrains moving upmarket under the Premier Inn banner, while competitors targeting upscale demand may capture growth and higher returns Whitbread cannot fully access.

- Concentration: limited luxury/lifestyle exposure

- ADR constraint: midscale pricing ceiling

- Brand-stretch: Premier Inn limits upmarket moves

- Competitive loss: upscale opportunities ceded

Exposure to business travel cycles

UK-heavy hotel operator: >80% UK revenue, ~833 hotels, midweek stays 8-12% below 2019

High UK concentration (>80% revenue) and ~833 hotels/≈82,000 rooms (FY24) leave Whitbread exposed to UK demand and policy shocks. Large owned estate drives mid-hundreds of millions in annual capex, compressing returns versus asset-light peers. Midweek stays remain ~8–12% below 2019, limiting ADR upside and margin resilience.

| Metric | Value |

|---|---|

| Group revenue FY24 | £3.6bn |

| UK revenue share | >80% |

| Hotels/rooms | ~833 / ~82,000 |

| Midweek gap vs 2019 | 8–12% |

Preview Before You Purchase

Whitbread SWOT Analysis

This is the actual Whitbread SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full report you'll get; buy to unlock the complete, editable version. The file shown is the real analysis you'll download after payment, ready to use in presentations or strategy work.