Whitehaven Coal Porter's Five Forces Analysis

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

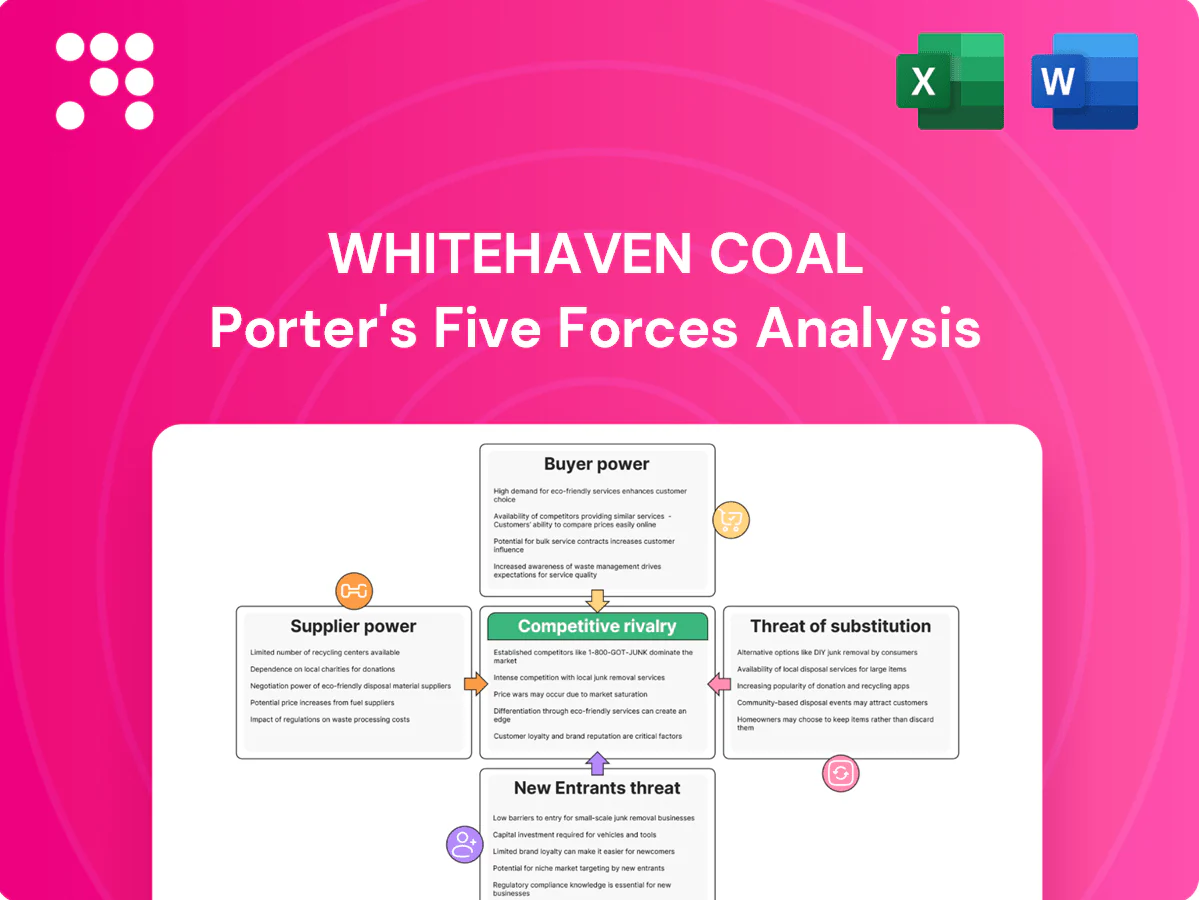

Whitehaven Coal faces strong supplier and regulatory pressures, intense buyer bargaining in thermal coal markets, and moderate threat from substitutes as energy transition accelerates; rivalry among incumbents remains heated. This snapshot highlights key dynamics but only scratches the surface. Unlock the full Porter's Five Forces Analysis for force-by-force ratings, visuals, and strategic implications to inform investment or strategy.

Suppliers Bargaining Power

Concentrated critical inputs

Heavy equipment OEMs (Caterpillar, Komatsu), explosives supplier Orica and a small set of rail/port operators dominate Australia’s coal corridors, giving them pricing leverage; Port of Newcastle handled roughly 150 million tonnes of coal in 2024, creating capacity constraints for train paths and berths. Switching suppliers requires delays, re-approvals and retraining, raising costs and limiting negotiating flexibility for Whitehaven.

Labor and contractor leverage

Skilled mining labour and specialist contractors are scarce in regional NSW, tightening suppliers' leverage and forcing Whitehaven to bid up for talent; mining full‑time average earnings were about AUD 2,690/week in May 2024 (ABS). Enterprise agreements and strict safety standards raise baseline costs and contractor rates, and labour actions or shortages can halt production schedules. Whitehaven pays observable premiums to attract and retain critical crews.

Energy and diesel volatility

Diesel and electricity are major input costs for Whitehaven; Brent crude averaged about US$86/bbl in 2024, contributing to elevated diesel landed costs and Australian retail diesel averaging near A$1.60/L in 2024. Limited onsite fuel or grid substitutes means short-term exposure remains high. Logistics fuel surcharges amplified spikes, at times adding up to c.15% to transport bills in 2024. Hedging mitigates but cannot fully neutralize sudden cost shocks.

Infrastructure gatekeepers

Rail network owners and port terminals act as throughput bottlenecks for Whitehaven; 2024 take-or-pay rail and berthing contracts shift volume risk back to miners and limit pricing leverage. Negotiating better terms is hard without credible alternative routes, and 2024 congestion and maintenance windows increased vessel queueing, curtailing shipments and flexibility.

- Bottleneck suppliers: rail + terminals constrain capacity

- Contract risk: take-or-pay shifts volume risk to miners

- Leverage: few credible alternative routes

- 2024 impact: congestion/maintenance raised queue times and cut shipments

Geology and blasting consumables

Geology at Whitehaven drives drill-and-blast inputs, wear-part turnover and ground support consumption, making demand site-specific; OEM parts and certified explosives have few substitutes and are subject to state explosives regulation, with typical supply lead times of weeks and strict safety compliance that limit rapid supplier switching, embedding moderate structural supplier power.

- Geology-driven demand

- Limited substitutes: OEM parts, certified explosives

- Lead times: weeks

- Safety/regulation constrains switching

Supplier power tight as Port Newcastle hits 150 Mt, diesel and labour up

Few heavy‑equipment OEMs, explosives firms and rail/port operators give suppliers pricing leverage; Port of Newcastle handled ~150 Mt coal in 2024, tightening capacity. Labour and contractors are scarce—mining avg earnings ~A$2,690/week (May 2024)—raising costs. Energy costs (Brent ~US$86/bbl; diesel ~A$1.60/L in 2024) and take‑or‑pay rail contracts keep supplier power elevated.

| Metric | 2024 Value |

|---|---|

| Port Newcastle throughput | ~150 Mt |

| Brent crude | ~US$86/bbl |

| Diesel retail AUS | ~A$1.60/L |

| Mining avg earnings (May) | A$2,690/week |

What is included in the product

Uncovers key drivers of competition, customer influence, and market entry risks tailored to Whitehaven Coal, detailing each Porter’s force with industry data and strategic commentary; evaluates supplier and buyer power, threats from substitutes and new entrants, and identifies disruptive forces and defensive dynamics to inform investor and corporate strategy.

One-sheet Porter's Five Forces for Whitehaven Coal—quickly spot supplier, buyer, entrant, substitute and rivalry pressures to relieve strategic blind spots and export slides-ready insights for faster, confident decision-making.

Customers Bargaining Power

Concentrated Asian buyers

Utilities, steel mills and trading houses in Japan, Korea, Taiwan and India are concentrated and sophisticated buyers that benchmark purchases to transparent indices such as Platts and ICE for both metallurgical and thermal coal. Their scale enables multi-sourcing and the negotiation of stringent contract terms, volume discounts and short notice windows. This concentration significantly elevates buyer bargaining power against suppliers like Whitehaven Coal.

Specification sensitivity

Buyers demand tight specs on energy, ash, sulfur and coking properties, pressuring Whitehaven to sustain QA systems and sampling protocols; in 2024 seaborne buyers tightened inspections amid market volatility. Off-spec cargoes face discounts or rejection, commonly ranging from low single-digit to double-digit percent penalties per industry trade reports. Higher-quality met coal earns premia but invites stringent contractual penalties for deviations, raising quality-control costs for Whitehaven.

Contracting mix dynamics

Contracting mix dynamics: a blend of long-, medium- and spot contracts shifts leverage to buyers; in weak markets buyers pushed shorter tenors and index-linked pricing, with spot share rising to ~35% in 2024. Destination flexibility and volume optionality (cargo re-direction) favor buyers. Take-or-pay logistics and Port of Newcastle throughput (~165 Mt in 2023–24) force sellers into thinner margins.

ESG and financing filters

ESG-driven divestment and financing screens in 2024 have pushed some buyers to cut thermal coal positions, narrowing the buyer pool and increasing negotiating leverage of remaining customers; extended credit and ESG due diligence lengthen sales cycles and raise transaction costs. Metallurgical coal demand remains more resilient but faces growing scrutiny.

- Reduced buyer pool → higher customer power

- Longer sales cycles from ESG/credit checks

- Met coal resilient but under rising scrutiny

Switching and regional options

Buyers can pivot among Australian, Indonesian, Russian (variable) and US suppliers, with 2024 seaborne flows roughly Indonesia 350–400 Mt and Australia ~200 Mt, making regional choice sensitive to geopolitics and freight. Freight arbitrage (Panamax/Handy rates shifting US$5–15/t) often offsets FOB gaps, while blending (10–20% grade mixes) lowers reliance on any single producer, keeping seller pricing in check.

- Regional supply mix: Indonesia ~350–400 Mt, Australia ~200 Mt

- Freight swing: US$5–15/t

- Blending flexibility: 10–20%

Index-linked buyers, ESG, freight arbitrage boost bargaining; spot ~35%

Concentrated, sophisticated buyers (utilities, steel mills, traders) use index-linked pricing and multi-sourcing to extract concessions, raising bargaining power vs Whitehaven. Quality specs, inspection tightening in 2024 and ESG screens increase transaction costs and shift volumes to shorter contracts; spot share ~35% in 2024. Freight arbitrage (US$5–15/t) and regional supply (IDN 350–400 Mt, AUS ~200 Mt) keep seller pricing constrained.

| Metric | 2024 Value |

|---|---|

| Spot share | ~35% |

| Port of Newcastle | ~165 Mt (2023–24) |

| Freight swing | US$5–15/t |

What You See Is What You Get

Whitehaven Coal Porter's Five Forces Analysis

This preview shows the complete Porter's Five Forces analysis of Whitehaven Coal and is exactly the same professionally formatted document you will receive after purchase. There are no placeholders or mockups—downloadable and ready for immediate use. The analysis covers competitive rivalry, supplier and buyer power, threats of entry and substitution, and strategic implications tailored to Whitehaven Coal.

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Whitehaven Coal faces strong supplier and regulatory pressures, intense buyer bargaining in thermal coal markets, and moderate threat from substitutes as energy transition accelerates; rivalry among incumbents remains heated. This snapshot highlights key dynamics but only scratches the surface. Unlock the full Porter's Five Forces Analysis for force-by-force ratings, visuals, and strategic implications to inform investment or strategy.

Suppliers Bargaining Power

Concentrated critical inputs

Heavy equipment OEMs (Caterpillar, Komatsu), explosives supplier Orica and a small set of rail/port operators dominate Australia’s coal corridors, giving them pricing leverage; Port of Newcastle handled roughly 150 million tonnes of coal in 2024, creating capacity constraints for train paths and berths. Switching suppliers requires delays, re-approvals and retraining, raising costs and limiting negotiating flexibility for Whitehaven.

Labor and contractor leverage

Skilled mining labour and specialist contractors are scarce in regional NSW, tightening suppliers' leverage and forcing Whitehaven to bid up for talent; mining full‑time average earnings were about AUD 2,690/week in May 2024 (ABS). Enterprise agreements and strict safety standards raise baseline costs and contractor rates, and labour actions or shortages can halt production schedules. Whitehaven pays observable premiums to attract and retain critical crews.

Energy and diesel volatility

Diesel and electricity are major input costs for Whitehaven; Brent crude averaged about US$86/bbl in 2024, contributing to elevated diesel landed costs and Australian retail diesel averaging near A$1.60/L in 2024. Limited onsite fuel or grid substitutes means short-term exposure remains high. Logistics fuel surcharges amplified spikes, at times adding up to c.15% to transport bills in 2024. Hedging mitigates but cannot fully neutralize sudden cost shocks.

Infrastructure gatekeepers

Rail network owners and port terminals act as throughput bottlenecks for Whitehaven; 2024 take-or-pay rail and berthing contracts shift volume risk back to miners and limit pricing leverage. Negotiating better terms is hard without credible alternative routes, and 2024 congestion and maintenance windows increased vessel queueing, curtailing shipments and flexibility.

- Bottleneck suppliers: rail + terminals constrain capacity

- Contract risk: take-or-pay shifts volume risk to miners

- Leverage: few credible alternative routes

- 2024 impact: congestion/maintenance raised queue times and cut shipments

Geology and blasting consumables

Geology at Whitehaven drives drill-and-blast inputs, wear-part turnover and ground support consumption, making demand site-specific; OEM parts and certified explosives have few substitutes and are subject to state explosives regulation, with typical supply lead times of weeks and strict safety compliance that limit rapid supplier switching, embedding moderate structural supplier power.

- Geology-driven demand

- Limited substitutes: OEM parts, certified explosives

- Lead times: weeks

- Safety/regulation constrains switching

Supplier power tight as Port Newcastle hits 150 Mt, diesel and labour up

Few heavy‑equipment OEMs, explosives firms and rail/port operators give suppliers pricing leverage; Port of Newcastle handled ~150 Mt coal in 2024, tightening capacity. Labour and contractors are scarce—mining avg earnings ~A$2,690/week (May 2024)—raising costs. Energy costs (Brent ~US$86/bbl; diesel ~A$1.60/L in 2024) and take‑or‑pay rail contracts keep supplier power elevated.

| Metric | 2024 Value |

|---|---|

| Port Newcastle throughput | ~150 Mt |

| Brent crude | ~US$86/bbl |

| Diesel retail AUS | ~A$1.60/L |

| Mining avg earnings (May) | A$2,690/week |

What is included in the product

Uncovers key drivers of competition, customer influence, and market entry risks tailored to Whitehaven Coal, detailing each Porter’s force with industry data and strategic commentary; evaluates supplier and buyer power, threats from substitutes and new entrants, and identifies disruptive forces and defensive dynamics to inform investor and corporate strategy.

One-sheet Porter's Five Forces for Whitehaven Coal—quickly spot supplier, buyer, entrant, substitute and rivalry pressures to relieve strategic blind spots and export slides-ready insights for faster, confident decision-making.

Customers Bargaining Power

Concentrated Asian buyers

Utilities, steel mills and trading houses in Japan, Korea, Taiwan and India are concentrated and sophisticated buyers that benchmark purchases to transparent indices such as Platts and ICE for both metallurgical and thermal coal. Their scale enables multi-sourcing and the negotiation of stringent contract terms, volume discounts and short notice windows. This concentration significantly elevates buyer bargaining power against suppliers like Whitehaven Coal.

Specification sensitivity

Buyers demand tight specs on energy, ash, sulfur and coking properties, pressuring Whitehaven to sustain QA systems and sampling protocols; in 2024 seaborne buyers tightened inspections amid market volatility. Off-spec cargoes face discounts or rejection, commonly ranging from low single-digit to double-digit percent penalties per industry trade reports. Higher-quality met coal earns premia but invites stringent contractual penalties for deviations, raising quality-control costs for Whitehaven.

Contracting mix dynamics

Contracting mix dynamics: a blend of long-, medium- and spot contracts shifts leverage to buyers; in weak markets buyers pushed shorter tenors and index-linked pricing, with spot share rising to ~35% in 2024. Destination flexibility and volume optionality (cargo re-direction) favor buyers. Take-or-pay logistics and Port of Newcastle throughput (~165 Mt in 2023–24) force sellers into thinner margins.

ESG and financing filters

ESG-driven divestment and financing screens in 2024 have pushed some buyers to cut thermal coal positions, narrowing the buyer pool and increasing negotiating leverage of remaining customers; extended credit and ESG due diligence lengthen sales cycles and raise transaction costs. Metallurgical coal demand remains more resilient but faces growing scrutiny.

- Reduced buyer pool → higher customer power

- Longer sales cycles from ESG/credit checks

- Met coal resilient but under rising scrutiny

Switching and regional options

Buyers can pivot among Australian, Indonesian, Russian (variable) and US suppliers, with 2024 seaborne flows roughly Indonesia 350–400 Mt and Australia ~200 Mt, making regional choice sensitive to geopolitics and freight. Freight arbitrage (Panamax/Handy rates shifting US$5–15/t) often offsets FOB gaps, while blending (10–20% grade mixes) lowers reliance on any single producer, keeping seller pricing in check.

- Regional supply mix: Indonesia ~350–400 Mt, Australia ~200 Mt

- Freight swing: US$5–15/t

- Blending flexibility: 10–20%

Index-linked buyers, ESG, freight arbitrage boost bargaining; spot ~35%

Concentrated, sophisticated buyers (utilities, steel mills, traders) use index-linked pricing and multi-sourcing to extract concessions, raising bargaining power vs Whitehaven. Quality specs, inspection tightening in 2024 and ESG screens increase transaction costs and shift volumes to shorter contracts; spot share ~35% in 2024. Freight arbitrage (US$5–15/t) and regional supply (IDN 350–400 Mt, AUS ~200 Mt) keep seller pricing constrained.

| Metric | 2024 Value |

|---|---|

| Spot share | ~35% |

| Port of Newcastle | ~165 Mt (2023–24) |

| Freight swing | US$5–15/t |

What You See Is What You Get

Whitehaven Coal Porter's Five Forces Analysis

This preview shows the complete Porter's Five Forces analysis of Whitehaven Coal and is exactly the same professionally formatted document you will receive after purchase. There are no placeholders or mockups—downloadable and ready for immediate use. The analysis covers competitive rivalry, supplier and buyer power, threats of entry and substitution, and strategic implications tailored to Whitehaven Coal.

Original: $10.00

-65%$10.00

$3.50Description

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Whitehaven Coal faces strong supplier and regulatory pressures, intense buyer bargaining in thermal coal markets, and moderate threat from substitutes as energy transition accelerates; rivalry among incumbents remains heated. This snapshot highlights key dynamics but only scratches the surface. Unlock the full Porter's Five Forces Analysis for force-by-force ratings, visuals, and strategic implications to inform investment or strategy.

Suppliers Bargaining Power

Concentrated critical inputs

Heavy equipment OEMs (Caterpillar, Komatsu), explosives supplier Orica and a small set of rail/port operators dominate Australia’s coal corridors, giving them pricing leverage; Port of Newcastle handled roughly 150 million tonnes of coal in 2024, creating capacity constraints for train paths and berths. Switching suppliers requires delays, re-approvals and retraining, raising costs and limiting negotiating flexibility for Whitehaven.

Labor and contractor leverage

Skilled mining labour and specialist contractors are scarce in regional NSW, tightening suppliers' leverage and forcing Whitehaven to bid up for talent; mining full‑time average earnings were about AUD 2,690/week in May 2024 (ABS). Enterprise agreements and strict safety standards raise baseline costs and contractor rates, and labour actions or shortages can halt production schedules. Whitehaven pays observable premiums to attract and retain critical crews.

Energy and diesel volatility

Diesel and electricity are major input costs for Whitehaven; Brent crude averaged about US$86/bbl in 2024, contributing to elevated diesel landed costs and Australian retail diesel averaging near A$1.60/L in 2024. Limited onsite fuel or grid substitutes means short-term exposure remains high. Logistics fuel surcharges amplified spikes, at times adding up to c.15% to transport bills in 2024. Hedging mitigates but cannot fully neutralize sudden cost shocks.

Infrastructure gatekeepers

Rail network owners and port terminals act as throughput bottlenecks for Whitehaven; 2024 take-or-pay rail and berthing contracts shift volume risk back to miners and limit pricing leverage. Negotiating better terms is hard without credible alternative routes, and 2024 congestion and maintenance windows increased vessel queueing, curtailing shipments and flexibility.

- Bottleneck suppliers: rail + terminals constrain capacity

- Contract risk: take-or-pay shifts volume risk to miners

- Leverage: few credible alternative routes

- 2024 impact: congestion/maintenance raised queue times and cut shipments

Geology and blasting consumables

Geology at Whitehaven drives drill-and-blast inputs, wear-part turnover and ground support consumption, making demand site-specific; OEM parts and certified explosives have few substitutes and are subject to state explosives regulation, with typical supply lead times of weeks and strict safety compliance that limit rapid supplier switching, embedding moderate structural supplier power.

- Geology-driven demand

- Limited substitutes: OEM parts, certified explosives

- Lead times: weeks

- Safety/regulation constrains switching

Supplier power tight as Port Newcastle hits 150 Mt, diesel and labour up

Few heavy‑equipment OEMs, explosives firms and rail/port operators give suppliers pricing leverage; Port of Newcastle handled ~150 Mt coal in 2024, tightening capacity. Labour and contractors are scarce—mining avg earnings ~A$2,690/week (May 2024)—raising costs. Energy costs (Brent ~US$86/bbl; diesel ~A$1.60/L in 2024) and take‑or‑pay rail contracts keep supplier power elevated.

| Metric | 2024 Value |

|---|---|

| Port Newcastle throughput | ~150 Mt |

| Brent crude | ~US$86/bbl |

| Diesel retail AUS | ~A$1.60/L |

| Mining avg earnings (May) | A$2,690/week |

What is included in the product

Uncovers key drivers of competition, customer influence, and market entry risks tailored to Whitehaven Coal, detailing each Porter’s force with industry data and strategic commentary; evaluates supplier and buyer power, threats from substitutes and new entrants, and identifies disruptive forces and defensive dynamics to inform investor and corporate strategy.

One-sheet Porter's Five Forces for Whitehaven Coal—quickly spot supplier, buyer, entrant, substitute and rivalry pressures to relieve strategic blind spots and export slides-ready insights for faster, confident decision-making.

Customers Bargaining Power

Concentrated Asian buyers

Utilities, steel mills and trading houses in Japan, Korea, Taiwan and India are concentrated and sophisticated buyers that benchmark purchases to transparent indices such as Platts and ICE for both metallurgical and thermal coal. Their scale enables multi-sourcing and the negotiation of stringent contract terms, volume discounts and short notice windows. This concentration significantly elevates buyer bargaining power against suppliers like Whitehaven Coal.

Specification sensitivity

Buyers demand tight specs on energy, ash, sulfur and coking properties, pressuring Whitehaven to sustain QA systems and sampling protocols; in 2024 seaborne buyers tightened inspections amid market volatility. Off-spec cargoes face discounts or rejection, commonly ranging from low single-digit to double-digit percent penalties per industry trade reports. Higher-quality met coal earns premia but invites stringent contractual penalties for deviations, raising quality-control costs for Whitehaven.

Contracting mix dynamics

Contracting mix dynamics: a blend of long-, medium- and spot contracts shifts leverage to buyers; in weak markets buyers pushed shorter tenors and index-linked pricing, with spot share rising to ~35% in 2024. Destination flexibility and volume optionality (cargo re-direction) favor buyers. Take-or-pay logistics and Port of Newcastle throughput (~165 Mt in 2023–24) force sellers into thinner margins.

ESG and financing filters

ESG-driven divestment and financing screens in 2024 have pushed some buyers to cut thermal coal positions, narrowing the buyer pool and increasing negotiating leverage of remaining customers; extended credit and ESG due diligence lengthen sales cycles and raise transaction costs. Metallurgical coal demand remains more resilient but faces growing scrutiny.

- Reduced buyer pool → higher customer power

- Longer sales cycles from ESG/credit checks

- Met coal resilient but under rising scrutiny

Switching and regional options

Buyers can pivot among Australian, Indonesian, Russian (variable) and US suppliers, with 2024 seaborne flows roughly Indonesia 350–400 Mt and Australia ~200 Mt, making regional choice sensitive to geopolitics and freight. Freight arbitrage (Panamax/Handy rates shifting US$5–15/t) often offsets FOB gaps, while blending (10–20% grade mixes) lowers reliance on any single producer, keeping seller pricing in check.

- Regional supply mix: Indonesia ~350–400 Mt, Australia ~200 Mt

- Freight swing: US$5–15/t

- Blending flexibility: 10–20%

Index-linked buyers, ESG, freight arbitrage boost bargaining; spot ~35%

Concentrated, sophisticated buyers (utilities, steel mills, traders) use index-linked pricing and multi-sourcing to extract concessions, raising bargaining power vs Whitehaven. Quality specs, inspection tightening in 2024 and ESG screens increase transaction costs and shift volumes to shorter contracts; spot share ~35% in 2024. Freight arbitrage (US$5–15/t) and regional supply (IDN 350–400 Mt, AUS ~200 Mt) keep seller pricing constrained.

| Metric | 2024 Value |

|---|---|

| Spot share | ~35% |

| Port of Newcastle | ~165 Mt (2023–24) |

| Freight swing | US$5–15/t |

What You See Is What You Get

Whitehaven Coal Porter's Five Forces Analysis

This preview shows the complete Porter's Five Forces analysis of Whitehaven Coal and is exactly the same professionally formatted document you will receive after purchase. There are no placeholders or mockups—downloadable and ready for immediate use. The analysis covers competitive rivalry, supplier and buyer power, threats of entry and substitution, and strategic implications tailored to Whitehaven Coal.