WHSmith PESTLE Analysis

Plan Smarter. Present Sharper. Compete Stronger.

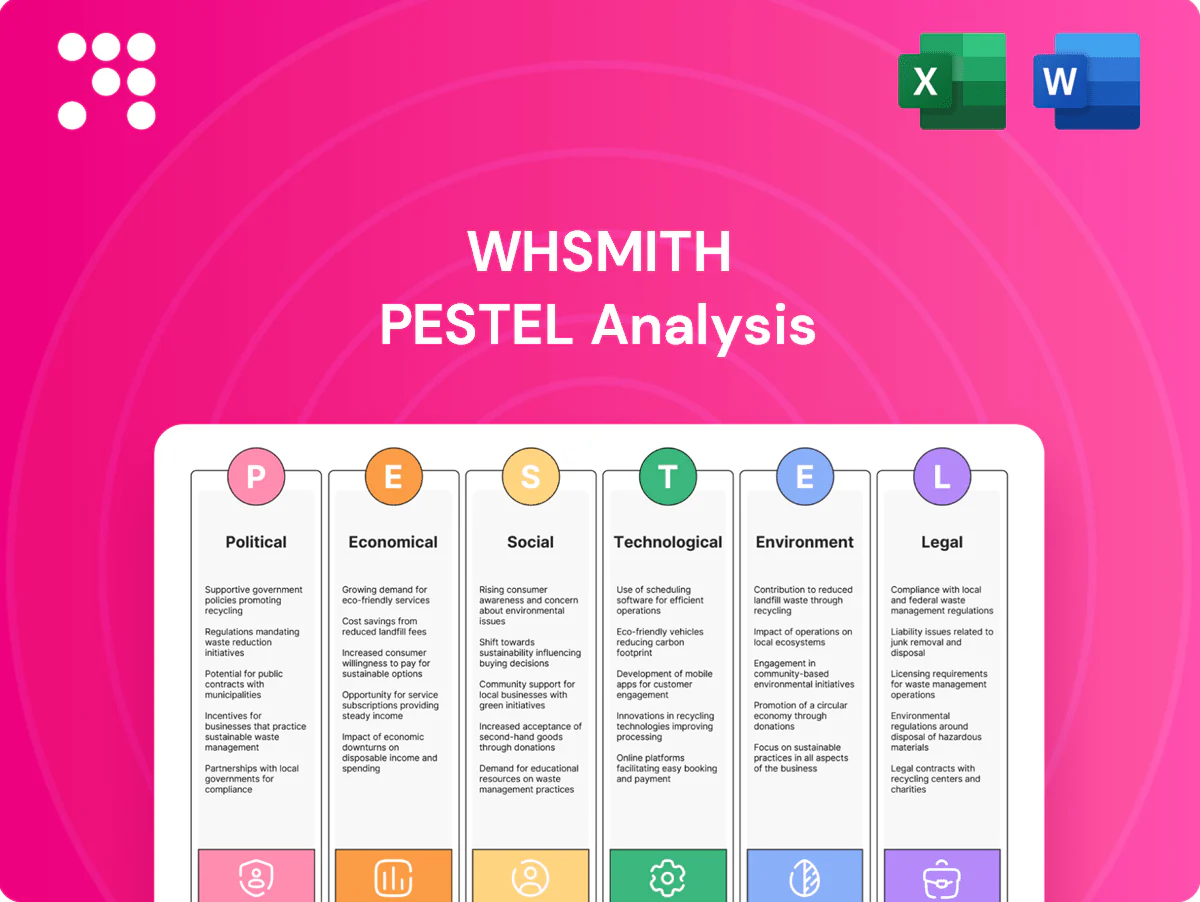

Gain a competitive edge with our PESTLE analysis of WHSmith. Explore how political, economic, social, technological, legal and environmental forces shape its strategy and risks. Ideal for investors, advisors and planners. Download the full, editable report now for instant, actionable insight.

Political factors

Aviation and transport policy shifts

Changes to airport slot rules, security protocols and rail franchising shift passenger flows and concession terms; UK air passenger volumes recovered to about 90% of 2019 levels by 2024, directly affecting WHSmith travel throughput. Tighter security or delays reduce dwell time and basket sizes, while transport infrastructure investment raises footfall and unit economics. Active engagement with transport authorities helps WHSmith anticipate operational impacts and renegotiate concessions.

Government procurement in hospitals

NHS policies shape WHSmiths' on-site retail mix, pricing and vendor access across hospital estates, driven by an NHS England budget of roughly £170bn in 2024/25 and procurement frameworks covering thousands of sites. Shifts toward healthier ranges and vending restrictions have materially reshaped category sales in hospitals. Tender cycles (typically 3–5 years) and framework agreements boost revenue visibility but increase compliance and audit burdens. Clear ESG credentials improve competitiveness in award decisions.

Trade, customs, and import policies

Post‑Brexit rules of origin and renewed customs checks have increased lead times and costs for books, stationery and confectionery, raising the risk of stockouts in WHSmith travel locations. Any tariff shocks or spikes in paperwork can compress already-tight margins and force price adjustments. Diversifying suppliers and nearshoring reduces disruption risk, while efficient customs brokerage and inventory buffers preserve availability in fast‑moving travel outlets.

Taxation and business rates

UK business rates and international sales taxes materially compress WHSmith high-street margins; business rates typically represent c.3–4% of retail sales costs for UK retailers and rose after 2022 revaluations, shifting returns toward travel and airport formats where per-passenger fees and concession uplifts are higher.

- Policy reliefs shift investment mix

- Airport concession fees vs local taxes

- Lobbying reduces rate exposure

- Property optimisation cuts effective rates

Geopolitical stability and security

Geopolitical instability—terror threats, conflicts and diplomatic tensions—can sharply cut travel demand or shift footfall overnight; 2024 passenger volumes rebounded to near‑prepandemic levels per IATA, making WHSmith’s travel estate sensitive to shocks. Currency swings after events complicate pricing for international sites and margins. Contingency plans, insured coverage and geographic diversification are essential for continuity and staff safety.

- Travel sensitivity: near‑prepandemic passenger volumes (2024)

- Currency risk: FX-driven margin pressure on international sales

- Operational safeguards: contingency plans, staff safety protocols

- Risk mitigation: insurance and geographic diversification

Airport and hospital retail shift as passengers hit ~90% and NHS tenders rise

Airport passenger volumes recovered to ~90% of 2019 levels by 2024, shifting sales toward travel formats; NHS England budget ~£170bn (2024/25) dictates hospital retail mix and tenders; business rates at c.3–4% of retail sales compress high‑street margins; post‑Brexit customs and geopolitical shocks increase costs and operational risk for travel outlets.

| Factor | 2024/25 metric | Impact |

|---|---|---|

| Airport traffic | ~90% of 2019 | Higher travel throughput |

| NHS policy | £170bn budget | Tender-driven sales mix |

| Business rates | 3–4% of sales | Margin pressure |

| Customs/FX | Post‑Brexit checks | Higher lead times/costs |

What is included in the product

Explores how macro-environmental factors uniquely affect WHSmith across Political, Economic, Social, Technological, Environmental and Legal dimensions, with each category expanded into detailed sub-points and business-specific examples. Every section is data-backed and forward-looking to support executives, consultants and investors in identifying threats, opportunities and scenario planning.

A clean, summarized WHSmith PESTLE that’s visually segmented by category for quick interpretation at a glance, ideal for dropping straight into presentations or strategy sessions. It uses clear language so teams can align fast on external risks and market positioning.

Economic factors

Travel demand and macro cycles

Passenger volumes, which IATA forecast to grow about 4.8% in 2024 and roughly 3.6% in 2025 as traffic approaches 2019 levels, closely track GDP, tourism trends and corporate travel budgets and thus drive WHSmith airport sales. Downturns compress discretionary purchases of books and impulse items, lowering per-passenger concession revenue. Recoveries typically restore spend per passenger and enable concession expansion, so WHSmith ties inventory and staffing to IATA/airport growth forecasts.

Inflation and input cost pressures

Rising wholesale costs (which surged c.8–10% across 2022–23 and remained elevated into 2024) plus wage growth (regular pay rose roughly 6% in 2023 then cooled) and higher utilities continue to squeeze margins across WHSmiths small high‑street and travel footprints. Price elasticity differs by category: essentials and grab‑and‑go show stronger resilience than discretionary reads. Active mix management and supplier renegotiations are therefore critical to protect margins. Implementing targeted price ladders preserves value perception while recovering cost increases.

Foreign exchange exposure

WHSmiths multi‑country operations expose its ~£1.08bn FY2024 group revenue to translation and transaction FX risks, with sterling moves materially affecting reported earnings and the cost of imported travel retail stock. Currency swings can compress margins in imported categories, so the group uses hedging and local sourcing to reduce volatility. Pricing governance must balance competitiveness in travel hubs with margin protection across markets.

Consumer confidence and spending power

Weak consumer confidence in 2024 curtailed impulse buys and premium stationery upgrades, pressuring non-essential margins; WHSmith reported group revenue of £1.46bn in FY2024, highlighting reliance on volume retention.

Promotions, bundles and entry-price ranges sustained transactions while upselling travel essentials helped offset softer discretionary categories; monitoring basket composition enables rapid assortment shifts.

- Confidence dip → fewer impulse buys

- Promotions/bundles sustain volumes

- Upsell travel essentials to protect sales

- Track basket mix for agile merchandising

Labour market tightness

Labour market tightness (UK unemployment ~3.8% in 2024; job vacancies ~1.0m) raises recruitment and retention costs for WHSmith as extended-hours staffing increases shift premiums and turnover. Minimum wage uplifts pressure store P&Ls, while targeted training and multi‑skilling raise productivity per labour hour. Automation (self‑checkout, stock robots) can partially offset wage inflation and reduce hourly headcount.

- Higher recruitment/retention costs

- Minimum wage pressure on margins

- Training boosts productivity

- Automation offsets wages

Airport and hospital retail shift as passengers hit ~90% and NHS tenders rise

Airport passenger growth (IATA +4.8% 2024, +3.6% 2025) drives travel retail; weaker confidence cut impulse spend, pressuring non‑essentials. Wholesale costs rose c.8–10% 2022–24 and wages grew ~6% in 2023, squeezing margins; promotions and mix shifts mitigate. Group revenue £1.46bn FY2024 and UK unemployment ~3.8% raise labour costs; hedging, local sourcing and automation reduce FX and wage risk.

| Metric | Figure | Impact |

|---|---|---|

| Passenger growth | +4.8% (2024), +3.6% (2025) | Drives travel sales |

| Wholesale costs | +8–10% | Margin pressure |

| Group revenue | £1.46bn FY2024 | Volume dependence |

| Unemployment (UK) | ~3.8% (2024) | Higher labour costs |

Preview Before You Purchase

WHSmith PESTLE Analysis

The WHSmith PESTLE Analysis preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use. The layout, content, and structure visible are exactly what you’ll download immediately after buying. No placeholders or teasers—this is the final, professionally structured file.

Plan Smarter. Present Sharper. Compete Stronger.

Gain a competitive edge with our PESTLE analysis of WHSmith. Explore how political, economic, social, technological, legal and environmental forces shape its strategy and risks. Ideal for investors, advisors and planners. Download the full, editable report now for instant, actionable insight.

Political factors

Aviation and transport policy shifts

Changes to airport slot rules, security protocols and rail franchising shift passenger flows and concession terms; UK air passenger volumes recovered to about 90% of 2019 levels by 2024, directly affecting WHSmith travel throughput. Tighter security or delays reduce dwell time and basket sizes, while transport infrastructure investment raises footfall and unit economics. Active engagement with transport authorities helps WHSmith anticipate operational impacts and renegotiate concessions.

Government procurement in hospitals

NHS policies shape WHSmiths' on-site retail mix, pricing and vendor access across hospital estates, driven by an NHS England budget of roughly £170bn in 2024/25 and procurement frameworks covering thousands of sites. Shifts toward healthier ranges and vending restrictions have materially reshaped category sales in hospitals. Tender cycles (typically 3–5 years) and framework agreements boost revenue visibility but increase compliance and audit burdens. Clear ESG credentials improve competitiveness in award decisions.

Trade, customs, and import policies

Post‑Brexit rules of origin and renewed customs checks have increased lead times and costs for books, stationery and confectionery, raising the risk of stockouts in WHSmith travel locations. Any tariff shocks or spikes in paperwork can compress already-tight margins and force price adjustments. Diversifying suppliers and nearshoring reduces disruption risk, while efficient customs brokerage and inventory buffers preserve availability in fast‑moving travel outlets.

Taxation and business rates

UK business rates and international sales taxes materially compress WHSmith high-street margins; business rates typically represent c.3–4% of retail sales costs for UK retailers and rose after 2022 revaluations, shifting returns toward travel and airport formats where per-passenger fees and concession uplifts are higher.

- Policy reliefs shift investment mix

- Airport concession fees vs local taxes

- Lobbying reduces rate exposure

- Property optimisation cuts effective rates

Geopolitical stability and security

Geopolitical instability—terror threats, conflicts and diplomatic tensions—can sharply cut travel demand or shift footfall overnight; 2024 passenger volumes rebounded to near‑prepandemic levels per IATA, making WHSmith’s travel estate sensitive to shocks. Currency swings after events complicate pricing for international sites and margins. Contingency plans, insured coverage and geographic diversification are essential for continuity and staff safety.

- Travel sensitivity: near‑prepandemic passenger volumes (2024)

- Currency risk: FX-driven margin pressure on international sales

- Operational safeguards: contingency plans, staff safety protocols

- Risk mitigation: insurance and geographic diversification

Airport and hospital retail shift as passengers hit ~90% and NHS tenders rise

Airport passenger volumes recovered to ~90% of 2019 levels by 2024, shifting sales toward travel formats; NHS England budget ~£170bn (2024/25) dictates hospital retail mix and tenders; business rates at c.3–4% of retail sales compress high‑street margins; post‑Brexit customs and geopolitical shocks increase costs and operational risk for travel outlets.

| Factor | 2024/25 metric | Impact |

|---|---|---|

| Airport traffic | ~90% of 2019 | Higher travel throughput |

| NHS policy | £170bn budget | Tender-driven sales mix |

| Business rates | 3–4% of sales | Margin pressure |

| Customs/FX | Post‑Brexit checks | Higher lead times/costs |

What is included in the product

Explores how macro-environmental factors uniquely affect WHSmith across Political, Economic, Social, Technological, Environmental and Legal dimensions, with each category expanded into detailed sub-points and business-specific examples. Every section is data-backed and forward-looking to support executives, consultants and investors in identifying threats, opportunities and scenario planning.

A clean, summarized WHSmith PESTLE that’s visually segmented by category for quick interpretation at a glance, ideal for dropping straight into presentations or strategy sessions. It uses clear language so teams can align fast on external risks and market positioning.

Economic factors

Travel demand and macro cycles

Passenger volumes, which IATA forecast to grow about 4.8% in 2024 and roughly 3.6% in 2025 as traffic approaches 2019 levels, closely track GDP, tourism trends and corporate travel budgets and thus drive WHSmith airport sales. Downturns compress discretionary purchases of books and impulse items, lowering per-passenger concession revenue. Recoveries typically restore spend per passenger and enable concession expansion, so WHSmith ties inventory and staffing to IATA/airport growth forecasts.

Inflation and input cost pressures

Rising wholesale costs (which surged c.8–10% across 2022–23 and remained elevated into 2024) plus wage growth (regular pay rose roughly 6% in 2023 then cooled) and higher utilities continue to squeeze margins across WHSmiths small high‑street and travel footprints. Price elasticity differs by category: essentials and grab‑and‑go show stronger resilience than discretionary reads. Active mix management and supplier renegotiations are therefore critical to protect margins. Implementing targeted price ladders preserves value perception while recovering cost increases.

Foreign exchange exposure

WHSmiths multi‑country operations expose its ~£1.08bn FY2024 group revenue to translation and transaction FX risks, with sterling moves materially affecting reported earnings and the cost of imported travel retail stock. Currency swings can compress margins in imported categories, so the group uses hedging and local sourcing to reduce volatility. Pricing governance must balance competitiveness in travel hubs with margin protection across markets.

Consumer confidence and spending power

Weak consumer confidence in 2024 curtailed impulse buys and premium stationery upgrades, pressuring non-essential margins; WHSmith reported group revenue of £1.46bn in FY2024, highlighting reliance on volume retention.

Promotions, bundles and entry-price ranges sustained transactions while upselling travel essentials helped offset softer discretionary categories; monitoring basket composition enables rapid assortment shifts.

- Confidence dip → fewer impulse buys

- Promotions/bundles sustain volumes

- Upsell travel essentials to protect sales

- Track basket mix for agile merchandising

Labour market tightness

Labour market tightness (UK unemployment ~3.8% in 2024; job vacancies ~1.0m) raises recruitment and retention costs for WHSmith as extended-hours staffing increases shift premiums and turnover. Minimum wage uplifts pressure store P&Ls, while targeted training and multi‑skilling raise productivity per labour hour. Automation (self‑checkout, stock robots) can partially offset wage inflation and reduce hourly headcount.

- Higher recruitment/retention costs

- Minimum wage pressure on margins

- Training boosts productivity

- Automation offsets wages

Airport and hospital retail shift as passengers hit ~90% and NHS tenders rise

Airport passenger growth (IATA +4.8% 2024, +3.6% 2025) drives travel retail; weaker confidence cut impulse spend, pressuring non‑essentials. Wholesale costs rose c.8–10% 2022–24 and wages grew ~6% in 2023, squeezing margins; promotions and mix shifts mitigate. Group revenue £1.46bn FY2024 and UK unemployment ~3.8% raise labour costs; hedging, local sourcing and automation reduce FX and wage risk.

| Metric | Figure | Impact |

|---|---|---|

| Passenger growth | +4.8% (2024), +3.6% (2025) | Drives travel sales |

| Wholesale costs | +8–10% | Margin pressure |

| Group revenue | £1.46bn FY2024 | Volume dependence |

| Unemployment (UK) | ~3.8% (2024) | Higher labour costs |

Preview Before You Purchase

WHSmith PESTLE Analysis

The WHSmith PESTLE Analysis preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use. The layout, content, and structure visible are exactly what you’ll download immediately after buying. No placeholders or teasers—this is the final, professionally structured file.

Description

Plan Smarter. Present Sharper. Compete Stronger.

Gain a competitive edge with our PESTLE analysis of WHSmith. Explore how political, economic, social, technological, legal and environmental forces shape its strategy and risks. Ideal for investors, advisors and planners. Download the full, editable report now for instant, actionable insight.

Political factors

Aviation and transport policy shifts

Changes to airport slot rules, security protocols and rail franchising shift passenger flows and concession terms; UK air passenger volumes recovered to about 90% of 2019 levels by 2024, directly affecting WHSmith travel throughput. Tighter security or delays reduce dwell time and basket sizes, while transport infrastructure investment raises footfall and unit economics. Active engagement with transport authorities helps WHSmith anticipate operational impacts and renegotiate concessions.

Government procurement in hospitals

NHS policies shape WHSmiths' on-site retail mix, pricing and vendor access across hospital estates, driven by an NHS England budget of roughly £170bn in 2024/25 and procurement frameworks covering thousands of sites. Shifts toward healthier ranges and vending restrictions have materially reshaped category sales in hospitals. Tender cycles (typically 3–5 years) and framework agreements boost revenue visibility but increase compliance and audit burdens. Clear ESG credentials improve competitiveness in award decisions.

Trade, customs, and import policies

Post‑Brexit rules of origin and renewed customs checks have increased lead times and costs for books, stationery and confectionery, raising the risk of stockouts in WHSmith travel locations. Any tariff shocks or spikes in paperwork can compress already-tight margins and force price adjustments. Diversifying suppliers and nearshoring reduces disruption risk, while efficient customs brokerage and inventory buffers preserve availability in fast‑moving travel outlets.

Taxation and business rates

UK business rates and international sales taxes materially compress WHSmith high-street margins; business rates typically represent c.3–4% of retail sales costs for UK retailers and rose after 2022 revaluations, shifting returns toward travel and airport formats where per-passenger fees and concession uplifts are higher.

- Policy reliefs shift investment mix

- Airport concession fees vs local taxes

- Lobbying reduces rate exposure

- Property optimisation cuts effective rates

Geopolitical stability and security

Geopolitical instability—terror threats, conflicts and diplomatic tensions—can sharply cut travel demand or shift footfall overnight; 2024 passenger volumes rebounded to near‑prepandemic levels per IATA, making WHSmith’s travel estate sensitive to shocks. Currency swings after events complicate pricing for international sites and margins. Contingency plans, insured coverage and geographic diversification are essential for continuity and staff safety.

- Travel sensitivity: near‑prepandemic passenger volumes (2024)

- Currency risk: FX-driven margin pressure on international sales

- Operational safeguards: contingency plans, staff safety protocols

- Risk mitigation: insurance and geographic diversification

Airport and hospital retail shift as passengers hit ~90% and NHS tenders rise

Airport passenger volumes recovered to ~90% of 2019 levels by 2024, shifting sales toward travel formats; NHS England budget ~£170bn (2024/25) dictates hospital retail mix and tenders; business rates at c.3–4% of retail sales compress high‑street margins; post‑Brexit customs and geopolitical shocks increase costs and operational risk for travel outlets.

| Factor | 2024/25 metric | Impact |

|---|---|---|

| Airport traffic | ~90% of 2019 | Higher travel throughput |

| NHS policy | £170bn budget | Tender-driven sales mix |

| Business rates | 3–4% of sales | Margin pressure |

| Customs/FX | Post‑Brexit checks | Higher lead times/costs |

What is included in the product

Explores how macro-environmental factors uniquely affect WHSmith across Political, Economic, Social, Technological, Environmental and Legal dimensions, with each category expanded into detailed sub-points and business-specific examples. Every section is data-backed and forward-looking to support executives, consultants and investors in identifying threats, opportunities and scenario planning.

A clean, summarized WHSmith PESTLE that’s visually segmented by category for quick interpretation at a glance, ideal for dropping straight into presentations or strategy sessions. It uses clear language so teams can align fast on external risks and market positioning.

Economic factors

Travel demand and macro cycles

Passenger volumes, which IATA forecast to grow about 4.8% in 2024 and roughly 3.6% in 2025 as traffic approaches 2019 levels, closely track GDP, tourism trends and corporate travel budgets and thus drive WHSmith airport sales. Downturns compress discretionary purchases of books and impulse items, lowering per-passenger concession revenue. Recoveries typically restore spend per passenger and enable concession expansion, so WHSmith ties inventory and staffing to IATA/airport growth forecasts.

Inflation and input cost pressures

Rising wholesale costs (which surged c.8–10% across 2022–23 and remained elevated into 2024) plus wage growth (regular pay rose roughly 6% in 2023 then cooled) and higher utilities continue to squeeze margins across WHSmiths small high‑street and travel footprints. Price elasticity differs by category: essentials and grab‑and‑go show stronger resilience than discretionary reads. Active mix management and supplier renegotiations are therefore critical to protect margins. Implementing targeted price ladders preserves value perception while recovering cost increases.

Foreign exchange exposure

WHSmiths multi‑country operations expose its ~£1.08bn FY2024 group revenue to translation and transaction FX risks, with sterling moves materially affecting reported earnings and the cost of imported travel retail stock. Currency swings can compress margins in imported categories, so the group uses hedging and local sourcing to reduce volatility. Pricing governance must balance competitiveness in travel hubs with margin protection across markets.

Consumer confidence and spending power

Weak consumer confidence in 2024 curtailed impulse buys and premium stationery upgrades, pressuring non-essential margins; WHSmith reported group revenue of £1.46bn in FY2024, highlighting reliance on volume retention.

Promotions, bundles and entry-price ranges sustained transactions while upselling travel essentials helped offset softer discretionary categories; monitoring basket composition enables rapid assortment shifts.

- Confidence dip → fewer impulse buys

- Promotions/bundles sustain volumes

- Upsell travel essentials to protect sales

- Track basket mix for agile merchandising

Labour market tightness

Labour market tightness (UK unemployment ~3.8% in 2024; job vacancies ~1.0m) raises recruitment and retention costs for WHSmith as extended-hours staffing increases shift premiums and turnover. Minimum wage uplifts pressure store P&Ls, while targeted training and multi‑skilling raise productivity per labour hour. Automation (self‑checkout, stock robots) can partially offset wage inflation and reduce hourly headcount.

- Higher recruitment/retention costs

- Minimum wage pressure on margins

- Training boosts productivity

- Automation offsets wages

Airport and hospital retail shift as passengers hit ~90% and NHS tenders rise

Airport passenger growth (IATA +4.8% 2024, +3.6% 2025) drives travel retail; weaker confidence cut impulse spend, pressuring non‑essentials. Wholesale costs rose c.8–10% 2022–24 and wages grew ~6% in 2023, squeezing margins; promotions and mix shifts mitigate. Group revenue £1.46bn FY2024 and UK unemployment ~3.8% raise labour costs; hedging, local sourcing and automation reduce FX and wage risk.

| Metric | Figure | Impact |

|---|---|---|

| Passenger growth | +4.8% (2024), +3.6% (2025) | Drives travel sales |

| Wholesale costs | +8–10% | Margin pressure |

| Group revenue | £1.46bn FY2024 | Volume dependence |

| Unemployment (UK) | ~3.8% (2024) | Higher labour costs |

Preview Before You Purchase

WHSmith PESTLE Analysis

The WHSmith PESTLE Analysis preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use. The layout, content, and structure visible are exactly what you’ll download immediately after buying. No placeholders or teasers—this is the final, professionally structured file.