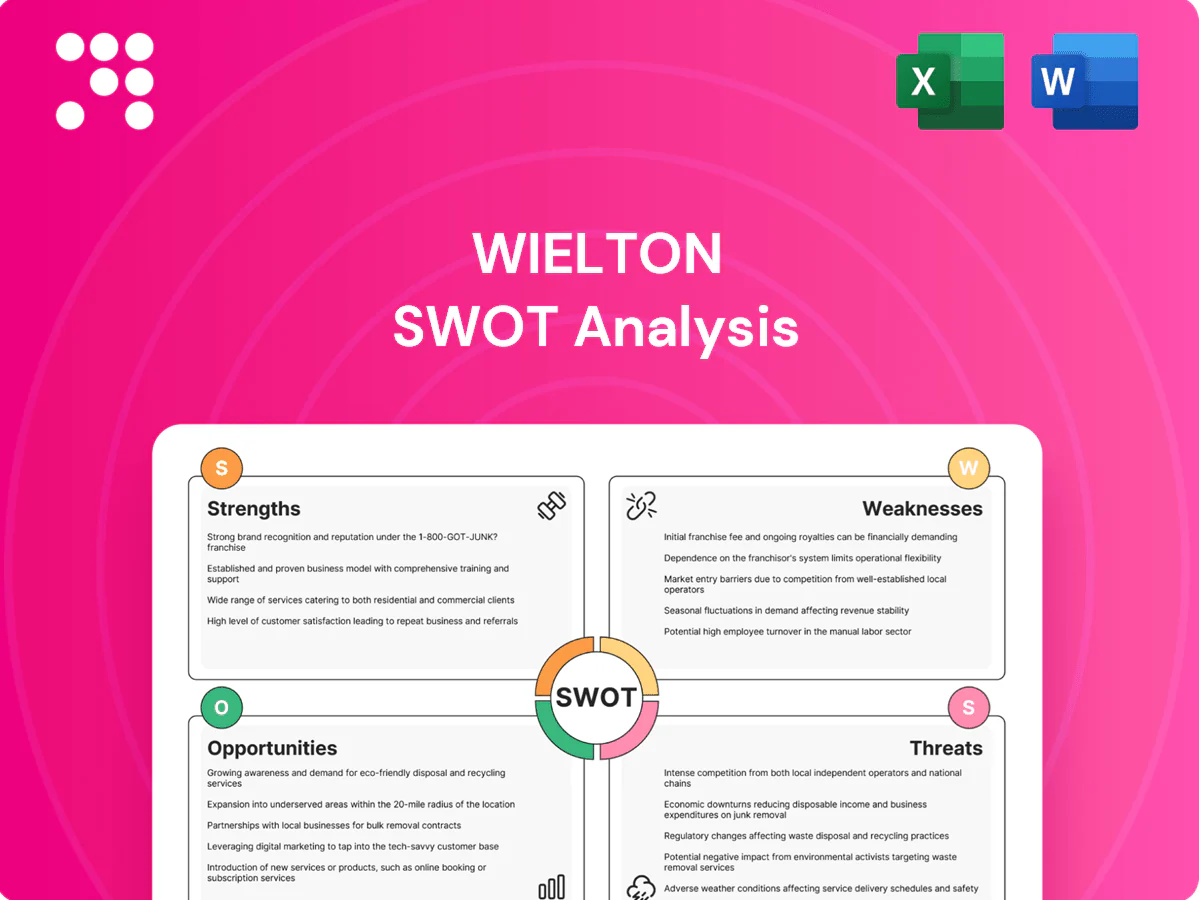

Wielton SWOT Analysis

Your Strategic Toolkit Starts Here

Wielton’s SWOT highlights resilient manufacturing capabilities, expanding EU footprint, and supply-chain pressures that could affect margins; it’s essential reading for stakeholders tracking commercial vehicle markets. Want the full strategic picture and financial context? Purchase the complete SWOT to get a professionally formatted Word report plus an editable Excel matrix for planning and presentations.

Strengths

Leading European manufacturer

Wielton, a leading European manufacturer present in over 30 countries, reported roughly PLN 3.1bn revenue in 2023, giving it strong bargaining power with suppliers and large fleets for semi-trailers, trailers and tippers. Market leadership drives tender wins and pan‑European fleet agreements, while scale-related learning effects and reputational reliability compress unit costs and shorten sales cycles in repeat segments.

Broad, specialized product portfolio

Wielton’s portfolio spans logistics, construction, infrastructure and agriculture, diversifying revenue and mitigating sector cyclicality while exporting to 30+ countries. Modular platforms and multiple variants let the company match payload, terrain and duty-cycle needs across fleets. Tailorable specifications increase success on complex tenders, supporting higher order conversion. Breadth enables cross-selling and fleet-standardization across customer lifecycles, backed by a workforce of over 2,000.

Extensive international sales and service network

Wielton’s international sales and service network spans 30+ markets, enabling distribution partners to expand reach and lower go-to-market costs. Dense service coverage across its 7 production and service sites improves uptime and total cost of ownership for operators. Proximity to customers speeds delivery and parts availability while local presence aids compliance with country-specific homologation rules.

Engineering and customization capability

Wielton's in-house design team enables rapid configuration to customer use cases, supporting bespoke trailers that leverage the firm's durability, weight-optimization and body-integration know-how—advantages reinforced by Wielton's Warsaw Stock Exchange listing and export-oriented model (exports ≈70% of output). Custom projects yield higher margins and stronger client retention, while service-partner feedback drives iterative product improvements and shorter development cycles.

- In-house design: rapid configuration

- Durability & weight optimization: product differentiation

- Custom projects: higher margins & loyalty

- Service feedback: continuous improvement

Cost-competitive CEE manufacturing base

Wielton leverages a cost-competitive CEE manufacturing base (seven plants across Poland and neighbouring CEE sites) that underpins pricing flexibility and supports competitive bids in price-sensitive tenders; Eurostat 2023 shows Poland manufacturing unit labour costs around 45% of Germany, aiding margin resilience and buffering input shocks via PLN/EUR currency advantages and EU-linked logistics for timely deliveries.

- 7 plants in CEE

- ~45% Poland vs DE unit labour cost (Eurostat 2023)

- High export/EU access enabling timely delivery

- Currency buffer vs EUR/USD for input price shocks

European trailer leader: PLN 3.1bn revenue, 70% exports, CEE cost edge

Wielton is a leading European trailer manufacturer active in 30+ countries with 2023 revenue ≈PLN 3.1bn and exports ≈70%, supporting strong tender power and fleet contracts. Seven CEE plants and a workforce >2,000 underpin cost-competitive production; Eurostat 2023 shows Poland unit labour costs ≈45% of Germany. In-house design and modular platforms enable tailored, higher‑margin projects and faster sales cycles.

| Metric | Value | Source |

|---|---|---|

| 2023 revenue | PLN 3.1bn | Wielton 2023 |

| Export share | ≈70% | Wielton |

| Plants | 7 (CEE) | Company data |

| Workforce | >2,000 | Company data |

| PL vs DE ULC | ≈45% | Eurostat 2023 |

What is included in the product

Provides a concise SWOT assessment of Wielton’s internal capabilities and external market forces, highlighting strengths, weaknesses, growth opportunities, and competitive risks shaping the company’s strategic outlook.

Provides a concise SWOT matrix for Wielton that quickly identifies strengths, weaknesses, opportunities and threats, enabling fast strategic alignment and stakeholder-ready summaries.

Weaknesses

High cyclical exposure

Wielton faces high cyclical exposure as demand tracks freight volumes, construction activity and capex cycles; as a WSE-listed trailer maker its fixed-cost footprint creates strong operating leverage in downturns, magnifying margin swings. Order volatility complicates capacity planning and inventory management, while residual values typically weaken in recessions, pressuring pricing for new units.

Geographic and segment concentration

Wielton remains highly Europe-centric, with roughly PLN 2.66bn revenue in 2023 and an estimated >75% of sales tied to EU markets, limiting diversification versus global peers. Limited penetration in North America and parts of Asia constrains scale and growth upside. Heavy reliance on trailer segments—over 80% of group sales—increases sensitivity to cyclical swings. EU political or regulatory shifts can therefore disproportionately affect results.

Raw material cost sensitivity

Steel, aluminum and components (axles, tires) drive Wielton’s COGS; with LME aluminum ~2,300 USD/t in mid‑2024 and European HRC roughly 700–900 USD/t, input swings can rapidly inflate costs. Price escalation clauses have lagged during sudden spikes, and partial hedging leaves margin exposure—Wielton reported ~PLN 4.6bn revenue in 2023, heightening impact on profits. Concentration of key suppliers for axles and tires reduces negotiating leverage and recovery speed.

Working capital intensity

Build-to-order cycles force Wielton to hold inventory buffers and carry extended receivables, so cash conversion weakens during rapid growth or supply-chain delays, increasing days sales outstanding and days inventory held.

- Dealer financing raises balance-sheet exposure

- Extended credit terms elevate working-capital needs

- Higher working capital ties liquidity and raises financing costs

Resource gap vs larger rivals

Wielton faces a resource gap versus larger rivals such as Schmitz Cargobull and Krone, which constrains R&D and digital investment; keeping pace in telematics, lightweight materials and aerodynamics can strain available capital and engineering bandwidth. Marketing reach and global service coverage remain narrower, and scale disadvantages limit competitiveness for mega-fleet tenders that favor high-volume suppliers.

- Smaller R&D/digital budgets vs market leaders

- Narrower marketing and service network

- Capacity/scale limits for mega-fleet contracts

Cyclical trailers business: fixed-costs amplify margin swings; EU concentration limits growth

Wielton’s high cyclicality and fixed-cost base magnify margin swings during downturns and create order volatility that strains capacity planning. EU concentration (>75% sales) and limited North America/Asia penetration cap growth and raise regulatory risk. Input-cost sensitivity (steel/aluminum, axles, tires) and supplier concentration expose margins and working capital.

| Metric | Value |

|---|---|

| 2023 revenue | PLN 4.6bn / PLN 2.66bn (sources) |

| EU sales share | >75% |

| Trailer share | >80% |

Preview Before You Purchase

Wielton SWOT Analysis

This is the actual Wielton SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full report; buying unlocks the complete, editable version. You’re viewing a live preview of the real file, ready for immediate download after checkout.

Your Strategic Toolkit Starts Here

Wielton’s SWOT highlights resilient manufacturing capabilities, expanding EU footprint, and supply-chain pressures that could affect margins; it’s essential reading for stakeholders tracking commercial vehicle markets. Want the full strategic picture and financial context? Purchase the complete SWOT to get a professionally formatted Word report plus an editable Excel matrix for planning and presentations.

Strengths

Leading European manufacturer

Wielton, a leading European manufacturer present in over 30 countries, reported roughly PLN 3.1bn revenue in 2023, giving it strong bargaining power with suppliers and large fleets for semi-trailers, trailers and tippers. Market leadership drives tender wins and pan‑European fleet agreements, while scale-related learning effects and reputational reliability compress unit costs and shorten sales cycles in repeat segments.

Broad, specialized product portfolio

Wielton’s portfolio spans logistics, construction, infrastructure and agriculture, diversifying revenue and mitigating sector cyclicality while exporting to 30+ countries. Modular platforms and multiple variants let the company match payload, terrain and duty-cycle needs across fleets. Tailorable specifications increase success on complex tenders, supporting higher order conversion. Breadth enables cross-selling and fleet-standardization across customer lifecycles, backed by a workforce of over 2,000.

Extensive international sales and service network

Wielton’s international sales and service network spans 30+ markets, enabling distribution partners to expand reach and lower go-to-market costs. Dense service coverage across its 7 production and service sites improves uptime and total cost of ownership for operators. Proximity to customers speeds delivery and parts availability while local presence aids compliance with country-specific homologation rules.

Engineering and customization capability

Wielton's in-house design team enables rapid configuration to customer use cases, supporting bespoke trailers that leverage the firm's durability, weight-optimization and body-integration know-how—advantages reinforced by Wielton's Warsaw Stock Exchange listing and export-oriented model (exports ≈70% of output). Custom projects yield higher margins and stronger client retention, while service-partner feedback drives iterative product improvements and shorter development cycles.

- In-house design: rapid configuration

- Durability & weight optimization: product differentiation

- Custom projects: higher margins & loyalty

- Service feedback: continuous improvement

Cost-competitive CEE manufacturing base

Wielton leverages a cost-competitive CEE manufacturing base (seven plants across Poland and neighbouring CEE sites) that underpins pricing flexibility and supports competitive bids in price-sensitive tenders; Eurostat 2023 shows Poland manufacturing unit labour costs around 45% of Germany, aiding margin resilience and buffering input shocks via PLN/EUR currency advantages and EU-linked logistics for timely deliveries.

- 7 plants in CEE

- ~45% Poland vs DE unit labour cost (Eurostat 2023)

- High export/EU access enabling timely delivery

- Currency buffer vs EUR/USD for input price shocks

European trailer leader: PLN 3.1bn revenue, 70% exports, CEE cost edge

Wielton is a leading European trailer manufacturer active in 30+ countries with 2023 revenue ≈PLN 3.1bn and exports ≈70%, supporting strong tender power and fleet contracts. Seven CEE plants and a workforce >2,000 underpin cost-competitive production; Eurostat 2023 shows Poland unit labour costs ≈45% of Germany. In-house design and modular platforms enable tailored, higher‑margin projects and faster sales cycles.

| Metric | Value | Source |

|---|---|---|

| 2023 revenue | PLN 3.1bn | Wielton 2023 |

| Export share | ≈70% | Wielton |

| Plants | 7 (CEE) | Company data |

| Workforce | >2,000 | Company data |

| PL vs DE ULC | ≈45% | Eurostat 2023 |

What is included in the product

Provides a concise SWOT assessment of Wielton’s internal capabilities and external market forces, highlighting strengths, weaknesses, growth opportunities, and competitive risks shaping the company’s strategic outlook.

Provides a concise SWOT matrix for Wielton that quickly identifies strengths, weaknesses, opportunities and threats, enabling fast strategic alignment and stakeholder-ready summaries.

Weaknesses

High cyclical exposure

Wielton faces high cyclical exposure as demand tracks freight volumes, construction activity and capex cycles; as a WSE-listed trailer maker its fixed-cost footprint creates strong operating leverage in downturns, magnifying margin swings. Order volatility complicates capacity planning and inventory management, while residual values typically weaken in recessions, pressuring pricing for new units.

Geographic and segment concentration

Wielton remains highly Europe-centric, with roughly PLN 2.66bn revenue in 2023 and an estimated >75% of sales tied to EU markets, limiting diversification versus global peers. Limited penetration in North America and parts of Asia constrains scale and growth upside. Heavy reliance on trailer segments—over 80% of group sales—increases sensitivity to cyclical swings. EU political or regulatory shifts can therefore disproportionately affect results.

Raw material cost sensitivity

Steel, aluminum and components (axles, tires) drive Wielton’s COGS; with LME aluminum ~2,300 USD/t in mid‑2024 and European HRC roughly 700–900 USD/t, input swings can rapidly inflate costs. Price escalation clauses have lagged during sudden spikes, and partial hedging leaves margin exposure—Wielton reported ~PLN 4.6bn revenue in 2023, heightening impact on profits. Concentration of key suppliers for axles and tires reduces negotiating leverage and recovery speed.

Working capital intensity

Build-to-order cycles force Wielton to hold inventory buffers and carry extended receivables, so cash conversion weakens during rapid growth or supply-chain delays, increasing days sales outstanding and days inventory held.

- Dealer financing raises balance-sheet exposure

- Extended credit terms elevate working-capital needs

- Higher working capital ties liquidity and raises financing costs

Resource gap vs larger rivals

Wielton faces a resource gap versus larger rivals such as Schmitz Cargobull and Krone, which constrains R&D and digital investment; keeping pace in telematics, lightweight materials and aerodynamics can strain available capital and engineering bandwidth. Marketing reach and global service coverage remain narrower, and scale disadvantages limit competitiveness for mega-fleet tenders that favor high-volume suppliers.

- Smaller R&D/digital budgets vs market leaders

- Narrower marketing and service network

- Capacity/scale limits for mega-fleet contracts

Cyclical trailers business: fixed-costs amplify margin swings; EU concentration limits growth

Wielton’s high cyclicality and fixed-cost base magnify margin swings during downturns and create order volatility that strains capacity planning. EU concentration (>75% sales) and limited North America/Asia penetration cap growth and raise regulatory risk. Input-cost sensitivity (steel/aluminum, axles, tires) and supplier concentration expose margins and working capital.

| Metric | Value |

|---|---|

| 2023 revenue | PLN 4.6bn / PLN 2.66bn (sources) |

| EU sales share | >75% |

| Trailer share | >80% |

Preview Before You Purchase

Wielton SWOT Analysis

This is the actual Wielton SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full report; buying unlocks the complete, editable version. You’re viewing a live preview of the real file, ready for immediate download after checkout.

Original: $10.00

-65%$10.00

$3.50Description

Your Strategic Toolkit Starts Here

Wielton’s SWOT highlights resilient manufacturing capabilities, expanding EU footprint, and supply-chain pressures that could affect margins; it’s essential reading for stakeholders tracking commercial vehicle markets. Want the full strategic picture and financial context? Purchase the complete SWOT to get a professionally formatted Word report plus an editable Excel matrix for planning and presentations.

Strengths

Leading European manufacturer

Wielton, a leading European manufacturer present in over 30 countries, reported roughly PLN 3.1bn revenue in 2023, giving it strong bargaining power with suppliers and large fleets for semi-trailers, trailers and tippers. Market leadership drives tender wins and pan‑European fleet agreements, while scale-related learning effects and reputational reliability compress unit costs and shorten sales cycles in repeat segments.

Broad, specialized product portfolio

Wielton’s portfolio spans logistics, construction, infrastructure and agriculture, diversifying revenue and mitigating sector cyclicality while exporting to 30+ countries. Modular platforms and multiple variants let the company match payload, terrain and duty-cycle needs across fleets. Tailorable specifications increase success on complex tenders, supporting higher order conversion. Breadth enables cross-selling and fleet-standardization across customer lifecycles, backed by a workforce of over 2,000.

Extensive international sales and service network

Wielton’s international sales and service network spans 30+ markets, enabling distribution partners to expand reach and lower go-to-market costs. Dense service coverage across its 7 production and service sites improves uptime and total cost of ownership for operators. Proximity to customers speeds delivery and parts availability while local presence aids compliance with country-specific homologation rules.

Engineering and customization capability

Wielton's in-house design team enables rapid configuration to customer use cases, supporting bespoke trailers that leverage the firm's durability, weight-optimization and body-integration know-how—advantages reinforced by Wielton's Warsaw Stock Exchange listing and export-oriented model (exports ≈70% of output). Custom projects yield higher margins and stronger client retention, while service-partner feedback drives iterative product improvements and shorter development cycles.

- In-house design: rapid configuration

- Durability & weight optimization: product differentiation

- Custom projects: higher margins & loyalty

- Service feedback: continuous improvement

Cost-competitive CEE manufacturing base

Wielton leverages a cost-competitive CEE manufacturing base (seven plants across Poland and neighbouring CEE sites) that underpins pricing flexibility and supports competitive bids in price-sensitive tenders; Eurostat 2023 shows Poland manufacturing unit labour costs around 45% of Germany, aiding margin resilience and buffering input shocks via PLN/EUR currency advantages and EU-linked logistics for timely deliveries.

- 7 plants in CEE

- ~45% Poland vs DE unit labour cost (Eurostat 2023)

- High export/EU access enabling timely delivery

- Currency buffer vs EUR/USD for input price shocks

European trailer leader: PLN 3.1bn revenue, 70% exports, CEE cost edge

Wielton is a leading European trailer manufacturer active in 30+ countries with 2023 revenue ≈PLN 3.1bn and exports ≈70%, supporting strong tender power and fleet contracts. Seven CEE plants and a workforce >2,000 underpin cost-competitive production; Eurostat 2023 shows Poland unit labour costs ≈45% of Germany. In-house design and modular platforms enable tailored, higher‑margin projects and faster sales cycles.

| Metric | Value | Source |

|---|---|---|

| 2023 revenue | PLN 3.1bn | Wielton 2023 |

| Export share | ≈70% | Wielton |

| Plants | 7 (CEE) | Company data |

| Workforce | >2,000 | Company data |

| PL vs DE ULC | ≈45% | Eurostat 2023 |

What is included in the product

Provides a concise SWOT assessment of Wielton’s internal capabilities and external market forces, highlighting strengths, weaknesses, growth opportunities, and competitive risks shaping the company’s strategic outlook.

Provides a concise SWOT matrix for Wielton that quickly identifies strengths, weaknesses, opportunities and threats, enabling fast strategic alignment and stakeholder-ready summaries.

Weaknesses

High cyclical exposure

Wielton faces high cyclical exposure as demand tracks freight volumes, construction activity and capex cycles; as a WSE-listed trailer maker its fixed-cost footprint creates strong operating leverage in downturns, magnifying margin swings. Order volatility complicates capacity planning and inventory management, while residual values typically weaken in recessions, pressuring pricing for new units.

Geographic and segment concentration

Wielton remains highly Europe-centric, with roughly PLN 2.66bn revenue in 2023 and an estimated >75% of sales tied to EU markets, limiting diversification versus global peers. Limited penetration in North America and parts of Asia constrains scale and growth upside. Heavy reliance on trailer segments—over 80% of group sales—increases sensitivity to cyclical swings. EU political or regulatory shifts can therefore disproportionately affect results.

Raw material cost sensitivity

Steel, aluminum and components (axles, tires) drive Wielton’s COGS; with LME aluminum ~2,300 USD/t in mid‑2024 and European HRC roughly 700–900 USD/t, input swings can rapidly inflate costs. Price escalation clauses have lagged during sudden spikes, and partial hedging leaves margin exposure—Wielton reported ~PLN 4.6bn revenue in 2023, heightening impact on profits. Concentration of key suppliers for axles and tires reduces negotiating leverage and recovery speed.

Working capital intensity

Build-to-order cycles force Wielton to hold inventory buffers and carry extended receivables, so cash conversion weakens during rapid growth or supply-chain delays, increasing days sales outstanding and days inventory held.

- Dealer financing raises balance-sheet exposure

- Extended credit terms elevate working-capital needs

- Higher working capital ties liquidity and raises financing costs

Resource gap vs larger rivals

Wielton faces a resource gap versus larger rivals such as Schmitz Cargobull and Krone, which constrains R&D and digital investment; keeping pace in telematics, lightweight materials and aerodynamics can strain available capital and engineering bandwidth. Marketing reach and global service coverage remain narrower, and scale disadvantages limit competitiveness for mega-fleet tenders that favor high-volume suppliers.

- Smaller R&D/digital budgets vs market leaders

- Narrower marketing and service network

- Capacity/scale limits for mega-fleet contracts

Cyclical trailers business: fixed-costs amplify margin swings; EU concentration limits growth

Wielton’s high cyclicality and fixed-cost base magnify margin swings during downturns and create order volatility that strains capacity planning. EU concentration (>75% sales) and limited North America/Asia penetration cap growth and raise regulatory risk. Input-cost sensitivity (steel/aluminum, axles, tires) and supplier concentration expose margins and working capital.

| Metric | Value |

|---|---|

| 2023 revenue | PLN 4.6bn / PLN 2.66bn (sources) |

| EU sales share | >75% |

| Trailer share | >80% |

Preview Before You Purchase

Wielton SWOT Analysis

This is the actual Wielton SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full report; buying unlocks the complete, editable version. You’re viewing a live preview of the real file, ready for immediate download after checkout.