Willi-Food PESTLE Analysis

Plan Smarter. Present Sharper. Compete Stronger.

Our Willi-Food PESTLE Analysis reveals how political shifts, economic trends, social preferences, technological advances, legal changes, and environmental pressures are reshaping the company's prospects. Packed with actionable insights, it’s ideal for investors and strategists. Buy the full report to access the complete, editable analysis and make smarter decisions now.

Political factors

Geopolitics & regional security

Since the Oct 7, 2023 state of war Israel’s security environment has caused intermittent closures at ports such as Ashdod and Haifa, disrupting logistics and consumer demand; war‑risk insurance and rerouting costs spiked in 2023–24, with some corridors seeing six‑figure per‑voyage premiums, while government emergency regulations have prioritized food and fuel allocations, and stability periods quickly restore predictable import flows and retail continuity.

Trade policy & import tariffs

Import duties, quotas and preferential deals directly shape landed costs—changes in 2023–24 drove landed-cost swings of roughly 5–20% across staple categories in several markets. Sudden shifts in trade ties with major origins (eg China, Ukraine, Brazil) have repriced categories overnight, forcing margin resets. Tariff exemptions for staples can improve competitiveness versus local producers; continuous monitoring enables agile sourcing and dynamic pricing.

Government subsidies & food programs

State subsidies and food programs materially reshape category demand: the EU Common Agricultural Policy commits €387 billion for 2021–27, directing volumes and prices that affect suppliers like Willi-Food.

Public procurement and voucher schemes—driving school, hospital and social purchases—can preferentially shift volumes toward compliant products and labels.

FAO reported about 768 million undernourished people (2023), so policy emphasis on domestic production and program alignment can unlock scale, visibility and stable revenue streams for firms meeting procurement criteria.

Customs efficiency & border controls

Customs clearance speed directly impacts Willi-Food freshness metrics and working capital cycles, as perishable windows shorten with each day of delay; heightened inspections for origin labeling or safety can add 24–72 hours to throughput. Digitized pre-clearance programs cut dwell time and demurrage, while strong broker relationships mitigate peak congestion risks and expedite releases.

- Perishable exposure: delays reduce shelf-life

- Inspections: +24–72h typical

- Digitization: lowers dwell/demurrage

- Broker ties: critical in peak weeks

Diplomacy & compliance risk

Sanctions and politically exposed suppliers raise counterparty risk for Willi-Food; OFAC and EU consolidated lists exceeded 10,000 entries combined in 2024, increasing screening needs. Rapid regulatory updates triggered supplier requalification waves in 2024, forcing 20–40% higher audit frequency in high‑risk corridors. Diplomatic shifts can abruptly close or open sourcing lanes; robust compliance frameworks protect continuity and reputation.

- Sanctions: 10,000+ listed entries (2024)

- Requalifications: +20–40% audits in high‑risk corridors (2024)

- Risk: politically exposed suppliers elevate counterparty exposure

- Mitigation: strong compliance preserves supply continuity and brand

War, tariffs and sanctions spike food supply costs, landed‑costs up 5–20%

Since Oct 7, 2023 war, port closures (Ashdod, Haifa) raised war‑risk premiums and disrupted logistics, increasing costs and demand volatility.

Trade policy shifts and tariffs in 2023–24 moved landed costs 5–20%; EU CAP €387bn (2021–27) and 768M undernourished (FAO 2023) shape subsidies and procurement.

Sanctions lists 10,000+ entries (OFAC+EU, 2024) raised screening/audits, driving 20–40% more requalifications in high‑risk corridors.

| Metric | Value |

|---|---|

| Landed‑cost swings | 5–20% |

| EU CAP | €387bn (2021–27) |

| Undernourished | 768M (2023) |

| Sanctions list | 10,000+ (2024) |

What is included in the product

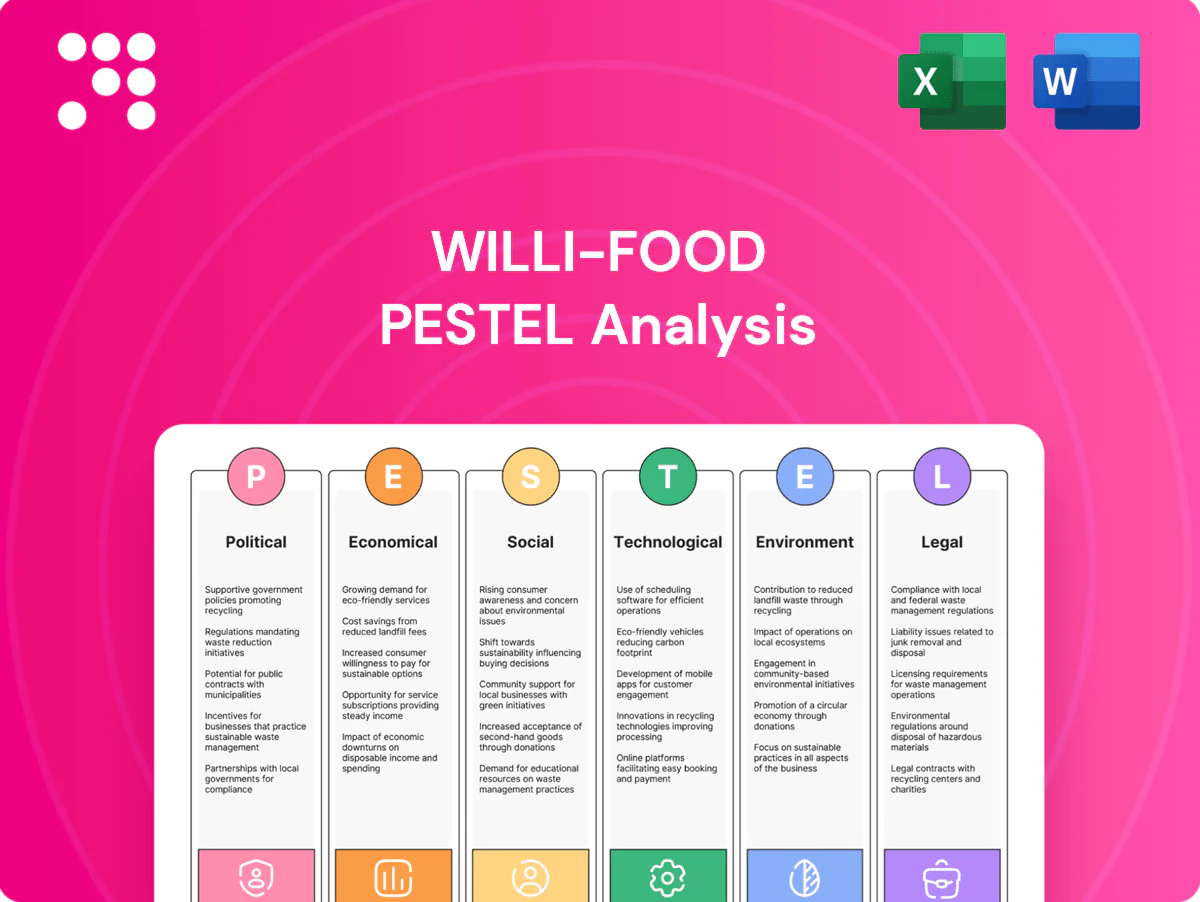

Explores how macro-environmental factors uniquely affect Willi-Food across Political, Economic, Social, Technological, Environmental and Legal dimensions, with data‑backed trends and region‑specific examples; designed for executives, consultants and investors to identify risks, opportunities and strategic responses, and delivered in a clean, forward‑looking format ready for business plans, decks or scenario planning.

A concise, visually segmented PESTLE summary for Willi‑Food that simplifies external risk assessment, is editable for regional or business‑line notes, and is easily shareable for meetings, presentations, and cross‑team alignment.

Economic factors

Consumer purchasing power

Inflation (US CPI 2024 3.4%) and higher benchmark rates (Fed funds ~5.25–5.5% mid‑2025) drive consumers to trade up in staples or down on discretionary categories, shifting category mix. Real wage stagnation in many advanced economies has boosted demand for value lines versus premium imports. Exchange‑rate passthrough (commonly 10–30% for food imports) raises shelf prices and elasticity, so assortment balancing—mixing private label, mid, and premium tiers—preserves volumes through cycles.

FX volatility & hedging

Shekel volatility versus USD/EUR causes immediate repricing of imports, with annual swings of roughly 5–10% in recent 2023–25 periods impacting landed costs and pass-through pricing. Hedging and contractual currency clauses have stabilized margins but added 0.5–1.5 percentage points to operating costs through premiums and administrative expense. Timing of inventory buys can swing gross margin by several percentage points, so diversifying currency exposure reduces single-currency concentration risk and smooths P&L shocks.

Logistics costs & capacity

Global freight volatility and port capacity swings kept landed costs and lead times elevated—global container fleet reached about 28m TEU in 2024 while spot rates eased ~60% from 2021 peaks but remained above pre‑pandemic levels, extending lead times for some lanes. Cold‑chain needs raise unit cost sensitivity, adding refrigeration capex and 15–25% higher freight premiums on perishables. Consolidation and load optimization improved unit economics; multi‑port strategies reduced disruption risk and surcharge exposure.

Competitive intensity & private label

Retailer private labels, which reached about 18% of global grocery sales in 2024 (NielsenIQ), pressure pricing and claim more shelf space, forcing Willi-Food to absorb margin compression. Scale retailers leverage rebates and promo funding—top chains often secure 3–7% effective price support—sharpening competitive advantage. Willi-Food defends margin with differentiated SKUs, retailer exclusives and data-driven category management that strengthens bargaining power.

- private-label-share: 18% (2024)

- promo-funding-leverage: 3–7% price support

- differentiation: exclusive SKUs protect margins

- data-driven: category analytics boosts negotiation

Macroeconomic growth & confidence

Macroeconomic growth steers category mix: IMF estimated 2024 global GDP growth near 3.1% and weaker consumer sentiment shifts volumes toward staples while expansions lift indulgence and specialty lines; Conference Board US consumer confidence averaged about 102 in 2024. Inventory and promo cadence must track demand inflections; strict forecast discipline reduces obsolescence and write-offs.

- GDP 2024 ~3.1%

- US consumer confidence 2024 ~102

- Downturns favor staples

- Forecast discipline limits write-offs

War, tariffs and sanctions spike food supply costs, landed‑costs up 5–20%

Inflation (US CPI 2024 3.4%) and Fed rates (~5.25–5.5% mid‑2025) shift shoppers to value, boosting private‑label share and compressing premium volumes. Shekel swings ~5–10% (2023–25) and 10–30% passthrough on imports raise elasticity; hedging adds ~0.5–1.5pp to costs. Freight and cold‑chain premiums (15–25%) and private label at 18% (2024) pressure margins, so SKU mix and timing are critical.

| Metric | Value |

|---|---|

| US CPI 2024 | 3.4% |

| Fed funds mid‑2025 | 5.25–5.5% |

| Shekel volatility (2023–25) | 5–10% |

| Import passthrough | 10–30% |

| Hedging cost | +0.5–1.5pp |

| Freight/cold‑chain premium | 15–25% |

| Private‑label share 2024 | 18% |

Preview the Actual Deliverable

Willi-Food PESTLE Analysis

The Willi-Food PESTLE Analysis offers a concise, professionally structured review of political, economic, social, technological, legal, and environmental factors affecting the business. The preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use. No placeholders or teasers; download the final file immediately after checkout.

Plan Smarter. Present Sharper. Compete Stronger.

Our Willi-Food PESTLE Analysis reveals how political shifts, economic trends, social preferences, technological advances, legal changes, and environmental pressures are reshaping the company's prospects. Packed with actionable insights, it’s ideal for investors and strategists. Buy the full report to access the complete, editable analysis and make smarter decisions now.

Political factors

Geopolitics & regional security

Since the Oct 7, 2023 state of war Israel’s security environment has caused intermittent closures at ports such as Ashdod and Haifa, disrupting logistics and consumer demand; war‑risk insurance and rerouting costs spiked in 2023–24, with some corridors seeing six‑figure per‑voyage premiums, while government emergency regulations have prioritized food and fuel allocations, and stability periods quickly restore predictable import flows and retail continuity.

Trade policy & import tariffs

Import duties, quotas and preferential deals directly shape landed costs—changes in 2023–24 drove landed-cost swings of roughly 5–20% across staple categories in several markets. Sudden shifts in trade ties with major origins (eg China, Ukraine, Brazil) have repriced categories overnight, forcing margin resets. Tariff exemptions for staples can improve competitiveness versus local producers; continuous monitoring enables agile sourcing and dynamic pricing.

Government subsidies & food programs

State subsidies and food programs materially reshape category demand: the EU Common Agricultural Policy commits €387 billion for 2021–27, directing volumes and prices that affect suppliers like Willi-Food.

Public procurement and voucher schemes—driving school, hospital and social purchases—can preferentially shift volumes toward compliant products and labels.

FAO reported about 768 million undernourished people (2023), so policy emphasis on domestic production and program alignment can unlock scale, visibility and stable revenue streams for firms meeting procurement criteria.

Customs efficiency & border controls

Customs clearance speed directly impacts Willi-Food freshness metrics and working capital cycles, as perishable windows shorten with each day of delay; heightened inspections for origin labeling or safety can add 24–72 hours to throughput. Digitized pre-clearance programs cut dwell time and demurrage, while strong broker relationships mitigate peak congestion risks and expedite releases.

- Perishable exposure: delays reduce shelf-life

- Inspections: +24–72h typical

- Digitization: lowers dwell/demurrage

- Broker ties: critical in peak weeks

Diplomacy & compliance risk

Sanctions and politically exposed suppliers raise counterparty risk for Willi-Food; OFAC and EU consolidated lists exceeded 10,000 entries combined in 2024, increasing screening needs. Rapid regulatory updates triggered supplier requalification waves in 2024, forcing 20–40% higher audit frequency in high‑risk corridors. Diplomatic shifts can abruptly close or open sourcing lanes; robust compliance frameworks protect continuity and reputation.

- Sanctions: 10,000+ listed entries (2024)

- Requalifications: +20–40% audits in high‑risk corridors (2024)

- Risk: politically exposed suppliers elevate counterparty exposure

- Mitigation: strong compliance preserves supply continuity and brand

War, tariffs and sanctions spike food supply costs, landed‑costs up 5–20%

Since Oct 7, 2023 war, port closures (Ashdod, Haifa) raised war‑risk premiums and disrupted logistics, increasing costs and demand volatility.

Trade policy shifts and tariffs in 2023–24 moved landed costs 5–20%; EU CAP €387bn (2021–27) and 768M undernourished (FAO 2023) shape subsidies and procurement.

Sanctions lists 10,000+ entries (OFAC+EU, 2024) raised screening/audits, driving 20–40% more requalifications in high‑risk corridors.

| Metric | Value |

|---|---|

| Landed‑cost swings | 5–20% |

| EU CAP | €387bn (2021–27) |

| Undernourished | 768M (2023) |

| Sanctions list | 10,000+ (2024) |

What is included in the product

Explores how macro-environmental factors uniquely affect Willi-Food across Political, Economic, Social, Technological, Environmental and Legal dimensions, with data‑backed trends and region‑specific examples; designed for executives, consultants and investors to identify risks, opportunities and strategic responses, and delivered in a clean, forward‑looking format ready for business plans, decks or scenario planning.

A concise, visually segmented PESTLE summary for Willi‑Food that simplifies external risk assessment, is editable for regional or business‑line notes, and is easily shareable for meetings, presentations, and cross‑team alignment.

Economic factors

Consumer purchasing power

Inflation (US CPI 2024 3.4%) and higher benchmark rates (Fed funds ~5.25–5.5% mid‑2025) drive consumers to trade up in staples or down on discretionary categories, shifting category mix. Real wage stagnation in many advanced economies has boosted demand for value lines versus premium imports. Exchange‑rate passthrough (commonly 10–30% for food imports) raises shelf prices and elasticity, so assortment balancing—mixing private label, mid, and premium tiers—preserves volumes through cycles.

FX volatility & hedging

Shekel volatility versus USD/EUR causes immediate repricing of imports, with annual swings of roughly 5–10% in recent 2023–25 periods impacting landed costs and pass-through pricing. Hedging and contractual currency clauses have stabilized margins but added 0.5–1.5 percentage points to operating costs through premiums and administrative expense. Timing of inventory buys can swing gross margin by several percentage points, so diversifying currency exposure reduces single-currency concentration risk and smooths P&L shocks.

Logistics costs & capacity

Global freight volatility and port capacity swings kept landed costs and lead times elevated—global container fleet reached about 28m TEU in 2024 while spot rates eased ~60% from 2021 peaks but remained above pre‑pandemic levels, extending lead times for some lanes. Cold‑chain needs raise unit cost sensitivity, adding refrigeration capex and 15–25% higher freight premiums on perishables. Consolidation and load optimization improved unit economics; multi‑port strategies reduced disruption risk and surcharge exposure.

Competitive intensity & private label

Retailer private labels, which reached about 18% of global grocery sales in 2024 (NielsenIQ), pressure pricing and claim more shelf space, forcing Willi-Food to absorb margin compression. Scale retailers leverage rebates and promo funding—top chains often secure 3–7% effective price support—sharpening competitive advantage. Willi-Food defends margin with differentiated SKUs, retailer exclusives and data-driven category management that strengthens bargaining power.

- private-label-share: 18% (2024)

- promo-funding-leverage: 3–7% price support

- differentiation: exclusive SKUs protect margins

- data-driven: category analytics boosts negotiation

Macroeconomic growth & confidence

Macroeconomic growth steers category mix: IMF estimated 2024 global GDP growth near 3.1% and weaker consumer sentiment shifts volumes toward staples while expansions lift indulgence and specialty lines; Conference Board US consumer confidence averaged about 102 in 2024. Inventory and promo cadence must track demand inflections; strict forecast discipline reduces obsolescence and write-offs.

- GDP 2024 ~3.1%

- US consumer confidence 2024 ~102

- Downturns favor staples

- Forecast discipline limits write-offs

War, tariffs and sanctions spike food supply costs, landed‑costs up 5–20%

Inflation (US CPI 2024 3.4%) and Fed rates (~5.25–5.5% mid‑2025) shift shoppers to value, boosting private‑label share and compressing premium volumes. Shekel swings ~5–10% (2023–25) and 10–30% passthrough on imports raise elasticity; hedging adds ~0.5–1.5pp to costs. Freight and cold‑chain premiums (15–25%) and private label at 18% (2024) pressure margins, so SKU mix and timing are critical.

| Metric | Value |

|---|---|

| US CPI 2024 | 3.4% |

| Fed funds mid‑2025 | 5.25–5.5% |

| Shekel volatility (2023–25) | 5–10% |

| Import passthrough | 10–30% |

| Hedging cost | +0.5–1.5pp |

| Freight/cold‑chain premium | 15–25% |

| Private‑label share 2024 | 18% |

Preview the Actual Deliverable

Willi-Food PESTLE Analysis

The Willi-Food PESTLE Analysis offers a concise, professionally structured review of political, economic, social, technological, legal, and environmental factors affecting the business. The preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use. No placeholders or teasers; download the final file immediately after checkout.

Description

Plan Smarter. Present Sharper. Compete Stronger.

Our Willi-Food PESTLE Analysis reveals how political shifts, economic trends, social preferences, technological advances, legal changes, and environmental pressures are reshaping the company's prospects. Packed with actionable insights, it’s ideal for investors and strategists. Buy the full report to access the complete, editable analysis and make smarter decisions now.

Political factors

Geopolitics & regional security

Since the Oct 7, 2023 state of war Israel’s security environment has caused intermittent closures at ports such as Ashdod and Haifa, disrupting logistics and consumer demand; war‑risk insurance and rerouting costs spiked in 2023–24, with some corridors seeing six‑figure per‑voyage premiums, while government emergency regulations have prioritized food and fuel allocations, and stability periods quickly restore predictable import flows and retail continuity.

Trade policy & import tariffs

Import duties, quotas and preferential deals directly shape landed costs—changes in 2023–24 drove landed-cost swings of roughly 5–20% across staple categories in several markets. Sudden shifts in trade ties with major origins (eg China, Ukraine, Brazil) have repriced categories overnight, forcing margin resets. Tariff exemptions for staples can improve competitiveness versus local producers; continuous monitoring enables agile sourcing and dynamic pricing.

Government subsidies & food programs

State subsidies and food programs materially reshape category demand: the EU Common Agricultural Policy commits €387 billion for 2021–27, directing volumes and prices that affect suppliers like Willi-Food.

Public procurement and voucher schemes—driving school, hospital and social purchases—can preferentially shift volumes toward compliant products and labels.

FAO reported about 768 million undernourished people (2023), so policy emphasis on domestic production and program alignment can unlock scale, visibility and stable revenue streams for firms meeting procurement criteria.

Customs efficiency & border controls

Customs clearance speed directly impacts Willi-Food freshness metrics and working capital cycles, as perishable windows shorten with each day of delay; heightened inspections for origin labeling or safety can add 24–72 hours to throughput. Digitized pre-clearance programs cut dwell time and demurrage, while strong broker relationships mitigate peak congestion risks and expedite releases.

- Perishable exposure: delays reduce shelf-life

- Inspections: +24–72h typical

- Digitization: lowers dwell/demurrage

- Broker ties: critical in peak weeks

Diplomacy & compliance risk

Sanctions and politically exposed suppliers raise counterparty risk for Willi-Food; OFAC and EU consolidated lists exceeded 10,000 entries combined in 2024, increasing screening needs. Rapid regulatory updates triggered supplier requalification waves in 2024, forcing 20–40% higher audit frequency in high‑risk corridors. Diplomatic shifts can abruptly close or open sourcing lanes; robust compliance frameworks protect continuity and reputation.

- Sanctions: 10,000+ listed entries (2024)

- Requalifications: +20–40% audits in high‑risk corridors (2024)

- Risk: politically exposed suppliers elevate counterparty exposure

- Mitigation: strong compliance preserves supply continuity and brand

War, tariffs and sanctions spike food supply costs, landed‑costs up 5–20%

Since Oct 7, 2023 war, port closures (Ashdod, Haifa) raised war‑risk premiums and disrupted logistics, increasing costs and demand volatility.

Trade policy shifts and tariffs in 2023–24 moved landed costs 5–20%; EU CAP €387bn (2021–27) and 768M undernourished (FAO 2023) shape subsidies and procurement.

Sanctions lists 10,000+ entries (OFAC+EU, 2024) raised screening/audits, driving 20–40% more requalifications in high‑risk corridors.

| Metric | Value |

|---|---|

| Landed‑cost swings | 5–20% |

| EU CAP | €387bn (2021–27) |

| Undernourished | 768M (2023) |

| Sanctions list | 10,000+ (2024) |

What is included in the product

Explores how macro-environmental factors uniquely affect Willi-Food across Political, Economic, Social, Technological, Environmental and Legal dimensions, with data‑backed trends and region‑specific examples; designed for executives, consultants and investors to identify risks, opportunities and strategic responses, and delivered in a clean, forward‑looking format ready for business plans, decks or scenario planning.

A concise, visually segmented PESTLE summary for Willi‑Food that simplifies external risk assessment, is editable for regional or business‑line notes, and is easily shareable for meetings, presentations, and cross‑team alignment.

Economic factors

Consumer purchasing power

Inflation (US CPI 2024 3.4%) and higher benchmark rates (Fed funds ~5.25–5.5% mid‑2025) drive consumers to trade up in staples or down on discretionary categories, shifting category mix. Real wage stagnation in many advanced economies has boosted demand for value lines versus premium imports. Exchange‑rate passthrough (commonly 10–30% for food imports) raises shelf prices and elasticity, so assortment balancing—mixing private label, mid, and premium tiers—preserves volumes through cycles.

FX volatility & hedging

Shekel volatility versus USD/EUR causes immediate repricing of imports, with annual swings of roughly 5–10% in recent 2023–25 periods impacting landed costs and pass-through pricing. Hedging and contractual currency clauses have stabilized margins but added 0.5–1.5 percentage points to operating costs through premiums and administrative expense. Timing of inventory buys can swing gross margin by several percentage points, so diversifying currency exposure reduces single-currency concentration risk and smooths P&L shocks.

Logistics costs & capacity

Global freight volatility and port capacity swings kept landed costs and lead times elevated—global container fleet reached about 28m TEU in 2024 while spot rates eased ~60% from 2021 peaks but remained above pre‑pandemic levels, extending lead times for some lanes. Cold‑chain needs raise unit cost sensitivity, adding refrigeration capex and 15–25% higher freight premiums on perishables. Consolidation and load optimization improved unit economics; multi‑port strategies reduced disruption risk and surcharge exposure.

Competitive intensity & private label

Retailer private labels, which reached about 18% of global grocery sales in 2024 (NielsenIQ), pressure pricing and claim more shelf space, forcing Willi-Food to absorb margin compression. Scale retailers leverage rebates and promo funding—top chains often secure 3–7% effective price support—sharpening competitive advantage. Willi-Food defends margin with differentiated SKUs, retailer exclusives and data-driven category management that strengthens bargaining power.

- private-label-share: 18% (2024)

- promo-funding-leverage: 3–7% price support

- differentiation: exclusive SKUs protect margins

- data-driven: category analytics boosts negotiation

Macroeconomic growth & confidence

Macroeconomic growth steers category mix: IMF estimated 2024 global GDP growth near 3.1% and weaker consumer sentiment shifts volumes toward staples while expansions lift indulgence and specialty lines; Conference Board US consumer confidence averaged about 102 in 2024. Inventory and promo cadence must track demand inflections; strict forecast discipline reduces obsolescence and write-offs.

- GDP 2024 ~3.1%

- US consumer confidence 2024 ~102

- Downturns favor staples

- Forecast discipline limits write-offs

War, tariffs and sanctions spike food supply costs, landed‑costs up 5–20%

Inflation (US CPI 2024 3.4%) and Fed rates (~5.25–5.5% mid‑2025) shift shoppers to value, boosting private‑label share and compressing premium volumes. Shekel swings ~5–10% (2023–25) and 10–30% passthrough on imports raise elasticity; hedging adds ~0.5–1.5pp to costs. Freight and cold‑chain premiums (15–25%) and private label at 18% (2024) pressure margins, so SKU mix and timing are critical.

| Metric | Value |

|---|---|

| US CPI 2024 | 3.4% |

| Fed funds mid‑2025 | 5.25–5.5% |

| Shekel volatility (2023–25) | 5–10% |

| Import passthrough | 10–30% |

| Hedging cost | +0.5–1.5pp |

| Freight/cold‑chain premium | 15–25% |

| Private‑label share 2024 | 18% |

Preview the Actual Deliverable

Willi-Food PESTLE Analysis

The Willi-Food PESTLE Analysis offers a concise, professionally structured review of political, economic, social, technological, legal, and environmental factors affecting the business. The preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use. No placeholders or teasers; download the final file immediately after checkout.