Winbond Electronics Porter's Five Forces Analysis

Go Beyond the Preview—Access the Full Strategic Report

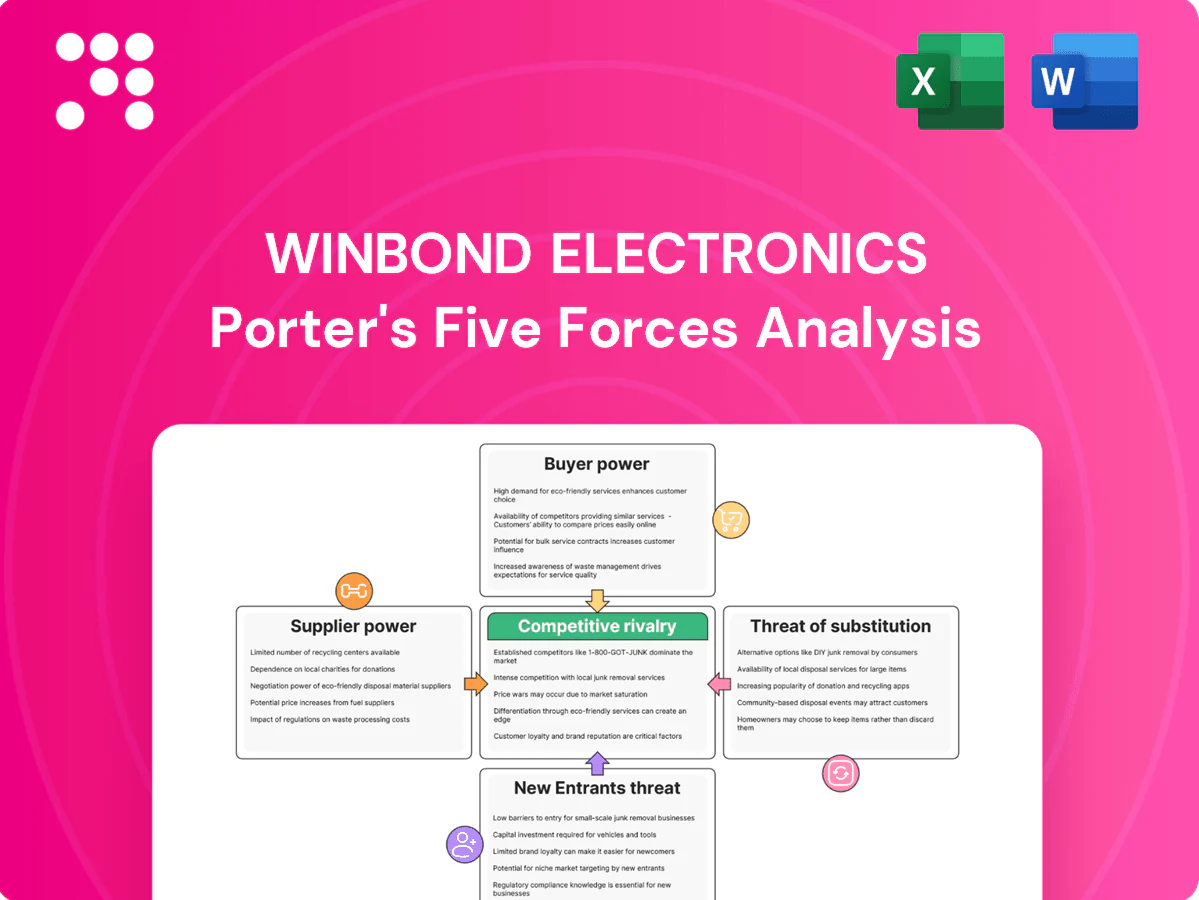

Winbond Electronics faces high competitive rivalry and shifting buyer demands, moderate supplier influence for specialized memory components, growing substitute threats from alternative memory technologies, and barriers that temper new entrants—creating a nuanced strategic landscape. This brief preview scratches the surface; unlock the full Porter's Five Forces Analysis for force-by-force ratings, visuals, and actionable insights to inform investment or strategic decisions.

Suppliers Bargaining Power

Concentrated equipment vendors

Memory fabrication relies on a handful of capital-equipment suppliers for lithography, deposition and metrology, concentrating leverage in vendor hands.

ASML held over 90% of EUV system supply in 2024, forcing premium prices and multi‑year lead times that boost supplier bargaining power on service and spares.

Winbond’s specialty nodes still require scarce tools and replacement parts, limiting its negotiating power; any supply disruption can quickly bottleneck capacity and delay yield ramps.

Critical materials and gases

Silicon wafers, specialty gases, photoresists and chemicals are tightly specified inputs with a narrow qualified supplier base—photoresists are dominated by top suppliers JSR, Tokyo Ohka Kogyo and Fujifilm—raising switching costs via long qualification and yield sensitivity. While some inputs are commoditized, high-purity consistency narrows the pool and increases price/leverage. Lead times for specialty gases and chemicals often extend for months, strengthening upstream power. Energy cost and utility stability in wafer fabs act as additional supplier-like constraints on Winbond.

Process IP and EDA ecosystems

Licenses for EDA tools, IP blocks and security libraries carry recurring fees and significant lock-in, with the top three EDA/IP vendors controlling roughly 75% of the market, giving them outsized pricing power. Deeply integrated design flows make switching toolchains risky and slow, often delaying projects and raising TCO. Compliance and security certifications (e.g., ISO 27001, Common Criteria) further increase dependency and vendor leverage.

Capacity and lead-time constraints

Semiconductor cycles can push tool and material lead-times to 6–12 months during upturns, letting suppliers prioritize larger customers or higher‑margin segments; the top three DRAM vendors control roughly 90% of capacity, intensifying allocation pressure on smaller players like Winbond. Balancing DRAM, NOR, and secure flash mixes increases internal scheduling friction, and tight supply windows amplify the power of time‑sensitive suppliers.

- Lead-times: 6–12 months

- Top-3 DRAM share: ~90%

- Mix complexity: DRAM + NOR + secure flash

- Effect: elevated supplier timing power

Partial mitigation via in-house fabs

Owning and operating fabs in Taiwan and China gives Winbond measurable bargaining leverage and tighter process control, and supported 2024 revenue of NT$67.3 billion, but multi-sourcing and long-term purchase agreements moderate raw-material and equipment volatility. Qualification inertia for specialized memory keeps supplier power structurally elevated, while geographic concentration raises geopolitical and logistics risks.

- In-house fabs: process control, cost leverage

- Multi-sourcing/long-term deals: volume stability

- Qualification inertia: high supplier switching costs

- Geographic concentration: Taiwan/China risk

ASML >90% EUV share and 6–12 month tool lead-times boost supplier pricing power

Supplier power is high: ASML held >90% EUV share in 2024 and tool/material lead‑times extend 6–12 months, enabling price and allocation leverage.

Specialty gases, photoresists (JSR/TOK/Fujifilm) and EDA/IP oligopolies raise switching costs and recurring fees, constraining Winbond’s negotiation room.

Winbond’s NT$67.3B 2024 in‑house fabs and long‑term deals reduce but do not eliminate supplier concentration and geopolitical risks.

| Metric | Value (2024) |

|---|---|

| EUV supplier | ASML >90% |

| Tool/material lead‑times | 6–12 months |

| Top‑3 DRAM share | ~90% |

| Winbond revenue | NT$67.3B |

What is included in the product

Concise Porter’s Five Forces assessment of Winbond Electronics, revealing competitive rivalry, buyer and supplier power, threat of entrants and substitutes, and strategic levers to protect margins and market share.

A concise one-sheet Porter's Five Forces for Winbond—visual radar and editable pressure sliders let you simulate supply‑chain shocks, memory market pricing, and new fab entrants for board‑ready slides.

Customers Bargaining Power

Large OEMs and Tier-1s

Consumer, computing and automotive buyers are concentrated and price-savvy; top 5 OEMs controlled over 50% of smartphone shipments in 2024, giving them strong leverage for volume discounts and rebates. High order volumes translate into aggressive pricing negotiations and rebate demands, while vendor scorecards and dual-sourcing are standard procurement practices. This intensifies pricing pressure on commodity-like memory lines, compressing Winbond margins.

Commoditized price visibility

DRAM and NOR pricing in 2024 remained highly transparent and cyclical, with spot and contract benchmarks (DRAM spot spreads widened ~20% vs contract in 2024) anchoring buyer expectations. Customers pressed for index-linked terms and shorter commitments during the 2024 downcycle. That behavior compressed Winbond margins and increased ASP volatility.

Design-in switching costs

Once qualified, Winbond parts become sticky because firmware integration, validation and reliability testing often require 6 to 12 months of effort, and automotive/industrial certifications such as AEC-Q and PPAP create inertia. Automotive component lifecycles of 10 to 15 years and long qualification lead times push buyers to trade lower prices for supply assurance and longevity. This supply-assurance dynamic moderates buyer power in qualified sockets, reducing churn and strengthening Winbond’s negotiating position.

Demand variability and mix

Demand variability shifts buyer leverage quarter to quarter: shortages reduce buyer power via allocations, while gluts increase it as customers press for price concessions; Winbond’s diversified exposure across consumer, industrial and automotive segments dampens volatility, but customers still time purchases to cycle troughs to extract better terms.

- Buyers leverage cycles to negotiate concessions

- Allocations in shortages weaken buyer bargaining

- Gluts strengthen buyer power and pricing pressure

- Winbond’s multi-segment exposure provides risk balance

Value-added differentiation

As of 2024 Winbond's TrustME secure flash, extended-temperature variants and long-life support create clear value by reducing direct product comparability and enabling price premiums in industrial and automotive segments; custom packaging and firmware services deepen customer lock-in and integration. These differentiated offerings lower buyer bargaining power in niche applications and favor long-term contracts.

- TrustME secure flash — security-led differentiation

- Extended-temp/long-life — industrial/automotive fit

- Custom packages & firmware — stronger customer ties

- Net effect — reduced buyer power, supported premiums

Concentrated buyers (Top-5 > 50%) force discounts; DRAM spot +20% widens leverage

Buyers are concentrated and price‑sensitive (top 5 OEMs >50% smartphone share in 2024), driving aggressive discounting and index‑linked terms. Transparent, cyclical DRAM/NOR markets (DRAM spot ~20% above contract in 2024) amplify buyer leverage in gluts; shortages reverse this. Long qualification (6–12 months) and automotive lifecycles (10–15 years) create stickiness, reducing buyer power in qualified sockets.

| Metric | Value (2024) |

|---|---|

| Top‑5 OEM smartphone share | >50% |

| DRAM spot vs contract | ~+20% |

| Qualification time | 6–12 months |

| Automotive lifecycle | 10–15 years |

Preview the Actual Deliverable

Winbond Electronics Porter's Five Forces Analysis

This preview is the exact Porter's Five Forces analysis for Winbond Electronics you'll receive after purchase—fully written, formatted, and ready to use. It covers competitive rivalry, supplier and buyer power, threats of substitution and entry, and strategic implications specific to Winbond. No samples or placeholders—what you see is the final deliverable, available for instant download upon payment.

Go Beyond the Preview—Access the Full Strategic Report

Winbond Electronics faces high competitive rivalry and shifting buyer demands, moderate supplier influence for specialized memory components, growing substitute threats from alternative memory technologies, and barriers that temper new entrants—creating a nuanced strategic landscape. This brief preview scratches the surface; unlock the full Porter's Five Forces Analysis for force-by-force ratings, visuals, and actionable insights to inform investment or strategic decisions.

Suppliers Bargaining Power

Concentrated equipment vendors

Memory fabrication relies on a handful of capital-equipment suppliers for lithography, deposition and metrology, concentrating leverage in vendor hands.

ASML held over 90% of EUV system supply in 2024, forcing premium prices and multi‑year lead times that boost supplier bargaining power on service and spares.

Winbond’s specialty nodes still require scarce tools and replacement parts, limiting its negotiating power; any supply disruption can quickly bottleneck capacity and delay yield ramps.

Critical materials and gases

Silicon wafers, specialty gases, photoresists and chemicals are tightly specified inputs with a narrow qualified supplier base—photoresists are dominated by top suppliers JSR, Tokyo Ohka Kogyo and Fujifilm—raising switching costs via long qualification and yield sensitivity. While some inputs are commoditized, high-purity consistency narrows the pool and increases price/leverage. Lead times for specialty gases and chemicals often extend for months, strengthening upstream power. Energy cost and utility stability in wafer fabs act as additional supplier-like constraints on Winbond.

Process IP and EDA ecosystems

Licenses for EDA tools, IP blocks and security libraries carry recurring fees and significant lock-in, with the top three EDA/IP vendors controlling roughly 75% of the market, giving them outsized pricing power. Deeply integrated design flows make switching toolchains risky and slow, often delaying projects and raising TCO. Compliance and security certifications (e.g., ISO 27001, Common Criteria) further increase dependency and vendor leverage.

Capacity and lead-time constraints

Semiconductor cycles can push tool and material lead-times to 6–12 months during upturns, letting suppliers prioritize larger customers or higher‑margin segments; the top three DRAM vendors control roughly 90% of capacity, intensifying allocation pressure on smaller players like Winbond. Balancing DRAM, NOR, and secure flash mixes increases internal scheduling friction, and tight supply windows amplify the power of time‑sensitive suppliers.

- Lead-times: 6–12 months

- Top-3 DRAM share: ~90%

- Mix complexity: DRAM + NOR + secure flash

- Effect: elevated supplier timing power

Partial mitigation via in-house fabs

Owning and operating fabs in Taiwan and China gives Winbond measurable bargaining leverage and tighter process control, and supported 2024 revenue of NT$67.3 billion, but multi-sourcing and long-term purchase agreements moderate raw-material and equipment volatility. Qualification inertia for specialized memory keeps supplier power structurally elevated, while geographic concentration raises geopolitical and logistics risks.

- In-house fabs: process control, cost leverage

- Multi-sourcing/long-term deals: volume stability

- Qualification inertia: high supplier switching costs

- Geographic concentration: Taiwan/China risk

ASML >90% EUV share and 6–12 month tool lead-times boost supplier pricing power

Supplier power is high: ASML held >90% EUV share in 2024 and tool/material lead‑times extend 6–12 months, enabling price and allocation leverage.

Specialty gases, photoresists (JSR/TOK/Fujifilm) and EDA/IP oligopolies raise switching costs and recurring fees, constraining Winbond’s negotiation room.

Winbond’s NT$67.3B 2024 in‑house fabs and long‑term deals reduce but do not eliminate supplier concentration and geopolitical risks.

| Metric | Value (2024) |

|---|---|

| EUV supplier | ASML >90% |

| Tool/material lead‑times | 6–12 months |

| Top‑3 DRAM share | ~90% |

| Winbond revenue | NT$67.3B |

What is included in the product

Concise Porter’s Five Forces assessment of Winbond Electronics, revealing competitive rivalry, buyer and supplier power, threat of entrants and substitutes, and strategic levers to protect margins and market share.

A concise one-sheet Porter's Five Forces for Winbond—visual radar and editable pressure sliders let you simulate supply‑chain shocks, memory market pricing, and new fab entrants for board‑ready slides.

Customers Bargaining Power

Large OEMs and Tier-1s

Consumer, computing and automotive buyers are concentrated and price-savvy; top 5 OEMs controlled over 50% of smartphone shipments in 2024, giving them strong leverage for volume discounts and rebates. High order volumes translate into aggressive pricing negotiations and rebate demands, while vendor scorecards and dual-sourcing are standard procurement practices. This intensifies pricing pressure on commodity-like memory lines, compressing Winbond margins.

Commoditized price visibility

DRAM and NOR pricing in 2024 remained highly transparent and cyclical, with spot and contract benchmarks (DRAM spot spreads widened ~20% vs contract in 2024) anchoring buyer expectations. Customers pressed for index-linked terms and shorter commitments during the 2024 downcycle. That behavior compressed Winbond margins and increased ASP volatility.

Design-in switching costs

Once qualified, Winbond parts become sticky because firmware integration, validation and reliability testing often require 6 to 12 months of effort, and automotive/industrial certifications such as AEC-Q and PPAP create inertia. Automotive component lifecycles of 10 to 15 years and long qualification lead times push buyers to trade lower prices for supply assurance and longevity. This supply-assurance dynamic moderates buyer power in qualified sockets, reducing churn and strengthening Winbond’s negotiating position.

Demand variability and mix

Demand variability shifts buyer leverage quarter to quarter: shortages reduce buyer power via allocations, while gluts increase it as customers press for price concessions; Winbond’s diversified exposure across consumer, industrial and automotive segments dampens volatility, but customers still time purchases to cycle troughs to extract better terms.

- Buyers leverage cycles to negotiate concessions

- Allocations in shortages weaken buyer bargaining

- Gluts strengthen buyer power and pricing pressure

- Winbond’s multi-segment exposure provides risk balance

Value-added differentiation

As of 2024 Winbond's TrustME secure flash, extended-temperature variants and long-life support create clear value by reducing direct product comparability and enabling price premiums in industrial and automotive segments; custom packaging and firmware services deepen customer lock-in and integration. These differentiated offerings lower buyer bargaining power in niche applications and favor long-term contracts.

- TrustME secure flash — security-led differentiation

- Extended-temp/long-life — industrial/automotive fit

- Custom packages & firmware — stronger customer ties

- Net effect — reduced buyer power, supported premiums

Concentrated buyers (Top-5 > 50%) force discounts; DRAM spot +20% widens leverage

Buyers are concentrated and price‑sensitive (top 5 OEMs >50% smartphone share in 2024), driving aggressive discounting and index‑linked terms. Transparent, cyclical DRAM/NOR markets (DRAM spot ~20% above contract in 2024) amplify buyer leverage in gluts; shortages reverse this. Long qualification (6–12 months) and automotive lifecycles (10–15 years) create stickiness, reducing buyer power in qualified sockets.

| Metric | Value (2024) |

|---|---|

| Top‑5 OEM smartphone share | >50% |

| DRAM spot vs contract | ~+20% |

| Qualification time | 6–12 months |

| Automotive lifecycle | 10–15 years |

Preview the Actual Deliverable

Winbond Electronics Porter's Five Forces Analysis

This preview is the exact Porter's Five Forces analysis for Winbond Electronics you'll receive after purchase—fully written, formatted, and ready to use. It covers competitive rivalry, supplier and buyer power, threats of substitution and entry, and strategic implications specific to Winbond. No samples or placeholders—what you see is the final deliverable, available for instant download upon payment.

Description

Go Beyond the Preview—Access the Full Strategic Report

Winbond Electronics faces high competitive rivalry and shifting buyer demands, moderate supplier influence for specialized memory components, growing substitute threats from alternative memory technologies, and barriers that temper new entrants—creating a nuanced strategic landscape. This brief preview scratches the surface; unlock the full Porter's Five Forces Analysis for force-by-force ratings, visuals, and actionable insights to inform investment or strategic decisions.

Suppliers Bargaining Power

Concentrated equipment vendors

Memory fabrication relies on a handful of capital-equipment suppliers for lithography, deposition and metrology, concentrating leverage in vendor hands.

ASML held over 90% of EUV system supply in 2024, forcing premium prices and multi‑year lead times that boost supplier bargaining power on service and spares.

Winbond’s specialty nodes still require scarce tools and replacement parts, limiting its negotiating power; any supply disruption can quickly bottleneck capacity and delay yield ramps.

Critical materials and gases

Silicon wafers, specialty gases, photoresists and chemicals are tightly specified inputs with a narrow qualified supplier base—photoresists are dominated by top suppliers JSR, Tokyo Ohka Kogyo and Fujifilm—raising switching costs via long qualification and yield sensitivity. While some inputs are commoditized, high-purity consistency narrows the pool and increases price/leverage. Lead times for specialty gases and chemicals often extend for months, strengthening upstream power. Energy cost and utility stability in wafer fabs act as additional supplier-like constraints on Winbond.

Process IP and EDA ecosystems

Licenses for EDA tools, IP blocks and security libraries carry recurring fees and significant lock-in, with the top three EDA/IP vendors controlling roughly 75% of the market, giving them outsized pricing power. Deeply integrated design flows make switching toolchains risky and slow, often delaying projects and raising TCO. Compliance and security certifications (e.g., ISO 27001, Common Criteria) further increase dependency and vendor leverage.

Capacity and lead-time constraints

Semiconductor cycles can push tool and material lead-times to 6–12 months during upturns, letting suppliers prioritize larger customers or higher‑margin segments; the top three DRAM vendors control roughly 90% of capacity, intensifying allocation pressure on smaller players like Winbond. Balancing DRAM, NOR, and secure flash mixes increases internal scheduling friction, and tight supply windows amplify the power of time‑sensitive suppliers.

- Lead-times: 6–12 months

- Top-3 DRAM share: ~90%

- Mix complexity: DRAM + NOR + secure flash

- Effect: elevated supplier timing power

Partial mitigation via in-house fabs

Owning and operating fabs in Taiwan and China gives Winbond measurable bargaining leverage and tighter process control, and supported 2024 revenue of NT$67.3 billion, but multi-sourcing and long-term purchase agreements moderate raw-material and equipment volatility. Qualification inertia for specialized memory keeps supplier power structurally elevated, while geographic concentration raises geopolitical and logistics risks.

- In-house fabs: process control, cost leverage

- Multi-sourcing/long-term deals: volume stability

- Qualification inertia: high supplier switching costs

- Geographic concentration: Taiwan/China risk

ASML >90% EUV share and 6–12 month tool lead-times boost supplier pricing power

Supplier power is high: ASML held >90% EUV share in 2024 and tool/material lead‑times extend 6–12 months, enabling price and allocation leverage.

Specialty gases, photoresists (JSR/TOK/Fujifilm) and EDA/IP oligopolies raise switching costs and recurring fees, constraining Winbond’s negotiation room.

Winbond’s NT$67.3B 2024 in‑house fabs and long‑term deals reduce but do not eliminate supplier concentration and geopolitical risks.

| Metric | Value (2024) |

|---|---|

| EUV supplier | ASML >90% |

| Tool/material lead‑times | 6–12 months |

| Top‑3 DRAM share | ~90% |

| Winbond revenue | NT$67.3B |

What is included in the product

Concise Porter’s Five Forces assessment of Winbond Electronics, revealing competitive rivalry, buyer and supplier power, threat of entrants and substitutes, and strategic levers to protect margins and market share.

A concise one-sheet Porter's Five Forces for Winbond—visual radar and editable pressure sliders let you simulate supply‑chain shocks, memory market pricing, and new fab entrants for board‑ready slides.

Customers Bargaining Power

Large OEMs and Tier-1s

Consumer, computing and automotive buyers are concentrated and price-savvy; top 5 OEMs controlled over 50% of smartphone shipments in 2024, giving them strong leverage for volume discounts and rebates. High order volumes translate into aggressive pricing negotiations and rebate demands, while vendor scorecards and dual-sourcing are standard procurement practices. This intensifies pricing pressure on commodity-like memory lines, compressing Winbond margins.

Commoditized price visibility

DRAM and NOR pricing in 2024 remained highly transparent and cyclical, with spot and contract benchmarks (DRAM spot spreads widened ~20% vs contract in 2024) anchoring buyer expectations. Customers pressed for index-linked terms and shorter commitments during the 2024 downcycle. That behavior compressed Winbond margins and increased ASP volatility.

Design-in switching costs

Once qualified, Winbond parts become sticky because firmware integration, validation and reliability testing often require 6 to 12 months of effort, and automotive/industrial certifications such as AEC-Q and PPAP create inertia. Automotive component lifecycles of 10 to 15 years and long qualification lead times push buyers to trade lower prices for supply assurance and longevity. This supply-assurance dynamic moderates buyer power in qualified sockets, reducing churn and strengthening Winbond’s negotiating position.

Demand variability and mix

Demand variability shifts buyer leverage quarter to quarter: shortages reduce buyer power via allocations, while gluts increase it as customers press for price concessions; Winbond’s diversified exposure across consumer, industrial and automotive segments dampens volatility, but customers still time purchases to cycle troughs to extract better terms.

- Buyers leverage cycles to negotiate concessions

- Allocations in shortages weaken buyer bargaining

- Gluts strengthen buyer power and pricing pressure

- Winbond’s multi-segment exposure provides risk balance

Value-added differentiation

As of 2024 Winbond's TrustME secure flash, extended-temperature variants and long-life support create clear value by reducing direct product comparability and enabling price premiums in industrial and automotive segments; custom packaging and firmware services deepen customer lock-in and integration. These differentiated offerings lower buyer bargaining power in niche applications and favor long-term contracts.

- TrustME secure flash — security-led differentiation

- Extended-temp/long-life — industrial/automotive fit

- Custom packages & firmware — stronger customer ties

- Net effect — reduced buyer power, supported premiums

Concentrated buyers (Top-5 > 50%) force discounts; DRAM spot +20% widens leverage

Buyers are concentrated and price‑sensitive (top 5 OEMs >50% smartphone share in 2024), driving aggressive discounting and index‑linked terms. Transparent, cyclical DRAM/NOR markets (DRAM spot ~20% above contract in 2024) amplify buyer leverage in gluts; shortages reverse this. Long qualification (6–12 months) and automotive lifecycles (10–15 years) create stickiness, reducing buyer power in qualified sockets.

| Metric | Value (2024) |

|---|---|

| Top‑5 OEM smartphone share | >50% |

| DRAM spot vs contract | ~+20% |

| Qualification time | 6–12 months |

| Automotive lifecycle | 10–15 years |

Preview the Actual Deliverable

Winbond Electronics Porter's Five Forces Analysis

This preview is the exact Porter's Five Forces analysis for Winbond Electronics you'll receive after purchase—fully written, formatted, and ready to use. It covers competitive rivalry, supplier and buyer power, threats of substitution and entry, and strategic implications specific to Winbond. No samples or placeholders—what you see is the final deliverable, available for instant download upon payment.