Wintrust Financial Business Model Canvas

Business Model Canvas: three-sentence blueprint of value proposition, revenue and partnerships

Discover Wintrust Financial’s competitive blueprint in our concise Business Model Canvas: three clear sentences revealing its value propositions, revenue engines, and key partnerships. This downloadable, editable canvas (Word & Excel) is perfect for investors and strategists. Purchase the full version to benchmark, adapt, and act on proven financial-sector strategies today.

Partnerships

Core banking and fintech providers

Partnerships with core platform vendors, digital banking suites, and cybersecurity firms give Wintrust scalable account processing, mobile features, APIs and real-time payments support; real-time payment volumes grew ~40% industry-wide in 2023. Co-innovation with vendors has cut time-to-market for new services by roughly 30% in comparable bank programs. Robust SLAs (commonly 99.99% uptime) ensure reliability and compliance.

Mortgage investors and secondary market conduits

In 2024 Wintrust deepened relationships with mortgage investors and agency buyers to facilitate origination, sales, and servicing transfers, enabling quicker turn times and investor diversification. Access to the secondary market improved balance sheet flexibility and capital efficiency through whole-loan and MBS channels. Pipeline hedging support helped stabilize gain-on-sale margins amid rate volatility, while correspondent and warehouse partners smoothed fulfillment and scale.

Payment networks and treasury ecosystem

Payment networks for debit, credit, ACH, wires and RTP/FedNow (FedNow launched July 2023) expand Wintrust client payment options and support faster settlement. Treasury tech partners improve receivables, payables and fraud controls, driving higher fee income and client stickiness. Integrated connections enable omni-channel cash management across digital, branch and API channels.

Community organizations and local businesses

Community organizations, local chambers, nonprofits and universities deepen Wintrust’s regional roots and pipeline for deposits and loans; in 2024 Wintrust operated over 160 branches and reported roughly $61 billion in assets, reinforcing local credibility. Referrals from realtors, CPAs and attorneys drive targeted customer acquisition; sponsorships and co-programs on financial literacy and small-business growth boost brand trust and retention.

- Local partners: chambers, universities, nonprofits

- Referral sources: realtors, CPAs, attorneys

- Outcomes: sponsorships, financial-literacy co-programs, SMB growth

Broker-dealers and asset managers

Broker-dealers and asset managers supply custodians, fund families and model portfolios that underpin Wintrust’s wealth and retirement solutions, supporting over $50 billion in client assets on the platform in 2024 and enabling open-architecture product breadth.

Research, analytics and third-party tools raise advisory quality while revenue-sharing and platform economics improve margins through scalable fee and custody arrangements.

- custodians

- open-architecture

- model portfolios

- research/tools

- revenue-sharing

Partnerships enable RTP/FedNow, 99.99% SLAs and mortgage/deposit liquidity

Partnerships with core platform, cybersecurity and payments vendors deliver scalable processing, APIs, RTP/FedNow support and enterprise SLAs (commonly 99.99%).

Mortgage investors, correspondent and warehouse partners enable whole-loan/MBS channels, pipeline hedging and balance-sheet flexibility to stabilize margins.

Community, referral and wealth partners drive deposit and advisory pipelines; Wintrust reported ~160 branches, ~$61B assets and ~$50B AUM in 2024.

| Partner | Role | 2024 metric |

|---|---|---|

| Core tech | Processing, APIs | 99.99% SLA |

| Payments | Settlement, fraud | FedNow/RTP live |

| Mortgage investors | Sale/servicing | Enhanced capital flexibility |

| Community/Wealth | Acquisition, custody | 160 branches; $61B assets; $50B AUM |

What is included in the product

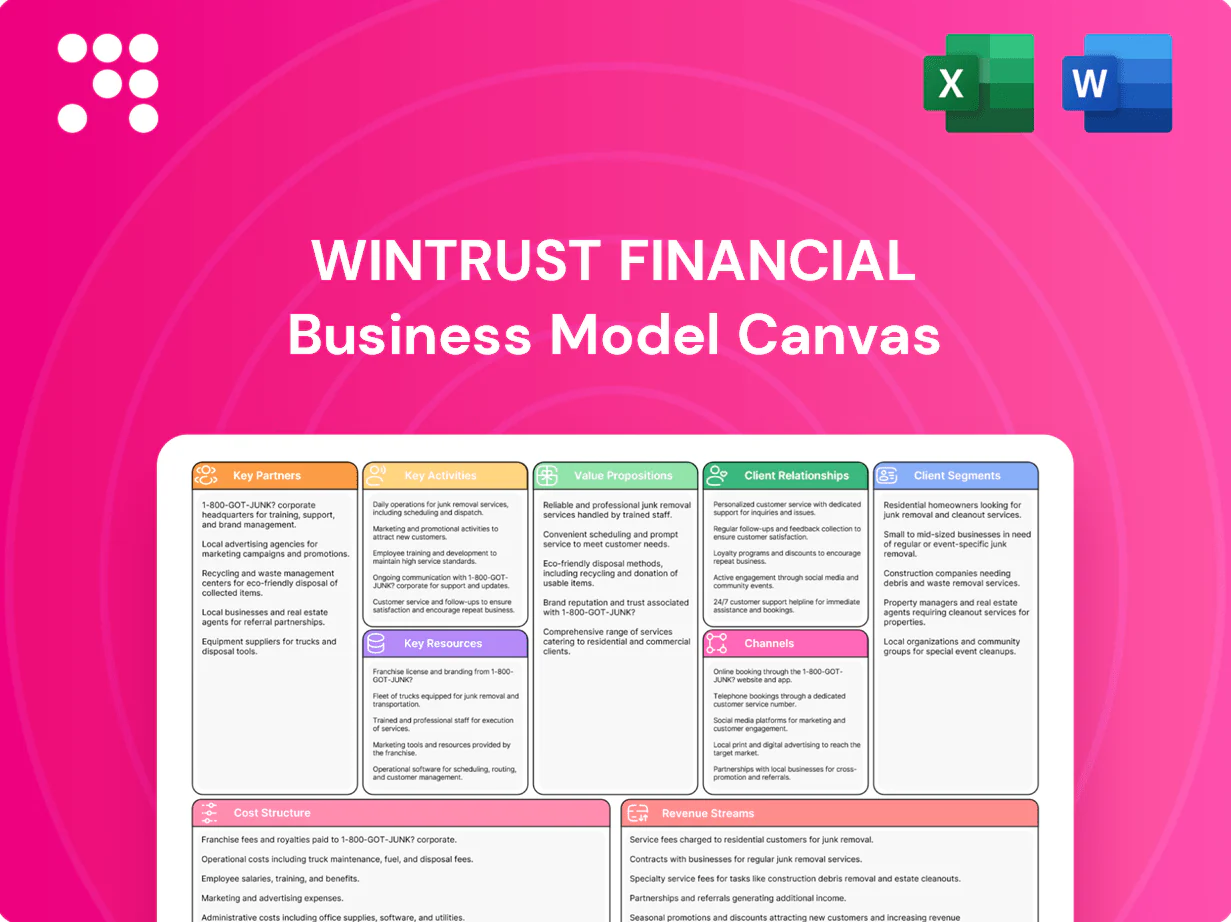

A comprehensive Business Model Canvas for Wintrust Financial that maps customer segments, channels, value propositions, revenue streams and cost structure across the 9 BMC blocks, reflecting real-world banking operations, competitive advantages and SWOT-linked insights to support presentations, investor discussions and strategic decision-making.

High-level view of Wintrust Financial’s business model with editable cells to quickly distill banking operations, revenue streams, and risk levers into a single, shareable page for faster strategic decisions and team alignment.

Activities

Deposit gathering and relationship banking

Attracting and retaining low-cost, stable deposits is central to Wintrust’s funding strategy, supporting over $60 billion in deposits in 2024 and financing loan growth and margin stability. Relationship managers deepen ties across personal, business, and wealth needs to increase loyalty. Competitive pricing, community-branch presence, and service drive balances while disciplined cross-sell expands share of wallet and fee income.

Commercial and retail lending

Underwriting C&I, CRE, SBA and consumer loans — supporting local businesses and households — drove Wintrusts lending engine, with total loans of $58.6 billion at year-end 2024.

Rigorous credit discipline and portfolio diversification across sectors and geographies constrained loss rates and preserved capital ratios through 2024 stress periods.

Fast, local decision-making by community bankers speeds deployment, while ongoing monitoring and workout resources sustained asset quality and kept NPLs relatively low in 2024.

Wealth management and advisory

Wealth management and advisory at Wintrust combines financial planning, investment advisory, and trust services to address complex client needs, serving clients alongside the bank's broader balance sheet (Wintrust reported roughly $66 billion in total assets in 2024). Goals-based frameworks align portfolios to life stages, improving long-term outcomes and retention. Fiduciary oversight and integrated banking-wealth views strengthen credibility and drive cross-sell revenue.

Mortgage origination and fulfillment

Lending teams at Wintrust originate, process, and close mortgages efficiently, leveraging centralized fulfillment centers and digital loan pipelines to shorten turn times and boost conversion. Secondary market execution actively hedges rate risk and manages capital, supporting volume stability amid 2024 mortgage market volatility. Strong realtor and builder pipelines plus a focus on borrower experience drive referrals and repeat business.

- Origination efficiency

- Secondary market hedging

- Realtor/builder channels

- Borrower experience = referrals

Risk, compliance, and digital enablement

Risk, compliance, and digital enablement at Wintrust integrate ALM, credit, liquidity, and operational risk programs to safeguard resilience, with regulatory compliance embedded into processes and systems in 2024. Digital enhancements expanded UX and efficiency across channels, while analytics drive pricing, marketing, and credit decisions using 2024 transaction and portfolio data.

- ALM/credit/liquidity: ongoing program coverage in 2024

- Regulatory compliance: embedded in systems (2024)

- Digital UX/efficiency: expanded in 2024

- Data analytics: informs pricing, marketing, credit (2024)

Deposits fund growth: $60B+, $58.6B loans

Attracting and retaining low-cost deposits (over $60 billion in 2024) funds loan growth and margin stability. Underwriting C&I, CRE, SBA and consumer loans drove a $58.6 billion loan book at year-end 2024. Local decision-making, ALM/hedging, digital fulfillment and wealth advisory integrated to preserve asset quality and expand fee income.

| Metric | 2024 |

|---|---|

| Deposits | $60B+ |

| Loans | $58.6B |

| Total assets | $66B |

Full Document Unlocks After Purchase

Business Model Canvas

The Business Model Canvas for Wintrust Financial shown here is a true preview of the exact deliverable—not a mockup or sample. When you purchase, you’ll receive this same professional, ready-to-use file in editable Word and Excel formats. The full document includes all sections and content as previewed, ready for presentation, customization, and implementation.

Business Model Canvas: three-sentence blueprint of value proposition, revenue and partnerships

Discover Wintrust Financial’s competitive blueprint in our concise Business Model Canvas: three clear sentences revealing its value propositions, revenue engines, and key partnerships. This downloadable, editable canvas (Word & Excel) is perfect for investors and strategists. Purchase the full version to benchmark, adapt, and act on proven financial-sector strategies today.

Partnerships

Core banking and fintech providers

Partnerships with core platform vendors, digital banking suites, and cybersecurity firms give Wintrust scalable account processing, mobile features, APIs and real-time payments support; real-time payment volumes grew ~40% industry-wide in 2023. Co-innovation with vendors has cut time-to-market for new services by roughly 30% in comparable bank programs. Robust SLAs (commonly 99.99% uptime) ensure reliability and compliance.

Mortgage investors and secondary market conduits

In 2024 Wintrust deepened relationships with mortgage investors and agency buyers to facilitate origination, sales, and servicing transfers, enabling quicker turn times and investor diversification. Access to the secondary market improved balance sheet flexibility and capital efficiency through whole-loan and MBS channels. Pipeline hedging support helped stabilize gain-on-sale margins amid rate volatility, while correspondent and warehouse partners smoothed fulfillment and scale.

Payment networks and treasury ecosystem

Payment networks for debit, credit, ACH, wires and RTP/FedNow (FedNow launched July 2023) expand Wintrust client payment options and support faster settlement. Treasury tech partners improve receivables, payables and fraud controls, driving higher fee income and client stickiness. Integrated connections enable omni-channel cash management across digital, branch and API channels.

Community organizations and local businesses

Community organizations, local chambers, nonprofits and universities deepen Wintrust’s regional roots and pipeline for deposits and loans; in 2024 Wintrust operated over 160 branches and reported roughly $61 billion in assets, reinforcing local credibility. Referrals from realtors, CPAs and attorneys drive targeted customer acquisition; sponsorships and co-programs on financial literacy and small-business growth boost brand trust and retention.

- Local partners: chambers, universities, nonprofits

- Referral sources: realtors, CPAs, attorneys

- Outcomes: sponsorships, financial-literacy co-programs, SMB growth

Broker-dealers and asset managers

Broker-dealers and asset managers supply custodians, fund families and model portfolios that underpin Wintrust’s wealth and retirement solutions, supporting over $50 billion in client assets on the platform in 2024 and enabling open-architecture product breadth.

Research, analytics and third-party tools raise advisory quality while revenue-sharing and platform economics improve margins through scalable fee and custody arrangements.

- custodians

- open-architecture

- model portfolios

- research/tools

- revenue-sharing

Partnerships enable RTP/FedNow, 99.99% SLAs and mortgage/deposit liquidity

Partnerships with core platform, cybersecurity and payments vendors deliver scalable processing, APIs, RTP/FedNow support and enterprise SLAs (commonly 99.99%).

Mortgage investors, correspondent and warehouse partners enable whole-loan/MBS channels, pipeline hedging and balance-sheet flexibility to stabilize margins.

Community, referral and wealth partners drive deposit and advisory pipelines; Wintrust reported ~160 branches, ~$61B assets and ~$50B AUM in 2024.

| Partner | Role | 2024 metric |

|---|---|---|

| Core tech | Processing, APIs | 99.99% SLA |

| Payments | Settlement, fraud | FedNow/RTP live |

| Mortgage investors | Sale/servicing | Enhanced capital flexibility |

| Community/Wealth | Acquisition, custody | 160 branches; $61B assets; $50B AUM |

What is included in the product

A comprehensive Business Model Canvas for Wintrust Financial that maps customer segments, channels, value propositions, revenue streams and cost structure across the 9 BMC blocks, reflecting real-world banking operations, competitive advantages and SWOT-linked insights to support presentations, investor discussions and strategic decision-making.

High-level view of Wintrust Financial’s business model with editable cells to quickly distill banking operations, revenue streams, and risk levers into a single, shareable page for faster strategic decisions and team alignment.

Activities

Deposit gathering and relationship banking

Attracting and retaining low-cost, stable deposits is central to Wintrust’s funding strategy, supporting over $60 billion in deposits in 2024 and financing loan growth and margin stability. Relationship managers deepen ties across personal, business, and wealth needs to increase loyalty. Competitive pricing, community-branch presence, and service drive balances while disciplined cross-sell expands share of wallet and fee income.

Commercial and retail lending

Underwriting C&I, CRE, SBA and consumer loans — supporting local businesses and households — drove Wintrusts lending engine, with total loans of $58.6 billion at year-end 2024.

Rigorous credit discipline and portfolio diversification across sectors and geographies constrained loss rates and preserved capital ratios through 2024 stress periods.

Fast, local decision-making by community bankers speeds deployment, while ongoing monitoring and workout resources sustained asset quality and kept NPLs relatively low in 2024.

Wealth management and advisory

Wealth management and advisory at Wintrust combines financial planning, investment advisory, and trust services to address complex client needs, serving clients alongside the bank's broader balance sheet (Wintrust reported roughly $66 billion in total assets in 2024). Goals-based frameworks align portfolios to life stages, improving long-term outcomes and retention. Fiduciary oversight and integrated banking-wealth views strengthen credibility and drive cross-sell revenue.

Mortgage origination and fulfillment

Lending teams at Wintrust originate, process, and close mortgages efficiently, leveraging centralized fulfillment centers and digital loan pipelines to shorten turn times and boost conversion. Secondary market execution actively hedges rate risk and manages capital, supporting volume stability amid 2024 mortgage market volatility. Strong realtor and builder pipelines plus a focus on borrower experience drive referrals and repeat business.

- Origination efficiency

- Secondary market hedging

- Realtor/builder channels

- Borrower experience = referrals

Risk, compliance, and digital enablement

Risk, compliance, and digital enablement at Wintrust integrate ALM, credit, liquidity, and operational risk programs to safeguard resilience, with regulatory compliance embedded into processes and systems in 2024. Digital enhancements expanded UX and efficiency across channels, while analytics drive pricing, marketing, and credit decisions using 2024 transaction and portfolio data.

- ALM/credit/liquidity: ongoing program coverage in 2024

- Regulatory compliance: embedded in systems (2024)

- Digital UX/efficiency: expanded in 2024

- Data analytics: informs pricing, marketing, credit (2024)

Deposits fund growth: $60B+, $58.6B loans

Attracting and retaining low-cost deposits (over $60 billion in 2024) funds loan growth and margin stability. Underwriting C&I, CRE, SBA and consumer loans drove a $58.6 billion loan book at year-end 2024. Local decision-making, ALM/hedging, digital fulfillment and wealth advisory integrated to preserve asset quality and expand fee income.

| Metric | 2024 |

|---|---|

| Deposits | $60B+ |

| Loans | $58.6B |

| Total assets | $66B |

Full Document Unlocks After Purchase

Business Model Canvas

The Business Model Canvas for Wintrust Financial shown here is a true preview of the exact deliverable—not a mockup or sample. When you purchase, you’ll receive this same professional, ready-to-use file in editable Word and Excel formats. The full document includes all sections and content as previewed, ready for presentation, customization, and implementation.

Original: $10.00

-65%$10.00

$3.50Description

Business Model Canvas: three-sentence blueprint of value proposition, revenue and partnerships

Discover Wintrust Financial’s competitive blueprint in our concise Business Model Canvas: three clear sentences revealing its value propositions, revenue engines, and key partnerships. This downloadable, editable canvas (Word & Excel) is perfect for investors and strategists. Purchase the full version to benchmark, adapt, and act on proven financial-sector strategies today.

Partnerships

Core banking and fintech providers

Partnerships with core platform vendors, digital banking suites, and cybersecurity firms give Wintrust scalable account processing, mobile features, APIs and real-time payments support; real-time payment volumes grew ~40% industry-wide in 2023. Co-innovation with vendors has cut time-to-market for new services by roughly 30% in comparable bank programs. Robust SLAs (commonly 99.99% uptime) ensure reliability and compliance.

Mortgage investors and secondary market conduits

In 2024 Wintrust deepened relationships with mortgage investors and agency buyers to facilitate origination, sales, and servicing transfers, enabling quicker turn times and investor diversification. Access to the secondary market improved balance sheet flexibility and capital efficiency through whole-loan and MBS channels. Pipeline hedging support helped stabilize gain-on-sale margins amid rate volatility, while correspondent and warehouse partners smoothed fulfillment and scale.

Payment networks and treasury ecosystem

Payment networks for debit, credit, ACH, wires and RTP/FedNow (FedNow launched July 2023) expand Wintrust client payment options and support faster settlement. Treasury tech partners improve receivables, payables and fraud controls, driving higher fee income and client stickiness. Integrated connections enable omni-channel cash management across digital, branch and API channels.

Community organizations and local businesses

Community organizations, local chambers, nonprofits and universities deepen Wintrust’s regional roots and pipeline for deposits and loans; in 2024 Wintrust operated over 160 branches and reported roughly $61 billion in assets, reinforcing local credibility. Referrals from realtors, CPAs and attorneys drive targeted customer acquisition; sponsorships and co-programs on financial literacy and small-business growth boost brand trust and retention.

- Local partners: chambers, universities, nonprofits

- Referral sources: realtors, CPAs, attorneys

- Outcomes: sponsorships, financial-literacy co-programs, SMB growth

Broker-dealers and asset managers

Broker-dealers and asset managers supply custodians, fund families and model portfolios that underpin Wintrust’s wealth and retirement solutions, supporting over $50 billion in client assets on the platform in 2024 and enabling open-architecture product breadth.

Research, analytics and third-party tools raise advisory quality while revenue-sharing and platform economics improve margins through scalable fee and custody arrangements.

- custodians

- open-architecture

- model portfolios

- research/tools

- revenue-sharing

Partnerships enable RTP/FedNow, 99.99% SLAs and mortgage/deposit liquidity

Partnerships with core platform, cybersecurity and payments vendors deliver scalable processing, APIs, RTP/FedNow support and enterprise SLAs (commonly 99.99%).

Mortgage investors, correspondent and warehouse partners enable whole-loan/MBS channels, pipeline hedging and balance-sheet flexibility to stabilize margins.

Community, referral and wealth partners drive deposit and advisory pipelines; Wintrust reported ~160 branches, ~$61B assets and ~$50B AUM in 2024.

| Partner | Role | 2024 metric |

|---|---|---|

| Core tech | Processing, APIs | 99.99% SLA |

| Payments | Settlement, fraud | FedNow/RTP live |

| Mortgage investors | Sale/servicing | Enhanced capital flexibility |

| Community/Wealth | Acquisition, custody | 160 branches; $61B assets; $50B AUM |

What is included in the product

A comprehensive Business Model Canvas for Wintrust Financial that maps customer segments, channels, value propositions, revenue streams and cost structure across the 9 BMC blocks, reflecting real-world banking operations, competitive advantages and SWOT-linked insights to support presentations, investor discussions and strategic decision-making.

High-level view of Wintrust Financial’s business model with editable cells to quickly distill banking operations, revenue streams, and risk levers into a single, shareable page for faster strategic decisions and team alignment.

Activities

Deposit gathering and relationship banking

Attracting and retaining low-cost, stable deposits is central to Wintrust’s funding strategy, supporting over $60 billion in deposits in 2024 and financing loan growth and margin stability. Relationship managers deepen ties across personal, business, and wealth needs to increase loyalty. Competitive pricing, community-branch presence, and service drive balances while disciplined cross-sell expands share of wallet and fee income.

Commercial and retail lending

Underwriting C&I, CRE, SBA and consumer loans — supporting local businesses and households — drove Wintrusts lending engine, with total loans of $58.6 billion at year-end 2024.

Rigorous credit discipline and portfolio diversification across sectors and geographies constrained loss rates and preserved capital ratios through 2024 stress periods.

Fast, local decision-making by community bankers speeds deployment, while ongoing monitoring and workout resources sustained asset quality and kept NPLs relatively low in 2024.

Wealth management and advisory

Wealth management and advisory at Wintrust combines financial planning, investment advisory, and trust services to address complex client needs, serving clients alongside the bank's broader balance sheet (Wintrust reported roughly $66 billion in total assets in 2024). Goals-based frameworks align portfolios to life stages, improving long-term outcomes and retention. Fiduciary oversight and integrated banking-wealth views strengthen credibility and drive cross-sell revenue.

Mortgage origination and fulfillment

Lending teams at Wintrust originate, process, and close mortgages efficiently, leveraging centralized fulfillment centers and digital loan pipelines to shorten turn times and boost conversion. Secondary market execution actively hedges rate risk and manages capital, supporting volume stability amid 2024 mortgage market volatility. Strong realtor and builder pipelines plus a focus on borrower experience drive referrals and repeat business.

- Origination efficiency

- Secondary market hedging

- Realtor/builder channels

- Borrower experience = referrals

Risk, compliance, and digital enablement

Risk, compliance, and digital enablement at Wintrust integrate ALM, credit, liquidity, and operational risk programs to safeguard resilience, with regulatory compliance embedded into processes and systems in 2024. Digital enhancements expanded UX and efficiency across channels, while analytics drive pricing, marketing, and credit decisions using 2024 transaction and portfolio data.

- ALM/credit/liquidity: ongoing program coverage in 2024

- Regulatory compliance: embedded in systems (2024)

- Digital UX/efficiency: expanded in 2024

- Data analytics: informs pricing, marketing, credit (2024)

Deposits fund growth: $60B+, $58.6B loans

Attracting and retaining low-cost deposits (over $60 billion in 2024) funds loan growth and margin stability. Underwriting C&I, CRE, SBA and consumer loans drove a $58.6 billion loan book at year-end 2024. Local decision-making, ALM/hedging, digital fulfillment and wealth advisory integrated to preserve asset quality and expand fee income.

| Metric | 2024 |

|---|---|

| Deposits | $60B+ |

| Loans | $58.6B |

| Total assets | $66B |

Full Document Unlocks After Purchase

Business Model Canvas

The Business Model Canvas for Wintrust Financial shown here is a true preview of the exact deliverable—not a mockup or sample. When you purchase, you’ll receive this same professional, ready-to-use file in editable Word and Excel formats. The full document includes all sections and content as previewed, ready for presentation, customization, and implementation.