WK Kellogg Co. Porter's Five Forces Analysis

From Overview to Strategy Blueprint

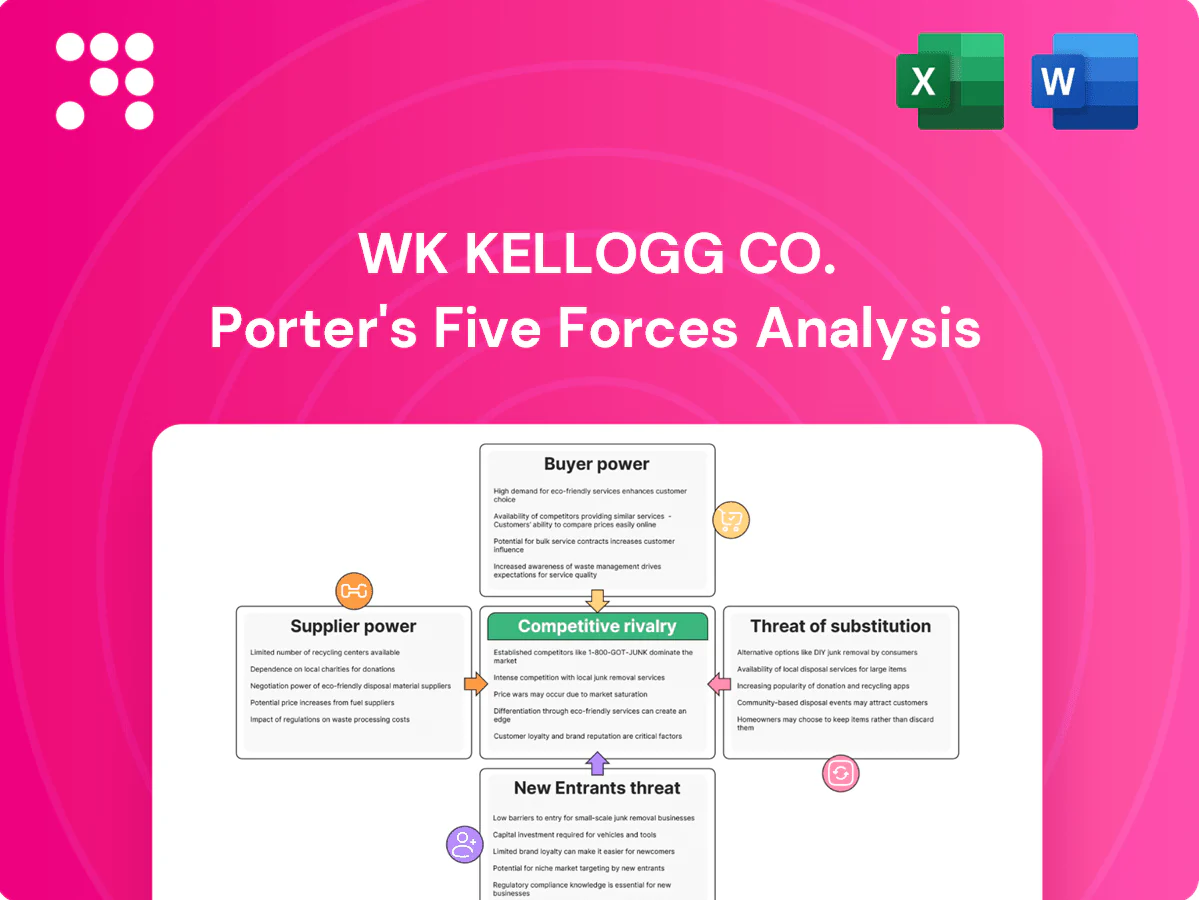

WK Kellogg Co. faces intense rivalry from global CPG brands and private labels, moderate supplier power for key commodities, strong buyer price sensitivity, and growing substitute threats from natural and DTC brands. Barriers to entry are moderate given scale and distribution advantages. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore WK Kellogg Co.’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Commoditized grain inputs

Core inputs like corn, wheat and sugar are highly commoditized, with US corn futures averaging about $4.50/bu and Chicago wheat near $7.00/bu in 2024, limiting individual farmer leverage. Weather- and trade-driven price swings (20–30% year-on-year moves seen in 2022–24) can compress Kellogg’s margins. Hedging and multi-sourcing reduce but do not remove commodity risk. Supplier power is moderate due to substitutability but elevated by high cyclicality.

Concentrated packaging vendors

In 2024 Kellogg relies on 3-4 major packaging firms for specialized cartons, liners and inks, concentrating supply and raising bargaining power. Machinery specs and food-safety certifications create meaningful switching costs and longer lead times. Supplier leverage can pressure pricing and timing, though long-term contracts and dual-qualification of vendors mitigate disruption risk.

Fortification and specialty inputs

Vitamins, minerals and specialty flavorings for Kellogg are concentrated among a limited set of certified global suppliers, including major ingredient firms such as DSM and BASF, which increases supplier leverage. Strict quality and regulatory requirements further narrow the vendor base, elevating the risk that disruptions will affect product formulation and on-pack labeling claims. Strategic long-term supply agreements and increased inventory buffers are used to mitigate this exposure and maintain shelf continuity.

Logistics and co-manufacturing

Logistics and co-manufacturing give suppliers stronger leverage for WK Kellogg Co., as tight freight markets in 2024 pushed contracted truck and co-packer premiums and raised delivered costs; fuel and labor constraints amplified margin pressure while regional redundancy reduced single-lane or plant dependency. Contracted capacity smooths throughput variability but carries a visible premium.

- WK Kellogg Co. launched Oct 2023; 2024 saw tight freight markets

- Fuel and labor spikes raised delivered costs

- Regional redundancy lowers single-point risk

- Contracted capacity stabilizes supply at a premium

Brand dependence vs. scale

WK Kellogg’s global scale (FY2023 net sales $13.6 billion) delivers volume leverage and preferred supplier status, tightening pricing and allocation in 2024; however strict branded quality specs and supplier qualifications limit rapid switching, preserving supplier bargaining clout. Joint planning, shared forecasting and demand visibility have improved terms and reduced volatility, so scale dampens but does not eliminate supplier power.

- Volume leverage: FY2023 net sales $13.6B

- Quality constraints: qualified supplier pools

- Mitigants: joint planning, demand visibility

- Net: supplier power reduced but persistent

Commoditized grains and concentrated packagers create margin volatility despite $13.6B scale

Core commodities (corn $4.50/bu; wheat $7.00/bu in 2024) are commoditized, limiting farmer leverage but creating margin volatility. Packaging and specialty ingredients are concentrated (3–4 major packagers; key suppliers like DSM/BASF), raising switching costs and supplier power. Scale (FY2023 net sales $13.6B) gives buying leverage but quality/certification needs keep supplier bargaining persistent.

| Metric | 2024/2023 |

|---|---|

| Corn | $4.50/bu (2024) |

| Wheat | $7.00/bu (2024) |

| FY2023 sales | $13.6B |

| Major packagers | 3–4 |

What is included in the product

Tailored Porter's Five Forces analysis of WK Kellogg Co. that uncovers competitive intensity from branded rivals and private labels, buyer and supplier leverage over pricing, threat of new entrants and substitutes (snacking trends and plant-based options), and industry barriers protecting incumbents, with strategic insights to inform pricing, innovation, and distribution decisions.

WK Kellogg Co. Porter's Five Forces one-sheet—your pain point reliever for quickly spotting supplier, buyer, rivalry, substitutes and new entrant pressures. Clean, customizable layout ready for decks or scenario comparisons to speed strategic decisions.

Customers Bargaining Power

Retail consolidation

Retail consolidation gives large chains and mass merchandisers outsized leverage over WK Kellogg Co., as Walmart, Kroger and Costco collectively account for roughly 40% of U.S. grocery sales (2024), enabling control of shelf space and demand for trade spend. Their scale forces tougher negotiations on price, promotions and costly slotting fees, compressing Kellogg margins. Losing a top retailer can cost material volume and revenue, so buyer power remains high among big-box and grocery leaders.

Low consumer switching costs

Low switching costs let shoppers substitute Kellogg across brands/flavors at shelf; Kellogg held roughly 30% of the US ready‑to‑eat cereal market in 2024, but promotions—present in about 40% of cereal transactions—drive trial and churn, keeping everyday pricing pressured and requiring frequent deal activity; loyalty depends on enduring brand equity and perceived health benefits to offset promo-driven switching.

Private label alternatives

Retailers pushed store brands to roughly 18% penetration in US grocery by 2024, promoting lower-priced private-label cereals that compress branded margins. Comparable taste profiles erode WK Kellogg Co’s pricing power for core SKUs, forcing emphasis on nutrition, product innovation, and targeted marketing. WK Kellogg must tightly manage price gaps to protect mix and gross margin.

Omnichannel transparency

- Price-comparison: higher buyer leverage

- Ratings: influence assortment velocity

- Digital shelf: favors top SKUs, compresses tail

- Data/promos: tool to rebalance power

Demand for health and sustainability

Consumers and retailers increasingly demand cleaner labels, whole grains and responsible sourcing, forcing WK Kellogg Co. to change formulations and supplier relationships; 2024 surveys show roughly 64% of shoppers prioritize healthier or sustainably sourced products, raising potential COGS and narrowing supplier options.

Meeting these demands can secure premium shelf placement and trust—retail listing gains can lift margins—whereas failure risks delisting or negative mix shifts toward lower-margin SKUs.

- Consumer demand: ~64% prioritize health/sustainability (2024)

- Cost impact: higher COGS and fewer approved suppliers

- Upside: premium placement, brand trust, better margins

- Downside: delisting risk, adverse mix shift

Retailer concentration and heavy promos squeeze cereal pricing power amid health focus

Concentrated retail buying (Walmart/Kroger/Costco ≈40% of US grocery sales in 2024) gives large chains strong leverage over WK Kellogg Co., forcing price, promo and slotting concessions. High promo incidence (~40% of cereal transactions) and low switching costs limit pricing power despite Kellogg's ~30% US ready‑to‑eat cereal share. Private‑label penetration (~18%) and online grocery (~12%) increase price sensitivity; ~64% of shoppers prioritize health/sustainability.

| Metric | 2024 Value |

|---|---|

| Top retailers share | ≈40% |

| Kellogg cereal share | ≈30% |

| Promo incidence (cereal) | ≈40% |

| Private‑label grocery | ≈18% |

| Online grocery | ≈12% |

| Shoppers prioritizing health | ≈64% |

Same Document Delivered

WK Kellogg Co. Porter's Five Forces Analysis

This preview shows the exact WK Kellogg Co. Porter's Five Forces Analysis you'll receive immediately after purchase—no surprises, fully formatted and ready to download. It assesses strong competitive rivalry, moderate buyer power, low-to-moderate supplier power, significant threat of substitutes, and moderate barriers to entry. Use it as a ready-to-use strategic input for valuation, market positioning, and risk assessment.

From Overview to Strategy Blueprint

WK Kellogg Co. faces intense rivalry from global CPG brands and private labels, moderate supplier power for key commodities, strong buyer price sensitivity, and growing substitute threats from natural and DTC brands. Barriers to entry are moderate given scale and distribution advantages. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore WK Kellogg Co.’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Commoditized grain inputs

Core inputs like corn, wheat and sugar are highly commoditized, with US corn futures averaging about $4.50/bu and Chicago wheat near $7.00/bu in 2024, limiting individual farmer leverage. Weather- and trade-driven price swings (20–30% year-on-year moves seen in 2022–24) can compress Kellogg’s margins. Hedging and multi-sourcing reduce but do not remove commodity risk. Supplier power is moderate due to substitutability but elevated by high cyclicality.

Concentrated packaging vendors

In 2024 Kellogg relies on 3-4 major packaging firms for specialized cartons, liners and inks, concentrating supply and raising bargaining power. Machinery specs and food-safety certifications create meaningful switching costs and longer lead times. Supplier leverage can pressure pricing and timing, though long-term contracts and dual-qualification of vendors mitigate disruption risk.

Fortification and specialty inputs

Vitamins, minerals and specialty flavorings for Kellogg are concentrated among a limited set of certified global suppliers, including major ingredient firms such as DSM and BASF, which increases supplier leverage. Strict quality and regulatory requirements further narrow the vendor base, elevating the risk that disruptions will affect product formulation and on-pack labeling claims. Strategic long-term supply agreements and increased inventory buffers are used to mitigate this exposure and maintain shelf continuity.

Logistics and co-manufacturing

Logistics and co-manufacturing give suppliers stronger leverage for WK Kellogg Co., as tight freight markets in 2024 pushed contracted truck and co-packer premiums and raised delivered costs; fuel and labor constraints amplified margin pressure while regional redundancy reduced single-lane or plant dependency. Contracted capacity smooths throughput variability but carries a visible premium.

- WK Kellogg Co. launched Oct 2023; 2024 saw tight freight markets

- Fuel and labor spikes raised delivered costs

- Regional redundancy lowers single-point risk

- Contracted capacity stabilizes supply at a premium

Brand dependence vs. scale

WK Kellogg’s global scale (FY2023 net sales $13.6 billion) delivers volume leverage and preferred supplier status, tightening pricing and allocation in 2024; however strict branded quality specs and supplier qualifications limit rapid switching, preserving supplier bargaining clout. Joint planning, shared forecasting and demand visibility have improved terms and reduced volatility, so scale dampens but does not eliminate supplier power.

- Volume leverage: FY2023 net sales $13.6B

- Quality constraints: qualified supplier pools

- Mitigants: joint planning, demand visibility

- Net: supplier power reduced but persistent

Commoditized grains and concentrated packagers create margin volatility despite $13.6B scale

Core commodities (corn $4.50/bu; wheat $7.00/bu in 2024) are commoditized, limiting farmer leverage but creating margin volatility. Packaging and specialty ingredients are concentrated (3–4 major packagers; key suppliers like DSM/BASF), raising switching costs and supplier power. Scale (FY2023 net sales $13.6B) gives buying leverage but quality/certification needs keep supplier bargaining persistent.

| Metric | 2024/2023 |

|---|---|

| Corn | $4.50/bu (2024) |

| Wheat | $7.00/bu (2024) |

| FY2023 sales | $13.6B |

| Major packagers | 3–4 |

What is included in the product

Tailored Porter's Five Forces analysis of WK Kellogg Co. that uncovers competitive intensity from branded rivals and private labels, buyer and supplier leverage over pricing, threat of new entrants and substitutes (snacking trends and plant-based options), and industry barriers protecting incumbents, with strategic insights to inform pricing, innovation, and distribution decisions.

WK Kellogg Co. Porter's Five Forces one-sheet—your pain point reliever for quickly spotting supplier, buyer, rivalry, substitutes and new entrant pressures. Clean, customizable layout ready for decks or scenario comparisons to speed strategic decisions.

Customers Bargaining Power

Retail consolidation

Retail consolidation gives large chains and mass merchandisers outsized leverage over WK Kellogg Co., as Walmart, Kroger and Costco collectively account for roughly 40% of U.S. grocery sales (2024), enabling control of shelf space and demand for trade spend. Their scale forces tougher negotiations on price, promotions and costly slotting fees, compressing Kellogg margins. Losing a top retailer can cost material volume and revenue, so buyer power remains high among big-box and grocery leaders.

Low consumer switching costs

Low switching costs let shoppers substitute Kellogg across brands/flavors at shelf; Kellogg held roughly 30% of the US ready‑to‑eat cereal market in 2024, but promotions—present in about 40% of cereal transactions—drive trial and churn, keeping everyday pricing pressured and requiring frequent deal activity; loyalty depends on enduring brand equity and perceived health benefits to offset promo-driven switching.

Private label alternatives

Retailers pushed store brands to roughly 18% penetration in US grocery by 2024, promoting lower-priced private-label cereals that compress branded margins. Comparable taste profiles erode WK Kellogg Co’s pricing power for core SKUs, forcing emphasis on nutrition, product innovation, and targeted marketing. WK Kellogg must tightly manage price gaps to protect mix and gross margin.

Omnichannel transparency

- Price-comparison: higher buyer leverage

- Ratings: influence assortment velocity

- Digital shelf: favors top SKUs, compresses tail

- Data/promos: tool to rebalance power

Demand for health and sustainability

Consumers and retailers increasingly demand cleaner labels, whole grains and responsible sourcing, forcing WK Kellogg Co. to change formulations and supplier relationships; 2024 surveys show roughly 64% of shoppers prioritize healthier or sustainably sourced products, raising potential COGS and narrowing supplier options.

Meeting these demands can secure premium shelf placement and trust—retail listing gains can lift margins—whereas failure risks delisting or negative mix shifts toward lower-margin SKUs.

- Consumer demand: ~64% prioritize health/sustainability (2024)

- Cost impact: higher COGS and fewer approved suppliers

- Upside: premium placement, brand trust, better margins

- Downside: delisting risk, adverse mix shift

Retailer concentration and heavy promos squeeze cereal pricing power amid health focus

Concentrated retail buying (Walmart/Kroger/Costco ≈40% of US grocery sales in 2024) gives large chains strong leverage over WK Kellogg Co., forcing price, promo and slotting concessions. High promo incidence (~40% of cereal transactions) and low switching costs limit pricing power despite Kellogg's ~30% US ready‑to‑eat cereal share. Private‑label penetration (~18%) and online grocery (~12%) increase price sensitivity; ~64% of shoppers prioritize health/sustainability.

| Metric | 2024 Value |

|---|---|

| Top retailers share | ≈40% |

| Kellogg cereal share | ≈30% |

| Promo incidence (cereal) | ≈40% |

| Private‑label grocery | ≈18% |

| Online grocery | ≈12% |

| Shoppers prioritizing health | ≈64% |

Same Document Delivered

WK Kellogg Co. Porter's Five Forces Analysis

This preview shows the exact WK Kellogg Co. Porter's Five Forces Analysis you'll receive immediately after purchase—no surprises, fully formatted and ready to download. It assesses strong competitive rivalry, moderate buyer power, low-to-moderate supplier power, significant threat of substitutes, and moderate barriers to entry. Use it as a ready-to-use strategic input for valuation, market positioning, and risk assessment.

Original: $10.00

-65%$10.00

$3.50Description

From Overview to Strategy Blueprint

WK Kellogg Co. faces intense rivalry from global CPG brands and private labels, moderate supplier power for key commodities, strong buyer price sensitivity, and growing substitute threats from natural and DTC brands. Barriers to entry are moderate given scale and distribution advantages. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore WK Kellogg Co.’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Commoditized grain inputs

Core inputs like corn, wheat and sugar are highly commoditized, with US corn futures averaging about $4.50/bu and Chicago wheat near $7.00/bu in 2024, limiting individual farmer leverage. Weather- and trade-driven price swings (20–30% year-on-year moves seen in 2022–24) can compress Kellogg’s margins. Hedging and multi-sourcing reduce but do not remove commodity risk. Supplier power is moderate due to substitutability but elevated by high cyclicality.

Concentrated packaging vendors

In 2024 Kellogg relies on 3-4 major packaging firms for specialized cartons, liners and inks, concentrating supply and raising bargaining power. Machinery specs and food-safety certifications create meaningful switching costs and longer lead times. Supplier leverage can pressure pricing and timing, though long-term contracts and dual-qualification of vendors mitigate disruption risk.

Fortification and specialty inputs

Vitamins, minerals and specialty flavorings for Kellogg are concentrated among a limited set of certified global suppliers, including major ingredient firms such as DSM and BASF, which increases supplier leverage. Strict quality and regulatory requirements further narrow the vendor base, elevating the risk that disruptions will affect product formulation and on-pack labeling claims. Strategic long-term supply agreements and increased inventory buffers are used to mitigate this exposure and maintain shelf continuity.

Logistics and co-manufacturing

Logistics and co-manufacturing give suppliers stronger leverage for WK Kellogg Co., as tight freight markets in 2024 pushed contracted truck and co-packer premiums and raised delivered costs; fuel and labor constraints amplified margin pressure while regional redundancy reduced single-lane or plant dependency. Contracted capacity smooths throughput variability but carries a visible premium.

- WK Kellogg Co. launched Oct 2023; 2024 saw tight freight markets

- Fuel and labor spikes raised delivered costs

- Regional redundancy lowers single-point risk

- Contracted capacity stabilizes supply at a premium

Brand dependence vs. scale

WK Kellogg’s global scale (FY2023 net sales $13.6 billion) delivers volume leverage and preferred supplier status, tightening pricing and allocation in 2024; however strict branded quality specs and supplier qualifications limit rapid switching, preserving supplier bargaining clout. Joint planning, shared forecasting and demand visibility have improved terms and reduced volatility, so scale dampens but does not eliminate supplier power.

- Volume leverage: FY2023 net sales $13.6B

- Quality constraints: qualified supplier pools

- Mitigants: joint planning, demand visibility

- Net: supplier power reduced but persistent

Commoditized grains and concentrated packagers create margin volatility despite $13.6B scale

Core commodities (corn $4.50/bu; wheat $7.00/bu in 2024) are commoditized, limiting farmer leverage but creating margin volatility. Packaging and specialty ingredients are concentrated (3–4 major packagers; key suppliers like DSM/BASF), raising switching costs and supplier power. Scale (FY2023 net sales $13.6B) gives buying leverage but quality/certification needs keep supplier bargaining persistent.

| Metric | 2024/2023 |

|---|---|

| Corn | $4.50/bu (2024) |

| Wheat | $7.00/bu (2024) |

| FY2023 sales | $13.6B |

| Major packagers | 3–4 |

What is included in the product

Tailored Porter's Five Forces analysis of WK Kellogg Co. that uncovers competitive intensity from branded rivals and private labels, buyer and supplier leverage over pricing, threat of new entrants and substitutes (snacking trends and plant-based options), and industry barriers protecting incumbents, with strategic insights to inform pricing, innovation, and distribution decisions.

WK Kellogg Co. Porter's Five Forces one-sheet—your pain point reliever for quickly spotting supplier, buyer, rivalry, substitutes and new entrant pressures. Clean, customizable layout ready for decks or scenario comparisons to speed strategic decisions.

Customers Bargaining Power

Retail consolidation

Retail consolidation gives large chains and mass merchandisers outsized leverage over WK Kellogg Co., as Walmart, Kroger and Costco collectively account for roughly 40% of U.S. grocery sales (2024), enabling control of shelf space and demand for trade spend. Their scale forces tougher negotiations on price, promotions and costly slotting fees, compressing Kellogg margins. Losing a top retailer can cost material volume and revenue, so buyer power remains high among big-box and grocery leaders.

Low consumer switching costs

Low switching costs let shoppers substitute Kellogg across brands/flavors at shelf; Kellogg held roughly 30% of the US ready‑to‑eat cereal market in 2024, but promotions—present in about 40% of cereal transactions—drive trial and churn, keeping everyday pricing pressured and requiring frequent deal activity; loyalty depends on enduring brand equity and perceived health benefits to offset promo-driven switching.

Private label alternatives

Retailers pushed store brands to roughly 18% penetration in US grocery by 2024, promoting lower-priced private-label cereals that compress branded margins. Comparable taste profiles erode WK Kellogg Co’s pricing power for core SKUs, forcing emphasis on nutrition, product innovation, and targeted marketing. WK Kellogg must tightly manage price gaps to protect mix and gross margin.

Omnichannel transparency

- Price-comparison: higher buyer leverage

- Ratings: influence assortment velocity

- Digital shelf: favors top SKUs, compresses tail

- Data/promos: tool to rebalance power

Demand for health and sustainability

Consumers and retailers increasingly demand cleaner labels, whole grains and responsible sourcing, forcing WK Kellogg Co. to change formulations and supplier relationships; 2024 surveys show roughly 64% of shoppers prioritize healthier or sustainably sourced products, raising potential COGS and narrowing supplier options.

Meeting these demands can secure premium shelf placement and trust—retail listing gains can lift margins—whereas failure risks delisting or negative mix shifts toward lower-margin SKUs.

- Consumer demand: ~64% prioritize health/sustainability (2024)

- Cost impact: higher COGS and fewer approved suppliers

- Upside: premium placement, brand trust, better margins

- Downside: delisting risk, adverse mix shift

Retailer concentration and heavy promos squeeze cereal pricing power amid health focus

Concentrated retail buying (Walmart/Kroger/Costco ≈40% of US grocery sales in 2024) gives large chains strong leverage over WK Kellogg Co., forcing price, promo and slotting concessions. High promo incidence (~40% of cereal transactions) and low switching costs limit pricing power despite Kellogg's ~30% US ready‑to‑eat cereal share. Private‑label penetration (~18%) and online grocery (~12%) increase price sensitivity; ~64% of shoppers prioritize health/sustainability.

| Metric | 2024 Value |

|---|---|

| Top retailers share | ≈40% |

| Kellogg cereal share | ≈30% |

| Promo incidence (cereal) | ≈40% |

| Private‑label grocery | ≈18% |

| Online grocery | ≈12% |

| Shoppers prioritizing health | ≈64% |

Same Document Delivered

WK Kellogg Co. Porter's Five Forces Analysis

This preview shows the exact WK Kellogg Co. Porter's Five Forces Analysis you'll receive immediately after purchase—no surprises, fully formatted and ready to download. It assesses strong competitive rivalry, moderate buyer power, low-to-moderate supplier power, significant threat of substitutes, and moderate barriers to entry. Use it as a ready-to-use strategic input for valuation, market positioning, and risk assessment.