Wolfspeed Porter's Five Forces Analysis

Go Beyond the Preview—Access the Full Strategic Report

Wolfspeed faces strong supplier leverage, rising competitive intensity in power electronics, and moderate buyer pressure shaped by industry consolidation. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Wolfspeed’s competitive dynamics, market pressures, and strategic advantages in detail.

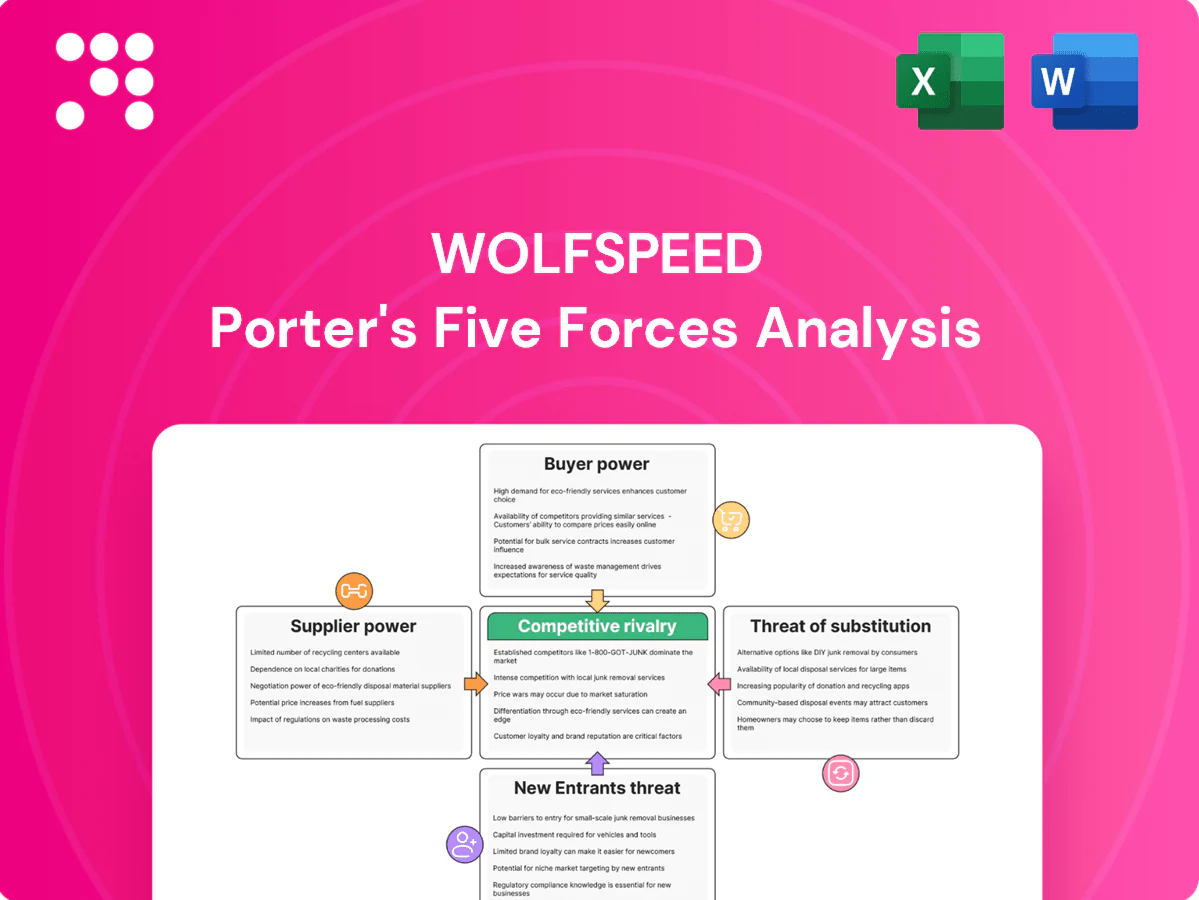

Suppliers Bargaining Power

Concentrated inputs

Suppliers of high‑purity SiC powders, specialty gases and epi reactors remain few and technically specialized, raising switching costs and lead times and were flagged in 2024 as a primary supply‑chain constraint for SiC device makers. This concentration can pressure pricing and delivery terms, with Tier‑1 vendors commanding premiums. Wolfspeed mitigates by vertical integration in substrates, owning epi/wafer capacity and using long‑term agreements to support 2024 capacity expansion.

Equipment dependence

Yield-critical tools for SiC crystal growth, wafering and epitaxy are concentrated among OEMs such as Aixtron, Veeco and Applied Materials, giving suppliers outsized leverage. Qualification and process transfer typically take months to years, enabling premium pricing on spare parts and service contracts. Wolfspeed and peers reduce exposure via multi-sourcing and growing in-house process IP, lowering long-term supplier dependence.

Material purity constraints

Ultra-high purity requirements (typically 6N–7N, 99.9999–99.99999%) for chemicals, graphite and ceramics narrow Wolfspeed’s supplier base and raise concentration risk. Even small quality drift can cause single- to double-digit percentage hits to device yields, giving suppliers leverage through tight specs and allocation. Rigorous incoming QA and dual-qualification strategies are used to rebalance supplier power and protect throughput.

Energy and utilities

Crystal growth and epitaxy are highly energy‑intensive, tying Wolfspeed’s fab economics to reliable power and industrial gas infrastructure; semiconductor fabs typically demand 10–100 MW of continuous power (industry data, 2024). Utility pricing and availability directly affect margins, while federal and state programs in 2024 helped offset some energy capex; multi‑site footprint reduces location‑specific supplier leverage.

- High energy intensity: 10–100 MW typical (2024)

- Utility costs materially affect COGS

- 2024 federal/state programs can offset energy capex

- Site diversification lowers single‑location supplier power

Geopolitical exposure

Export controls and trade policies in 2024 tightened access to advanced tools and materials, directly affecting Wolfspeed supply chains; US export restrictions on advanced semiconductors to China increased sourcing complexity. Sanctions and licensing hurdles narrowed supplier options while suppliers often favor markets with fewer restrictions, raising supply concentration risk. Proactive compliance and localized sourcing, supported by the CHIPS Act $52 billion incentives, mitigate disruption.

- Export controls: heightened in 2024

- Supplier preference: markets with fewer restrictions

- Risk mitigation: compliance + local sourcing

Concentrated SiC supply and energy-intensive fabs drive pricing power after 2024 shortages

Suppliers of SiC powders, epi reactors and specialty gases remain concentrated, increasing switching costs and pricing power; 2024 shortages were a primary constraint. Wolfspeed lowers exposure via vertical integration (wafers/epi), multi‑sourcing and long‑term contracts. Energy intensity (10–100 MW fabs) and tightened 2024 export controls further amplify supplier leverage.

| Metric | 2024 |

|---|---|

| Fab power | 10–100 MW |

| CHIPS funding | $52B |

| Purity | 6N–7N |

What is included in the product

Tailored Porter's Five Forces analysis for Wolfspeed that uncovers key competitive drivers, supplier and buyer power, threats from substitutes and new entrants, and strategic levers to protect market share and profitability.

Concise Porter's Five Forces for Wolfspeed, clearly mapping supplier/customer power, competitive intensity, entrant risk and substitutes—ideal for quick strategic decisions, slide-ready summaries, and stress-testing scenarios.

Customers Bargaining Power

Large OEM buyers

Large EV, renewable and industrial power OEMs buy high volumes and negotiate aggressively, using scale to benchmark SiC pricing across vendors. Design-in cycles and rigorous qualification create stickiness, raising switching costs and locking in designs. Multi-year supply agreements, commonly 3–5 years, balance bargaining power by securing capacity for suppliers while providing price and delivery commitments for OEMs.

Design-in switching costs

SiC devices are deeply integrated into inverter and module designs, making design-in changes costly; Wolfspeed reported roughly $1.08 billion in 2024 revenue, reflecting strong OEM reliance. Requalification typically requires 6–12 months and affects timelines, certifications and yields, reducing buyer willingness to switch quickly. These barriers give Wolfspeed pricing and allocation discipline with strategic customers.

Dual-sourcing trends

Many Wolfspeed customers pursue second sources among major SiC vendors, increasing buyer leverage at renewals. Dual-sourcing bids helped buyers negotiate price concessions and flexibility in 2024 as supply chains normalized. However global SiC capacity tightness (utilizations often above 90% in 2024) caps buyer power. Priority allocations continue to favor long-term strategic partners.

Total system economics

Buyers evaluate total system economics — $/kW, efficiency and thermal advantages — not just die price; SiC typically delivers 1–3 percentage points higher efficiency and can cut system cost up to 20%, supporting Wolfspeed’s value-based pricing, while marginal system benefits trigger tougher price negotiation. Wolfspeed’s application support and reference designs help justify premiums by accelerating integration and lowering development cost.

Module vs. discrete mix

Customers purchasing full modules gain greater negotiating leverage than buyers of discrete dies because modules bundle system-level value and procurement simplicity, shifting pricing focus from component cost to total solution value.

Integration moves value capture toward system suppliers, allowing Wolfspeed’s module offerings to protect margins through higher ASPs and bundled services; custom module designs further raise switching costs by embedding Wolfspeed into customers’ supply chains and system designs.

- Module buyers = higher negotiating leverage

- Integration shifts value to system suppliers

- Wolfspeed modules defend margins via higher ASPs

- Custom solutions increase switching costs

OEM scale vs supplier leverage — $1.08B, >90% SiC use

Large OEMs exert strong price pressure via high-volume buying and dual-sourcing, but Wolfspeed’s $1.08B 2024 revenue, >90% SiC utilization and 6–12 month requalification windows give suppliers leverage; multi-year 3–5 year contracts balance power. System-level metrics (1–3 pp efficiency gain, up to 20% system cost reduction) limit pure price-driven switching.

| Metric | 2024 |

|---|---|

| Wolfspeed revenue | $1.08B |

| SiC utilization | >90% |

| Requalification | 6–12 months |

| Contracts | 3–5 yrs |

| Efficiency gain | 1–3 pp |

| System cost red. | up to 20% |

Preview Before You Purchase

Wolfspeed Porter's Five Forces Analysis

This preview shows the exact Porter's Five Forces analysis for Wolfspeed you'll receive immediately after purchase—no surprises or placeholders. The document is fully formatted, professionally written, and ready for download and use the moment you buy. You're viewing the final deliverable; once payment completes you'll have instant access to this same file.

Go Beyond the Preview—Access the Full Strategic Report

Wolfspeed faces strong supplier leverage, rising competitive intensity in power electronics, and moderate buyer pressure shaped by industry consolidation. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Wolfspeed’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentrated inputs

Suppliers of high‑purity SiC powders, specialty gases and epi reactors remain few and technically specialized, raising switching costs and lead times and were flagged in 2024 as a primary supply‑chain constraint for SiC device makers. This concentration can pressure pricing and delivery terms, with Tier‑1 vendors commanding premiums. Wolfspeed mitigates by vertical integration in substrates, owning epi/wafer capacity and using long‑term agreements to support 2024 capacity expansion.

Equipment dependence

Yield-critical tools for SiC crystal growth, wafering and epitaxy are concentrated among OEMs such as Aixtron, Veeco and Applied Materials, giving suppliers outsized leverage. Qualification and process transfer typically take months to years, enabling premium pricing on spare parts and service contracts. Wolfspeed and peers reduce exposure via multi-sourcing and growing in-house process IP, lowering long-term supplier dependence.

Material purity constraints

Ultra-high purity requirements (typically 6N–7N, 99.9999–99.99999%) for chemicals, graphite and ceramics narrow Wolfspeed’s supplier base and raise concentration risk. Even small quality drift can cause single- to double-digit percentage hits to device yields, giving suppliers leverage through tight specs and allocation. Rigorous incoming QA and dual-qualification strategies are used to rebalance supplier power and protect throughput.

Energy and utilities

Crystal growth and epitaxy are highly energy‑intensive, tying Wolfspeed’s fab economics to reliable power and industrial gas infrastructure; semiconductor fabs typically demand 10–100 MW of continuous power (industry data, 2024). Utility pricing and availability directly affect margins, while federal and state programs in 2024 helped offset some energy capex; multi‑site footprint reduces location‑specific supplier leverage.

- High energy intensity: 10–100 MW typical (2024)

- Utility costs materially affect COGS

- 2024 federal/state programs can offset energy capex

- Site diversification lowers single‑location supplier power

Geopolitical exposure

Export controls and trade policies in 2024 tightened access to advanced tools and materials, directly affecting Wolfspeed supply chains; US export restrictions on advanced semiconductors to China increased sourcing complexity. Sanctions and licensing hurdles narrowed supplier options while suppliers often favor markets with fewer restrictions, raising supply concentration risk. Proactive compliance and localized sourcing, supported by the CHIPS Act $52 billion incentives, mitigate disruption.

- Export controls: heightened in 2024

- Supplier preference: markets with fewer restrictions

- Risk mitigation: compliance + local sourcing

Concentrated SiC supply and energy-intensive fabs drive pricing power after 2024 shortages

Suppliers of SiC powders, epi reactors and specialty gases remain concentrated, increasing switching costs and pricing power; 2024 shortages were a primary constraint. Wolfspeed lowers exposure via vertical integration (wafers/epi), multi‑sourcing and long‑term contracts. Energy intensity (10–100 MW fabs) and tightened 2024 export controls further amplify supplier leverage.

| Metric | 2024 |

|---|---|

| Fab power | 10–100 MW |

| CHIPS funding | $52B |

| Purity | 6N–7N |

What is included in the product

Tailored Porter's Five Forces analysis for Wolfspeed that uncovers key competitive drivers, supplier and buyer power, threats from substitutes and new entrants, and strategic levers to protect market share and profitability.

Concise Porter's Five Forces for Wolfspeed, clearly mapping supplier/customer power, competitive intensity, entrant risk and substitutes—ideal for quick strategic decisions, slide-ready summaries, and stress-testing scenarios.

Customers Bargaining Power

Large OEM buyers

Large EV, renewable and industrial power OEMs buy high volumes and negotiate aggressively, using scale to benchmark SiC pricing across vendors. Design-in cycles and rigorous qualification create stickiness, raising switching costs and locking in designs. Multi-year supply agreements, commonly 3–5 years, balance bargaining power by securing capacity for suppliers while providing price and delivery commitments for OEMs.

Design-in switching costs

SiC devices are deeply integrated into inverter and module designs, making design-in changes costly; Wolfspeed reported roughly $1.08 billion in 2024 revenue, reflecting strong OEM reliance. Requalification typically requires 6–12 months and affects timelines, certifications and yields, reducing buyer willingness to switch quickly. These barriers give Wolfspeed pricing and allocation discipline with strategic customers.

Dual-sourcing trends

Many Wolfspeed customers pursue second sources among major SiC vendors, increasing buyer leverage at renewals. Dual-sourcing bids helped buyers negotiate price concessions and flexibility in 2024 as supply chains normalized. However global SiC capacity tightness (utilizations often above 90% in 2024) caps buyer power. Priority allocations continue to favor long-term strategic partners.

Total system economics

Buyers evaluate total system economics — $/kW, efficiency and thermal advantages — not just die price; SiC typically delivers 1–3 percentage points higher efficiency and can cut system cost up to 20%, supporting Wolfspeed’s value-based pricing, while marginal system benefits trigger tougher price negotiation. Wolfspeed’s application support and reference designs help justify premiums by accelerating integration and lowering development cost.

Module vs. discrete mix

Customers purchasing full modules gain greater negotiating leverage than buyers of discrete dies because modules bundle system-level value and procurement simplicity, shifting pricing focus from component cost to total solution value.

Integration moves value capture toward system suppliers, allowing Wolfspeed’s module offerings to protect margins through higher ASPs and bundled services; custom module designs further raise switching costs by embedding Wolfspeed into customers’ supply chains and system designs.

- Module buyers = higher negotiating leverage

- Integration shifts value to system suppliers

- Wolfspeed modules defend margins via higher ASPs

- Custom solutions increase switching costs

OEM scale vs supplier leverage — $1.08B, >90% SiC use

Large OEMs exert strong price pressure via high-volume buying and dual-sourcing, but Wolfspeed’s $1.08B 2024 revenue, >90% SiC utilization and 6–12 month requalification windows give suppliers leverage; multi-year 3–5 year contracts balance power. System-level metrics (1–3 pp efficiency gain, up to 20% system cost reduction) limit pure price-driven switching.

| Metric | 2024 |

|---|---|

| Wolfspeed revenue | $1.08B |

| SiC utilization | >90% |

| Requalification | 6–12 months |

| Contracts | 3–5 yrs |

| Efficiency gain | 1–3 pp |

| System cost red. | up to 20% |

Preview Before You Purchase

Wolfspeed Porter's Five Forces Analysis

This preview shows the exact Porter's Five Forces analysis for Wolfspeed you'll receive immediately after purchase—no surprises or placeholders. The document is fully formatted, professionally written, and ready for download and use the moment you buy. You're viewing the final deliverable; once payment completes you'll have instant access to this same file.

Original: $10.00

-65%$10.00

$3.50Description

Go Beyond the Preview—Access the Full Strategic Report

Wolfspeed faces strong supplier leverage, rising competitive intensity in power electronics, and moderate buyer pressure shaped by industry consolidation. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Wolfspeed’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentrated inputs

Suppliers of high‑purity SiC powders, specialty gases and epi reactors remain few and technically specialized, raising switching costs and lead times and were flagged in 2024 as a primary supply‑chain constraint for SiC device makers. This concentration can pressure pricing and delivery terms, with Tier‑1 vendors commanding premiums. Wolfspeed mitigates by vertical integration in substrates, owning epi/wafer capacity and using long‑term agreements to support 2024 capacity expansion.

Equipment dependence

Yield-critical tools for SiC crystal growth, wafering and epitaxy are concentrated among OEMs such as Aixtron, Veeco and Applied Materials, giving suppliers outsized leverage. Qualification and process transfer typically take months to years, enabling premium pricing on spare parts and service contracts. Wolfspeed and peers reduce exposure via multi-sourcing and growing in-house process IP, lowering long-term supplier dependence.

Material purity constraints

Ultra-high purity requirements (typically 6N–7N, 99.9999–99.99999%) for chemicals, graphite and ceramics narrow Wolfspeed’s supplier base and raise concentration risk. Even small quality drift can cause single- to double-digit percentage hits to device yields, giving suppliers leverage through tight specs and allocation. Rigorous incoming QA and dual-qualification strategies are used to rebalance supplier power and protect throughput.

Energy and utilities

Crystal growth and epitaxy are highly energy‑intensive, tying Wolfspeed’s fab economics to reliable power and industrial gas infrastructure; semiconductor fabs typically demand 10–100 MW of continuous power (industry data, 2024). Utility pricing and availability directly affect margins, while federal and state programs in 2024 helped offset some energy capex; multi‑site footprint reduces location‑specific supplier leverage.

- High energy intensity: 10–100 MW typical (2024)

- Utility costs materially affect COGS

- 2024 federal/state programs can offset energy capex

- Site diversification lowers single‑location supplier power

Geopolitical exposure

Export controls and trade policies in 2024 tightened access to advanced tools and materials, directly affecting Wolfspeed supply chains; US export restrictions on advanced semiconductors to China increased sourcing complexity. Sanctions and licensing hurdles narrowed supplier options while suppliers often favor markets with fewer restrictions, raising supply concentration risk. Proactive compliance and localized sourcing, supported by the CHIPS Act $52 billion incentives, mitigate disruption.

- Export controls: heightened in 2024

- Supplier preference: markets with fewer restrictions

- Risk mitigation: compliance + local sourcing

Concentrated SiC supply and energy-intensive fabs drive pricing power after 2024 shortages

Suppliers of SiC powders, epi reactors and specialty gases remain concentrated, increasing switching costs and pricing power; 2024 shortages were a primary constraint. Wolfspeed lowers exposure via vertical integration (wafers/epi), multi‑sourcing and long‑term contracts. Energy intensity (10–100 MW fabs) and tightened 2024 export controls further amplify supplier leverage.

| Metric | 2024 |

|---|---|

| Fab power | 10–100 MW |

| CHIPS funding | $52B |

| Purity | 6N–7N |

What is included in the product

Tailored Porter's Five Forces analysis for Wolfspeed that uncovers key competitive drivers, supplier and buyer power, threats from substitutes and new entrants, and strategic levers to protect market share and profitability.

Concise Porter's Five Forces for Wolfspeed, clearly mapping supplier/customer power, competitive intensity, entrant risk and substitutes—ideal for quick strategic decisions, slide-ready summaries, and stress-testing scenarios.

Customers Bargaining Power

Large OEM buyers

Large EV, renewable and industrial power OEMs buy high volumes and negotiate aggressively, using scale to benchmark SiC pricing across vendors. Design-in cycles and rigorous qualification create stickiness, raising switching costs and locking in designs. Multi-year supply agreements, commonly 3–5 years, balance bargaining power by securing capacity for suppliers while providing price and delivery commitments for OEMs.

Design-in switching costs

SiC devices are deeply integrated into inverter and module designs, making design-in changes costly; Wolfspeed reported roughly $1.08 billion in 2024 revenue, reflecting strong OEM reliance. Requalification typically requires 6–12 months and affects timelines, certifications and yields, reducing buyer willingness to switch quickly. These barriers give Wolfspeed pricing and allocation discipline with strategic customers.

Dual-sourcing trends

Many Wolfspeed customers pursue second sources among major SiC vendors, increasing buyer leverage at renewals. Dual-sourcing bids helped buyers negotiate price concessions and flexibility in 2024 as supply chains normalized. However global SiC capacity tightness (utilizations often above 90% in 2024) caps buyer power. Priority allocations continue to favor long-term strategic partners.

Total system economics

Buyers evaluate total system economics — $/kW, efficiency and thermal advantages — not just die price; SiC typically delivers 1–3 percentage points higher efficiency and can cut system cost up to 20%, supporting Wolfspeed’s value-based pricing, while marginal system benefits trigger tougher price negotiation. Wolfspeed’s application support and reference designs help justify premiums by accelerating integration and lowering development cost.

Module vs. discrete mix

Customers purchasing full modules gain greater negotiating leverage than buyers of discrete dies because modules bundle system-level value and procurement simplicity, shifting pricing focus from component cost to total solution value.

Integration moves value capture toward system suppliers, allowing Wolfspeed’s module offerings to protect margins through higher ASPs and bundled services; custom module designs further raise switching costs by embedding Wolfspeed into customers’ supply chains and system designs.

- Module buyers = higher negotiating leverage

- Integration shifts value to system suppliers

- Wolfspeed modules defend margins via higher ASPs

- Custom solutions increase switching costs

OEM scale vs supplier leverage — $1.08B, >90% SiC use

Large OEMs exert strong price pressure via high-volume buying and dual-sourcing, but Wolfspeed’s $1.08B 2024 revenue, >90% SiC utilization and 6–12 month requalification windows give suppliers leverage; multi-year 3–5 year contracts balance power. System-level metrics (1–3 pp efficiency gain, up to 20% system cost reduction) limit pure price-driven switching.

| Metric | 2024 |

|---|---|

| Wolfspeed revenue | $1.08B |

| SiC utilization | >90% |

| Requalification | 6–12 months |

| Contracts | 3–5 yrs |

| Efficiency gain | 1–3 pp |

| System cost red. | up to 20% |

Preview Before You Purchase

Wolfspeed Porter's Five Forces Analysis

This preview shows the exact Porter's Five Forces analysis for Wolfspeed you'll receive immediately after purchase—no surprises or placeholders. The document is fully formatted, professionally written, and ready for download and use the moment you buy. You're viewing the final deliverable; once payment completes you'll have instant access to this same file.