John Wood Group Boston Consulting Group Matrix

Unlock Strategic Clarity

Curious where John Wood Group’s offerings sit—Stars, Cash Cows, Dogs, or Question Marks? This preview sketches the picture; the full BCG Matrix gives quadrant-by-quadrant placement, data-backed recommendations, and tactical next steps you can act on. Buy the complete report for a ready-to-use Word and Excel pack that saves hours and sharpens your investment moves. Get instant access and start reallocating smarter today.

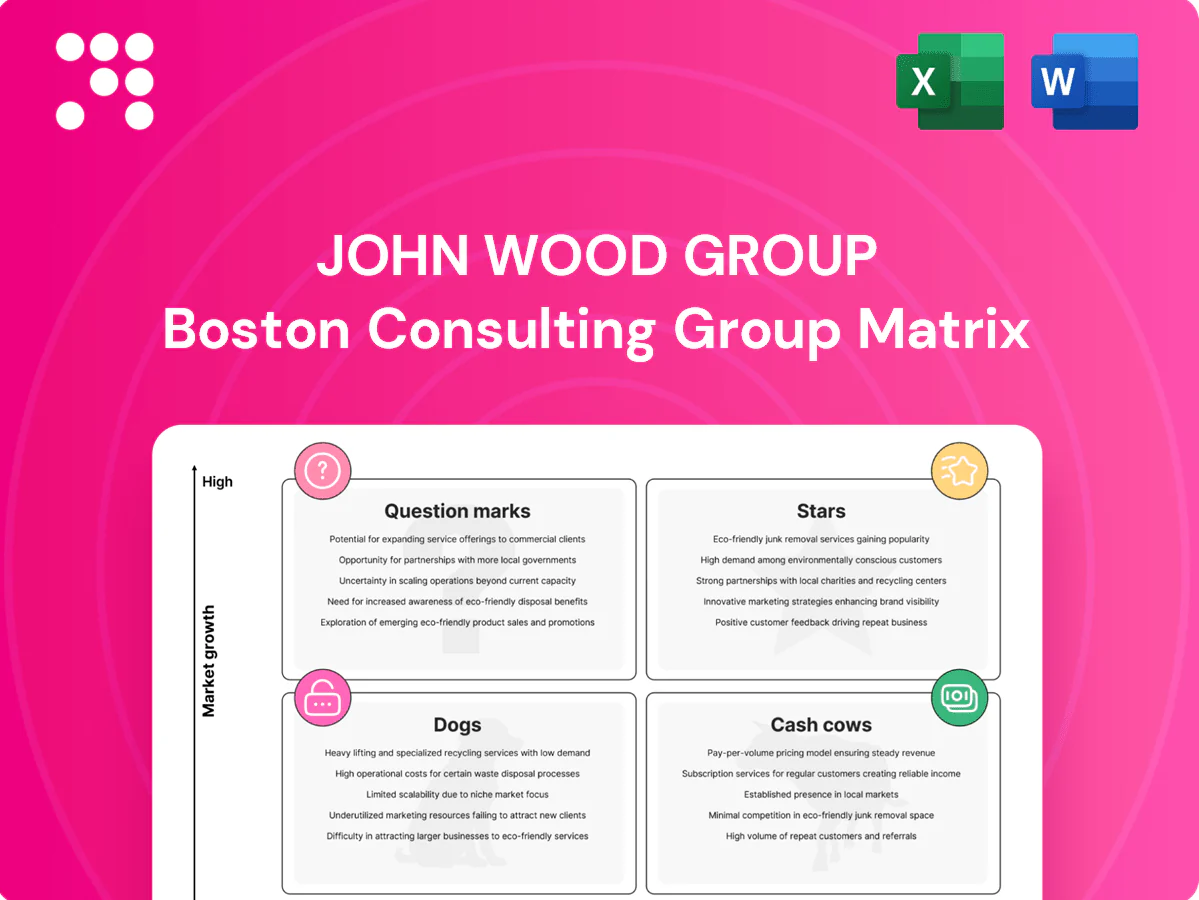

Stars

Decarbonization consulting & CCUS programs

High-growth demand for decarbonization and CCUS—IEA says global CCUS capacity must scale roughly 6–19x by 2030—puts this squarely in the hotspot for Wood. Wood’s advisory-to-delivery span secures strong share in select regions and sectors, backed by a project pipeline targeting >200 MtCO2 by 2030. It still needs focused investment in talent, partnerships, and reference projects to lock leadership; sustained funding will turn it into a powerhouse cash engine.

Hydrogen and low-carbon fuels engineering

Hydrogen, SAF and biofuels are scaling rapidly and demand complex engineering—an explicit Wood sweet spot as low-carbon project pipelines expanded in 2024. Early wins and credibility drive momentum, though capex cycles remain lumpy and can compress returns. Active marketing, pilots and strategic alliances keep the pipeline warm and de‑risk bids. With scale, standardization and repeatable EPC execution this segment can convert to dependable, higher-margin returns.

Digital asset performance & optimization

APM, analytics and data-led operations are gaining traction across brownfield assets, with 2024 industry surveys showing roughly 70% of operators prioritizing digital optimization. Wood’s engineering domain know‑how makes digital work stickier and higher-margin, turning platform-backed APM into ongoing platform investment and client enablement. If adoption endures, these projects convert to durable annuities with strong cross-sell potential.

Integrated project management for energy transition

Large low‑carbon builds require tight PMO, assurance and risk control — high growth, higher stakes as global clean‑energy investment rose to about $1.7tn in 2024; Wood’s multi‑discipline coverage secures a visible seat at the table but mobilization and systems can consume 2–5% of project value. Nail delivery, retain share, and it compounds into category leadership.

- Growth: high demand, ~$1.7tn clean‑energy spend (2024)

- Strength: multi‑discipline presence = strategic access

- Risk: mobilization cash burn ~2–5% of capex

- Outcome: delivery drives sustained market share

Sustainable materials & circular process engineering

Clients are retooling for circularity, waste-to-value and lower‑carbon chemistries as global plastic production remains near 400 million tonnes annually (2023–24), creating niche engineering demand where Wood’s early-mover credibility in chemical recycling and solvent recovery gives leverage in select projects. Scale is uneven; prioritized case studies and replicable EPC frameworks are needed to convert pilot wins into scalable revenue. Invest now to help set standards and capture premium margins before suppliers standardize.

- tag:early-mover

- tag:case-studies

- tag:invest-now

Scale or stall: CCUS must grow 6-19x by 2030 as $1.7tn clean-energy spend fuels demand

High-growth decarbonization (IEA CCUS 6–19x by 2030) and Wood’s >200 MtCO2 by 2030 pipeline position Stars for scale; 2024 clean‑energy spend ~$1.7tn and ~70% operator digital priority drive demand. Execution risk: mobilization cash burn ~2–5% capex; invest in talent, pilots and alliances to convert to durable cash engines.

| Metric | 2024/2030 |

|---|---|

| Clean‑energy spend | $1.7tn (2024) |

| CCUS scale need | 6–19x by 2030 |

| Wood pipeline | >200 MtCO2 by 2030 |

What is included in the product

Concise BCG Matrix review of John Wood Group: stars, cash cows, question marks, and dogs with clear invest, hold, divest guidance.

One-page BCG matrix for John Wood Group, clarifying unit roles and easing portfolio decisions for faster strategic focus.

Cash Cows

Operations & maintenance for mature assets

Recurring O&M across upstream, midstream and processing remains a dependable earner for John Wood Group, contributing about 30% of group revenue in 2024 and underpinning cash generation. Established contracts, embedded on-site teams and specialist know-how sustain steady cash flow and operating margins near 10% in 2024. Growth is modest, but high utilization and strong safety performance keep margins healthy. Optimize delivery and keep churn low — milk, don’t overfeed.

Brownfield engineering & modifications

Tie-ins, debottlenecking and life‑extension work drive steady brownfield revenue in mature basins; Wood’s scale and standardized playbooks lower unit cost and client risk. Not high-growth but defendable share with strong cash conversion—Wood reported FY2024 revenue of $6.3bn and maintained high operating cash conversion. Discipline on scope, standardization and protection of key frame agreements preserves margins and repeat work.

Integrity, reliability, and inspection services

Statutory and risk-driven inspection work remains non‑discretionary and delivers steady revenue for Wood’s inspection and integrity services, with high utilization, repeat scopes, and embedded tooling driving strong cash generation. Growth ceiling is modest, but targeted add‑ons and bundling raise yield per contract. Maintain a lean bench and strict process controls to protect margin.

Framework consulting with IOCs/NOCs

Framework consulting with IOCs/NOCs delivers predictable throughput via multi‑year (typically 3–7 year) advisory and engineering agreements, low sales friction and stable billing rates; contribution margins for E&C framework work generally run in the 20–30% range and market growth in 2024 was flat (~0–1% CAGR) for upstream services. Focus on delivery quality and incremental scope capture keeps wallet share defensible.

- Duration: 3–7 years

- Market growth 2024: ~0–1% CAGR

- Typical margins: 20–30%

- Client retention: high, >80%

- Priority: delivery quality + scope uplift

Midstream operations support & pipeline services

Midstream operations and pipeline services sit as Cash Cows for Wood: stable, regulated-like spend patterns underpin reliable volumes and FY2024 disclosures show steady midstream revenues and backlog, supporting predictable cash generation. Wood’s long-standing client relationships and delivery track record sustain pricing and contract renewals while modest innovation needs keep capital expenditure low. Focus on margin-enhancing efficiency and broader service bundles to maximize free cash flow.

- Stable volumes: regulated-like spend

- Pricing power: strong renewal rates

- Low capex: limited innovation needs

- Value drivers: efficiency and service breadth

Stable cash from recurring O&M - $6.3bn, ~30% O&M

Recurring O&M, midstream services and inspection work generate predictable cash for John Wood Group, with FY2024 revenue $6.3bn and recurring O&M ~30% of group revenue, O&M margins ~10%. Framework E&C yields 20–30% margins and client retention >80%, supporting high cash conversion. Focus: efficiency, standardization and scope uplift to preserve cash flows.

| Metric | 2024 |

|---|---|

| Group revenue | $6.3bn |

| Recurring O&M share | ~30% |

| O&M margin | ~10% |

| Framework margins | 20–30% |

| Client retention | >80% |

What You’re Viewing Is Included

John Wood Group BCG Matrix

The John Wood Group BCG Matrix you’re previewing on this page is the exact file you’ll get after purchase. No watermarks, no demo placeholders—just a fully formatted, ready-to-use strategic report tailored for clarity. Buy once and the final document is delivered straight to your inbox, editable, printable, and presentation-ready. It’s the same analysis-backed matrix shown here, crafted for decision-makers who need to act fast.

Unlock Strategic Clarity

Curious where John Wood Group’s offerings sit—Stars, Cash Cows, Dogs, or Question Marks? This preview sketches the picture; the full BCG Matrix gives quadrant-by-quadrant placement, data-backed recommendations, and tactical next steps you can act on. Buy the complete report for a ready-to-use Word and Excel pack that saves hours and sharpens your investment moves. Get instant access and start reallocating smarter today.

Stars

Decarbonization consulting & CCUS programs

High-growth demand for decarbonization and CCUS—IEA says global CCUS capacity must scale roughly 6–19x by 2030—puts this squarely in the hotspot for Wood. Wood’s advisory-to-delivery span secures strong share in select regions and sectors, backed by a project pipeline targeting >200 MtCO2 by 2030. It still needs focused investment in talent, partnerships, and reference projects to lock leadership; sustained funding will turn it into a powerhouse cash engine.

Hydrogen and low-carbon fuels engineering

Hydrogen, SAF and biofuels are scaling rapidly and demand complex engineering—an explicit Wood sweet spot as low-carbon project pipelines expanded in 2024. Early wins and credibility drive momentum, though capex cycles remain lumpy and can compress returns. Active marketing, pilots and strategic alliances keep the pipeline warm and de‑risk bids. With scale, standardization and repeatable EPC execution this segment can convert to dependable, higher-margin returns.

Digital asset performance & optimization

APM, analytics and data-led operations are gaining traction across brownfield assets, with 2024 industry surveys showing roughly 70% of operators prioritizing digital optimization. Wood’s engineering domain know‑how makes digital work stickier and higher-margin, turning platform-backed APM into ongoing platform investment and client enablement. If adoption endures, these projects convert to durable annuities with strong cross-sell potential.

Integrated project management for energy transition

Large low‑carbon builds require tight PMO, assurance and risk control — high growth, higher stakes as global clean‑energy investment rose to about $1.7tn in 2024; Wood’s multi‑discipline coverage secures a visible seat at the table but mobilization and systems can consume 2–5% of project value. Nail delivery, retain share, and it compounds into category leadership.

- Growth: high demand, ~$1.7tn clean‑energy spend (2024)

- Strength: multi‑discipline presence = strategic access

- Risk: mobilization cash burn ~2–5% of capex

- Outcome: delivery drives sustained market share

Sustainable materials & circular process engineering

Clients are retooling for circularity, waste-to-value and lower‑carbon chemistries as global plastic production remains near 400 million tonnes annually (2023–24), creating niche engineering demand where Wood’s early-mover credibility in chemical recycling and solvent recovery gives leverage in select projects. Scale is uneven; prioritized case studies and replicable EPC frameworks are needed to convert pilot wins into scalable revenue. Invest now to help set standards and capture premium margins before suppliers standardize.

- tag:early-mover

- tag:case-studies

- tag:invest-now

Scale or stall: CCUS must grow 6-19x by 2030 as $1.7tn clean-energy spend fuels demand

High-growth decarbonization (IEA CCUS 6–19x by 2030) and Wood’s >200 MtCO2 by 2030 pipeline position Stars for scale; 2024 clean‑energy spend ~$1.7tn and ~70% operator digital priority drive demand. Execution risk: mobilization cash burn ~2–5% capex; invest in talent, pilots and alliances to convert to durable cash engines.

| Metric | 2024/2030 |

|---|---|

| Clean‑energy spend | $1.7tn (2024) |

| CCUS scale need | 6–19x by 2030 |

| Wood pipeline | >200 MtCO2 by 2030 |

What is included in the product

Concise BCG Matrix review of John Wood Group: stars, cash cows, question marks, and dogs with clear invest, hold, divest guidance.

One-page BCG matrix for John Wood Group, clarifying unit roles and easing portfolio decisions for faster strategic focus.

Cash Cows

Operations & maintenance for mature assets

Recurring O&M across upstream, midstream and processing remains a dependable earner for John Wood Group, contributing about 30% of group revenue in 2024 and underpinning cash generation. Established contracts, embedded on-site teams and specialist know-how sustain steady cash flow and operating margins near 10% in 2024. Growth is modest, but high utilization and strong safety performance keep margins healthy. Optimize delivery and keep churn low — milk, don’t overfeed.

Brownfield engineering & modifications

Tie-ins, debottlenecking and life‑extension work drive steady brownfield revenue in mature basins; Wood’s scale and standardized playbooks lower unit cost and client risk. Not high-growth but defendable share with strong cash conversion—Wood reported FY2024 revenue of $6.3bn and maintained high operating cash conversion. Discipline on scope, standardization and protection of key frame agreements preserves margins and repeat work.

Integrity, reliability, and inspection services

Statutory and risk-driven inspection work remains non‑discretionary and delivers steady revenue for Wood’s inspection and integrity services, with high utilization, repeat scopes, and embedded tooling driving strong cash generation. Growth ceiling is modest, but targeted add‑ons and bundling raise yield per contract. Maintain a lean bench and strict process controls to protect margin.

Framework consulting with IOCs/NOCs

Framework consulting with IOCs/NOCs delivers predictable throughput via multi‑year (typically 3–7 year) advisory and engineering agreements, low sales friction and stable billing rates; contribution margins for E&C framework work generally run in the 20–30% range and market growth in 2024 was flat (~0–1% CAGR) for upstream services. Focus on delivery quality and incremental scope capture keeps wallet share defensible.

- Duration: 3–7 years

- Market growth 2024: ~0–1% CAGR

- Typical margins: 20–30%

- Client retention: high, >80%

- Priority: delivery quality + scope uplift

Midstream operations support & pipeline services

Midstream operations and pipeline services sit as Cash Cows for Wood: stable, regulated-like spend patterns underpin reliable volumes and FY2024 disclosures show steady midstream revenues and backlog, supporting predictable cash generation. Wood’s long-standing client relationships and delivery track record sustain pricing and contract renewals while modest innovation needs keep capital expenditure low. Focus on margin-enhancing efficiency and broader service bundles to maximize free cash flow.

- Stable volumes: regulated-like spend

- Pricing power: strong renewal rates

- Low capex: limited innovation needs

- Value drivers: efficiency and service breadth

Stable cash from recurring O&M - $6.3bn, ~30% O&M

Recurring O&M, midstream services and inspection work generate predictable cash for John Wood Group, with FY2024 revenue $6.3bn and recurring O&M ~30% of group revenue, O&M margins ~10%. Framework E&C yields 20–30% margins and client retention >80%, supporting high cash conversion. Focus: efficiency, standardization and scope uplift to preserve cash flows.

| Metric | 2024 |

|---|---|

| Group revenue | $6.3bn |

| Recurring O&M share | ~30% |

| O&M margin | ~10% |

| Framework margins | 20–30% |

| Client retention | >80% |

What You’re Viewing Is Included

John Wood Group BCG Matrix

The John Wood Group BCG Matrix you’re previewing on this page is the exact file you’ll get after purchase. No watermarks, no demo placeholders—just a fully formatted, ready-to-use strategic report tailored for clarity. Buy once and the final document is delivered straight to your inbox, editable, printable, and presentation-ready. It’s the same analysis-backed matrix shown here, crafted for decision-makers who need to act fast.

Original: $10.00

-65%$10.00

$3.50Description

Unlock Strategic Clarity

Curious where John Wood Group’s offerings sit—Stars, Cash Cows, Dogs, or Question Marks? This preview sketches the picture; the full BCG Matrix gives quadrant-by-quadrant placement, data-backed recommendations, and tactical next steps you can act on. Buy the complete report for a ready-to-use Word and Excel pack that saves hours and sharpens your investment moves. Get instant access and start reallocating smarter today.

Stars

Decarbonization consulting & CCUS programs

High-growth demand for decarbonization and CCUS—IEA says global CCUS capacity must scale roughly 6–19x by 2030—puts this squarely in the hotspot for Wood. Wood’s advisory-to-delivery span secures strong share in select regions and sectors, backed by a project pipeline targeting >200 MtCO2 by 2030. It still needs focused investment in talent, partnerships, and reference projects to lock leadership; sustained funding will turn it into a powerhouse cash engine.

Hydrogen and low-carbon fuels engineering

Hydrogen, SAF and biofuels are scaling rapidly and demand complex engineering—an explicit Wood sweet spot as low-carbon project pipelines expanded in 2024. Early wins and credibility drive momentum, though capex cycles remain lumpy and can compress returns. Active marketing, pilots and strategic alliances keep the pipeline warm and de‑risk bids. With scale, standardization and repeatable EPC execution this segment can convert to dependable, higher-margin returns.

Digital asset performance & optimization

APM, analytics and data-led operations are gaining traction across brownfield assets, with 2024 industry surveys showing roughly 70% of operators prioritizing digital optimization. Wood’s engineering domain know‑how makes digital work stickier and higher-margin, turning platform-backed APM into ongoing platform investment and client enablement. If adoption endures, these projects convert to durable annuities with strong cross-sell potential.

Integrated project management for energy transition

Large low‑carbon builds require tight PMO, assurance and risk control — high growth, higher stakes as global clean‑energy investment rose to about $1.7tn in 2024; Wood’s multi‑discipline coverage secures a visible seat at the table but mobilization and systems can consume 2–5% of project value. Nail delivery, retain share, and it compounds into category leadership.

- Growth: high demand, ~$1.7tn clean‑energy spend (2024)

- Strength: multi‑discipline presence = strategic access

- Risk: mobilization cash burn ~2–5% of capex

- Outcome: delivery drives sustained market share

Sustainable materials & circular process engineering

Clients are retooling for circularity, waste-to-value and lower‑carbon chemistries as global plastic production remains near 400 million tonnes annually (2023–24), creating niche engineering demand where Wood’s early-mover credibility in chemical recycling and solvent recovery gives leverage in select projects. Scale is uneven; prioritized case studies and replicable EPC frameworks are needed to convert pilot wins into scalable revenue. Invest now to help set standards and capture premium margins before suppliers standardize.

- tag:early-mover

- tag:case-studies

- tag:invest-now

Scale or stall: CCUS must grow 6-19x by 2030 as $1.7tn clean-energy spend fuels demand

High-growth decarbonization (IEA CCUS 6–19x by 2030) and Wood’s >200 MtCO2 by 2030 pipeline position Stars for scale; 2024 clean‑energy spend ~$1.7tn and ~70% operator digital priority drive demand. Execution risk: mobilization cash burn ~2–5% capex; invest in talent, pilots and alliances to convert to durable cash engines.

| Metric | 2024/2030 |

|---|---|

| Clean‑energy spend | $1.7tn (2024) |

| CCUS scale need | 6–19x by 2030 |

| Wood pipeline | >200 MtCO2 by 2030 |

What is included in the product

Concise BCG Matrix review of John Wood Group: stars, cash cows, question marks, and dogs with clear invest, hold, divest guidance.

One-page BCG matrix for John Wood Group, clarifying unit roles and easing portfolio decisions for faster strategic focus.

Cash Cows

Operations & maintenance for mature assets

Recurring O&M across upstream, midstream and processing remains a dependable earner for John Wood Group, contributing about 30% of group revenue in 2024 and underpinning cash generation. Established contracts, embedded on-site teams and specialist know-how sustain steady cash flow and operating margins near 10% in 2024. Growth is modest, but high utilization and strong safety performance keep margins healthy. Optimize delivery and keep churn low — milk, don’t overfeed.

Brownfield engineering & modifications

Tie-ins, debottlenecking and life‑extension work drive steady brownfield revenue in mature basins; Wood’s scale and standardized playbooks lower unit cost and client risk. Not high-growth but defendable share with strong cash conversion—Wood reported FY2024 revenue of $6.3bn and maintained high operating cash conversion. Discipline on scope, standardization and protection of key frame agreements preserves margins and repeat work.

Integrity, reliability, and inspection services

Statutory and risk-driven inspection work remains non‑discretionary and delivers steady revenue for Wood’s inspection and integrity services, with high utilization, repeat scopes, and embedded tooling driving strong cash generation. Growth ceiling is modest, but targeted add‑ons and bundling raise yield per contract. Maintain a lean bench and strict process controls to protect margin.

Framework consulting with IOCs/NOCs

Framework consulting with IOCs/NOCs delivers predictable throughput via multi‑year (typically 3–7 year) advisory and engineering agreements, low sales friction and stable billing rates; contribution margins for E&C framework work generally run in the 20–30% range and market growth in 2024 was flat (~0–1% CAGR) for upstream services. Focus on delivery quality and incremental scope capture keeps wallet share defensible.

- Duration: 3–7 years

- Market growth 2024: ~0–1% CAGR

- Typical margins: 20–30%

- Client retention: high, >80%

- Priority: delivery quality + scope uplift

Midstream operations support & pipeline services

Midstream operations and pipeline services sit as Cash Cows for Wood: stable, regulated-like spend patterns underpin reliable volumes and FY2024 disclosures show steady midstream revenues and backlog, supporting predictable cash generation. Wood’s long-standing client relationships and delivery track record sustain pricing and contract renewals while modest innovation needs keep capital expenditure low. Focus on margin-enhancing efficiency and broader service bundles to maximize free cash flow.

- Stable volumes: regulated-like spend

- Pricing power: strong renewal rates

- Low capex: limited innovation needs

- Value drivers: efficiency and service breadth

Stable cash from recurring O&M - $6.3bn, ~30% O&M

Recurring O&M, midstream services and inspection work generate predictable cash for John Wood Group, with FY2024 revenue $6.3bn and recurring O&M ~30% of group revenue, O&M margins ~10%. Framework E&C yields 20–30% margins and client retention >80%, supporting high cash conversion. Focus: efficiency, standardization and scope uplift to preserve cash flows.

| Metric | 2024 |

|---|---|

| Group revenue | $6.3bn |

| Recurring O&M share | ~30% |

| O&M margin | ~10% |

| Framework margins | 20–30% |

| Client retention | >80% |

What You’re Viewing Is Included

John Wood Group BCG Matrix

The John Wood Group BCG Matrix you’re previewing on this page is the exact file you’ll get after purchase. No watermarks, no demo placeholders—just a fully formatted, ready-to-use strategic report tailored for clarity. Buy once and the final document is delivered straight to your inbox, editable, printable, and presentation-ready. It’s the same analysis-backed matrix shown here, crafted for decision-makers who need to act fast.