Woolworths SWOT Analysis

Your Strategic Toolkit Starts Here

Woolworths stands out with market-leading grocery share, strong supply-chain capabilities and a trusted brand, but faces margin pressure and heavy domestic exposure. Growth in online grocery and sustainability initiatives offer upside while fierce retail competition and regulatory risks threaten returns. Purchase the full SWOT analysis for a detailed, editable report and strategic takeaways.

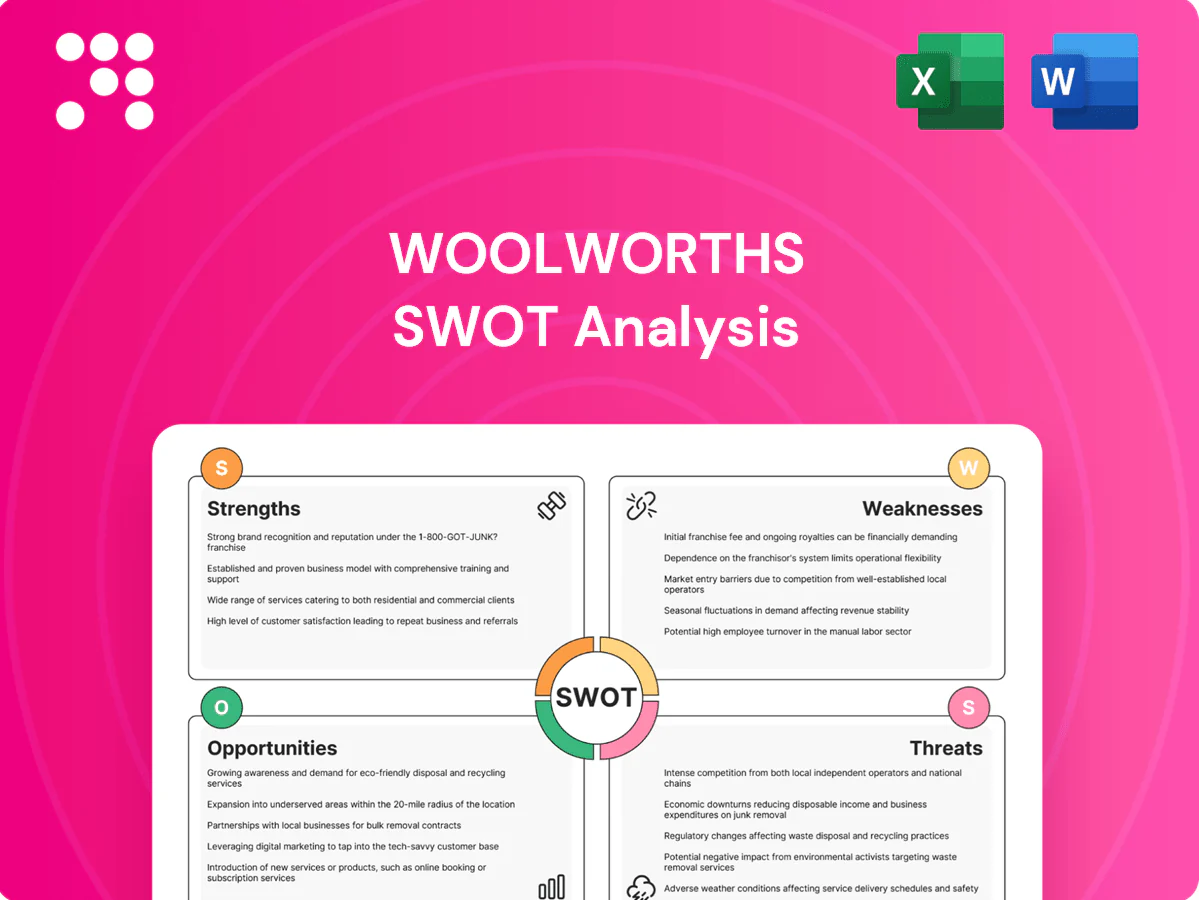

Strengths

Market leadership in ANZ groceries

Woolworths holds roughly a 32% share of the Australian supermarket market and about 33% in New Zealand, operating ~1,000 Australian stores and ~180 Countdown outlets, driving high footfall and scale efficiencies. Strong brand recognition and dense store coverage create habitual shopping, raising switching costs. Scale secures better vendor terms and promotional funding, underpinning resilient cash flows across cycles.

Extensive omnichannel and last‑mile capability

Woolworths' omnichannel reach—around 995 supermarkets plus extensive click & collect and on‑demand delivery—supported double‑digit e‑commerce growth in FY24 and strategic partnerships that extend reach. Integrated inventory visibility and flexible fulfillment increase basket size and customer stickiness. Ongoing investment in automation and micro‑fulfillment improves cost‑to‑serve and reinforces a moat versus digital‑only rivals.

Loyalty, data, and retail media assets

Everyday Rewards exceeds 16 million members (FY24), feeding Woolworths’ digital ecosystem with rich first-party data. Personalization and targeted offers lift basket spend and margins while retail media monetisation opens a new high-margin revenue stream. Customer insights directly inform pricing, store space and assortment decisions to optimise sales per square metre. These assets reinforce a virtuous loop of engagement and profitability.

Diversified retail portfolio

Do you mean Woolworths Group (Australia, ASX:WOW) or Woolworths Holdings (South Africa)?

Strong supply chain and vendor relationships

Woolworths' national distribution network and cold-chain expertise support high availability across 1,000+ stores and an estimated ~35% Australian grocery market share, with sophisticated replenishment systems that drive freshness. Longstanding supplier partnerships enable joint planning and innovation, while operational excellence lowers waste and strengthens reliability, boosting brand trust and repeat purchases.

- 1,000+ stores

- ~35% market share

- Cold-chain & replenishment

- Supplier joint planning

Market-leading supermarket: ~32% AU share, 16m+ rewards, rapid e-commerce growth

Woolworths Group (ASX:WOW) holds ~32% of the Australian supermarket market, operating ~995 supermarkets and ~180 Countdown stores in NZ, delivering scale-driven margins and vendor leverage. Everyday Rewards exceeded 16 million members in FY24, fuelling personalization and retail media monetisation. Omnichannel operations posted double‑digit e‑commerce growth in FY24, with strong cold‑chain and replenishment systems supporting freshness and availability.

| Metric | Value |

|---|---|

| AU market share | ~32% |

| Stores (AU) | ~995 |

| Rewards members (FY24) | 16m+ |

| E‑commerce (FY24) | Double‑digit growth |

What is included in the product

Delivers a strategic overview of Woolworths’s internal and external business factors, outlining its strengths, weaknesses, opportunities, and threats to assess competitive position and future risks.

Provides a concise Woolworths SWOT matrix for fast strategic alignment and decision-making, enabling executives to quickly visualize strengths, weaknesses, opportunities and threats.

Weaknesses

High exposure to Australia and NZ

High concentration in Australia and New Zealand leaves Woolworths exposed to local economic and regulatory shifts, with over 90% of FY24 group sales generated in those markets. Limited international diversification constrains growth optionality and makes the group reliant on ANZ consumer trends. A downturn in consumer sentiment or disposable income can quickly pressure volumes and product mix. Regional disruptions—extreme weather, supply-chain shocks—can ripple rapidly through operations.

Structural margin pressure in groceries

Supermarket categories are low-margin and highly promotional, with grocery gross margins in Australia typically in the low single digits (~4%); price investment to defend share (Woolworths increased promotional activity in 2024) compresses gross margin. Rising labor and logistics costs in 2024–25 have strained operating leverage, forcing Woolworths to target continuous efficiency gains and productivity programs to sustain profitability.

Legacy reputational and compliance risks

Prior wage underpayment and supplier controversies (remediation provisions around A$300m reported in remediation rounds) have heightened regulatory and media scrutiny, raising legacy reputational and compliance risks. Remediation costs and ongoing monitoring add material overhead to operating expenses. Rebuilding trust demands sustained transparency and rigorous compliance frameworks. Any recurrence could trigger fines, class actions and further brand damage.

Complexity from multi-banner operations

Managing multiple banners and channels (supermarkets, liquor, general merchandise) creates operational complexity for Woolworths, with assortment, pricing and promo alignment consuming significant resources and contributing to higher costs; Woolworths served over 10 million customers weekly in 2024, amplifying coordination needs.

IT integration and data governance gaps—noted in past transformation projects—raise execution risk during change programs, increasing chances of shelf gaps, pricing errors and margin leakage.

- formats: multi-banner/channel coordination

- costs: resource-heavy assortment & promo alignment

- IT: integration & data governance risks

- execution: elevated risk in transformations

Large fixed cost and lease commitments

Woolworths' extensive store network—around 1,000 supermarkets plus convenience and fuel sites—creates substantial multi‑year lease liabilities and ongoing maintenance capex. Negative operating leverage emerges when traffic or basket sizes fall, compressing margins. Portfolio optimisation and closures carry heavy exit costs and lower flexibility versus asset‑light rivals.

- Lease scale: ~1,000 sites

- High maintenance capex

- Negative operating leverage risk

- Lower flexibility than asset‑light peers

ANZ-heavy grocer: >90% sales, ~4% grocery margin, A$300m remediation, ~1,000 stores risk

High ANZ concentration (>90% of FY24 group sales) limits growth optionality and raises exposure to local downturns. Low-margin supermarket mix (grocery gross margin ~4% in Australia) and increased 2024–25 labor/logistics costs compress profitability. Legacy remediation (~A$300m) and ~1,000-store lease scale raise compliance, capex and operating‑leverage risks.

| Metric | Value |

|---|---|

| ANZ sales share (FY24) | >90% |

| Grocery gross margin (AU) | ~4% |

| Remediation provisions | ~A$300m |

| Store count | ~1,000 |

Preview the Actual Deliverable

Woolworths SWOT Analysis

This is the actual Woolworths SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full SWOT report you'll get; purchase unlocks the entire in-depth, editable version. Buy now to download the complete, structured analysis ready for use.

Your Strategic Toolkit Starts Here

Woolworths stands out with market-leading grocery share, strong supply-chain capabilities and a trusted brand, but faces margin pressure and heavy domestic exposure. Growth in online grocery and sustainability initiatives offer upside while fierce retail competition and regulatory risks threaten returns. Purchase the full SWOT analysis for a detailed, editable report and strategic takeaways.

Strengths

Market leadership in ANZ groceries

Woolworths holds roughly a 32% share of the Australian supermarket market and about 33% in New Zealand, operating ~1,000 Australian stores and ~180 Countdown outlets, driving high footfall and scale efficiencies. Strong brand recognition and dense store coverage create habitual shopping, raising switching costs. Scale secures better vendor terms and promotional funding, underpinning resilient cash flows across cycles.

Extensive omnichannel and last‑mile capability

Woolworths' omnichannel reach—around 995 supermarkets plus extensive click & collect and on‑demand delivery—supported double‑digit e‑commerce growth in FY24 and strategic partnerships that extend reach. Integrated inventory visibility and flexible fulfillment increase basket size and customer stickiness. Ongoing investment in automation and micro‑fulfillment improves cost‑to‑serve and reinforces a moat versus digital‑only rivals.

Loyalty, data, and retail media assets

Everyday Rewards exceeds 16 million members (FY24), feeding Woolworths’ digital ecosystem with rich first-party data. Personalization and targeted offers lift basket spend and margins while retail media monetisation opens a new high-margin revenue stream. Customer insights directly inform pricing, store space and assortment decisions to optimise sales per square metre. These assets reinforce a virtuous loop of engagement and profitability.

Diversified retail portfolio

Do you mean Woolworths Group (Australia, ASX:WOW) or Woolworths Holdings (South Africa)?

Strong supply chain and vendor relationships

Woolworths' national distribution network and cold-chain expertise support high availability across 1,000+ stores and an estimated ~35% Australian grocery market share, with sophisticated replenishment systems that drive freshness. Longstanding supplier partnerships enable joint planning and innovation, while operational excellence lowers waste and strengthens reliability, boosting brand trust and repeat purchases.

- 1,000+ stores

- ~35% market share

- Cold-chain & replenishment

- Supplier joint planning

Market-leading supermarket: ~32% AU share, 16m+ rewards, rapid e-commerce growth

Woolworths Group (ASX:WOW) holds ~32% of the Australian supermarket market, operating ~995 supermarkets and ~180 Countdown stores in NZ, delivering scale-driven margins and vendor leverage. Everyday Rewards exceeded 16 million members in FY24, fuelling personalization and retail media monetisation. Omnichannel operations posted double‑digit e‑commerce growth in FY24, with strong cold‑chain and replenishment systems supporting freshness and availability.

| Metric | Value |

|---|---|

| AU market share | ~32% |

| Stores (AU) | ~995 |

| Rewards members (FY24) | 16m+ |

| E‑commerce (FY24) | Double‑digit growth |

What is included in the product

Delivers a strategic overview of Woolworths’s internal and external business factors, outlining its strengths, weaknesses, opportunities, and threats to assess competitive position and future risks.

Provides a concise Woolworths SWOT matrix for fast strategic alignment and decision-making, enabling executives to quickly visualize strengths, weaknesses, opportunities and threats.

Weaknesses

High exposure to Australia and NZ

High concentration in Australia and New Zealand leaves Woolworths exposed to local economic and regulatory shifts, with over 90% of FY24 group sales generated in those markets. Limited international diversification constrains growth optionality and makes the group reliant on ANZ consumer trends. A downturn in consumer sentiment or disposable income can quickly pressure volumes and product mix. Regional disruptions—extreme weather, supply-chain shocks—can ripple rapidly through operations.

Structural margin pressure in groceries

Supermarket categories are low-margin and highly promotional, with grocery gross margins in Australia typically in the low single digits (~4%); price investment to defend share (Woolworths increased promotional activity in 2024) compresses gross margin. Rising labor and logistics costs in 2024–25 have strained operating leverage, forcing Woolworths to target continuous efficiency gains and productivity programs to sustain profitability.

Legacy reputational and compliance risks

Prior wage underpayment and supplier controversies (remediation provisions around A$300m reported in remediation rounds) have heightened regulatory and media scrutiny, raising legacy reputational and compliance risks. Remediation costs and ongoing monitoring add material overhead to operating expenses. Rebuilding trust demands sustained transparency and rigorous compliance frameworks. Any recurrence could trigger fines, class actions and further brand damage.

Complexity from multi-banner operations

Managing multiple banners and channels (supermarkets, liquor, general merchandise) creates operational complexity for Woolworths, with assortment, pricing and promo alignment consuming significant resources and contributing to higher costs; Woolworths served over 10 million customers weekly in 2024, amplifying coordination needs.

IT integration and data governance gaps—noted in past transformation projects—raise execution risk during change programs, increasing chances of shelf gaps, pricing errors and margin leakage.

- formats: multi-banner/channel coordination

- costs: resource-heavy assortment & promo alignment

- IT: integration & data governance risks

- execution: elevated risk in transformations

Large fixed cost and lease commitments

Woolworths' extensive store network—around 1,000 supermarkets plus convenience and fuel sites—creates substantial multi‑year lease liabilities and ongoing maintenance capex. Negative operating leverage emerges when traffic or basket sizes fall, compressing margins. Portfolio optimisation and closures carry heavy exit costs and lower flexibility versus asset‑light rivals.

- Lease scale: ~1,000 sites

- High maintenance capex

- Negative operating leverage risk

- Lower flexibility than asset‑light peers

ANZ-heavy grocer: >90% sales, ~4% grocery margin, A$300m remediation, ~1,000 stores risk

High ANZ concentration (>90% of FY24 group sales) limits growth optionality and raises exposure to local downturns. Low-margin supermarket mix (grocery gross margin ~4% in Australia) and increased 2024–25 labor/logistics costs compress profitability. Legacy remediation (~A$300m) and ~1,000-store lease scale raise compliance, capex and operating‑leverage risks.

| Metric | Value |

|---|---|

| ANZ sales share (FY24) | >90% |

| Grocery gross margin (AU) | ~4% |

| Remediation provisions | ~A$300m |

| Store count | ~1,000 |

Preview the Actual Deliverable

Woolworths SWOT Analysis

This is the actual Woolworths SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full SWOT report you'll get; purchase unlocks the entire in-depth, editable version. Buy now to download the complete, structured analysis ready for use.

Description

Your Strategic Toolkit Starts Here

Woolworths stands out with market-leading grocery share, strong supply-chain capabilities and a trusted brand, but faces margin pressure and heavy domestic exposure. Growth in online grocery and sustainability initiatives offer upside while fierce retail competition and regulatory risks threaten returns. Purchase the full SWOT analysis for a detailed, editable report and strategic takeaways.

Strengths

Market leadership in ANZ groceries

Woolworths holds roughly a 32% share of the Australian supermarket market and about 33% in New Zealand, operating ~1,000 Australian stores and ~180 Countdown outlets, driving high footfall and scale efficiencies. Strong brand recognition and dense store coverage create habitual shopping, raising switching costs. Scale secures better vendor terms and promotional funding, underpinning resilient cash flows across cycles.

Extensive omnichannel and last‑mile capability

Woolworths' omnichannel reach—around 995 supermarkets plus extensive click & collect and on‑demand delivery—supported double‑digit e‑commerce growth in FY24 and strategic partnerships that extend reach. Integrated inventory visibility and flexible fulfillment increase basket size and customer stickiness. Ongoing investment in automation and micro‑fulfillment improves cost‑to‑serve and reinforces a moat versus digital‑only rivals.

Loyalty, data, and retail media assets

Everyday Rewards exceeds 16 million members (FY24), feeding Woolworths’ digital ecosystem with rich first-party data. Personalization and targeted offers lift basket spend and margins while retail media monetisation opens a new high-margin revenue stream. Customer insights directly inform pricing, store space and assortment decisions to optimise sales per square metre. These assets reinforce a virtuous loop of engagement and profitability.

Diversified retail portfolio

Do you mean Woolworths Group (Australia, ASX:WOW) or Woolworths Holdings (South Africa)?

Strong supply chain and vendor relationships

Woolworths' national distribution network and cold-chain expertise support high availability across 1,000+ stores and an estimated ~35% Australian grocery market share, with sophisticated replenishment systems that drive freshness. Longstanding supplier partnerships enable joint planning and innovation, while operational excellence lowers waste and strengthens reliability, boosting brand trust and repeat purchases.

- 1,000+ stores

- ~35% market share

- Cold-chain & replenishment

- Supplier joint planning

Market-leading supermarket: ~32% AU share, 16m+ rewards, rapid e-commerce growth

Woolworths Group (ASX:WOW) holds ~32% of the Australian supermarket market, operating ~995 supermarkets and ~180 Countdown stores in NZ, delivering scale-driven margins and vendor leverage. Everyday Rewards exceeded 16 million members in FY24, fuelling personalization and retail media monetisation. Omnichannel operations posted double‑digit e‑commerce growth in FY24, with strong cold‑chain and replenishment systems supporting freshness and availability.

| Metric | Value |

|---|---|

| AU market share | ~32% |

| Stores (AU) | ~995 |

| Rewards members (FY24) | 16m+ |

| E‑commerce (FY24) | Double‑digit growth |

What is included in the product

Delivers a strategic overview of Woolworths’s internal and external business factors, outlining its strengths, weaknesses, opportunities, and threats to assess competitive position and future risks.

Provides a concise Woolworths SWOT matrix for fast strategic alignment and decision-making, enabling executives to quickly visualize strengths, weaknesses, opportunities and threats.

Weaknesses

High exposure to Australia and NZ

High concentration in Australia and New Zealand leaves Woolworths exposed to local economic and regulatory shifts, with over 90% of FY24 group sales generated in those markets. Limited international diversification constrains growth optionality and makes the group reliant on ANZ consumer trends. A downturn in consumer sentiment or disposable income can quickly pressure volumes and product mix. Regional disruptions—extreme weather, supply-chain shocks—can ripple rapidly through operations.

Structural margin pressure in groceries

Supermarket categories are low-margin and highly promotional, with grocery gross margins in Australia typically in the low single digits (~4%); price investment to defend share (Woolworths increased promotional activity in 2024) compresses gross margin. Rising labor and logistics costs in 2024–25 have strained operating leverage, forcing Woolworths to target continuous efficiency gains and productivity programs to sustain profitability.

Legacy reputational and compliance risks

Prior wage underpayment and supplier controversies (remediation provisions around A$300m reported in remediation rounds) have heightened regulatory and media scrutiny, raising legacy reputational and compliance risks. Remediation costs and ongoing monitoring add material overhead to operating expenses. Rebuilding trust demands sustained transparency and rigorous compliance frameworks. Any recurrence could trigger fines, class actions and further brand damage.

Complexity from multi-banner operations

Managing multiple banners and channels (supermarkets, liquor, general merchandise) creates operational complexity for Woolworths, with assortment, pricing and promo alignment consuming significant resources and contributing to higher costs; Woolworths served over 10 million customers weekly in 2024, amplifying coordination needs.

IT integration and data governance gaps—noted in past transformation projects—raise execution risk during change programs, increasing chances of shelf gaps, pricing errors and margin leakage.

- formats: multi-banner/channel coordination

- costs: resource-heavy assortment & promo alignment

- IT: integration & data governance risks

- execution: elevated risk in transformations

Large fixed cost and lease commitments

Woolworths' extensive store network—around 1,000 supermarkets plus convenience and fuel sites—creates substantial multi‑year lease liabilities and ongoing maintenance capex. Negative operating leverage emerges when traffic or basket sizes fall, compressing margins. Portfolio optimisation and closures carry heavy exit costs and lower flexibility versus asset‑light rivals.

- Lease scale: ~1,000 sites

- High maintenance capex

- Negative operating leverage risk

- Lower flexibility than asset‑light peers

ANZ-heavy grocer: >90% sales, ~4% grocery margin, A$300m remediation, ~1,000 stores risk

High ANZ concentration (>90% of FY24 group sales) limits growth optionality and raises exposure to local downturns. Low-margin supermarket mix (grocery gross margin ~4% in Australia) and increased 2024–25 labor/logistics costs compress profitability. Legacy remediation (~A$300m) and ~1,000-store lease scale raise compliance, capex and operating‑leverage risks.

| Metric | Value |

|---|---|

| ANZ sales share (FY24) | >90% |

| Grocery gross margin (AU) | ~4% |

| Remediation provisions | ~A$300m |

| Store count | ~1,000 |

Preview the Actual Deliverable

Woolworths SWOT Analysis

This is the actual Woolworths SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full SWOT report you'll get; purchase unlocks the entire in-depth, editable version. Buy now to download the complete, structured analysis ready for use.