Woolworths SWOT Analysis

Elevate Your Analysis with the Complete SWOT Report

Woolworths' SWOT highlights market leadership, strong supply-chain and grocery scale, plus digital growth, against margin pressure, regulatory risk and fierce competition; strategic gaps include private-label expansion and sustainability execution. Discover the full, editable SWOT—detailed analysis, financial context and Word+Excel deliverables—to plan, pitch or invest with confidence; purchase the complete report now.

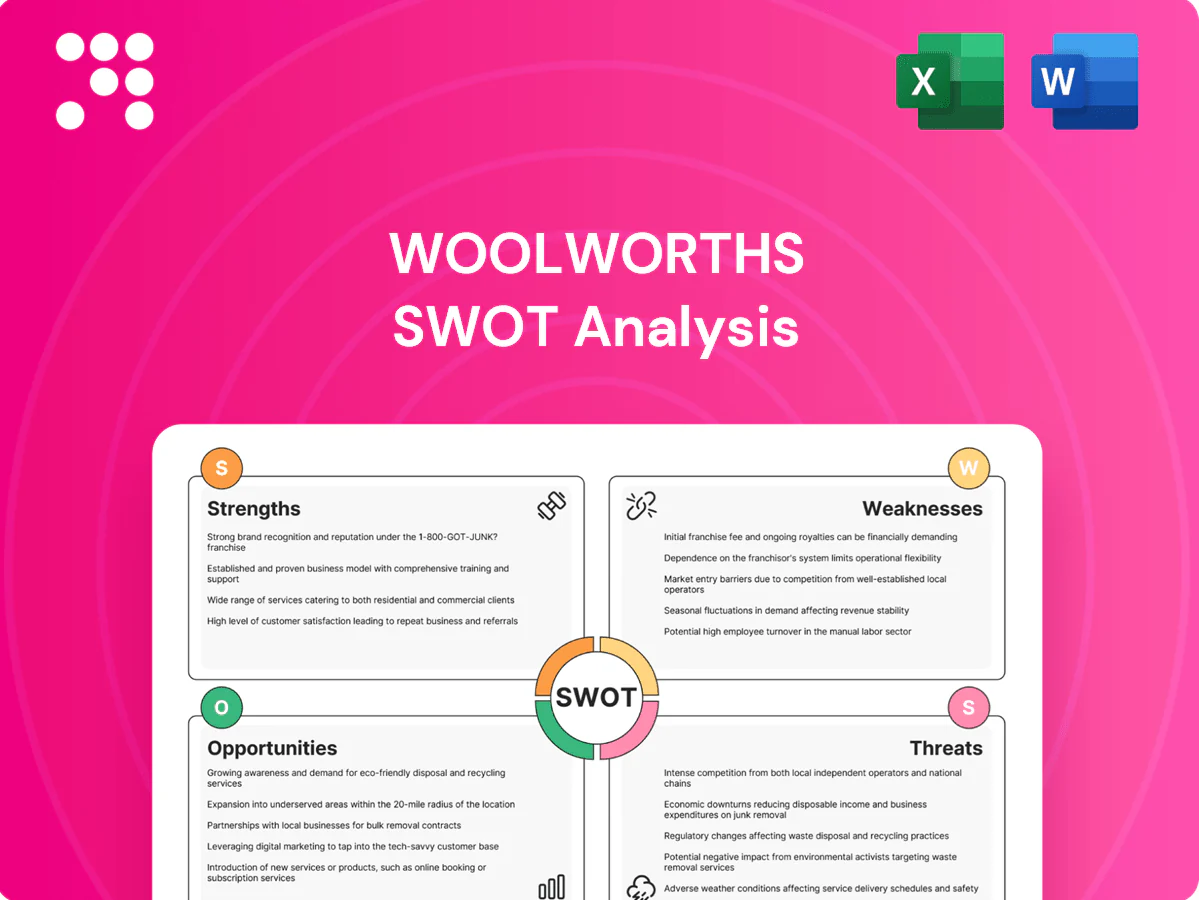

Strengths

Diversified premium retail portfolio

WHL spans food, fashion, beauty and homeware across South Africa, Australia and New Zealand through Woolworths SA, David Jones and the Country Road Group, providing multi-category exposure. Multi-brand reach balances category cycles and reduces single-category dependency. Premium positioning underpins pricing power and brand equity across its diversified retail portfolio.

Strong private label and quality reputation

Woolworths Food and own-brand apparel are consistently rated for quality, freshness and design, reinforcing brand equity in FY24. Its private-label range drives margin advantage and differentiation versus mass competitors. Consistent standards foster trust and repeat purchase, while vertical control improves supply-chain responsiveness and agility.

Omnichannel and loyalty capabilities

Integrated stores, digital platforms and click-and-collect boost convenience and average basket size for Woolworths, supporting its ~33% Australian grocery market share. Everyday Rewards, with about 15 million members, generates transaction-level data used for personalization and promotions. Cross-banner insights across supermarkets, BIG W and BWS enable precise targeted marketing. These capabilities drive higher customer lifetime value and repeat frequency.

Vertical sourcing and supply chain discipline

Vertical sourcing and tight supply-chain discipline give Woolworths—operator of around 1,000 Australian supermarkets—curated assortments and strong vendor partnerships that reduce complexity, improve inventory turns and limit shrink, boosting margins. Rigorous traceability and ethical sourcing programs strengthen brand trust, while supply-chain investments accelerate fresh and fashion speed-to-market.

- vendor-relationships

- inventory-turns

- shrink-control

- traceability-ethics

- speed-to-market

Financial services adjacency

Woolworths leverages financial services via Everyday Rewards and Woolworths Money to deepen engagement; Everyday Rewards had about 16.7 million members in 2024, boosting targeted promotions and spend. Credit capabilities and co-branded offers (cards, BNPL partnerships) create fee and interest revenue streams while providing rich customer data for personalization. Risk-managed lending through partnerships limits capital intensity while enhancing returns.

- Everyday Rewards ~16.7M members (2024)

- Credit/co-branding drives fee + interest income

- Data enables personalized offers and higher basket spend

- Partnership lending reduces capital needs, improves ROE

Multi-category retailer with 16.7M members and ~33% grocery share

Woolworths combines multi-category reach (food, fashion, beauty, home) across Australia, NZ and SA with premium private labels driving margin and trust; Everyday Rewards had ~16.7M members in 2024 supporting personalization and higher basket spend. Vertical sourcing and ~1,000 Australian supermarkets enable strong inventory turns, shrink control and speed-to-market, underpinning pricing power and steady margins.

| Metric | 2024 |

|---|---|

| Everyday Rewards members | 16.7M |

| Australian grocery share | ~33% |

| Australian supermarkets | ~1,000 |

What is included in the product

Examines strengths, weaknesses, opportunities, and threats shaping Woolworths’ competitive position and future growth, highlighting internal capabilities, operational gaps, and external market risks.

Provides a concise Woolworths SWOT matrix for fast strategic alignment across retail operations, ideal for executives and teams needing a snapshot to quickly resolve decision-making bottlenecks and guide priority actions.

Weaknesses

Exposure to South African macro volatility

Consumer income pressure, energy disruptions and logistics challenges in South Africa impair Woolworths operations and margin recovery. Load-shedding reduces store uptime and threatens cold‑chain integrity for fresh and frozen goods. Elevated unemployment at about 33% (Stats SA 2024) constrains discretionary spend and amplifies earnings volatility for the group.

Australian department store complexity

Australian department store formats face structural pressure from online and specialty players, compressing margins and footfall; David Jones needs continual range, space and cost optimisation to remain competitive. The required turnaround demands significant capital allocation and sustained management focus, diverting resources from core supermarket growth. Execution risk is high and can dilute group returns if improvements lag or investment overruns occur.

Premium price perception

Price gaps versus value retailers (ALDI ~10% market share vs Woolworths ~33% in Australia, 2024) drive downtrading in tougher cycles, hitting volumes in staples and basics. Sensitivity is acute for everyday grocery items where customers trade down first. Maintaining perceived value demands relentless quality control and promotional discipline, and margin can be materially pressured if sustained price investment is required.

Cross-border management complexity

Operating across South Africa, Australia and New Zealand exposes Woolworths to regulatory and cultural complexity across markets with a combined population of about 92 million (2024 est.), which can slow strategy alignment and systems integration and create duplicated overheads that raise cost-to-serve. Cross-banner governance frictions and multi-jurisdictional compliance can reduce decision speed and responsiveness.

- Multi-country footprint: SA, AU, NZ (~92m people)

- Systems lag: integration delays hamper rollout

- Higher cost-to-serve: duplicated overheads

- Slower decisions: governance across banners/geographies

Currency translation and input cost risk

Currency translation and input cost risk: volatility between the ZAR and AUD raises sourcing costs for Woolworths and can compress reported earnings when translated into group currency; imported textiles and food inputs remain particularly sensitive to FX swings. Hedging programs mitigate timing and price risk but do not eliminate exposure to sudden moves. Passing costs to consumers via price increases risks dampening demand in price-sensitive segments.

- FX-sensitive imports: textiles, food inputs

- Hedging mitigates but not eliminates risk

- Translation impacts reported earnings

- Price hikes may face consumer resistance

SA 33% unemployment, load-shedding; AU capex drag; 92m footprint FX risk

High SA unemployment (33% Stats SA 2024) and load‑shedding disrupt demand and cold‑chain reliability; AU department store drag requires heavy capex and risks execution; price gap to value chains (ALDI ~10% vs Woolworths ~33% AU, 2024) drives downtrading; FX volatility across a ~92m population footprint raises input and translation risk.

| Weakness | Key metric (2024) |

|---|---|

| SA demand/energy | Unemployment 33% / frequent load‑shedding |

| AU department store drag | High capex & execution risk |

| Value retailer pressure | ALDI ~10% vs Wools ~33% AU |

| Cross‑border FX | Footprint ~92m (SA, AU, NZ) |

Same Document Delivered

Woolworths SWOT Analysis

This is the actual Woolworths SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality and structured insights. The preview below is taken directly from the full report you'll get; buying unlocks the complete, editable version with detailed strengths, weaknesses, opportunities and threats. Purchase to download the entire file immediately after checkout.

Elevate Your Analysis with the Complete SWOT Report

Woolworths' SWOT highlights market leadership, strong supply-chain and grocery scale, plus digital growth, against margin pressure, regulatory risk and fierce competition; strategic gaps include private-label expansion and sustainability execution. Discover the full, editable SWOT—detailed analysis, financial context and Word+Excel deliverables—to plan, pitch or invest with confidence; purchase the complete report now.

Strengths

Diversified premium retail portfolio

WHL spans food, fashion, beauty and homeware across South Africa, Australia and New Zealand through Woolworths SA, David Jones and the Country Road Group, providing multi-category exposure. Multi-brand reach balances category cycles and reduces single-category dependency. Premium positioning underpins pricing power and brand equity across its diversified retail portfolio.

Strong private label and quality reputation

Woolworths Food and own-brand apparel are consistently rated for quality, freshness and design, reinforcing brand equity in FY24. Its private-label range drives margin advantage and differentiation versus mass competitors. Consistent standards foster trust and repeat purchase, while vertical control improves supply-chain responsiveness and agility.

Omnichannel and loyalty capabilities

Integrated stores, digital platforms and click-and-collect boost convenience and average basket size for Woolworths, supporting its ~33% Australian grocery market share. Everyday Rewards, with about 15 million members, generates transaction-level data used for personalization and promotions. Cross-banner insights across supermarkets, BIG W and BWS enable precise targeted marketing. These capabilities drive higher customer lifetime value and repeat frequency.

Vertical sourcing and supply chain discipline

Vertical sourcing and tight supply-chain discipline give Woolworths—operator of around 1,000 Australian supermarkets—curated assortments and strong vendor partnerships that reduce complexity, improve inventory turns and limit shrink, boosting margins. Rigorous traceability and ethical sourcing programs strengthen brand trust, while supply-chain investments accelerate fresh and fashion speed-to-market.

- vendor-relationships

- inventory-turns

- shrink-control

- traceability-ethics

- speed-to-market

Financial services adjacency

Woolworths leverages financial services via Everyday Rewards and Woolworths Money to deepen engagement; Everyday Rewards had about 16.7 million members in 2024, boosting targeted promotions and spend. Credit capabilities and co-branded offers (cards, BNPL partnerships) create fee and interest revenue streams while providing rich customer data for personalization. Risk-managed lending through partnerships limits capital intensity while enhancing returns.

- Everyday Rewards ~16.7M members (2024)

- Credit/co-branding drives fee + interest income

- Data enables personalized offers and higher basket spend

- Partnership lending reduces capital needs, improves ROE

Multi-category retailer with 16.7M members and ~33% grocery share

Woolworths combines multi-category reach (food, fashion, beauty, home) across Australia, NZ and SA with premium private labels driving margin and trust; Everyday Rewards had ~16.7M members in 2024 supporting personalization and higher basket spend. Vertical sourcing and ~1,000 Australian supermarkets enable strong inventory turns, shrink control and speed-to-market, underpinning pricing power and steady margins.

| Metric | 2024 |

|---|---|

| Everyday Rewards members | 16.7M |

| Australian grocery share | ~33% |

| Australian supermarkets | ~1,000 |

What is included in the product

Examines strengths, weaknesses, opportunities, and threats shaping Woolworths’ competitive position and future growth, highlighting internal capabilities, operational gaps, and external market risks.

Provides a concise Woolworths SWOT matrix for fast strategic alignment across retail operations, ideal for executives and teams needing a snapshot to quickly resolve decision-making bottlenecks and guide priority actions.

Weaknesses

Exposure to South African macro volatility

Consumer income pressure, energy disruptions and logistics challenges in South Africa impair Woolworths operations and margin recovery. Load-shedding reduces store uptime and threatens cold‑chain integrity for fresh and frozen goods. Elevated unemployment at about 33% (Stats SA 2024) constrains discretionary spend and amplifies earnings volatility for the group.

Australian department store complexity

Australian department store formats face structural pressure from online and specialty players, compressing margins and footfall; David Jones needs continual range, space and cost optimisation to remain competitive. The required turnaround demands significant capital allocation and sustained management focus, diverting resources from core supermarket growth. Execution risk is high and can dilute group returns if improvements lag or investment overruns occur.

Premium price perception

Price gaps versus value retailers (ALDI ~10% market share vs Woolworths ~33% in Australia, 2024) drive downtrading in tougher cycles, hitting volumes in staples and basics. Sensitivity is acute for everyday grocery items where customers trade down first. Maintaining perceived value demands relentless quality control and promotional discipline, and margin can be materially pressured if sustained price investment is required.

Cross-border management complexity

Operating across South Africa, Australia and New Zealand exposes Woolworths to regulatory and cultural complexity across markets with a combined population of about 92 million (2024 est.), which can slow strategy alignment and systems integration and create duplicated overheads that raise cost-to-serve. Cross-banner governance frictions and multi-jurisdictional compliance can reduce decision speed and responsiveness.

- Multi-country footprint: SA, AU, NZ (~92m people)

- Systems lag: integration delays hamper rollout

- Higher cost-to-serve: duplicated overheads

- Slower decisions: governance across banners/geographies

Currency translation and input cost risk

Currency translation and input cost risk: volatility between the ZAR and AUD raises sourcing costs for Woolworths and can compress reported earnings when translated into group currency; imported textiles and food inputs remain particularly sensitive to FX swings. Hedging programs mitigate timing and price risk but do not eliminate exposure to sudden moves. Passing costs to consumers via price increases risks dampening demand in price-sensitive segments.

- FX-sensitive imports: textiles, food inputs

- Hedging mitigates but not eliminates risk

- Translation impacts reported earnings

- Price hikes may face consumer resistance

SA 33% unemployment, load-shedding; AU capex drag; 92m footprint FX risk

High SA unemployment (33% Stats SA 2024) and load‑shedding disrupt demand and cold‑chain reliability; AU department store drag requires heavy capex and risks execution; price gap to value chains (ALDI ~10% vs Woolworths ~33% AU, 2024) drives downtrading; FX volatility across a ~92m population footprint raises input and translation risk.

| Weakness | Key metric (2024) |

|---|---|

| SA demand/energy | Unemployment 33% / frequent load‑shedding |

| AU department store drag | High capex & execution risk |

| Value retailer pressure | ALDI ~10% vs Wools ~33% AU |

| Cross‑border FX | Footprint ~92m (SA, AU, NZ) |

Same Document Delivered

Woolworths SWOT Analysis

This is the actual Woolworths SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality and structured insights. The preview below is taken directly from the full report you'll get; buying unlocks the complete, editable version with detailed strengths, weaknesses, opportunities and threats. Purchase to download the entire file immediately after checkout.

Original: $10.00

-65%$10.00

$3.50Description

Elevate Your Analysis with the Complete SWOT Report

Woolworths' SWOT highlights market leadership, strong supply-chain and grocery scale, plus digital growth, against margin pressure, regulatory risk and fierce competition; strategic gaps include private-label expansion and sustainability execution. Discover the full, editable SWOT—detailed analysis, financial context and Word+Excel deliverables—to plan, pitch or invest with confidence; purchase the complete report now.

Strengths

Diversified premium retail portfolio

WHL spans food, fashion, beauty and homeware across South Africa, Australia and New Zealand through Woolworths SA, David Jones and the Country Road Group, providing multi-category exposure. Multi-brand reach balances category cycles and reduces single-category dependency. Premium positioning underpins pricing power and brand equity across its diversified retail portfolio.

Strong private label and quality reputation

Woolworths Food and own-brand apparel are consistently rated for quality, freshness and design, reinforcing brand equity in FY24. Its private-label range drives margin advantage and differentiation versus mass competitors. Consistent standards foster trust and repeat purchase, while vertical control improves supply-chain responsiveness and agility.

Omnichannel and loyalty capabilities

Integrated stores, digital platforms and click-and-collect boost convenience and average basket size for Woolworths, supporting its ~33% Australian grocery market share. Everyday Rewards, with about 15 million members, generates transaction-level data used for personalization and promotions. Cross-banner insights across supermarkets, BIG W and BWS enable precise targeted marketing. These capabilities drive higher customer lifetime value and repeat frequency.

Vertical sourcing and supply chain discipline

Vertical sourcing and tight supply-chain discipline give Woolworths—operator of around 1,000 Australian supermarkets—curated assortments and strong vendor partnerships that reduce complexity, improve inventory turns and limit shrink, boosting margins. Rigorous traceability and ethical sourcing programs strengthen brand trust, while supply-chain investments accelerate fresh and fashion speed-to-market.

- vendor-relationships

- inventory-turns

- shrink-control

- traceability-ethics

- speed-to-market

Financial services adjacency

Woolworths leverages financial services via Everyday Rewards and Woolworths Money to deepen engagement; Everyday Rewards had about 16.7 million members in 2024, boosting targeted promotions and spend. Credit capabilities and co-branded offers (cards, BNPL partnerships) create fee and interest revenue streams while providing rich customer data for personalization. Risk-managed lending through partnerships limits capital intensity while enhancing returns.

- Everyday Rewards ~16.7M members (2024)

- Credit/co-branding drives fee + interest income

- Data enables personalized offers and higher basket spend

- Partnership lending reduces capital needs, improves ROE

Multi-category retailer with 16.7M members and ~33% grocery share

Woolworths combines multi-category reach (food, fashion, beauty, home) across Australia, NZ and SA with premium private labels driving margin and trust; Everyday Rewards had ~16.7M members in 2024 supporting personalization and higher basket spend. Vertical sourcing and ~1,000 Australian supermarkets enable strong inventory turns, shrink control and speed-to-market, underpinning pricing power and steady margins.

| Metric | 2024 |

|---|---|

| Everyday Rewards members | 16.7M |

| Australian grocery share | ~33% |

| Australian supermarkets | ~1,000 |

What is included in the product

Examines strengths, weaknesses, opportunities, and threats shaping Woolworths’ competitive position and future growth, highlighting internal capabilities, operational gaps, and external market risks.

Provides a concise Woolworths SWOT matrix for fast strategic alignment across retail operations, ideal for executives and teams needing a snapshot to quickly resolve decision-making bottlenecks and guide priority actions.

Weaknesses

Exposure to South African macro volatility

Consumer income pressure, energy disruptions and logistics challenges in South Africa impair Woolworths operations and margin recovery. Load-shedding reduces store uptime and threatens cold‑chain integrity for fresh and frozen goods. Elevated unemployment at about 33% (Stats SA 2024) constrains discretionary spend and amplifies earnings volatility for the group.

Australian department store complexity

Australian department store formats face structural pressure from online and specialty players, compressing margins and footfall; David Jones needs continual range, space and cost optimisation to remain competitive. The required turnaround demands significant capital allocation and sustained management focus, diverting resources from core supermarket growth. Execution risk is high and can dilute group returns if improvements lag or investment overruns occur.

Premium price perception

Price gaps versus value retailers (ALDI ~10% market share vs Woolworths ~33% in Australia, 2024) drive downtrading in tougher cycles, hitting volumes in staples and basics. Sensitivity is acute for everyday grocery items where customers trade down first. Maintaining perceived value demands relentless quality control and promotional discipline, and margin can be materially pressured if sustained price investment is required.

Cross-border management complexity

Operating across South Africa, Australia and New Zealand exposes Woolworths to regulatory and cultural complexity across markets with a combined population of about 92 million (2024 est.), which can slow strategy alignment and systems integration and create duplicated overheads that raise cost-to-serve. Cross-banner governance frictions and multi-jurisdictional compliance can reduce decision speed and responsiveness.

- Multi-country footprint: SA, AU, NZ (~92m people)

- Systems lag: integration delays hamper rollout

- Higher cost-to-serve: duplicated overheads

- Slower decisions: governance across banners/geographies

Currency translation and input cost risk

Currency translation and input cost risk: volatility between the ZAR and AUD raises sourcing costs for Woolworths and can compress reported earnings when translated into group currency; imported textiles and food inputs remain particularly sensitive to FX swings. Hedging programs mitigate timing and price risk but do not eliminate exposure to sudden moves. Passing costs to consumers via price increases risks dampening demand in price-sensitive segments.

- FX-sensitive imports: textiles, food inputs

- Hedging mitigates but not eliminates risk

- Translation impacts reported earnings

- Price hikes may face consumer resistance

SA 33% unemployment, load-shedding; AU capex drag; 92m footprint FX risk

High SA unemployment (33% Stats SA 2024) and load‑shedding disrupt demand and cold‑chain reliability; AU department store drag requires heavy capex and risks execution; price gap to value chains (ALDI ~10% vs Woolworths ~33% AU, 2024) drives downtrading; FX volatility across a ~92m population footprint raises input and translation risk.

| Weakness | Key metric (2024) |

|---|---|

| SA demand/energy | Unemployment 33% / frequent load‑shedding |

| AU department store drag | High capex & execution risk |

| Value retailer pressure | ALDI ~10% vs Wools ~33% AU |

| Cross‑border FX | Footprint ~92m (SA, AU, NZ) |

Same Document Delivered

Woolworths SWOT Analysis

This is the actual Woolworths SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality and structured insights. The preview below is taken directly from the full report you'll get; buying unlocks the complete, editable version with detailed strengths, weaknesses, opportunities and threats. Purchase to download the entire file immediately after checkout.