Woori Financial Group Boston Consulting Group Matrix

Actionable Strategy Starts Here

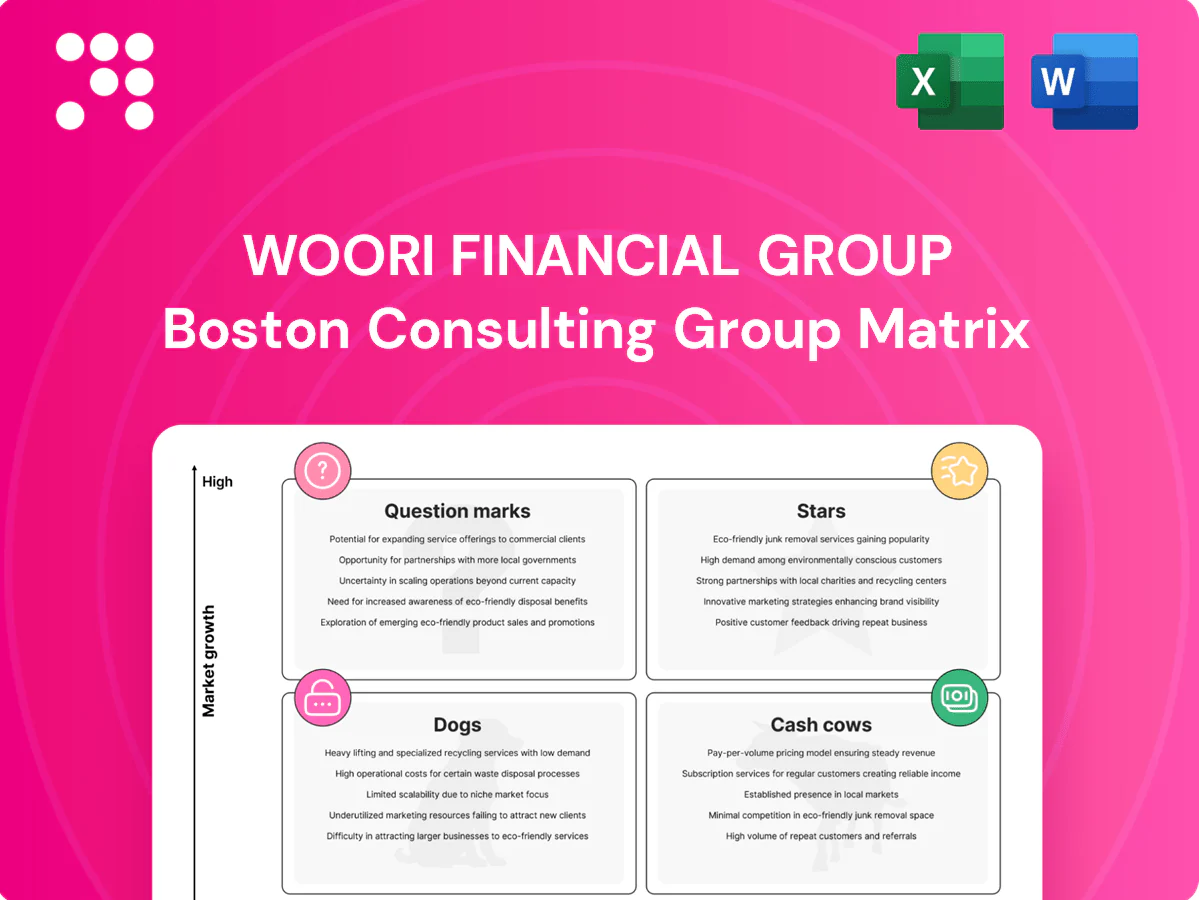

Curious how Woori Financial Group’s businesses stack up—Stars, Cash Cows, Dogs or Question Marks? This preview skims the surface; buy the full BCG Matrix for quadrant-by-quadrant placements, sharp strategic moves, and a ready-to-use Word report plus an Excel summary. Skip the guesswork and get clear, actionable guidance now.

Stars

Mobile banking platform

Explosive user growth (11 million MAU in 2024) and top-tier engagement put Woori’s mobile banking in the lead bucket, driven by a strong brand flywheel that boosts referrals and retention. Korea’s smartphone penetration ~96% and fast digital-banking expansion are converging payments, savings and micro-investing. The app burns cash on UX, data and security but wins retention; keep investing to cement share before growth cools.

SME digital lending

SME demand in Korea is rising—SMEs make up 99.9% of firms and employ about 88% of the workforce (2024 KOSIS)—giving scale for Woori’s data-driven underwriting to capture risk-adjusted volume. Fast decisioning and embedded finance partnerships drive high-volume originations, and unit economics improve as the book seasons. Doubling down on risk models and acquisition can graduate this line into a cash cow.

Trade finance & FX for exporters

Korea’s export engine, which expanded about 3.2% y/y in 2024, keeps trade finance and FX volumes rising, positioning Woori as a go-to for mid-to-large corporates. Cross-sell into FX hedging and cash-management products boosts wallet share and fee income. The business is capital-intensive and relationship-heavy, but premium margins support continued focus. Prioritize digital portals and sticky bundled solutions to deepen retention.

Wealth for mass affluent

Rising household wealth and DIY investing are expanding the mass-affluent segment; Korea household financial assets exceeded 4,000 trillion KRW in 2024, enlarging investable pools. Woori’s distribution reach and brand trust convert to high share in model portfolios and advisory, but brisk growth makes marketing and advisor capacity critical. Build product depth and keep churn low to sustain margins.

- segment: mass affluent

- advantage: distribution & trust

- priority: marketing & advisor hiring

- product: deepen suite

- retention: minimize churn

Green/ESG corporate lending

Woori Financial Group sits in the BCG Matrix as a rising Star in Green/ESG corporate lending: pipeline demand has surged as corporates decarbonize and seek labeled financing, with global sustainable debt issuance topping $1.7 trillion in 2024. Woori’s early mover advantage and syndication strength have translated into visible deal share in Korea’s market, while reporting and third-party verification costs compress margins. The segment scales with standardization; continued origination and common frameworks are needed to lock leadership.

- Pipeline growth: global sustainable debt > $1.7 trillion in 2024

- Strength: early mover + syndication = visible domestic deal share

- Headwind: reporting and verification raise transaction costs

- Strategy: keep originating and standardizing to secure leadership

11M MAU and $1.7T sustainable debt make digital banking a growth bet

Woori’s digital banking and green lending are Stars: 11M MAU and ~96% smartphone penetration fuel rapid customer growth, while global sustainable debt topped $1.7T in 2024, driving labeled loan demand; both require continued investment to secure share and margin. SME and mass‑affluent engines scale cross‑sell and fees but need product depth and risk models to convert to cash cows.

| Metric | 2024 | Implication |

|---|---|---|

| MAU | 11M | Top acquisition |

| Smartphone | ~96% | Digital reach |

| Sustainable debt | $1.7T | Origination runway |

What is included in the product

In-depth BCG Matrix of Woori Financial Group: identifies Stars, Cash Cows, Question Marks, Dogs with invest/hold/divest guidance and trend context.

One-page overview placing each Woori business unit in a quadrant — quick clarity for busy leaders.

Cash Cows

Retail deposits franchise

Woori's retail deposits franchise sits in a mature Korean market where, as of 2024, the group ranks among the top five banks by deposits and holds a double-digit domestic retail deposit market share. Low acquisition cost and minimal promotional spend preserve core balances, providing stable NIM support across the group. Maintaining service quality and strict price discipline allows Woori to milk the float while funding growth at controlled cost.

Credit card issuing

Woori Card sits in the BCG Cash Cow quadrant: card spend in Korea remained steady in 2024 with low single-digit transaction growth, competition has rationalized pricing, and Woori’s large card base drives scale economies; interchange fees and revolving balances provide predictable fee and interest income.

Residential mortgages

Woori Financial Group’s residential mortgage portfolio, about KRW 120 trillion as of mid-2024, is a large, stable book with tight underwriting and an NPL ratio near 0.3%, driving low credit losses. Market growth is muted in 2024 but Woori’s mortgage share remains entrenched—roughly 8% of Korea’s mortgage stock—so marketing intensity stays low and operating costs are contained. Continued back-office automation is targeted to lift margins by cutting processing costs and turnaround times.

Cash management for corporates

Woori Financial Group’s corporate cash management is a cash cow: high stickiness and market share among Korea’s top-5 banks in 2024, with low churn and predictable fee income showing limited organic growth; integration moats from ERP/payments connections deter switching, and focus is on incremental platform upgrades rather than large capex to protect and monetize client flows.

- High stickiness

- High share (top-5 bank, 2024)

- Low churn

- Predictable fee income, limited growth

- Integration moats limit switching

- Incremental upgrades, protect & monetize

Traditional asset management

Traditional asset management is a cash cow for Woori Financial Group: established retail and institutional funds with strong bank-channel distribution generate stable recurring management fees, supporting consistent operating income in 2024; AUM stood at about KRW 60 trillion and net fee income remained a steady share of fee revenue.

Market maturity and fee compression persist, but scale cushions margin pressure—net flows in 2024 were steady rather than spectacular, prompting a focus on efficiency and flagship product promotion to preserve margins.

- Established funds

- Strong distribution

- Recurring fees

- 2024 AUM ~ KRW 60 trillion

- Steady net flows, focus on efficiency

Retail deposits, KRW 120tn mortgages & KRW 60tn AUM underpin 2024 margins

Woori's cash cows—retail deposits, Woori Card, mortgages, corporate cash management and asset management—deliver steady fees and low‑cost funding, supporting group margins in 2024. Retail deposits: top‑5 by deposits with double‑digit domestic retail share; mortgages KRW 120tn (~8% market, NPL 0.3%); AUM KRW 60tn; card sees low‑single digit spend growth.

| Business | 2024 metric | Note |

|---|---|---|

| Mortgages | KRW 120tn | ~8% market, NPL 0.3% |

| AUM | KRW 60tn | steady net flows |

| Card | low‑single % txn growth | scale fees & revolv balances |

What You’re Viewing Is Included

Woori Financial Group BCG Matrix

The file you're previewing is the exact Woori Financial Group BCG Matrix report you'll get after purchase. No watermarks, no placeholders—just a fully formatted, analysis-ready document designed for strategic clarity. It’s immediately downloadable, editable, and presentation-ready. Delivered as shown, no surprises, no extra edits required.

Actionable Strategy Starts Here

Curious how Woori Financial Group’s businesses stack up—Stars, Cash Cows, Dogs or Question Marks? This preview skims the surface; buy the full BCG Matrix for quadrant-by-quadrant placements, sharp strategic moves, and a ready-to-use Word report plus an Excel summary. Skip the guesswork and get clear, actionable guidance now.

Stars

Mobile banking platform

Explosive user growth (11 million MAU in 2024) and top-tier engagement put Woori’s mobile banking in the lead bucket, driven by a strong brand flywheel that boosts referrals and retention. Korea’s smartphone penetration ~96% and fast digital-banking expansion are converging payments, savings and micro-investing. The app burns cash on UX, data and security but wins retention; keep investing to cement share before growth cools.

SME digital lending

SME demand in Korea is rising—SMEs make up 99.9% of firms and employ about 88% of the workforce (2024 KOSIS)—giving scale for Woori’s data-driven underwriting to capture risk-adjusted volume. Fast decisioning and embedded finance partnerships drive high-volume originations, and unit economics improve as the book seasons. Doubling down on risk models and acquisition can graduate this line into a cash cow.

Trade finance & FX for exporters

Korea’s export engine, which expanded about 3.2% y/y in 2024, keeps trade finance and FX volumes rising, positioning Woori as a go-to for mid-to-large corporates. Cross-sell into FX hedging and cash-management products boosts wallet share and fee income. The business is capital-intensive and relationship-heavy, but premium margins support continued focus. Prioritize digital portals and sticky bundled solutions to deepen retention.

Wealth for mass affluent

Rising household wealth and DIY investing are expanding the mass-affluent segment; Korea household financial assets exceeded 4,000 trillion KRW in 2024, enlarging investable pools. Woori’s distribution reach and brand trust convert to high share in model portfolios and advisory, but brisk growth makes marketing and advisor capacity critical. Build product depth and keep churn low to sustain margins.

- segment: mass affluent

- advantage: distribution & trust

- priority: marketing & advisor hiring

- product: deepen suite

- retention: minimize churn

Green/ESG corporate lending

Woori Financial Group sits in the BCG Matrix as a rising Star in Green/ESG corporate lending: pipeline demand has surged as corporates decarbonize and seek labeled financing, with global sustainable debt issuance topping $1.7 trillion in 2024. Woori’s early mover advantage and syndication strength have translated into visible deal share in Korea’s market, while reporting and third-party verification costs compress margins. The segment scales with standardization; continued origination and common frameworks are needed to lock leadership.

- Pipeline growth: global sustainable debt > $1.7 trillion in 2024

- Strength: early mover + syndication = visible domestic deal share

- Headwind: reporting and verification raise transaction costs

- Strategy: keep originating and standardizing to secure leadership

11M MAU and $1.7T sustainable debt make digital banking a growth bet

Woori’s digital banking and green lending are Stars: 11M MAU and ~96% smartphone penetration fuel rapid customer growth, while global sustainable debt topped $1.7T in 2024, driving labeled loan demand; both require continued investment to secure share and margin. SME and mass‑affluent engines scale cross‑sell and fees but need product depth and risk models to convert to cash cows.

| Metric | 2024 | Implication |

|---|---|---|

| MAU | 11M | Top acquisition |

| Smartphone | ~96% | Digital reach |

| Sustainable debt | $1.7T | Origination runway |

What is included in the product

In-depth BCG Matrix of Woori Financial Group: identifies Stars, Cash Cows, Question Marks, Dogs with invest/hold/divest guidance and trend context.

One-page overview placing each Woori business unit in a quadrant — quick clarity for busy leaders.

Cash Cows

Retail deposits franchise

Woori's retail deposits franchise sits in a mature Korean market where, as of 2024, the group ranks among the top five banks by deposits and holds a double-digit domestic retail deposit market share. Low acquisition cost and minimal promotional spend preserve core balances, providing stable NIM support across the group. Maintaining service quality and strict price discipline allows Woori to milk the float while funding growth at controlled cost.

Credit card issuing

Woori Card sits in the BCG Cash Cow quadrant: card spend in Korea remained steady in 2024 with low single-digit transaction growth, competition has rationalized pricing, and Woori’s large card base drives scale economies; interchange fees and revolving balances provide predictable fee and interest income.

Residential mortgages

Woori Financial Group’s residential mortgage portfolio, about KRW 120 trillion as of mid-2024, is a large, stable book with tight underwriting and an NPL ratio near 0.3%, driving low credit losses. Market growth is muted in 2024 but Woori’s mortgage share remains entrenched—roughly 8% of Korea’s mortgage stock—so marketing intensity stays low and operating costs are contained. Continued back-office automation is targeted to lift margins by cutting processing costs and turnaround times.

Cash management for corporates

Woori Financial Group’s corporate cash management is a cash cow: high stickiness and market share among Korea’s top-5 banks in 2024, with low churn and predictable fee income showing limited organic growth; integration moats from ERP/payments connections deter switching, and focus is on incremental platform upgrades rather than large capex to protect and monetize client flows.

- High stickiness

- High share (top-5 bank, 2024)

- Low churn

- Predictable fee income, limited growth

- Integration moats limit switching

- Incremental upgrades, protect & monetize

Traditional asset management

Traditional asset management is a cash cow for Woori Financial Group: established retail and institutional funds with strong bank-channel distribution generate stable recurring management fees, supporting consistent operating income in 2024; AUM stood at about KRW 60 trillion and net fee income remained a steady share of fee revenue.

Market maturity and fee compression persist, but scale cushions margin pressure—net flows in 2024 were steady rather than spectacular, prompting a focus on efficiency and flagship product promotion to preserve margins.

- Established funds

- Strong distribution

- Recurring fees

- 2024 AUM ~ KRW 60 trillion

- Steady net flows, focus on efficiency

Retail deposits, KRW 120tn mortgages & KRW 60tn AUM underpin 2024 margins

Woori's cash cows—retail deposits, Woori Card, mortgages, corporate cash management and asset management—deliver steady fees and low‑cost funding, supporting group margins in 2024. Retail deposits: top‑5 by deposits with double‑digit domestic retail share; mortgages KRW 120tn (~8% market, NPL 0.3%); AUM KRW 60tn; card sees low‑single digit spend growth.

| Business | 2024 metric | Note |

|---|---|---|

| Mortgages | KRW 120tn | ~8% market, NPL 0.3% |

| AUM | KRW 60tn | steady net flows |

| Card | low‑single % txn growth | scale fees & revolv balances |

What You’re Viewing Is Included

Woori Financial Group BCG Matrix

The file you're previewing is the exact Woori Financial Group BCG Matrix report you'll get after purchase. No watermarks, no placeholders—just a fully formatted, analysis-ready document designed for strategic clarity. It’s immediately downloadable, editable, and presentation-ready. Delivered as shown, no surprises, no extra edits required.

Original: $10.00

-65%$10.00

$3.50Description

Actionable Strategy Starts Here

Curious how Woori Financial Group’s businesses stack up—Stars, Cash Cows, Dogs or Question Marks? This preview skims the surface; buy the full BCG Matrix for quadrant-by-quadrant placements, sharp strategic moves, and a ready-to-use Word report plus an Excel summary. Skip the guesswork and get clear, actionable guidance now.

Stars

Mobile banking platform

Explosive user growth (11 million MAU in 2024) and top-tier engagement put Woori’s mobile banking in the lead bucket, driven by a strong brand flywheel that boosts referrals and retention. Korea’s smartphone penetration ~96% and fast digital-banking expansion are converging payments, savings and micro-investing. The app burns cash on UX, data and security but wins retention; keep investing to cement share before growth cools.

SME digital lending

SME demand in Korea is rising—SMEs make up 99.9% of firms and employ about 88% of the workforce (2024 KOSIS)—giving scale for Woori’s data-driven underwriting to capture risk-adjusted volume. Fast decisioning and embedded finance partnerships drive high-volume originations, and unit economics improve as the book seasons. Doubling down on risk models and acquisition can graduate this line into a cash cow.

Trade finance & FX for exporters

Korea’s export engine, which expanded about 3.2% y/y in 2024, keeps trade finance and FX volumes rising, positioning Woori as a go-to for mid-to-large corporates. Cross-sell into FX hedging and cash-management products boosts wallet share and fee income. The business is capital-intensive and relationship-heavy, but premium margins support continued focus. Prioritize digital portals and sticky bundled solutions to deepen retention.

Wealth for mass affluent

Rising household wealth and DIY investing are expanding the mass-affluent segment; Korea household financial assets exceeded 4,000 trillion KRW in 2024, enlarging investable pools. Woori’s distribution reach and brand trust convert to high share in model portfolios and advisory, but brisk growth makes marketing and advisor capacity critical. Build product depth and keep churn low to sustain margins.

- segment: mass affluent

- advantage: distribution & trust

- priority: marketing & advisor hiring

- product: deepen suite

- retention: minimize churn

Green/ESG corporate lending

Woori Financial Group sits in the BCG Matrix as a rising Star in Green/ESG corporate lending: pipeline demand has surged as corporates decarbonize and seek labeled financing, with global sustainable debt issuance topping $1.7 trillion in 2024. Woori’s early mover advantage and syndication strength have translated into visible deal share in Korea’s market, while reporting and third-party verification costs compress margins. The segment scales with standardization; continued origination and common frameworks are needed to lock leadership.

- Pipeline growth: global sustainable debt > $1.7 trillion in 2024

- Strength: early mover + syndication = visible domestic deal share

- Headwind: reporting and verification raise transaction costs

- Strategy: keep originating and standardizing to secure leadership

11M MAU and $1.7T sustainable debt make digital banking a growth bet

Woori’s digital banking and green lending are Stars: 11M MAU and ~96% smartphone penetration fuel rapid customer growth, while global sustainable debt topped $1.7T in 2024, driving labeled loan demand; both require continued investment to secure share and margin. SME and mass‑affluent engines scale cross‑sell and fees but need product depth and risk models to convert to cash cows.

| Metric | 2024 | Implication |

|---|---|---|

| MAU | 11M | Top acquisition |

| Smartphone | ~96% | Digital reach |

| Sustainable debt | $1.7T | Origination runway |

What is included in the product

In-depth BCG Matrix of Woori Financial Group: identifies Stars, Cash Cows, Question Marks, Dogs with invest/hold/divest guidance and trend context.

One-page overview placing each Woori business unit in a quadrant — quick clarity for busy leaders.

Cash Cows

Retail deposits franchise

Woori's retail deposits franchise sits in a mature Korean market where, as of 2024, the group ranks among the top five banks by deposits and holds a double-digit domestic retail deposit market share. Low acquisition cost and minimal promotional spend preserve core balances, providing stable NIM support across the group. Maintaining service quality and strict price discipline allows Woori to milk the float while funding growth at controlled cost.

Credit card issuing

Woori Card sits in the BCG Cash Cow quadrant: card spend in Korea remained steady in 2024 with low single-digit transaction growth, competition has rationalized pricing, and Woori’s large card base drives scale economies; interchange fees and revolving balances provide predictable fee and interest income.

Residential mortgages

Woori Financial Group’s residential mortgage portfolio, about KRW 120 trillion as of mid-2024, is a large, stable book with tight underwriting and an NPL ratio near 0.3%, driving low credit losses. Market growth is muted in 2024 but Woori’s mortgage share remains entrenched—roughly 8% of Korea’s mortgage stock—so marketing intensity stays low and operating costs are contained. Continued back-office automation is targeted to lift margins by cutting processing costs and turnaround times.

Cash management for corporates

Woori Financial Group’s corporate cash management is a cash cow: high stickiness and market share among Korea’s top-5 banks in 2024, with low churn and predictable fee income showing limited organic growth; integration moats from ERP/payments connections deter switching, and focus is on incremental platform upgrades rather than large capex to protect and monetize client flows.

- High stickiness

- High share (top-5 bank, 2024)

- Low churn

- Predictable fee income, limited growth

- Integration moats limit switching

- Incremental upgrades, protect & monetize

Traditional asset management

Traditional asset management is a cash cow for Woori Financial Group: established retail and institutional funds with strong bank-channel distribution generate stable recurring management fees, supporting consistent operating income in 2024; AUM stood at about KRW 60 trillion and net fee income remained a steady share of fee revenue.

Market maturity and fee compression persist, but scale cushions margin pressure—net flows in 2024 were steady rather than spectacular, prompting a focus on efficiency and flagship product promotion to preserve margins.

- Established funds

- Strong distribution

- Recurring fees

- 2024 AUM ~ KRW 60 trillion

- Steady net flows, focus on efficiency

Retail deposits, KRW 120tn mortgages & KRW 60tn AUM underpin 2024 margins

Woori's cash cows—retail deposits, Woori Card, mortgages, corporate cash management and asset management—deliver steady fees and low‑cost funding, supporting group margins in 2024. Retail deposits: top‑5 by deposits with double‑digit domestic retail share; mortgages KRW 120tn (~8% market, NPL 0.3%); AUM KRW 60tn; card sees low‑single digit spend growth.

| Business | 2024 metric | Note |

|---|---|---|

| Mortgages | KRW 120tn | ~8% market, NPL 0.3% |

| AUM | KRW 60tn | steady net flows |

| Card | low‑single % txn growth | scale fees & revolv balances |

What You’re Viewing Is Included

Woori Financial Group BCG Matrix

The file you're previewing is the exact Woori Financial Group BCG Matrix report you'll get after purchase. No watermarks, no placeholders—just a fully formatted, analysis-ready document designed for strategic clarity. It’s immediately downloadable, editable, and presentation-ready. Delivered as shown, no surprises, no extra edits required.