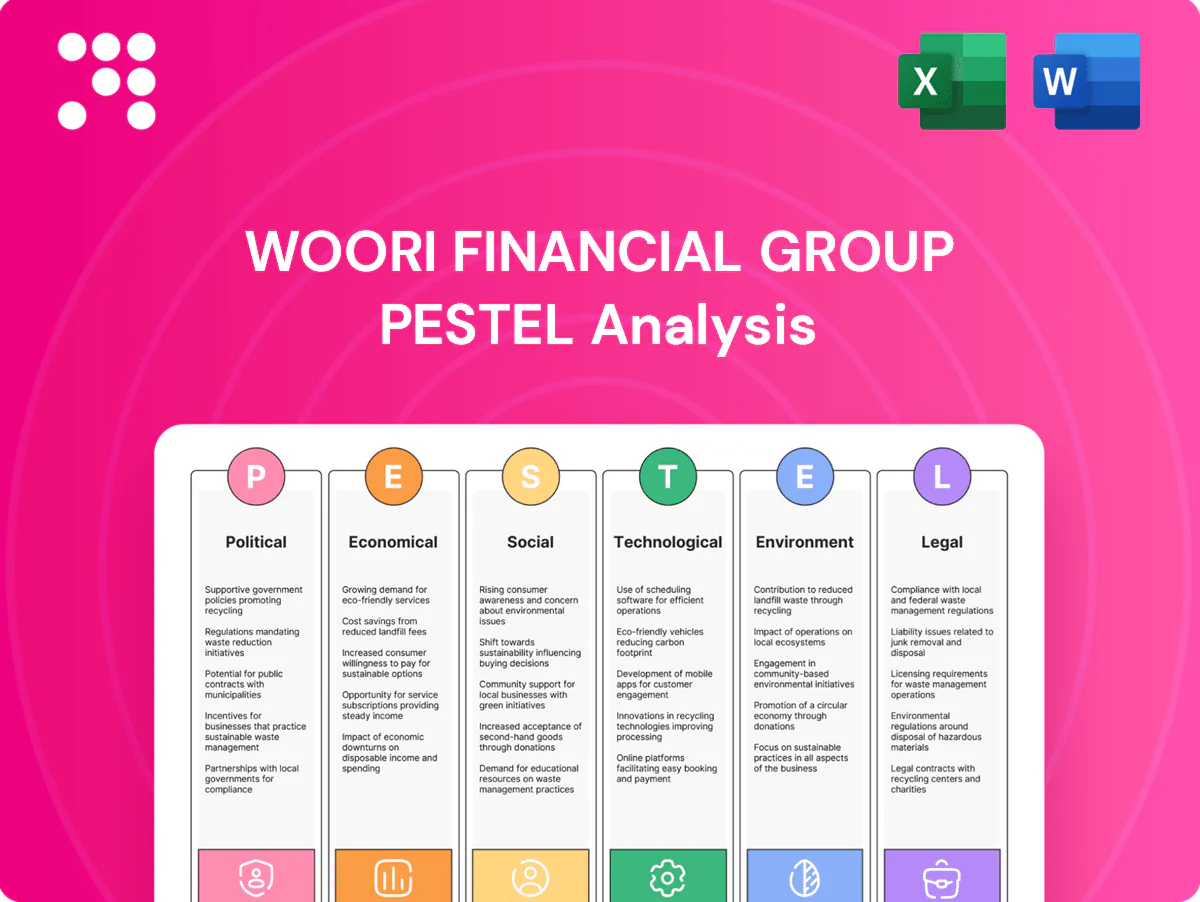

Woori Financial Group PESTLE Analysis

Skip the Research. Get the Strategy.

Our PESTLE Analysis of Woori Financial Group reveals how political regulation, shifting economic conditions, social trends, technological disruption, and legal and environmental pressures shape strategic risk and opportunity. Gain practical insights to refine forecasts and competitive moves. Purchase the full report for the complete, ready-to-use breakdown.

Political factors

Regulatory direction by Korea’s FSC/FSS

Policy shifts on capital, consumer protection and supervision by Korea’s FSC/FSS can materially alter Woori’s lending appetite, fee structures and product design.

Heightened scrutiny on household debt curbs—Korea household debt was about 1,930 trillion won in Q1 2024—can constrain retail growth while improving asset quality.

Woori must align quickly with thematic exams and stress-test guidance; proactive engagement limits remediation costs and reputational risk.

Government stance on household debt

South Korea's household debt remains elevated at around 1,900 trillion won as of 2024, prompting macroprudential limits that can cap mortgage volumes and tighten underwriting standards. Such measures compress net interest income and shift loan mix toward SMEs or unsecured credit, raising portfolio risk. Woori can pivot to fee-based businesses and tighter risk-adjusted pricing to protect margins. Close monitoring of LTV/DTI rule changes is essential for strategic lending adjustments.

Geopolitical tensions on the peninsula

Geopolitical tensions on the peninsula raise market volatility and can inflate funding spreads, pressuring Woori’s liquidity and cost of capital; South Korea held about $439 billion in FX reserves at end‑2023 (IMF). Robust contingency planning for sudden liquidity and FX shocks is essential. Insurance, hedging and higher capital buffers mitigate tail risks. Clear, stable communication preserves depositor confidence and reduces run risk.

Industrial policy and financial digitalization

State promotion of fintech, open banking (launched 2019) and SME support increases competition but expands partnership routes; Woori can use sandboxes and consortiums to pilot services, aligning with national digital finance goals. Incentives reduce innovation costs while raising expectations for faster execution; Korea reported over 27 million open-banking users by 2024, accelerating adoption pressures on incumbents.

- Sandbox access: faster pilots

- Incentives: lower capex, higher speed

- Open banking scale: ~27M users (2024)

International relations and sanctions regimes

International sanctions regimes materially affect Woori Financial Group’s cross-border payments and trade finance, especially in high-risk corridors; with group assets near 448 trillion KRW (end-2024), compliance lapses risk heavy fines and restricted correspondent access.

Robust screening, sanctions filtering and correspondent-banking oversight are critical; diversifying geographic exposure reduces concentration risk and operational choke points.

- Sanctions compliance: critical for trade finance and payments

- Financial exposure: group assets ~448 trillion KRW (end-2024)

- Risk: fines and access restrictions if controls fail

- Controls: screening, correspondent oversight, geographic diversification

FSC policy and household debt ≈1,900 trn KRW tighten retail margins

Policy shifts by FSC/FSS on capital, consumer protection and household debt (≈1,900trn KRW in 2024) can constrain Woori’s retail lending and margins.

Geopolitical tensions raise funding spreads; FX reserves were $439bn end‑2023, so liquidity planning is critical.

Open banking (~27M users in 2024) and sanctions risk reshape competition and cross‑border operations.

| Metric | Value |

|---|---|

| Household debt | ≈1,900 trn KRW (Q1 2024) |

| Group assets | ≈448 trn KRW (end‑2024) |

| Open‑banking users | ~27M (2024) |

| FX reserves | $439bn (end‑2023) |

What is included in the product

Explores how external macro-environmental factors uniquely affect Woori Financial Group across Political, Economic, Social, Technological, Environmental and Legal dimensions, with each section backed by relevant data and regional regulatory context. Designed for executives and investors, it offers forward-looking insights, scenario implications, and actionable opportunities and risks for strategy and capital planning.

A concise, visually segmented PESTLE summary of Woori Financial Group for easy sharing and drop‑in use in presentations, enabling quick alignment across teams and supporting external risk and market‑positioning discussions.

Economic factors

Interest rate cycle and NIM sensitivity

Bank of Korea moves in 2024–25 directly swing Woori Financial Group margins and loan demand, with tightening cycles initially boosting net interest margin while cooling credit appetite. Rising rates lift NIM but increase credit costs, especially in mortgages and SME portfolios where delinquencies historically rise after hikes. Robust asset-liability management is essential to stabilize earnings and hedge duration mismatch. Scenario planning across plausible rate paths underpins disciplined loan and deposit pricing.

Export-driven GDP and global demand

Korea's export-driven GDP (exports ≈44% of GDP) and semiconductors (~20% of merchandise exports) make corporate credit highly cyclical, with chip and manufacturing downturns stressing borrowers. Slowdowns in US/China/EU erode SME cash flows via trade linkages. Woori needs granular sectoral concentration limits and to grow counter-cyclical fee income to hedge revenue.

KRW volatility and FX risk

KRW swings (USD/KRW roughly 1,200–1,400 in 2024 with ~8% annual movement) press Woori’s funding costs, CET1 capital ratios and overseas-unit valuations, squeezing capital adequacy during depreciations. Client demand for FX hedges raises fee income but increases trading VaR and market risk exposure. Robust treasury controls, strict VaR limits and contingent liquidity lines (supported by Korea's ~420bn USD FX reserves in 2024) are essential to cushion stress periods.

Household leverage and real estate prices

High household debt, ~1,930 trillion won in 2024, increases Woori Financial Group sensitivity to unemployment and interest-rate shocks, amplifying default risk; a 1 percentage-point rate rise could materially press cashflows. Real estate corrections can drive NPL upticks and collateral haircuts, as seen in rising stress indicators and a banking-sector NPL trend near 0.5% in 2024. Tighter underwriting and enhanced early-warning systems have reduced loss severity, while rebalancing toward secured SME lending with strong covenants improves portfolio resilience.

- household debt: ~1,930 trillion won (2024)

- NPL trend: ~0.5% (2024)

- mitigants: tighter underwriting, early-warning systems

- strategy: shift to secured SME with strong covenants

Inflation and cost management

Inflation in South Korea averaged 2.6% in 2024 (Statistics Korea), pushing Woori Financial Group operating expenses higher via wage and tech investments and pressuring efficiency ratios and margins. Softer household purchasing power has dampened retail credit demand, while pricing, fee optimization and automation are used to offset margin pressure. Procurement renegotiation can unlock procurement savings and improve cost-to-income over time.

- Operating costs: wage/tech up → efficiency pressure

- Retail demand: weaker disposable income → lower credit growth

- Mitigants: pricing, fees, automation

- Savings: procurement/vendor renegotiation

FSC policy and household debt ≈1,900 trn KRW tighten retail margins

Korea rate cycle 2024–25 alters NIM vs credit costs; BoK hikes lift NIM but raise mortgage/SME delinquencies. Export cyclicality (exports ≈44% GDP; semiconductors ~20% merch exports) heightens corporate credit volatility. KRW swings (USD/KRW 1,200–1,400 in 2024) stress funding and CET1. Household debt ~1,930 tn won (2024) raises default sensitivity.

| Metric | 2024 |

|---|---|

| Household debt | 1,930 tn won |

| NPLs | ~0.5% |

| Exports/GDP | ≈44% |

| USD/KRW | 1,200–1,400 |

What You See Is What You Get

Woori Financial Group PESTLE Analysis

The preview shown here is the exact Woori Financial Group PESTLE Analysis you’ll receive after purchase—fully formatted and ready to use. It contains the complete political, economic, social, technological, legal and environmental assessments and professional layout as displayed. No placeholders or edits are required; download the final file immediately after payment.

Skip the Research. Get the Strategy.

Our PESTLE Analysis of Woori Financial Group reveals how political regulation, shifting economic conditions, social trends, technological disruption, and legal and environmental pressures shape strategic risk and opportunity. Gain practical insights to refine forecasts and competitive moves. Purchase the full report for the complete, ready-to-use breakdown.

Political factors

Regulatory direction by Korea’s FSC/FSS

Policy shifts on capital, consumer protection and supervision by Korea’s FSC/FSS can materially alter Woori’s lending appetite, fee structures and product design.

Heightened scrutiny on household debt curbs—Korea household debt was about 1,930 trillion won in Q1 2024—can constrain retail growth while improving asset quality.

Woori must align quickly with thematic exams and stress-test guidance; proactive engagement limits remediation costs and reputational risk.

Government stance on household debt

South Korea's household debt remains elevated at around 1,900 trillion won as of 2024, prompting macroprudential limits that can cap mortgage volumes and tighten underwriting standards. Such measures compress net interest income and shift loan mix toward SMEs or unsecured credit, raising portfolio risk. Woori can pivot to fee-based businesses and tighter risk-adjusted pricing to protect margins. Close monitoring of LTV/DTI rule changes is essential for strategic lending adjustments.

Geopolitical tensions on the peninsula

Geopolitical tensions on the peninsula raise market volatility and can inflate funding spreads, pressuring Woori’s liquidity and cost of capital; South Korea held about $439 billion in FX reserves at end‑2023 (IMF). Robust contingency planning for sudden liquidity and FX shocks is essential. Insurance, hedging and higher capital buffers mitigate tail risks. Clear, stable communication preserves depositor confidence and reduces run risk.

Industrial policy and financial digitalization

State promotion of fintech, open banking (launched 2019) and SME support increases competition but expands partnership routes; Woori can use sandboxes and consortiums to pilot services, aligning with national digital finance goals. Incentives reduce innovation costs while raising expectations for faster execution; Korea reported over 27 million open-banking users by 2024, accelerating adoption pressures on incumbents.

- Sandbox access: faster pilots

- Incentives: lower capex, higher speed

- Open banking scale: ~27M users (2024)

International relations and sanctions regimes

International sanctions regimes materially affect Woori Financial Group’s cross-border payments and trade finance, especially in high-risk corridors; with group assets near 448 trillion KRW (end-2024), compliance lapses risk heavy fines and restricted correspondent access.

Robust screening, sanctions filtering and correspondent-banking oversight are critical; diversifying geographic exposure reduces concentration risk and operational choke points.

- Sanctions compliance: critical for trade finance and payments

- Financial exposure: group assets ~448 trillion KRW (end-2024)

- Risk: fines and access restrictions if controls fail

- Controls: screening, correspondent oversight, geographic diversification

FSC policy and household debt ≈1,900 trn KRW tighten retail margins

Policy shifts by FSC/FSS on capital, consumer protection and household debt (≈1,900trn KRW in 2024) can constrain Woori’s retail lending and margins.

Geopolitical tensions raise funding spreads; FX reserves were $439bn end‑2023, so liquidity planning is critical.

Open banking (~27M users in 2024) and sanctions risk reshape competition and cross‑border operations.

| Metric | Value |

|---|---|

| Household debt | ≈1,900 trn KRW (Q1 2024) |

| Group assets | ≈448 trn KRW (end‑2024) |

| Open‑banking users | ~27M (2024) |

| FX reserves | $439bn (end‑2023) |

What is included in the product

Explores how external macro-environmental factors uniquely affect Woori Financial Group across Political, Economic, Social, Technological, Environmental and Legal dimensions, with each section backed by relevant data and regional regulatory context. Designed for executives and investors, it offers forward-looking insights, scenario implications, and actionable opportunities and risks for strategy and capital planning.

A concise, visually segmented PESTLE summary of Woori Financial Group for easy sharing and drop‑in use in presentations, enabling quick alignment across teams and supporting external risk and market‑positioning discussions.

Economic factors

Interest rate cycle and NIM sensitivity

Bank of Korea moves in 2024–25 directly swing Woori Financial Group margins and loan demand, with tightening cycles initially boosting net interest margin while cooling credit appetite. Rising rates lift NIM but increase credit costs, especially in mortgages and SME portfolios where delinquencies historically rise after hikes. Robust asset-liability management is essential to stabilize earnings and hedge duration mismatch. Scenario planning across plausible rate paths underpins disciplined loan and deposit pricing.

Export-driven GDP and global demand

Korea's export-driven GDP (exports ≈44% of GDP) and semiconductors (~20% of merchandise exports) make corporate credit highly cyclical, with chip and manufacturing downturns stressing borrowers. Slowdowns in US/China/EU erode SME cash flows via trade linkages. Woori needs granular sectoral concentration limits and to grow counter-cyclical fee income to hedge revenue.

KRW volatility and FX risk

KRW swings (USD/KRW roughly 1,200–1,400 in 2024 with ~8% annual movement) press Woori’s funding costs, CET1 capital ratios and overseas-unit valuations, squeezing capital adequacy during depreciations. Client demand for FX hedges raises fee income but increases trading VaR and market risk exposure. Robust treasury controls, strict VaR limits and contingent liquidity lines (supported by Korea's ~420bn USD FX reserves in 2024) are essential to cushion stress periods.

Household leverage and real estate prices

High household debt, ~1,930 trillion won in 2024, increases Woori Financial Group sensitivity to unemployment and interest-rate shocks, amplifying default risk; a 1 percentage-point rate rise could materially press cashflows. Real estate corrections can drive NPL upticks and collateral haircuts, as seen in rising stress indicators and a banking-sector NPL trend near 0.5% in 2024. Tighter underwriting and enhanced early-warning systems have reduced loss severity, while rebalancing toward secured SME lending with strong covenants improves portfolio resilience.

- household debt: ~1,930 trillion won (2024)

- NPL trend: ~0.5% (2024)

- mitigants: tighter underwriting, early-warning systems

- strategy: shift to secured SME with strong covenants

Inflation and cost management

Inflation in South Korea averaged 2.6% in 2024 (Statistics Korea), pushing Woori Financial Group operating expenses higher via wage and tech investments and pressuring efficiency ratios and margins. Softer household purchasing power has dampened retail credit demand, while pricing, fee optimization and automation are used to offset margin pressure. Procurement renegotiation can unlock procurement savings and improve cost-to-income over time.

- Operating costs: wage/tech up → efficiency pressure

- Retail demand: weaker disposable income → lower credit growth

- Mitigants: pricing, fees, automation

- Savings: procurement/vendor renegotiation

FSC policy and household debt ≈1,900 trn KRW tighten retail margins

Korea rate cycle 2024–25 alters NIM vs credit costs; BoK hikes lift NIM but raise mortgage/SME delinquencies. Export cyclicality (exports ≈44% GDP; semiconductors ~20% merch exports) heightens corporate credit volatility. KRW swings (USD/KRW 1,200–1,400 in 2024) stress funding and CET1. Household debt ~1,930 tn won (2024) raises default sensitivity.

| Metric | 2024 |

|---|---|

| Household debt | 1,930 tn won |

| NPLs | ~0.5% |

| Exports/GDP | ≈44% |

| USD/KRW | 1,200–1,400 |

What You See Is What You Get

Woori Financial Group PESTLE Analysis

The preview shown here is the exact Woori Financial Group PESTLE Analysis you’ll receive after purchase—fully formatted and ready to use. It contains the complete political, economic, social, technological, legal and environmental assessments and professional layout as displayed. No placeholders or edits are required; download the final file immediately after payment.

Description

Skip the Research. Get the Strategy.

Our PESTLE Analysis of Woori Financial Group reveals how political regulation, shifting economic conditions, social trends, technological disruption, and legal and environmental pressures shape strategic risk and opportunity. Gain practical insights to refine forecasts and competitive moves. Purchase the full report for the complete, ready-to-use breakdown.

Political factors

Regulatory direction by Korea’s FSC/FSS

Policy shifts on capital, consumer protection and supervision by Korea’s FSC/FSS can materially alter Woori’s lending appetite, fee structures and product design.

Heightened scrutiny on household debt curbs—Korea household debt was about 1,930 trillion won in Q1 2024—can constrain retail growth while improving asset quality.

Woori must align quickly with thematic exams and stress-test guidance; proactive engagement limits remediation costs and reputational risk.

Government stance on household debt

South Korea's household debt remains elevated at around 1,900 trillion won as of 2024, prompting macroprudential limits that can cap mortgage volumes and tighten underwriting standards. Such measures compress net interest income and shift loan mix toward SMEs or unsecured credit, raising portfolio risk. Woori can pivot to fee-based businesses and tighter risk-adjusted pricing to protect margins. Close monitoring of LTV/DTI rule changes is essential for strategic lending adjustments.

Geopolitical tensions on the peninsula

Geopolitical tensions on the peninsula raise market volatility and can inflate funding spreads, pressuring Woori’s liquidity and cost of capital; South Korea held about $439 billion in FX reserves at end‑2023 (IMF). Robust contingency planning for sudden liquidity and FX shocks is essential. Insurance, hedging and higher capital buffers mitigate tail risks. Clear, stable communication preserves depositor confidence and reduces run risk.

Industrial policy and financial digitalization

State promotion of fintech, open banking (launched 2019) and SME support increases competition but expands partnership routes; Woori can use sandboxes and consortiums to pilot services, aligning with national digital finance goals. Incentives reduce innovation costs while raising expectations for faster execution; Korea reported over 27 million open-banking users by 2024, accelerating adoption pressures on incumbents.

- Sandbox access: faster pilots

- Incentives: lower capex, higher speed

- Open banking scale: ~27M users (2024)

International relations and sanctions regimes

International sanctions regimes materially affect Woori Financial Group’s cross-border payments and trade finance, especially in high-risk corridors; with group assets near 448 trillion KRW (end-2024), compliance lapses risk heavy fines and restricted correspondent access.

Robust screening, sanctions filtering and correspondent-banking oversight are critical; diversifying geographic exposure reduces concentration risk and operational choke points.

- Sanctions compliance: critical for trade finance and payments

- Financial exposure: group assets ~448 trillion KRW (end-2024)

- Risk: fines and access restrictions if controls fail

- Controls: screening, correspondent oversight, geographic diversification

FSC policy and household debt ≈1,900 trn KRW tighten retail margins

Policy shifts by FSC/FSS on capital, consumer protection and household debt (≈1,900trn KRW in 2024) can constrain Woori’s retail lending and margins.

Geopolitical tensions raise funding spreads; FX reserves were $439bn end‑2023, so liquidity planning is critical.

Open banking (~27M users in 2024) and sanctions risk reshape competition and cross‑border operations.

| Metric | Value |

|---|---|

| Household debt | ≈1,900 trn KRW (Q1 2024) |

| Group assets | ≈448 trn KRW (end‑2024) |

| Open‑banking users | ~27M (2024) |

| FX reserves | $439bn (end‑2023) |

What is included in the product

Explores how external macro-environmental factors uniquely affect Woori Financial Group across Political, Economic, Social, Technological, Environmental and Legal dimensions, with each section backed by relevant data and regional regulatory context. Designed for executives and investors, it offers forward-looking insights, scenario implications, and actionable opportunities and risks for strategy and capital planning.

A concise, visually segmented PESTLE summary of Woori Financial Group for easy sharing and drop‑in use in presentations, enabling quick alignment across teams and supporting external risk and market‑positioning discussions.

Economic factors

Interest rate cycle and NIM sensitivity

Bank of Korea moves in 2024–25 directly swing Woori Financial Group margins and loan demand, with tightening cycles initially boosting net interest margin while cooling credit appetite. Rising rates lift NIM but increase credit costs, especially in mortgages and SME portfolios where delinquencies historically rise after hikes. Robust asset-liability management is essential to stabilize earnings and hedge duration mismatch. Scenario planning across plausible rate paths underpins disciplined loan and deposit pricing.

Export-driven GDP and global demand

Korea's export-driven GDP (exports ≈44% of GDP) and semiconductors (~20% of merchandise exports) make corporate credit highly cyclical, with chip and manufacturing downturns stressing borrowers. Slowdowns in US/China/EU erode SME cash flows via trade linkages. Woori needs granular sectoral concentration limits and to grow counter-cyclical fee income to hedge revenue.

KRW volatility and FX risk

KRW swings (USD/KRW roughly 1,200–1,400 in 2024 with ~8% annual movement) press Woori’s funding costs, CET1 capital ratios and overseas-unit valuations, squeezing capital adequacy during depreciations. Client demand for FX hedges raises fee income but increases trading VaR and market risk exposure. Robust treasury controls, strict VaR limits and contingent liquidity lines (supported by Korea's ~420bn USD FX reserves in 2024) are essential to cushion stress periods.

Household leverage and real estate prices

High household debt, ~1,930 trillion won in 2024, increases Woori Financial Group sensitivity to unemployment and interest-rate shocks, amplifying default risk; a 1 percentage-point rate rise could materially press cashflows. Real estate corrections can drive NPL upticks and collateral haircuts, as seen in rising stress indicators and a banking-sector NPL trend near 0.5% in 2024. Tighter underwriting and enhanced early-warning systems have reduced loss severity, while rebalancing toward secured SME lending with strong covenants improves portfolio resilience.

- household debt: ~1,930 trillion won (2024)

- NPL trend: ~0.5% (2024)

- mitigants: tighter underwriting, early-warning systems

- strategy: shift to secured SME with strong covenants

Inflation and cost management

Inflation in South Korea averaged 2.6% in 2024 (Statistics Korea), pushing Woori Financial Group operating expenses higher via wage and tech investments and pressuring efficiency ratios and margins. Softer household purchasing power has dampened retail credit demand, while pricing, fee optimization and automation are used to offset margin pressure. Procurement renegotiation can unlock procurement savings and improve cost-to-income over time.

- Operating costs: wage/tech up → efficiency pressure

- Retail demand: weaker disposable income → lower credit growth

- Mitigants: pricing, fees, automation

- Savings: procurement/vendor renegotiation

FSC policy and household debt ≈1,900 trn KRW tighten retail margins

Korea rate cycle 2024–25 alters NIM vs credit costs; BoK hikes lift NIM but raise mortgage/SME delinquencies. Export cyclicality (exports ≈44% GDP; semiconductors ~20% merch exports) heightens corporate credit volatility. KRW swings (USD/KRW 1,200–1,400 in 2024) stress funding and CET1. Household debt ~1,930 tn won (2024) raises default sensitivity.

| Metric | 2024 |

|---|---|

| Household debt | 1,930 tn won |

| NPLs | ~0.5% |

| Exports/GDP | ≈44% |

| USD/KRW | 1,200–1,400 |

What You See Is What You Get

Woori Financial Group PESTLE Analysis

The preview shown here is the exact Woori Financial Group PESTLE Analysis you’ll receive after purchase—fully formatted and ready to use. It contains the complete political, economic, social, technological, legal and environmental assessments and professional layout as displayed. No placeholders or edits are required; download the final file immediately after payment.