Workday SWOT Analysis

Go Beyond the Preview—Access the Full Strategic Report

Explore Workday’s competitive advantages, innovation drivers, and risk profile in a concise SWOT snapshot that highlights strategic implications for investors and enterprise buyers. Want the full picture with data-backed recommendations and editable deliverables? Purchase the complete SWOT analysis to get the detailed Word report and Excel model you can use for planning, pitching, or investing.

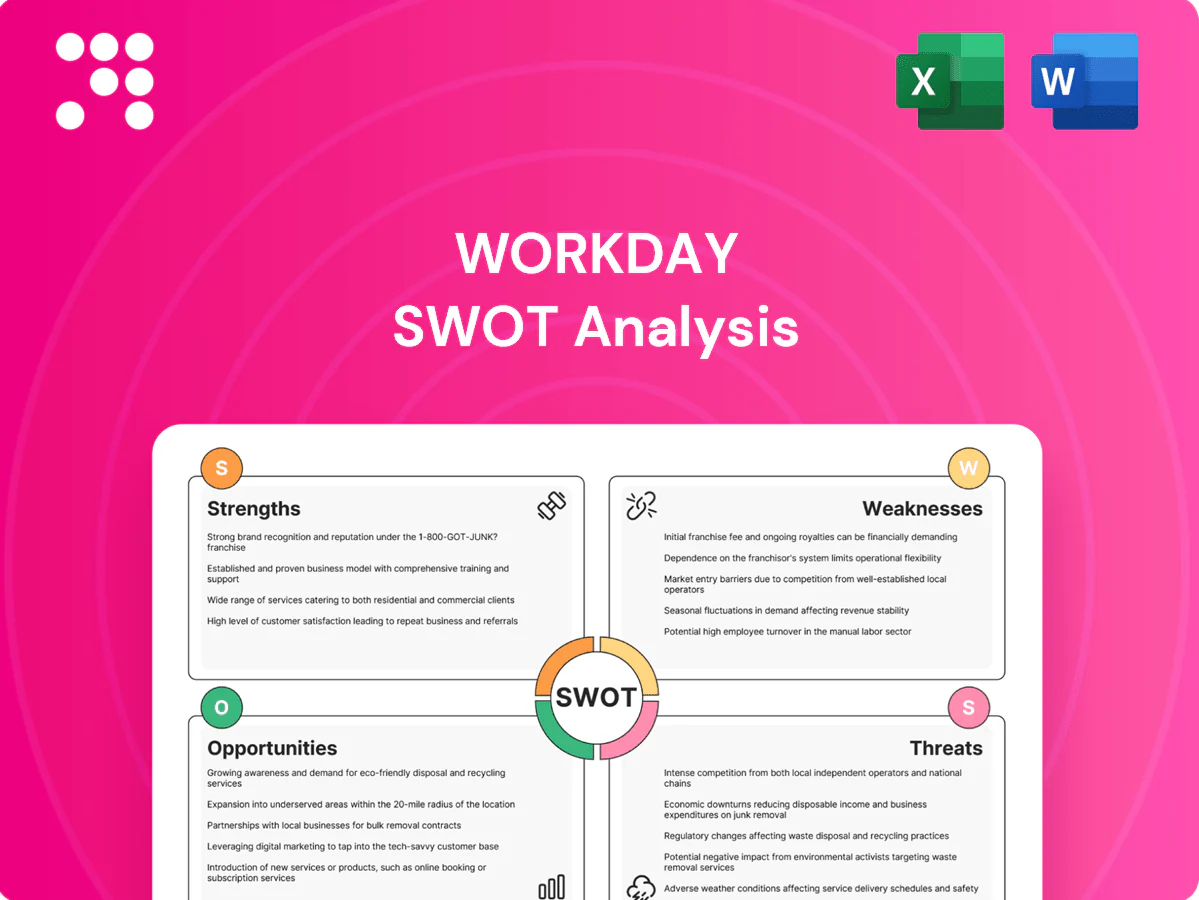

Strengths

Unified cloud platform

Workday delivers HCM, finance and analytics on a single cloud-native architecture, supporting $6.29 billion revenue in FY2025 and driving integrated customer adoption. A unified data model reduces silos and reconciliation effort, cutting close-rate and close-cycle friction for finance teams. This enables real-time visibility and consistent controls across processes. It differentiates Workday against fragmented legacy stacks.

Recurring SaaS revenue

Subscription contracts drive predictable cash flow and visibility, with subscriptions accounting for roughly 90% of Workday’s FY2024 revenue; multi-year deals and low churn enable confident expansion planning. Usage-based add-ons lift net retention, and the steady recurring base funds ongoing product and go-to-market investment.

Enterprise customer trust

Workday’s enterprise trust is reflected in over 8,800 customers worldwide as of 2024, signaling strong brand adoption among large and mid-sized enterprises. Referenceable wins in complex deployments across industries validate platform scalability, while SOC 1/2 and ISO 27001 certifications and >99.9% uptime reinforce credibility. These factors materially lower perceived risk for prospective buyers.

AI and analytics depth

Workday embeds machine learning across planning, skills inference and anomaly detection, with native analytics on unified tenant data that accelerates decision speed. Its continuous, cloud-delivered updates (biannual major releases plus interim patches) deliver new automations without customer upgrades, increasing platform value and efficiency over time.

- Biannual releases: continuous feature delivery

- Embedded ML: planning, skills, anomalies

- Unified analytics: faster decisions

- Compounding value: automated improvements

High switching costs

Workday's deep HR, payroll and finance workflows entrench customer processes, creating high switching costs; role-based configurations and proprietary data models are difficult to replicate. Integrations, deployment training and custom reports add exit friction, supporting pricing power and retention: Workday reports 97%+ subscription revenue retention and 10,000+ customers.

- Deep workflows

- 97%+ retention

- 10,000+ customers

- Pricing power

Cloud-native HCM & Finance platform: $6.29B revenue, >97% retention

Workday delivers HCM, finance and analytics on a single cloud-native architecture, supporting $6.29B revenue in FY2025 and ~90% subscription mix (FY2024). Unified data model, embedded ML, biannual releases and >97% subscription retention with ~10,000 customers create high switching costs, predictable cash flow and strong net retention.

| Metric | Value |

|---|---|

| Revenue FY2025 | $6.29B |

| Subscription mix FY2024 | ~90% |

| Customers (2024/25) | ~10,000 |

| Subscription retention | >97% |

| Certs / Uptime | SOC1/2, ISO27001, >99.9% uptime |

What is included in the product

Provides a strategic overview of Workday’s internal strengths and weaknesses and external opportunities and threats, mapping competitive position, growth drivers, operational gaps, and market risks to inform strategic decisions.

Delivers a concise, visual Workday SWOT matrix to quickly pinpoint HR and finance pain points and align remediation strategies across teams.

Weaknesses

Premium pricing

Workday’s premium pricing drives strong per-customer revenue but total cost can be prohibitive for cost-sensitive and smaller customers, pushing many to lower-priced competitors or modular point solutions.

Lengthy internal budget approvals in mid-market and public-sector deals commonly extend sales cycles, delaying bookings and reducing short-term growth predictability.

Aggressive discounting in competitive bids can compress margins; investors note subscription gross margin pressure when deals include heavy concessions in renewals and expansions.

High price points limit penetration in emerging markets where local payroll/HCM vendors offer comparable functionality at substantially lower local-currency prices.

Functional gaps vs full ERP

Workday’s manufacturing, supply-chain and complex shop-floor functionality remains less developed than ERP incumbents such as SAP and Oracle, leaving gaps for asset-intensive customers. Buyers often require complementary MES/SCM systems, increasing integration complexity and deal friction. This narrows TAM in heavy-asset verticals like discrete manufacturing. Workday FY2024 revenue was about $6.2 billion, driven mainly by HCM and financials.

Implementation complexity

Global HR/payroll and finance transformations with Workday commonly span 12–24 months, with data migration and change management often consuming 25–35% of project budgets, raising risk and cost. Outcomes depend heavily on systems integrator capability, producing wide ROI variance, and time-to-value frequently stretches to 12–18 months—deterring some prospects.

Enterprise concentration

Margin pressure from growth spend

Margin pressure from sustained R&D and go-to-market spending supports product leadership but compresses operating margins; cloud infrastructure costs rise with usage and can outpace revenue efficiency, while a higher-services mix (implementation, consulting) further dilutes gross margins and reported profitability; efficiency gains may lag rapid revenue growth.

- R&D and GTM intensity reduces operating margin

- Variable cloud costs scale with customer usage

- Services-heavy revenue dilutes SaaS gross margins

- Efficiency improvements may trail topline growth

Premium pricing and 12–24 month deployments limit SMBs; FY2024 $6.2B, ~70% Americas

Premium pricing and high implementation costs limit SMB and emerging-market adoption, pushing price-sensitive buyers to lower-cost local vendors.

Revenue concentration (FY2024 revenue ~$6.2B; ~70% Americas) and dependence on large renewals amplify quarter-to-quarter volatility and FX/compliance exposure.

Product gaps in manufacturing/SCM, lengthy 12–24 month transformations, and sustained R&D/GTM spend compress margins and slow net-new TAM expansion.

| Metric | Value |

|---|---|

| FY2024 revenue | $6.2B |

| Americas share | ~70% |

| Implementation timeline | 12–24 months |

| Project budget on data/change | 25–35% |

Preview the Actual Deliverable

Workday SWOT Analysis

This is the actual Workday SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full report and reflects the same structured, editable content included in your download. Purchase unlocks the complete, detailed version immediately after checkout.

Go Beyond the Preview—Access the Full Strategic Report

Explore Workday’s competitive advantages, innovation drivers, and risk profile in a concise SWOT snapshot that highlights strategic implications for investors and enterprise buyers. Want the full picture with data-backed recommendations and editable deliverables? Purchase the complete SWOT analysis to get the detailed Word report and Excel model you can use for planning, pitching, or investing.

Strengths

Unified cloud platform

Workday delivers HCM, finance and analytics on a single cloud-native architecture, supporting $6.29 billion revenue in FY2025 and driving integrated customer adoption. A unified data model reduces silos and reconciliation effort, cutting close-rate and close-cycle friction for finance teams. This enables real-time visibility and consistent controls across processes. It differentiates Workday against fragmented legacy stacks.

Recurring SaaS revenue

Subscription contracts drive predictable cash flow and visibility, with subscriptions accounting for roughly 90% of Workday’s FY2024 revenue; multi-year deals and low churn enable confident expansion planning. Usage-based add-ons lift net retention, and the steady recurring base funds ongoing product and go-to-market investment.

Enterprise customer trust

Workday’s enterprise trust is reflected in over 8,800 customers worldwide as of 2024, signaling strong brand adoption among large and mid-sized enterprises. Referenceable wins in complex deployments across industries validate platform scalability, while SOC 1/2 and ISO 27001 certifications and >99.9% uptime reinforce credibility. These factors materially lower perceived risk for prospective buyers.

AI and analytics depth

Workday embeds machine learning across planning, skills inference and anomaly detection, with native analytics on unified tenant data that accelerates decision speed. Its continuous, cloud-delivered updates (biannual major releases plus interim patches) deliver new automations without customer upgrades, increasing platform value and efficiency over time.

- Biannual releases: continuous feature delivery

- Embedded ML: planning, skills, anomalies

- Unified analytics: faster decisions

- Compounding value: automated improvements

High switching costs

Workday's deep HR, payroll and finance workflows entrench customer processes, creating high switching costs; role-based configurations and proprietary data models are difficult to replicate. Integrations, deployment training and custom reports add exit friction, supporting pricing power and retention: Workday reports 97%+ subscription revenue retention and 10,000+ customers.

- Deep workflows

- 97%+ retention

- 10,000+ customers

- Pricing power

Cloud-native HCM & Finance platform: $6.29B revenue, >97% retention

Workday delivers HCM, finance and analytics on a single cloud-native architecture, supporting $6.29B revenue in FY2025 and ~90% subscription mix (FY2024). Unified data model, embedded ML, biannual releases and >97% subscription retention with ~10,000 customers create high switching costs, predictable cash flow and strong net retention.

| Metric | Value |

|---|---|

| Revenue FY2025 | $6.29B |

| Subscription mix FY2024 | ~90% |

| Customers (2024/25) | ~10,000 |

| Subscription retention | >97% |

| Certs / Uptime | SOC1/2, ISO27001, >99.9% uptime |

What is included in the product

Provides a strategic overview of Workday’s internal strengths and weaknesses and external opportunities and threats, mapping competitive position, growth drivers, operational gaps, and market risks to inform strategic decisions.

Delivers a concise, visual Workday SWOT matrix to quickly pinpoint HR and finance pain points and align remediation strategies across teams.

Weaknesses

Premium pricing

Workday’s premium pricing drives strong per-customer revenue but total cost can be prohibitive for cost-sensitive and smaller customers, pushing many to lower-priced competitors or modular point solutions.

Lengthy internal budget approvals in mid-market and public-sector deals commonly extend sales cycles, delaying bookings and reducing short-term growth predictability.

Aggressive discounting in competitive bids can compress margins; investors note subscription gross margin pressure when deals include heavy concessions in renewals and expansions.

High price points limit penetration in emerging markets where local payroll/HCM vendors offer comparable functionality at substantially lower local-currency prices.

Functional gaps vs full ERP

Workday’s manufacturing, supply-chain and complex shop-floor functionality remains less developed than ERP incumbents such as SAP and Oracle, leaving gaps for asset-intensive customers. Buyers often require complementary MES/SCM systems, increasing integration complexity and deal friction. This narrows TAM in heavy-asset verticals like discrete manufacturing. Workday FY2024 revenue was about $6.2 billion, driven mainly by HCM and financials.

Implementation complexity

Global HR/payroll and finance transformations with Workday commonly span 12–24 months, with data migration and change management often consuming 25–35% of project budgets, raising risk and cost. Outcomes depend heavily on systems integrator capability, producing wide ROI variance, and time-to-value frequently stretches to 12–18 months—deterring some prospects.

Enterprise concentration

Margin pressure from growth spend

Margin pressure from sustained R&D and go-to-market spending supports product leadership but compresses operating margins; cloud infrastructure costs rise with usage and can outpace revenue efficiency, while a higher-services mix (implementation, consulting) further dilutes gross margins and reported profitability; efficiency gains may lag rapid revenue growth.

- R&D and GTM intensity reduces operating margin

- Variable cloud costs scale with customer usage

- Services-heavy revenue dilutes SaaS gross margins

- Efficiency improvements may trail topline growth

Premium pricing and 12–24 month deployments limit SMBs; FY2024 $6.2B, ~70% Americas

Premium pricing and high implementation costs limit SMB and emerging-market adoption, pushing price-sensitive buyers to lower-cost local vendors.

Revenue concentration (FY2024 revenue ~$6.2B; ~70% Americas) and dependence on large renewals amplify quarter-to-quarter volatility and FX/compliance exposure.

Product gaps in manufacturing/SCM, lengthy 12–24 month transformations, and sustained R&D/GTM spend compress margins and slow net-new TAM expansion.

| Metric | Value |

|---|---|

| FY2024 revenue | $6.2B |

| Americas share | ~70% |

| Implementation timeline | 12–24 months |

| Project budget on data/change | 25–35% |

Preview the Actual Deliverable

Workday SWOT Analysis

This is the actual Workday SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full report and reflects the same structured, editable content included in your download. Purchase unlocks the complete, detailed version immediately after checkout.

Original: $10.00

-65%$10.00

$3.50Description

Go Beyond the Preview—Access the Full Strategic Report

Explore Workday’s competitive advantages, innovation drivers, and risk profile in a concise SWOT snapshot that highlights strategic implications for investors and enterprise buyers. Want the full picture with data-backed recommendations and editable deliverables? Purchase the complete SWOT analysis to get the detailed Word report and Excel model you can use for planning, pitching, or investing.

Strengths

Unified cloud platform

Workday delivers HCM, finance and analytics on a single cloud-native architecture, supporting $6.29 billion revenue in FY2025 and driving integrated customer adoption. A unified data model reduces silos and reconciliation effort, cutting close-rate and close-cycle friction for finance teams. This enables real-time visibility and consistent controls across processes. It differentiates Workday against fragmented legacy stacks.

Recurring SaaS revenue

Subscription contracts drive predictable cash flow and visibility, with subscriptions accounting for roughly 90% of Workday’s FY2024 revenue; multi-year deals and low churn enable confident expansion planning. Usage-based add-ons lift net retention, and the steady recurring base funds ongoing product and go-to-market investment.

Enterprise customer trust

Workday’s enterprise trust is reflected in over 8,800 customers worldwide as of 2024, signaling strong brand adoption among large and mid-sized enterprises. Referenceable wins in complex deployments across industries validate platform scalability, while SOC 1/2 and ISO 27001 certifications and >99.9% uptime reinforce credibility. These factors materially lower perceived risk for prospective buyers.

AI and analytics depth

Workday embeds machine learning across planning, skills inference and anomaly detection, with native analytics on unified tenant data that accelerates decision speed. Its continuous, cloud-delivered updates (biannual major releases plus interim patches) deliver new automations without customer upgrades, increasing platform value and efficiency over time.

- Biannual releases: continuous feature delivery

- Embedded ML: planning, skills, anomalies

- Unified analytics: faster decisions

- Compounding value: automated improvements

High switching costs

Workday's deep HR, payroll and finance workflows entrench customer processes, creating high switching costs; role-based configurations and proprietary data models are difficult to replicate. Integrations, deployment training and custom reports add exit friction, supporting pricing power and retention: Workday reports 97%+ subscription revenue retention and 10,000+ customers.

- Deep workflows

- 97%+ retention

- 10,000+ customers

- Pricing power

Cloud-native HCM & Finance platform: $6.29B revenue, >97% retention

Workday delivers HCM, finance and analytics on a single cloud-native architecture, supporting $6.29B revenue in FY2025 and ~90% subscription mix (FY2024). Unified data model, embedded ML, biannual releases and >97% subscription retention with ~10,000 customers create high switching costs, predictable cash flow and strong net retention.

| Metric | Value |

|---|---|

| Revenue FY2025 | $6.29B |

| Subscription mix FY2024 | ~90% |

| Customers (2024/25) | ~10,000 |

| Subscription retention | >97% |

| Certs / Uptime | SOC1/2, ISO27001, >99.9% uptime |

What is included in the product

Provides a strategic overview of Workday’s internal strengths and weaknesses and external opportunities and threats, mapping competitive position, growth drivers, operational gaps, and market risks to inform strategic decisions.

Delivers a concise, visual Workday SWOT matrix to quickly pinpoint HR and finance pain points and align remediation strategies across teams.

Weaknesses

Premium pricing

Workday’s premium pricing drives strong per-customer revenue but total cost can be prohibitive for cost-sensitive and smaller customers, pushing many to lower-priced competitors or modular point solutions.

Lengthy internal budget approvals in mid-market and public-sector deals commonly extend sales cycles, delaying bookings and reducing short-term growth predictability.

Aggressive discounting in competitive bids can compress margins; investors note subscription gross margin pressure when deals include heavy concessions in renewals and expansions.

High price points limit penetration in emerging markets where local payroll/HCM vendors offer comparable functionality at substantially lower local-currency prices.

Functional gaps vs full ERP

Workday’s manufacturing, supply-chain and complex shop-floor functionality remains less developed than ERP incumbents such as SAP and Oracle, leaving gaps for asset-intensive customers. Buyers often require complementary MES/SCM systems, increasing integration complexity and deal friction. This narrows TAM in heavy-asset verticals like discrete manufacturing. Workday FY2024 revenue was about $6.2 billion, driven mainly by HCM and financials.

Implementation complexity

Global HR/payroll and finance transformations with Workday commonly span 12–24 months, with data migration and change management often consuming 25–35% of project budgets, raising risk and cost. Outcomes depend heavily on systems integrator capability, producing wide ROI variance, and time-to-value frequently stretches to 12–18 months—deterring some prospects.

Enterprise concentration

Margin pressure from growth spend

Margin pressure from sustained R&D and go-to-market spending supports product leadership but compresses operating margins; cloud infrastructure costs rise with usage and can outpace revenue efficiency, while a higher-services mix (implementation, consulting) further dilutes gross margins and reported profitability; efficiency gains may lag rapid revenue growth.

- R&D and GTM intensity reduces operating margin

- Variable cloud costs scale with customer usage

- Services-heavy revenue dilutes SaaS gross margins

- Efficiency improvements may trail topline growth

Premium pricing and 12–24 month deployments limit SMBs; FY2024 $6.2B, ~70% Americas

Premium pricing and high implementation costs limit SMB and emerging-market adoption, pushing price-sensitive buyers to lower-cost local vendors.

Revenue concentration (FY2024 revenue ~$6.2B; ~70% Americas) and dependence on large renewals amplify quarter-to-quarter volatility and FX/compliance exposure.

Product gaps in manufacturing/SCM, lengthy 12–24 month transformations, and sustained R&D/GTM spend compress margins and slow net-new TAM expansion.

| Metric | Value |

|---|---|

| FY2024 revenue | $6.2B |

| Americas share | ~70% |

| Implementation timeline | 12–24 months |

| Project budget on data/change | 25–35% |

Preview the Actual Deliverable

Workday SWOT Analysis

This is the actual Workday SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full report and reflects the same structured, editable content included in your download. Purchase unlocks the complete, detailed version immediately after checkout.