WPG Holdings Porter's Five Forces Analysis

Don't Miss the Bigger Picture

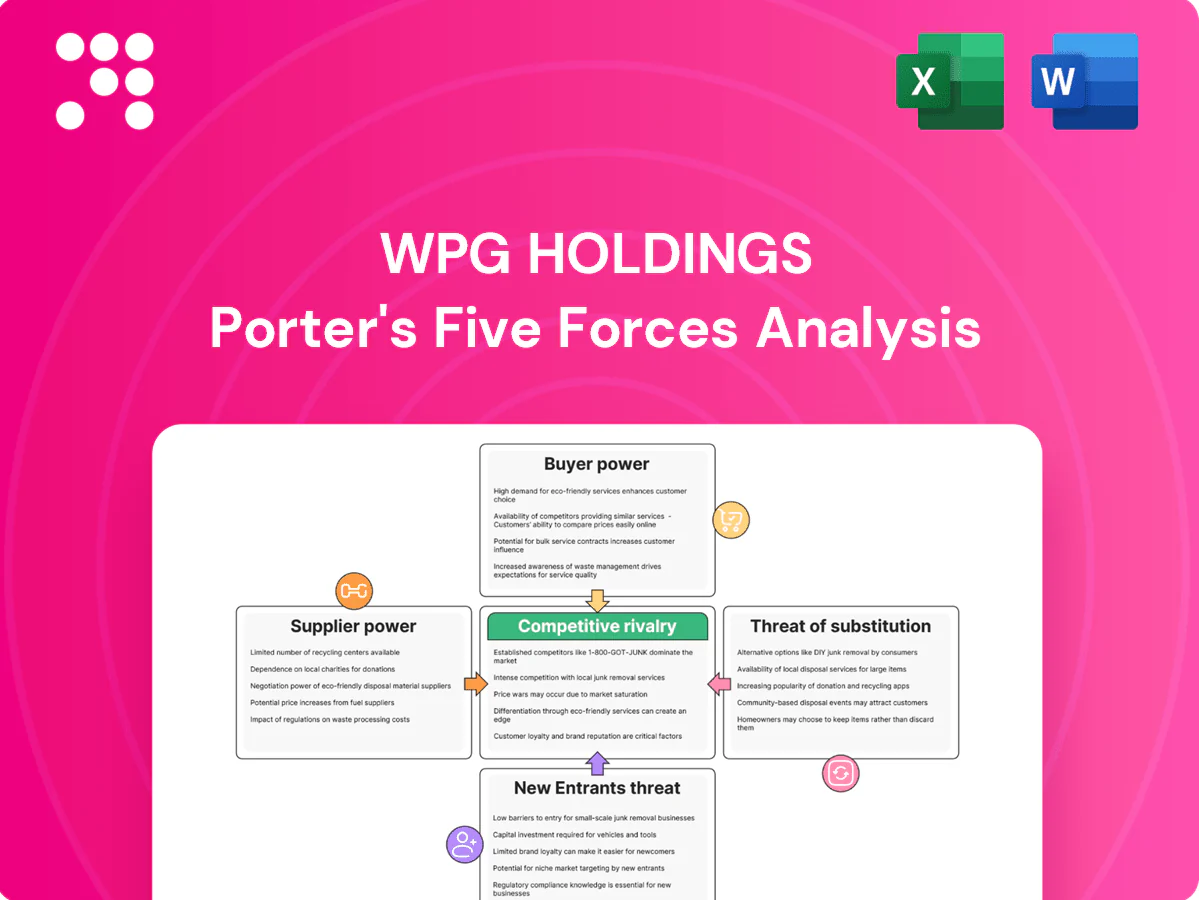

WPG Holdings faces moderate supplier power, intense buyer price sensitivity, and rising competitive rivalry as distributors and manufacturers consolidate, while threats from new entrants and substitutes remain manageable due to scale and broad product range. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore WPG Holdings’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentrated semiconductor principals

Concentrated upstream powerhouses—NXP, STMicro, Infineon, Samsung, Micron—retain strong leverage in 2024, collectively controlling over 50% of supply in key MCU/analog/memory/power IC segments, so allocation and regional franchise rules materially shape distributor margins and volumes. WPG must sustain top-tier performance to keep coveted lines, which limits its bargaining power, though its scale and Asia-Pacific channel reach secure firmer terms than smaller peers.

Design-in influence and preferred channeling

Suppliers steer demand via design-in programs and reference designs that lock customers to specific components, allowing principals to set distributor mix, pricing floors and inventory policies. WPG’s expanded technical support and FAE coverage in 2024 helped secure preferred-channel status with several vendors, partially mitigating supplier control. Nonetheless, vendor-driven roadmaps and lifecycle management preserved strong supplier bargaining power.

Capacity cycles and lead-time volatility

In tight cycles suppliers prioritize strategic OEMs and direct channels, tightening allocations to distributors like WPG and forcing hand-to-mouth purchasing. Elevated lead times have compelled WPG to hold higher inventories or forgo bookings, compressing margins and working-capital turns. In downcycles supplier bargaining eases but is offset by price erosion and inventory write-down risks, so cyclicality structurally reinforces supplier power.

Line card diversification vs. dependence

WPG’s broad line card reduces reliance on any single principal, giving the distributor greater negotiation flexibility and alternative sourcing across categories; however, high-revenue anchor lines still create concentration risk and vendor-specific terms that can constrain margins. Losing a top line would materially erode regional share and service breadth, and while diversification lowers supplier dependence it does not eliminate supplier leverage over pricing, lead times, or product allocation.

- Broad line card: improved bargaining flexibility

- Anchor lines: concentration risk and restrictive terms

- Loss impact: material revenue and service erosion

- Diversification: reduces but does not remove supplier leverage

Exclusive franchises and compliance demands

Franchise agreements force WPG to meet stringent quality, traceability, and brand-protection clauses that raise compliance overhead and constrain channel flexibility; suppliers’ exclusivity provisions can restrict WPG’s territorial and inventory decisions. Suppliers deploy scorecards and tight MDF/coop marketing controls to steer pricing and promotional cadence, reinforcing supplier leverage over margins and stocking norms.

- Scorecards: influence pricing/placement

- MDF/Coop: conditional marketing funds

- Exclusivity: limits territories/inventory

- Compliance: adds audit and quality costs

Suppliers control >50%, keeping bargaining power with producers

Concentrated principals control >50% of key MCU/analog/memory/power IC supply in 2024, limiting WPG’s bargaining despite its scale and expanded 2024 FAE/support that secured preferred status with several vendors. Supplier design-in, allocation and franchise clauses keep pricing, inventory and territory constraints in producers’ hands, sustaining strong supplier power through the cycle.

| Metric | 2024 |

|---|---|

| Share by top suppliers | >50% |

| WPG mitigation | Expanded FAE/support (2024) |

What is included in the product

Tailored Porter's Five Forces analysis for WPG Holdings highlighting competitive rivalry, supplier and buyer power, entry barriers, and substitutes, identifying disruptive threats and strategic levers to protect margins.

A one-sheet Porter's Five Forces summary tailored to WPG Holdings—clarifies supplier, buyer, and competitive pressures at a glance for faster strategic decisions. Clean, no-code layout ready to copy into pitch decks or duplicate for scenario comparisons.

Customers Bargaining Power

OEM/EMS consolidation and scale

Large OEMs and EMS consolidation concentrates purchasing power—top OEM/EMS customers account for over 50% of assembly demand—letting them extract steep discounts and SLA commitments. Their volumes enable multi-distributor sourcing and competitive bidding, squeezing distributor margins on core categories. WPG must defend share with value-added services, credit facilities and VMI to offset pricing pressure and customer concentration.

High price transparency and commoditization

Components often trade to transparent benchmarks and public broker quotes, enabling global buyers to compare offers in real time. As of 2024 buyers routinely cross-quote among distributors, compressing distributor gross margins by roughly 100–300 basis points. Catalog-like passives and commodity memory show thin differentiation, amplifying buyer power. WPG mitigates pressure through bundled services and program pricing to protect margin pools.

Switching costs via design and services

WPGs design-in support, reference designs and field application engineers create measurable partial switching costs, helping embed the distributor early in NPI to mass production. VMI/hub logistics, bonded inventory and extended credit terms deepen operational ties—WPG reported FY2024 revenue of about NT$1.0 trillion, reflecting scale that strengthens these services. This reduces buyer power where WPG is integrated, although common dual-sourcing policies limit full lock-in.

Demand volatility and forecast risk

Quality, traceability, and compliance expectations

Enterprise buyers demand rigorous QA, PPAP/IPC adherence and counterfeit avoidance, which raises WPG’s cost-to-serve but creates a service moat versus brokers; in 2024 heightened audit frequency has tightened contract terms and penalty clauses. Strong execution of traceability and compliance reduces churn and limits raw-price pressure from buyers.

- Higher QA/PPAP costs = stronger differentiation

- Audits/penalties shift contractual leverage to buyers

- Effective traceability lowers churn and price erosion

OEM/EMS >50% and real-time pricing squeeze margins 100–300 bps despite NT$1.0T

Large OEM/EMS concentration (top customers >50% assembly demand) and real-time price transparency compress margins ~100–300 bps; WPG FY2024 revenue ≈ NT$1.0 trillion supports VMI, credit and FAE-led design-in, reducing but not eliminating buyer leverage—inventory risk and flexible cancels still shift costs to distributors, rising buyer power in downturns.

| Metric | 2024 |

|---|---|

| Revenue | NT$1.0T |

| Margin compression | 100–300 bps |

| Top customers' share | >50% |

Preview the Actual Deliverable

WPG Holdings Porter's Five Forces Analysis

This preview shows the exact Porter's Five Forces analysis for WPG Holdings you'll receive immediately after purchase—no surprises or placeholders. The document is fully formatted and ready for download and use the moment you buy. It provides actionable insights on competitive rivalry, supplier and buyer power, and threats of entry and substitution. What you see is what you get.

Don't Miss the Bigger Picture

WPG Holdings faces moderate supplier power, intense buyer price sensitivity, and rising competitive rivalry as distributors and manufacturers consolidate, while threats from new entrants and substitutes remain manageable due to scale and broad product range. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore WPG Holdings’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentrated semiconductor principals

Concentrated upstream powerhouses—NXP, STMicro, Infineon, Samsung, Micron—retain strong leverage in 2024, collectively controlling over 50% of supply in key MCU/analog/memory/power IC segments, so allocation and regional franchise rules materially shape distributor margins and volumes. WPG must sustain top-tier performance to keep coveted lines, which limits its bargaining power, though its scale and Asia-Pacific channel reach secure firmer terms than smaller peers.

Design-in influence and preferred channeling

Suppliers steer demand via design-in programs and reference designs that lock customers to specific components, allowing principals to set distributor mix, pricing floors and inventory policies. WPG’s expanded technical support and FAE coverage in 2024 helped secure preferred-channel status with several vendors, partially mitigating supplier control. Nonetheless, vendor-driven roadmaps and lifecycle management preserved strong supplier bargaining power.

Capacity cycles and lead-time volatility

In tight cycles suppliers prioritize strategic OEMs and direct channels, tightening allocations to distributors like WPG and forcing hand-to-mouth purchasing. Elevated lead times have compelled WPG to hold higher inventories or forgo bookings, compressing margins and working-capital turns. In downcycles supplier bargaining eases but is offset by price erosion and inventory write-down risks, so cyclicality structurally reinforces supplier power.

Line card diversification vs. dependence

WPG’s broad line card reduces reliance on any single principal, giving the distributor greater negotiation flexibility and alternative sourcing across categories; however, high-revenue anchor lines still create concentration risk and vendor-specific terms that can constrain margins. Losing a top line would materially erode regional share and service breadth, and while diversification lowers supplier dependence it does not eliminate supplier leverage over pricing, lead times, or product allocation.

- Broad line card: improved bargaining flexibility

- Anchor lines: concentration risk and restrictive terms

- Loss impact: material revenue and service erosion

- Diversification: reduces but does not remove supplier leverage

Exclusive franchises and compliance demands

Franchise agreements force WPG to meet stringent quality, traceability, and brand-protection clauses that raise compliance overhead and constrain channel flexibility; suppliers’ exclusivity provisions can restrict WPG’s territorial and inventory decisions. Suppliers deploy scorecards and tight MDF/coop marketing controls to steer pricing and promotional cadence, reinforcing supplier leverage over margins and stocking norms.

- Scorecards: influence pricing/placement

- MDF/Coop: conditional marketing funds

- Exclusivity: limits territories/inventory

- Compliance: adds audit and quality costs

Suppliers control >50%, keeping bargaining power with producers

Concentrated principals control >50% of key MCU/analog/memory/power IC supply in 2024, limiting WPG’s bargaining despite its scale and expanded 2024 FAE/support that secured preferred status with several vendors. Supplier design-in, allocation and franchise clauses keep pricing, inventory and territory constraints in producers’ hands, sustaining strong supplier power through the cycle.

| Metric | 2024 |

|---|---|

| Share by top suppliers | >50% |

| WPG mitigation | Expanded FAE/support (2024) |

What is included in the product

Tailored Porter's Five Forces analysis for WPG Holdings highlighting competitive rivalry, supplier and buyer power, entry barriers, and substitutes, identifying disruptive threats and strategic levers to protect margins.

A one-sheet Porter's Five Forces summary tailored to WPG Holdings—clarifies supplier, buyer, and competitive pressures at a glance for faster strategic decisions. Clean, no-code layout ready to copy into pitch decks or duplicate for scenario comparisons.

Customers Bargaining Power

OEM/EMS consolidation and scale

Large OEMs and EMS consolidation concentrates purchasing power—top OEM/EMS customers account for over 50% of assembly demand—letting them extract steep discounts and SLA commitments. Their volumes enable multi-distributor sourcing and competitive bidding, squeezing distributor margins on core categories. WPG must defend share with value-added services, credit facilities and VMI to offset pricing pressure and customer concentration.

High price transparency and commoditization

Components often trade to transparent benchmarks and public broker quotes, enabling global buyers to compare offers in real time. As of 2024 buyers routinely cross-quote among distributors, compressing distributor gross margins by roughly 100–300 basis points. Catalog-like passives and commodity memory show thin differentiation, amplifying buyer power. WPG mitigates pressure through bundled services and program pricing to protect margin pools.

Switching costs via design and services

WPGs design-in support, reference designs and field application engineers create measurable partial switching costs, helping embed the distributor early in NPI to mass production. VMI/hub logistics, bonded inventory and extended credit terms deepen operational ties—WPG reported FY2024 revenue of about NT$1.0 trillion, reflecting scale that strengthens these services. This reduces buyer power where WPG is integrated, although common dual-sourcing policies limit full lock-in.

Demand volatility and forecast risk

Quality, traceability, and compliance expectations

Enterprise buyers demand rigorous QA, PPAP/IPC adherence and counterfeit avoidance, which raises WPG’s cost-to-serve but creates a service moat versus brokers; in 2024 heightened audit frequency has tightened contract terms and penalty clauses. Strong execution of traceability and compliance reduces churn and limits raw-price pressure from buyers.

- Higher QA/PPAP costs = stronger differentiation

- Audits/penalties shift contractual leverage to buyers

- Effective traceability lowers churn and price erosion

OEM/EMS >50% and real-time pricing squeeze margins 100–300 bps despite NT$1.0T

Large OEM/EMS concentration (top customers >50% assembly demand) and real-time price transparency compress margins ~100–300 bps; WPG FY2024 revenue ≈ NT$1.0 trillion supports VMI, credit and FAE-led design-in, reducing but not eliminating buyer leverage—inventory risk and flexible cancels still shift costs to distributors, rising buyer power in downturns.

| Metric | 2024 |

|---|---|

| Revenue | NT$1.0T |

| Margin compression | 100–300 bps |

| Top customers' share | >50% |

Preview the Actual Deliverable

WPG Holdings Porter's Five Forces Analysis

This preview shows the exact Porter's Five Forces analysis for WPG Holdings you'll receive immediately after purchase—no surprises or placeholders. The document is fully formatted and ready for download and use the moment you buy. It provides actionable insights on competitive rivalry, supplier and buyer power, and threats of entry and substitution. What you see is what you get.

Original: $10.00

-65%$10.00

$3.50Description

Don't Miss the Bigger Picture

WPG Holdings faces moderate supplier power, intense buyer price sensitivity, and rising competitive rivalry as distributors and manufacturers consolidate, while threats from new entrants and substitutes remain manageable due to scale and broad product range. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore WPG Holdings’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentrated semiconductor principals

Concentrated upstream powerhouses—NXP, STMicro, Infineon, Samsung, Micron—retain strong leverage in 2024, collectively controlling over 50% of supply in key MCU/analog/memory/power IC segments, so allocation and regional franchise rules materially shape distributor margins and volumes. WPG must sustain top-tier performance to keep coveted lines, which limits its bargaining power, though its scale and Asia-Pacific channel reach secure firmer terms than smaller peers.

Design-in influence and preferred channeling

Suppliers steer demand via design-in programs and reference designs that lock customers to specific components, allowing principals to set distributor mix, pricing floors and inventory policies. WPG’s expanded technical support and FAE coverage in 2024 helped secure preferred-channel status with several vendors, partially mitigating supplier control. Nonetheless, vendor-driven roadmaps and lifecycle management preserved strong supplier bargaining power.

Capacity cycles and lead-time volatility

In tight cycles suppliers prioritize strategic OEMs and direct channels, tightening allocations to distributors like WPG and forcing hand-to-mouth purchasing. Elevated lead times have compelled WPG to hold higher inventories or forgo bookings, compressing margins and working-capital turns. In downcycles supplier bargaining eases but is offset by price erosion and inventory write-down risks, so cyclicality structurally reinforces supplier power.

Line card diversification vs. dependence

WPG’s broad line card reduces reliance on any single principal, giving the distributor greater negotiation flexibility and alternative sourcing across categories; however, high-revenue anchor lines still create concentration risk and vendor-specific terms that can constrain margins. Losing a top line would materially erode regional share and service breadth, and while diversification lowers supplier dependence it does not eliminate supplier leverage over pricing, lead times, or product allocation.

- Broad line card: improved bargaining flexibility

- Anchor lines: concentration risk and restrictive terms

- Loss impact: material revenue and service erosion

- Diversification: reduces but does not remove supplier leverage

Exclusive franchises and compliance demands

Franchise agreements force WPG to meet stringent quality, traceability, and brand-protection clauses that raise compliance overhead and constrain channel flexibility; suppliers’ exclusivity provisions can restrict WPG’s territorial and inventory decisions. Suppliers deploy scorecards and tight MDF/coop marketing controls to steer pricing and promotional cadence, reinforcing supplier leverage over margins and stocking norms.

- Scorecards: influence pricing/placement

- MDF/Coop: conditional marketing funds

- Exclusivity: limits territories/inventory

- Compliance: adds audit and quality costs

Suppliers control >50%, keeping bargaining power with producers

Concentrated principals control >50% of key MCU/analog/memory/power IC supply in 2024, limiting WPG’s bargaining despite its scale and expanded 2024 FAE/support that secured preferred status with several vendors. Supplier design-in, allocation and franchise clauses keep pricing, inventory and territory constraints in producers’ hands, sustaining strong supplier power through the cycle.

| Metric | 2024 |

|---|---|

| Share by top suppliers | >50% |

| WPG mitigation | Expanded FAE/support (2024) |

What is included in the product

Tailored Porter's Five Forces analysis for WPG Holdings highlighting competitive rivalry, supplier and buyer power, entry barriers, and substitutes, identifying disruptive threats and strategic levers to protect margins.

A one-sheet Porter's Five Forces summary tailored to WPG Holdings—clarifies supplier, buyer, and competitive pressures at a glance for faster strategic decisions. Clean, no-code layout ready to copy into pitch decks or duplicate for scenario comparisons.

Customers Bargaining Power

OEM/EMS consolidation and scale

Large OEMs and EMS consolidation concentrates purchasing power—top OEM/EMS customers account for over 50% of assembly demand—letting them extract steep discounts and SLA commitments. Their volumes enable multi-distributor sourcing and competitive bidding, squeezing distributor margins on core categories. WPG must defend share with value-added services, credit facilities and VMI to offset pricing pressure and customer concentration.

High price transparency and commoditization

Components often trade to transparent benchmarks and public broker quotes, enabling global buyers to compare offers in real time. As of 2024 buyers routinely cross-quote among distributors, compressing distributor gross margins by roughly 100–300 basis points. Catalog-like passives and commodity memory show thin differentiation, amplifying buyer power. WPG mitigates pressure through bundled services and program pricing to protect margin pools.

Switching costs via design and services

WPGs design-in support, reference designs and field application engineers create measurable partial switching costs, helping embed the distributor early in NPI to mass production. VMI/hub logistics, bonded inventory and extended credit terms deepen operational ties—WPG reported FY2024 revenue of about NT$1.0 trillion, reflecting scale that strengthens these services. This reduces buyer power where WPG is integrated, although common dual-sourcing policies limit full lock-in.

Demand volatility and forecast risk

Quality, traceability, and compliance expectations

Enterprise buyers demand rigorous QA, PPAP/IPC adherence and counterfeit avoidance, which raises WPG’s cost-to-serve but creates a service moat versus brokers; in 2024 heightened audit frequency has tightened contract terms and penalty clauses. Strong execution of traceability and compliance reduces churn and limits raw-price pressure from buyers.

- Higher QA/PPAP costs = stronger differentiation

- Audits/penalties shift contractual leverage to buyers

- Effective traceability lowers churn and price erosion

OEM/EMS >50% and real-time pricing squeeze margins 100–300 bps despite NT$1.0T

Large OEM/EMS concentration (top customers >50% assembly demand) and real-time price transparency compress margins ~100–300 bps; WPG FY2024 revenue ≈ NT$1.0 trillion supports VMI, credit and FAE-led design-in, reducing but not eliminating buyer leverage—inventory risk and flexible cancels still shift costs to distributors, rising buyer power in downturns.

| Metric | 2024 |

|---|---|

| Revenue | NT$1.0T |

| Margin compression | 100–300 bps |

| Top customers' share | >50% |

Preview the Actual Deliverable

WPG Holdings Porter's Five Forces Analysis

This preview shows the exact Porter's Five Forces analysis for WPG Holdings you'll receive immediately after purchase—no surprises or placeholders. The document is fully formatted and ready for download and use the moment you buy. It provides actionable insights on competitive rivalry, supplier and buyer power, and threats of entry and substitution. What you see is what you get.