WPP Porter's Five Forces Analysis

Don't Miss the Bigger Picture

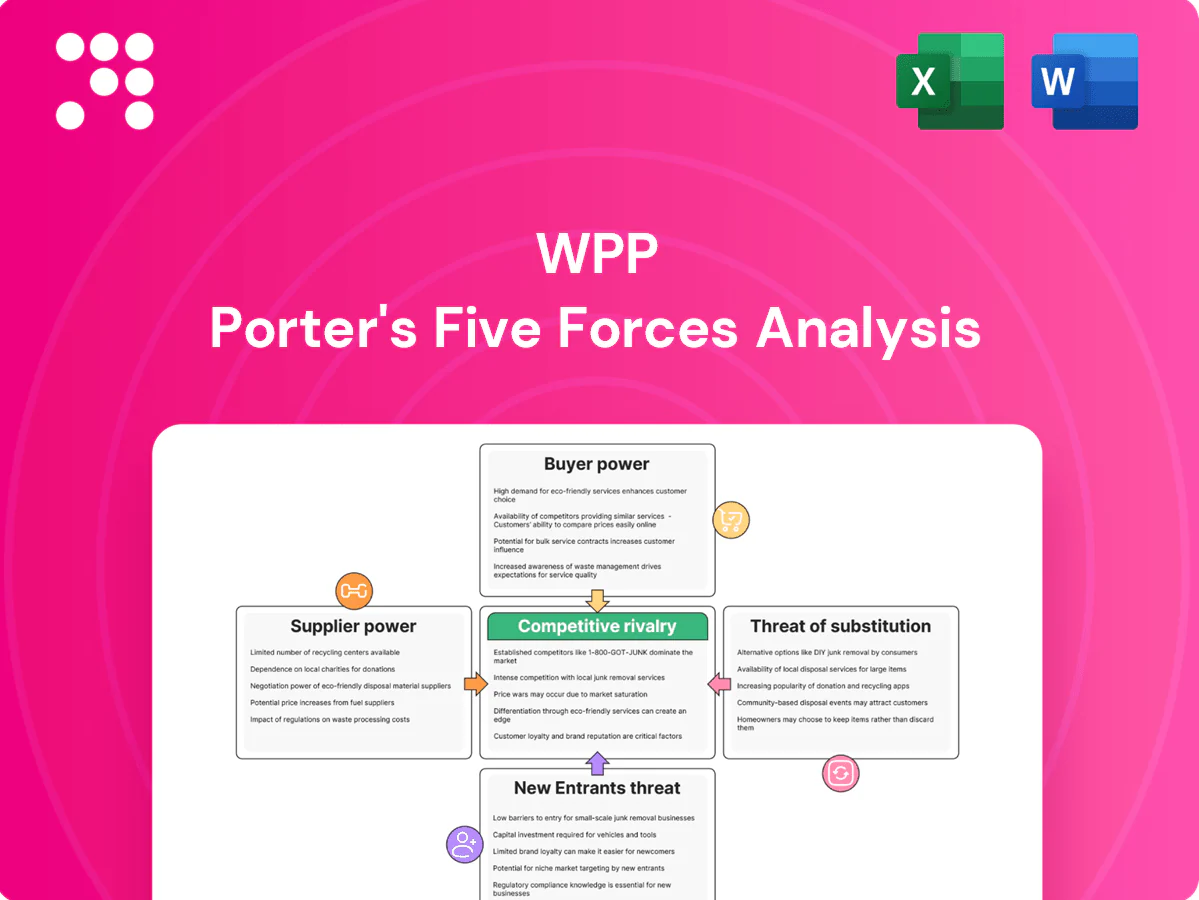

WPP's Porter's Five Forces snapshot highlights moderate buyer power, fragmenting supplier dynamics, high competitive rivalry, low threat of substitutes, and barriers limiting new entrants. This brief sketches strategic pressures and growth levers. Unlock the full Porter's Five Forces Analysis to explore WPP’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Scarce top creative talent

Elite creatives, strategists and data scientists are scarce and highly mobile, driving wage inflation and retention costs; WPP’s global workforce of roughly 100,000 concentrates star talent in flagship agencies, increasing supplier leverage during key pitches. Their personal brands can command premiums and sway client loyalty, raising churn risk. WPP must invest in culture, pay and defined career paths to lock in talent and mitigate pitch-time bargaining power.

Dominant media & tech platforms

Google and Meta captured roughly 55% of global digital ad spend in 2024, while Amazon (≈12%) and TikTok (≈8%) own growing inventory and Apple controls iOS measurement rails via ATT and SKAdNetwork. Sudden API, privacy or pricing changes can rapidly shift campaign economics and attribution. Limited viable alternatives elevate platform bargaining power. WPP counters with multi-platform planning and first-party data solutions to retain negotiating leverage.

Specialist data & SaaS dependencies

Adtech, martech and measurement vendors (DSPs, CDPs, MMM tools) are deeply embedded in WPP workflows, with programmatic buying accounting for roughly 80% of digital display spend, creating high switching costs via contracts and integrations. The martech landscape grew to about 10,000 solutions in 2024, and vendor consolidation or unique capabilities can drive fee inflation. Building proprietary stacks can materially reduce this supplier leverage.

Production studios and niche partners

High-quality production houses, influencers and niche content partners hold significant leverage over WPP when premium creative is required, becoming bottlenecks for flagship campaigns.

Peak demand windows drive higher rates and longer lead times, while exclusivity around formats or creators further amplifies supplier power.

WPP’s preferred networks and in-house studios, including global production arms, help rebalance terms and reduce dependency.

- suppliers: production houses, influencers, niche partners

- drivers: peak demand, exclusivity

- mitigants: in-house studios, preferred networks

Regulatory data gatekeepers

Privacy regulators and standards bodies function as data suppliers for WPP, with GDPR enforcement creating material constraints (EU cumulative fines exceeded €2.3bn by 2024) and cookie deprecation timelines from major browsers shifting addressability and raising bid costs. Consent frameworks and technical controls increase operational complexity and compliance spend, while close policy engagement and privacy-by-design systems preserve targeting options and reduce regulatory disruption risk.

- Regulatory fines: EU GDPR >€2.3bn (through 2024)

- Consent rates: ~57% average in EU (IAB trends)

- Tech shift: Chrome cookie phase timeline extended into 2024–25

- Mitigation: privacy-by-design + policy engagement

Talent scarcity, platform concentration and programmatic dominance raise costs and supplier leverage

Scarce elite talent (WPP ~100,000) drives wage inflation and retention costs, increasing supplier leverage at pitch-time. Google+Meta held ~55% of global digital ad spend in 2024 (Amazon ~12%, TikTok ~8%), concentrating platform power. Programmatic ~80% of display spend and ~10,000 martech vendors raise switching costs; GDPR fines >€2.3bn through 2024 add regulatory supplier constraints.

| Supplier | 2024 metric |

|---|---|

| Talent | WPP workforce ~100,000 |

| Platforms | Google+Meta ~55% share; Amazon ~12%; TikTok ~8% |

| Adtech | Programmatic ~80% display; ~10,000 vendors |

| Regulatory | GDPR fines >€2.3bn |

What is included in the product

Tailored Porter's Five Forces analysis for WPP that uncovers key drivers of competition, buyer and supplier power, and market entry barriers; identifies disruptive substitutes and emerging threats to market share, and provides strategic commentary to inform pricing, profitability and defensive growth strategies.

A concise one-sheet Porter's Five Forces for WPP that highlights supplier, buyer, rivalry, substitutes and new entrant pressures—ready to paste into decks; customize scores and scenarios to model impacts of digital ad shifts, client consolidation and regulatory change.

Customers Bargaining Power

Global blue-chip clients

Global blue-chip clients wield strong bargaining power: large multinationals control sizable budgets (P&G spends over 7bn USD on media annually) and run competitive RFPs demanding integrated services, rate cards and performance guarantees. Consolidation of scopes across media, creative and commerce further increases their leverage. WPP counters with its scale, integrated offerings and growing outcome-linked commercial models tied to KPIs.

Low switching costs across agencies

Low switching costs across agencies mean capabilities are increasingly commoditized, with industry client tenure around 4 years (2024) facilitating rotation. Procurement-led reviews push fees and tighter payment terms, squeezing margins during renegotiations. Knowledge transfer and staff movement reduce client stickiness over time. WPP counters by building lock-in through data platforms (Xaxis), proprietary stacks and embedded teams; WPP reported group revenue ~£12.8bn in 2024.

In-housing marketing capabilities

Clients are building internal studios, media buying and analytics pods—Forrester 2024 reports 48% of advertisers now operate in-house teams—reducing external spend and strengthening negotiating positions. Hybrid models let clients cherry-pick agency services, pressuring fees and scope. WPP responds by shifting to consultative, specialist and upstream strategy roles to retain higher-value work. This elevates client bargaining power while reshaping agency margins.

Performance and ROI accountability

Buyers push for measurable outcomes and variable compensation, driving transparent reporting and MMM/MTA fee scrutiny; underperforming campaigns trigger rapid reallocations while WPP reported 2024 revenue of £12.9bn and increased investment in measurement, retail media and AI to defend pricing and margins.

- Buyers: ROI-first, variable fees

- Measurement: MMM/MTA increases fee scrutiny

- WPP 2024: £12.9bn revenue, ramped AI/retail media spend

Demand for end-to-end integration

Clients increasingly demand seamless creative, media, PR, commerce and data under one roof, which can raise average deal size but also strengthens buyers’ leverage to negotiate bundled discounts; WPP reported group revenue of £12.9bn in 2024 as it pushed integrated offerings. Multi-market briefs amplify pressure for rate harmonization across regions, while WPP’s network model seeks scale efficiencies to protect margins.

- Integrated demand increases deal size yet fuels bundled discounting

- Multi-market scope → higher pressure on rate harmonization

- WPP 2024 revenue: £12.9bn — network model targets scale to defend margins

Buyers Gain Leverage as In-Housing Hits 48%; Agencies Face Margin Pressure

Large global clients (eg P&G >7bn USD media spend) and rising in-housing (Forrester 2024: 48%) give buyers strong leverage; low switching costs and ~4-year client tenure (2024) increase churn. Procurement-driven RFPs push variable fees and tighter terms, squeezing agency margins. WPP defends via scale, integrated stacks and outcome-linked models (WPP 2024 revenue £12.9bn).

| Metric | 2024 |

|---|---|

| WPP revenue | £12.9bn |

| P&G media spend | >$7bn |

| Advertisers in-house | 48% |

| Avg client tenure | 4 yrs |

Full Version Awaits

WPP Porter's Five Forces Analysis

This preview is the exact WPP Porter's Five Forces Analysis you'll receive after purchase—no placeholders or samples. The file shown is fully formatted and ready for immediate download and use. Once you complete your purchase, you’ll get instant access to this same document.

Don't Miss the Bigger Picture

WPP's Porter's Five Forces snapshot highlights moderate buyer power, fragmenting supplier dynamics, high competitive rivalry, low threat of substitutes, and barriers limiting new entrants. This brief sketches strategic pressures and growth levers. Unlock the full Porter's Five Forces Analysis to explore WPP’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Scarce top creative talent

Elite creatives, strategists and data scientists are scarce and highly mobile, driving wage inflation and retention costs; WPP’s global workforce of roughly 100,000 concentrates star talent in flagship agencies, increasing supplier leverage during key pitches. Their personal brands can command premiums and sway client loyalty, raising churn risk. WPP must invest in culture, pay and defined career paths to lock in talent and mitigate pitch-time bargaining power.

Dominant media & tech platforms

Google and Meta captured roughly 55% of global digital ad spend in 2024, while Amazon (≈12%) and TikTok (≈8%) own growing inventory and Apple controls iOS measurement rails via ATT and SKAdNetwork. Sudden API, privacy or pricing changes can rapidly shift campaign economics and attribution. Limited viable alternatives elevate platform bargaining power. WPP counters with multi-platform planning and first-party data solutions to retain negotiating leverage.

Specialist data & SaaS dependencies

Adtech, martech and measurement vendors (DSPs, CDPs, MMM tools) are deeply embedded in WPP workflows, with programmatic buying accounting for roughly 80% of digital display spend, creating high switching costs via contracts and integrations. The martech landscape grew to about 10,000 solutions in 2024, and vendor consolidation or unique capabilities can drive fee inflation. Building proprietary stacks can materially reduce this supplier leverage.

Production studios and niche partners

High-quality production houses, influencers and niche content partners hold significant leverage over WPP when premium creative is required, becoming bottlenecks for flagship campaigns.

Peak demand windows drive higher rates and longer lead times, while exclusivity around formats or creators further amplifies supplier power.

WPP’s preferred networks and in-house studios, including global production arms, help rebalance terms and reduce dependency.

- suppliers: production houses, influencers, niche partners

- drivers: peak demand, exclusivity

- mitigants: in-house studios, preferred networks

Regulatory data gatekeepers

Privacy regulators and standards bodies function as data suppliers for WPP, with GDPR enforcement creating material constraints (EU cumulative fines exceeded €2.3bn by 2024) and cookie deprecation timelines from major browsers shifting addressability and raising bid costs. Consent frameworks and technical controls increase operational complexity and compliance spend, while close policy engagement and privacy-by-design systems preserve targeting options and reduce regulatory disruption risk.

- Regulatory fines: EU GDPR >€2.3bn (through 2024)

- Consent rates: ~57% average in EU (IAB trends)

- Tech shift: Chrome cookie phase timeline extended into 2024–25

- Mitigation: privacy-by-design + policy engagement

Talent scarcity, platform concentration and programmatic dominance raise costs and supplier leverage

Scarce elite talent (WPP ~100,000) drives wage inflation and retention costs, increasing supplier leverage at pitch-time. Google+Meta held ~55% of global digital ad spend in 2024 (Amazon ~12%, TikTok ~8%), concentrating platform power. Programmatic ~80% of display spend and ~10,000 martech vendors raise switching costs; GDPR fines >€2.3bn through 2024 add regulatory supplier constraints.

| Supplier | 2024 metric |

|---|---|

| Talent | WPP workforce ~100,000 |

| Platforms | Google+Meta ~55% share; Amazon ~12%; TikTok ~8% |

| Adtech | Programmatic ~80% display; ~10,000 vendors |

| Regulatory | GDPR fines >€2.3bn |

What is included in the product

Tailored Porter's Five Forces analysis for WPP that uncovers key drivers of competition, buyer and supplier power, and market entry barriers; identifies disruptive substitutes and emerging threats to market share, and provides strategic commentary to inform pricing, profitability and defensive growth strategies.

A concise one-sheet Porter's Five Forces for WPP that highlights supplier, buyer, rivalry, substitutes and new entrant pressures—ready to paste into decks; customize scores and scenarios to model impacts of digital ad shifts, client consolidation and regulatory change.

Customers Bargaining Power

Global blue-chip clients

Global blue-chip clients wield strong bargaining power: large multinationals control sizable budgets (P&G spends over 7bn USD on media annually) and run competitive RFPs demanding integrated services, rate cards and performance guarantees. Consolidation of scopes across media, creative and commerce further increases their leverage. WPP counters with its scale, integrated offerings and growing outcome-linked commercial models tied to KPIs.

Low switching costs across agencies

Low switching costs across agencies mean capabilities are increasingly commoditized, with industry client tenure around 4 years (2024) facilitating rotation. Procurement-led reviews push fees and tighter payment terms, squeezing margins during renegotiations. Knowledge transfer and staff movement reduce client stickiness over time. WPP counters by building lock-in through data platforms (Xaxis), proprietary stacks and embedded teams; WPP reported group revenue ~£12.8bn in 2024.

In-housing marketing capabilities

Clients are building internal studios, media buying and analytics pods—Forrester 2024 reports 48% of advertisers now operate in-house teams—reducing external spend and strengthening negotiating positions. Hybrid models let clients cherry-pick agency services, pressuring fees and scope. WPP responds by shifting to consultative, specialist and upstream strategy roles to retain higher-value work. This elevates client bargaining power while reshaping agency margins.

Performance and ROI accountability

Buyers push for measurable outcomes and variable compensation, driving transparent reporting and MMM/MTA fee scrutiny; underperforming campaigns trigger rapid reallocations while WPP reported 2024 revenue of £12.9bn and increased investment in measurement, retail media and AI to defend pricing and margins.

- Buyers: ROI-first, variable fees

- Measurement: MMM/MTA increases fee scrutiny

- WPP 2024: £12.9bn revenue, ramped AI/retail media spend

Demand for end-to-end integration

Clients increasingly demand seamless creative, media, PR, commerce and data under one roof, which can raise average deal size but also strengthens buyers’ leverage to negotiate bundled discounts; WPP reported group revenue of £12.9bn in 2024 as it pushed integrated offerings. Multi-market briefs amplify pressure for rate harmonization across regions, while WPP’s network model seeks scale efficiencies to protect margins.

- Integrated demand increases deal size yet fuels bundled discounting

- Multi-market scope → higher pressure on rate harmonization

- WPP 2024 revenue: £12.9bn — network model targets scale to defend margins

Buyers Gain Leverage as In-Housing Hits 48%; Agencies Face Margin Pressure

Large global clients (eg P&G >7bn USD media spend) and rising in-housing (Forrester 2024: 48%) give buyers strong leverage; low switching costs and ~4-year client tenure (2024) increase churn. Procurement-driven RFPs push variable fees and tighter terms, squeezing agency margins. WPP defends via scale, integrated stacks and outcome-linked models (WPP 2024 revenue £12.9bn).

| Metric | 2024 |

|---|---|

| WPP revenue | £12.9bn |

| P&G media spend | >$7bn |

| Advertisers in-house | 48% |

| Avg client tenure | 4 yrs |

Full Version Awaits

WPP Porter's Five Forces Analysis

This preview is the exact WPP Porter's Five Forces Analysis you'll receive after purchase—no placeholders or samples. The file shown is fully formatted and ready for immediate download and use. Once you complete your purchase, you’ll get instant access to this same document.

Original: $10.00

-65%$10.00

$3.50Description

Don't Miss the Bigger Picture

WPP's Porter's Five Forces snapshot highlights moderate buyer power, fragmenting supplier dynamics, high competitive rivalry, low threat of substitutes, and barriers limiting new entrants. This brief sketches strategic pressures and growth levers. Unlock the full Porter's Five Forces Analysis to explore WPP’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Scarce top creative talent

Elite creatives, strategists and data scientists are scarce and highly mobile, driving wage inflation and retention costs; WPP’s global workforce of roughly 100,000 concentrates star talent in flagship agencies, increasing supplier leverage during key pitches. Their personal brands can command premiums and sway client loyalty, raising churn risk. WPP must invest in culture, pay and defined career paths to lock in talent and mitigate pitch-time bargaining power.

Dominant media & tech platforms

Google and Meta captured roughly 55% of global digital ad spend in 2024, while Amazon (≈12%) and TikTok (≈8%) own growing inventory and Apple controls iOS measurement rails via ATT and SKAdNetwork. Sudden API, privacy or pricing changes can rapidly shift campaign economics and attribution. Limited viable alternatives elevate platform bargaining power. WPP counters with multi-platform planning and first-party data solutions to retain negotiating leverage.

Specialist data & SaaS dependencies

Adtech, martech and measurement vendors (DSPs, CDPs, MMM tools) are deeply embedded in WPP workflows, with programmatic buying accounting for roughly 80% of digital display spend, creating high switching costs via contracts and integrations. The martech landscape grew to about 10,000 solutions in 2024, and vendor consolidation or unique capabilities can drive fee inflation. Building proprietary stacks can materially reduce this supplier leverage.

Production studios and niche partners

High-quality production houses, influencers and niche content partners hold significant leverage over WPP when premium creative is required, becoming bottlenecks for flagship campaigns.

Peak demand windows drive higher rates and longer lead times, while exclusivity around formats or creators further amplifies supplier power.

WPP’s preferred networks and in-house studios, including global production arms, help rebalance terms and reduce dependency.

- suppliers: production houses, influencers, niche partners

- drivers: peak demand, exclusivity

- mitigants: in-house studios, preferred networks

Regulatory data gatekeepers

Privacy regulators and standards bodies function as data suppliers for WPP, with GDPR enforcement creating material constraints (EU cumulative fines exceeded €2.3bn by 2024) and cookie deprecation timelines from major browsers shifting addressability and raising bid costs. Consent frameworks and technical controls increase operational complexity and compliance spend, while close policy engagement and privacy-by-design systems preserve targeting options and reduce regulatory disruption risk.

- Regulatory fines: EU GDPR >€2.3bn (through 2024)

- Consent rates: ~57% average in EU (IAB trends)

- Tech shift: Chrome cookie phase timeline extended into 2024–25

- Mitigation: privacy-by-design + policy engagement

Talent scarcity, platform concentration and programmatic dominance raise costs and supplier leverage

Scarce elite talent (WPP ~100,000) drives wage inflation and retention costs, increasing supplier leverage at pitch-time. Google+Meta held ~55% of global digital ad spend in 2024 (Amazon ~12%, TikTok ~8%), concentrating platform power. Programmatic ~80% of display spend and ~10,000 martech vendors raise switching costs; GDPR fines >€2.3bn through 2024 add regulatory supplier constraints.

| Supplier | 2024 metric |

|---|---|

| Talent | WPP workforce ~100,000 |

| Platforms | Google+Meta ~55% share; Amazon ~12%; TikTok ~8% |

| Adtech | Programmatic ~80% display; ~10,000 vendors |

| Regulatory | GDPR fines >€2.3bn |

What is included in the product

Tailored Porter's Five Forces analysis for WPP that uncovers key drivers of competition, buyer and supplier power, and market entry barriers; identifies disruptive substitutes and emerging threats to market share, and provides strategic commentary to inform pricing, profitability and defensive growth strategies.

A concise one-sheet Porter's Five Forces for WPP that highlights supplier, buyer, rivalry, substitutes and new entrant pressures—ready to paste into decks; customize scores and scenarios to model impacts of digital ad shifts, client consolidation and regulatory change.

Customers Bargaining Power

Global blue-chip clients

Global blue-chip clients wield strong bargaining power: large multinationals control sizable budgets (P&G spends over 7bn USD on media annually) and run competitive RFPs demanding integrated services, rate cards and performance guarantees. Consolidation of scopes across media, creative and commerce further increases their leverage. WPP counters with its scale, integrated offerings and growing outcome-linked commercial models tied to KPIs.

Low switching costs across agencies

Low switching costs across agencies mean capabilities are increasingly commoditized, with industry client tenure around 4 years (2024) facilitating rotation. Procurement-led reviews push fees and tighter payment terms, squeezing margins during renegotiations. Knowledge transfer and staff movement reduce client stickiness over time. WPP counters by building lock-in through data platforms (Xaxis), proprietary stacks and embedded teams; WPP reported group revenue ~£12.8bn in 2024.

In-housing marketing capabilities

Clients are building internal studios, media buying and analytics pods—Forrester 2024 reports 48% of advertisers now operate in-house teams—reducing external spend and strengthening negotiating positions. Hybrid models let clients cherry-pick agency services, pressuring fees and scope. WPP responds by shifting to consultative, specialist and upstream strategy roles to retain higher-value work. This elevates client bargaining power while reshaping agency margins.

Performance and ROI accountability

Buyers push for measurable outcomes and variable compensation, driving transparent reporting and MMM/MTA fee scrutiny; underperforming campaigns trigger rapid reallocations while WPP reported 2024 revenue of £12.9bn and increased investment in measurement, retail media and AI to defend pricing and margins.

- Buyers: ROI-first, variable fees

- Measurement: MMM/MTA increases fee scrutiny

- WPP 2024: £12.9bn revenue, ramped AI/retail media spend

Demand for end-to-end integration

Clients increasingly demand seamless creative, media, PR, commerce and data under one roof, which can raise average deal size but also strengthens buyers’ leverage to negotiate bundled discounts; WPP reported group revenue of £12.9bn in 2024 as it pushed integrated offerings. Multi-market briefs amplify pressure for rate harmonization across regions, while WPP’s network model seeks scale efficiencies to protect margins.

- Integrated demand increases deal size yet fuels bundled discounting

- Multi-market scope → higher pressure on rate harmonization

- WPP 2024 revenue: £12.9bn — network model targets scale to defend margins

Buyers Gain Leverage as In-Housing Hits 48%; Agencies Face Margin Pressure

Large global clients (eg P&G >7bn USD media spend) and rising in-housing (Forrester 2024: 48%) give buyers strong leverage; low switching costs and ~4-year client tenure (2024) increase churn. Procurement-driven RFPs push variable fees and tighter terms, squeezing agency margins. WPP defends via scale, integrated stacks and outcome-linked models (WPP 2024 revenue £12.9bn).

| Metric | 2024 |

|---|---|

| WPP revenue | £12.9bn |

| P&G media spend | >$7bn |

| Advertisers in-house | 48% |

| Avg client tenure | 4 yrs |

Full Version Awaits

WPP Porter's Five Forces Analysis

This preview is the exact WPP Porter's Five Forces Analysis you'll receive after purchase—no placeholders or samples. The file shown is fully formatted and ready for immediate download and use. Once you complete your purchase, you’ll get instant access to this same document.