WT Microelectronics PESTLE Analysis

Plan Smarter. Present Sharper. Compete Stronger.

Stay ahead with our targeted PESTLE Analysis for WT Microelectronics—three concise sections reveal how politics, economics, and technology will shape the firm's trajectory. Ideal for investors and strategists, this report turns external trends into actionable moves. Purchase the full analysis to access the complete, editable insights and make smarter decisions today.

Political factors

US–China export controls

US and allied export controls since 2022 restrict advanced semiconductors and related equipment—notably targeting chips at 14 nm and below—shaping what WT can legally distribute and to whom. Compliance has curtailed high-margin flows to PRC customers and pushed volume toward other Asian markets. Ongoing policy updates force agile product-mix decisions and stricter customer vetting, as missteps invite heavy penalties and supplier-relationship strain.

Taiwan Strait geopolitics

Heightened Taiwan Strait tensions raise supply-chain and insurance risk for WT, with Taiwan accounting for roughly 60% of global foundry capacity and TSMC holding ~50%+ of foundry share in 2024, prompting customers to diversify sourcing. Insurers and brokers reported Asia-Pacific freight and war-risk premiums up ~25% 2021–2024, pushing suppliers toward multi-location inventory. WT must reinforce contingency logistics, regional hubs and dual-sourcing to limit disruptions. Crisis scenarios could spike distribution delays and financing costs within weeks.

Industrial policy subsidies

US CHIPS Act channels about 52.7 billion USD and the EU Chips Act aims to mobilize roughly 43 billion EUR by 2030, while Asian subsidies and tax incentives have similarly expanded local fabs and design hubs. These policy-driven programs create regional demand nodes for components and support services. WT can embed in grant-backed projects to secure early supply-chain positions. Localization may force local entity build-outs and compliance overheads.

Tariffs and trade agreements

- 75% USMCA rule-of-origin

- RCEP ≈30% global GDP

- Duty optimization = margin lift

- Customs expertise = client lock-in

- Tariff shocks → order pull-ins

Political stability in key hubs

Political stability in Taiwan, Singapore, Korea, Japan and ASEAN underpins operational continuity; Taiwan hosts TSMC with ~55% global foundry share in 2024, ASEAN drew about $160B FDI in 2023, and elections can shift labor, tax and import regimes. WT leverages diversified warehousing, bonded zones and government partnerships to ease permits and speed expansions.

- Stability impact on continuity

- Election-driven policy risk

- Diversified warehouses & bonded zones

- Government partnerships accelerate permits

Export curbs and CHIPS funds reshape chips; Taiwan foundry dominance, Strait risk raise costs

Export controls since 2022 limit 14 nm+ shipments, cutting PRC high-margin sales; CHIPS Act $52.7B and EU €43B spur regional demand. Taiwan/TSMC (~50–55% foundry share 2024) and Strait tensions raise insurance/freight premiums ~+25% (2021–24). Tariff/FTA shifts (USMCA 75% rule, RCEP ≈30% GDP) force routing, localization and customs-service monetization.

| Metric | Value |

|---|---|

| CHIPS Act | $52.7B |

| EU Chips | €43B |

| TSMC foundry share 2024 | 50–55% |

| APAC war-risk premium rise | ~+25% (2021–24) |

| RCEP share | ≈30% world GDP |

What is included in the product

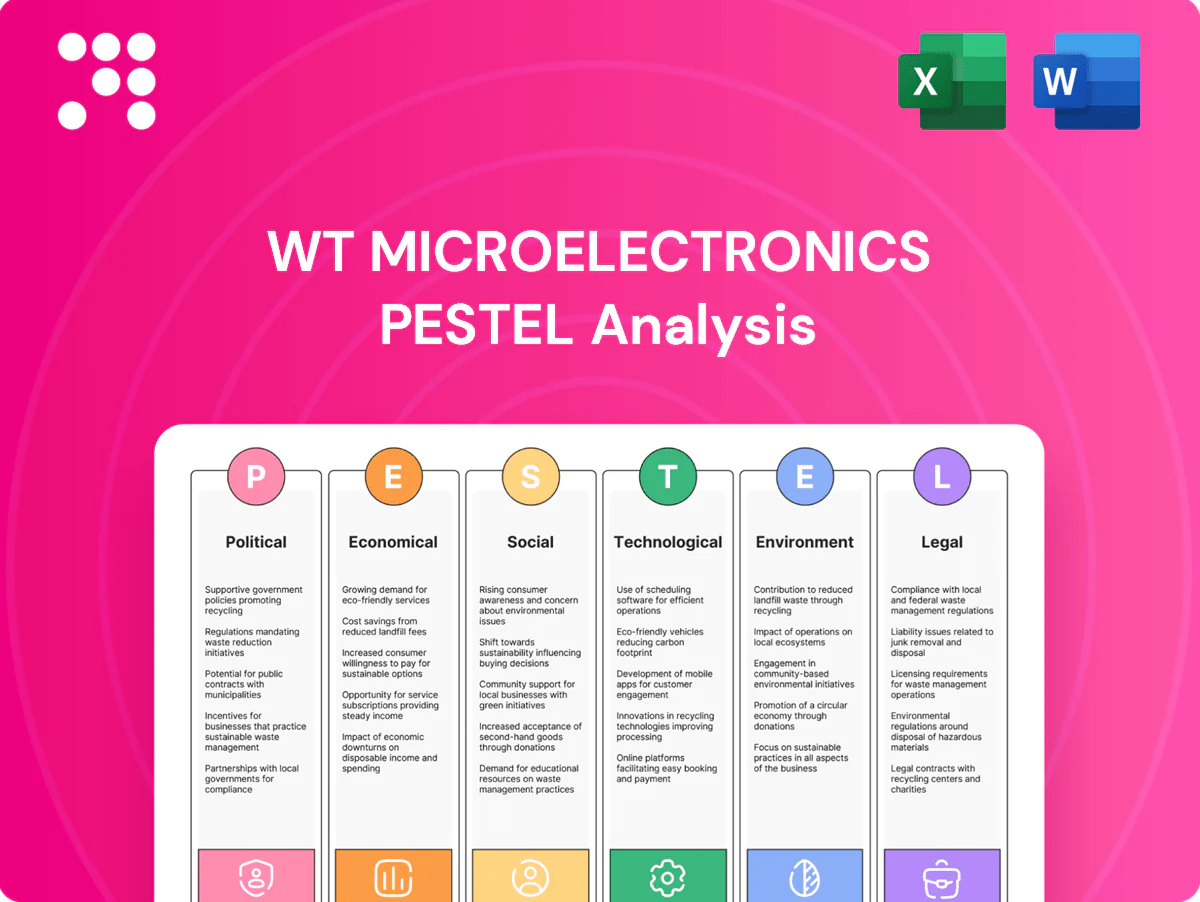

Explores how external macro-environmental factors uniquely affect WT Microelectronics across six dimensions—Political, Economic, Social, Technological, Environmental, and Legal—providing data-backed trends and forward-looking insights to inform strategy, investor communications, and scenario planning.

A concise, visually segmented PESTLE summary of WT Microelectronics that eases meeting prep and cross-team alignment, allows quick annotation for regional or product-specific risks, and drops straight into presentations or strategy packs.

Economic factors

Semiconductor cycle

The semiconductor market is highly cyclical; global chip sales were $556.8 billion in 2023 (WSTS) and experienced sharp inventory corrections after PC, smartphone and server booms. AI accelerators and automotive chips have grown share, cushioning troughs but not removing volatility. WT must tightly balance inventory risk versus service levels. Forecast accuracy and supplier allocation access directly drive margin and profitability.

Currency exposure

Revenue and procurement span USD, TWD, CNY, JPY and EUR, exposing WT Microelectronics to multi-currency risk that compressed gross margins during 2023–2024 FX turbulence. FX swings, notably JPY and CNY moves, materially affect pricing competitiveness and required pass-through in customer contracts. Robust hedging policies and natural offsets (local sourcing vs sales) are critical to protect margins.

Logistics and freight costs

Air and ocean rates remain highly sensitive to fuel prices and capacity swings; Red Sea reroutes in 2023–24 added up to 3,000 nautical miles on some voyages, lengthening transit and raising spot costs. Port congestion and blank sailings further extend lead times, increasing inventory carrying costs. WT’s multi-carrier contracts and near-shore stocking dampen rate volatility and shorten response times. Efficient logistics therefore protects gross margins.

Interest rates and credit

WT Microelectronics faces high working-capital intensity with inventory ~90–120 days and receivables ~60–75 days; US policy rates around 5.25–5.50% mid-2025 raise borrowing costs and tighten customer credit, increasing liquidity strain. Robust credit underwriting and insured receivables (up to ~80% coverage) reduce bad-debt risk, while supplier financing programs that extend payables 60–90 days can preserve cash-conversion cycles.

- Working capital: inventory 90–120 days, DSO 60–75 days

- Financing cost: policy rate ~5.25–5.50% (mid-2025)

- Credit risk mitigation: insured receivables ~80% coverage

- Supplier finance: extend payables 60–90 days

End-market mix

End-market mix spans AI servers, EVs, industrial automation and IoT, each with distinct demand curves; global EV sales reached about 14 million in 2023, while rising AI/data-center spend and IoT deployments underpin diversified semiconductor demand. Diversification reduces reliance on consumer electronics and WT's design-win pipeline provides medium-term revenue visibility, enabling portfolio tilt toward structurally growing segments.

- Design-wins = medium-term revenue visibility

- EVs ~14m global sales (2023)

- IoT and AI: structural double-digit growth

Export curbs and CHIPS funds reshape chips; Taiwan foundry dominance, Strait risk raise costs

WT faces cyclical semiconductor demand (global chip sales $556.8B in 2023) with AI and automotive moderating but not eliminating volatility; inventory management and forecast accuracy directly drive margins. Multi-currency exposure (USD, TWD, CNY, JPY, EUR) and mid-2025 policy rates ~5.25–5.50% compress margins and raise financing costs. High working-capital (inv 90–120d, DSO 60–75d) and logistics volatility increase cash strain; hedging, insured receivables and supplier finance are essential.

| Metric | Value |

|---|---|

| Global chip sales 2023 | $556.8B (WSTS) |

| Policy rate (mid‑2025) | ~5.25–5.50% |

| Inventory | 90–120 days |

| DSO | 60–75 days |

Full Version Awaits

WT Microelectronics PESTLE Analysis

The WT Microelectronics PESTLE Analysis provides a concise, professionally structured review of political, economic, social, technological, legal and environmental factors affecting the company. The preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use. No placeholders or teasers; this is the final file available for immediate download.

Plan Smarter. Present Sharper. Compete Stronger.

Stay ahead with our targeted PESTLE Analysis for WT Microelectronics—three concise sections reveal how politics, economics, and technology will shape the firm's trajectory. Ideal for investors and strategists, this report turns external trends into actionable moves. Purchase the full analysis to access the complete, editable insights and make smarter decisions today.

Political factors

US–China export controls

US and allied export controls since 2022 restrict advanced semiconductors and related equipment—notably targeting chips at 14 nm and below—shaping what WT can legally distribute and to whom. Compliance has curtailed high-margin flows to PRC customers and pushed volume toward other Asian markets. Ongoing policy updates force agile product-mix decisions and stricter customer vetting, as missteps invite heavy penalties and supplier-relationship strain.

Taiwan Strait geopolitics

Heightened Taiwan Strait tensions raise supply-chain and insurance risk for WT, with Taiwan accounting for roughly 60% of global foundry capacity and TSMC holding ~50%+ of foundry share in 2024, prompting customers to diversify sourcing. Insurers and brokers reported Asia-Pacific freight and war-risk premiums up ~25% 2021–2024, pushing suppliers toward multi-location inventory. WT must reinforce contingency logistics, regional hubs and dual-sourcing to limit disruptions. Crisis scenarios could spike distribution delays and financing costs within weeks.

Industrial policy subsidies

US CHIPS Act channels about 52.7 billion USD and the EU Chips Act aims to mobilize roughly 43 billion EUR by 2030, while Asian subsidies and tax incentives have similarly expanded local fabs and design hubs. These policy-driven programs create regional demand nodes for components and support services. WT can embed in grant-backed projects to secure early supply-chain positions. Localization may force local entity build-outs and compliance overheads.

Tariffs and trade agreements

- 75% USMCA rule-of-origin

- RCEP ≈30% global GDP

- Duty optimization = margin lift

- Customs expertise = client lock-in

- Tariff shocks → order pull-ins

Political stability in key hubs

Political stability in Taiwan, Singapore, Korea, Japan and ASEAN underpins operational continuity; Taiwan hosts TSMC with ~55% global foundry share in 2024, ASEAN drew about $160B FDI in 2023, and elections can shift labor, tax and import regimes. WT leverages diversified warehousing, bonded zones and government partnerships to ease permits and speed expansions.

- Stability impact on continuity

- Election-driven policy risk

- Diversified warehouses & bonded zones

- Government partnerships accelerate permits

Export curbs and CHIPS funds reshape chips; Taiwan foundry dominance, Strait risk raise costs

Export controls since 2022 limit 14 nm+ shipments, cutting PRC high-margin sales; CHIPS Act $52.7B and EU €43B spur regional demand. Taiwan/TSMC (~50–55% foundry share 2024) and Strait tensions raise insurance/freight premiums ~+25% (2021–24). Tariff/FTA shifts (USMCA 75% rule, RCEP ≈30% GDP) force routing, localization and customs-service monetization.

| Metric | Value |

|---|---|

| CHIPS Act | $52.7B |

| EU Chips | €43B |

| TSMC foundry share 2024 | 50–55% |

| APAC war-risk premium rise | ~+25% (2021–24) |

| RCEP share | ≈30% world GDP |

What is included in the product

Explores how external macro-environmental factors uniquely affect WT Microelectronics across six dimensions—Political, Economic, Social, Technological, Environmental, and Legal—providing data-backed trends and forward-looking insights to inform strategy, investor communications, and scenario planning.

A concise, visually segmented PESTLE summary of WT Microelectronics that eases meeting prep and cross-team alignment, allows quick annotation for regional or product-specific risks, and drops straight into presentations or strategy packs.

Economic factors

Semiconductor cycle

The semiconductor market is highly cyclical; global chip sales were $556.8 billion in 2023 (WSTS) and experienced sharp inventory corrections after PC, smartphone and server booms. AI accelerators and automotive chips have grown share, cushioning troughs but not removing volatility. WT must tightly balance inventory risk versus service levels. Forecast accuracy and supplier allocation access directly drive margin and profitability.

Currency exposure

Revenue and procurement span USD, TWD, CNY, JPY and EUR, exposing WT Microelectronics to multi-currency risk that compressed gross margins during 2023–2024 FX turbulence. FX swings, notably JPY and CNY moves, materially affect pricing competitiveness and required pass-through in customer contracts. Robust hedging policies and natural offsets (local sourcing vs sales) are critical to protect margins.

Logistics and freight costs

Air and ocean rates remain highly sensitive to fuel prices and capacity swings; Red Sea reroutes in 2023–24 added up to 3,000 nautical miles on some voyages, lengthening transit and raising spot costs. Port congestion and blank sailings further extend lead times, increasing inventory carrying costs. WT’s multi-carrier contracts and near-shore stocking dampen rate volatility and shorten response times. Efficient logistics therefore protects gross margins.

Interest rates and credit

WT Microelectronics faces high working-capital intensity with inventory ~90–120 days and receivables ~60–75 days; US policy rates around 5.25–5.50% mid-2025 raise borrowing costs and tighten customer credit, increasing liquidity strain. Robust credit underwriting and insured receivables (up to ~80% coverage) reduce bad-debt risk, while supplier financing programs that extend payables 60–90 days can preserve cash-conversion cycles.

- Working capital: inventory 90–120 days, DSO 60–75 days

- Financing cost: policy rate ~5.25–5.50% (mid-2025)

- Credit risk mitigation: insured receivables ~80% coverage

- Supplier finance: extend payables 60–90 days

End-market mix

End-market mix spans AI servers, EVs, industrial automation and IoT, each with distinct demand curves; global EV sales reached about 14 million in 2023, while rising AI/data-center spend and IoT deployments underpin diversified semiconductor demand. Diversification reduces reliance on consumer electronics and WT's design-win pipeline provides medium-term revenue visibility, enabling portfolio tilt toward structurally growing segments.

- Design-wins = medium-term revenue visibility

- EVs ~14m global sales (2023)

- IoT and AI: structural double-digit growth

Export curbs and CHIPS funds reshape chips; Taiwan foundry dominance, Strait risk raise costs

WT faces cyclical semiconductor demand (global chip sales $556.8B in 2023) with AI and automotive moderating but not eliminating volatility; inventory management and forecast accuracy directly drive margins. Multi-currency exposure (USD, TWD, CNY, JPY, EUR) and mid-2025 policy rates ~5.25–5.50% compress margins and raise financing costs. High working-capital (inv 90–120d, DSO 60–75d) and logistics volatility increase cash strain; hedging, insured receivables and supplier finance are essential.

| Metric | Value |

|---|---|

| Global chip sales 2023 | $556.8B (WSTS) |

| Policy rate (mid‑2025) | ~5.25–5.50% |

| Inventory | 90–120 days |

| DSO | 60–75 days |

Full Version Awaits

WT Microelectronics PESTLE Analysis

The WT Microelectronics PESTLE Analysis provides a concise, professionally structured review of political, economic, social, technological, legal and environmental factors affecting the company. The preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use. No placeholders or teasers; this is the final file available for immediate download.

Original: $10.00

-65%$10.00

$3.50Description

Plan Smarter. Present Sharper. Compete Stronger.

Stay ahead with our targeted PESTLE Analysis for WT Microelectronics—three concise sections reveal how politics, economics, and technology will shape the firm's trajectory. Ideal for investors and strategists, this report turns external trends into actionable moves. Purchase the full analysis to access the complete, editable insights and make smarter decisions today.

Political factors

US–China export controls

US and allied export controls since 2022 restrict advanced semiconductors and related equipment—notably targeting chips at 14 nm and below—shaping what WT can legally distribute and to whom. Compliance has curtailed high-margin flows to PRC customers and pushed volume toward other Asian markets. Ongoing policy updates force agile product-mix decisions and stricter customer vetting, as missteps invite heavy penalties and supplier-relationship strain.

Taiwan Strait geopolitics

Heightened Taiwan Strait tensions raise supply-chain and insurance risk for WT, with Taiwan accounting for roughly 60% of global foundry capacity and TSMC holding ~50%+ of foundry share in 2024, prompting customers to diversify sourcing. Insurers and brokers reported Asia-Pacific freight and war-risk premiums up ~25% 2021–2024, pushing suppliers toward multi-location inventory. WT must reinforce contingency logistics, regional hubs and dual-sourcing to limit disruptions. Crisis scenarios could spike distribution delays and financing costs within weeks.

Industrial policy subsidies

US CHIPS Act channels about 52.7 billion USD and the EU Chips Act aims to mobilize roughly 43 billion EUR by 2030, while Asian subsidies and tax incentives have similarly expanded local fabs and design hubs. These policy-driven programs create regional demand nodes for components and support services. WT can embed in grant-backed projects to secure early supply-chain positions. Localization may force local entity build-outs and compliance overheads.

Tariffs and trade agreements

- 75% USMCA rule-of-origin

- RCEP ≈30% global GDP

- Duty optimization = margin lift

- Customs expertise = client lock-in

- Tariff shocks → order pull-ins

Political stability in key hubs

Political stability in Taiwan, Singapore, Korea, Japan and ASEAN underpins operational continuity; Taiwan hosts TSMC with ~55% global foundry share in 2024, ASEAN drew about $160B FDI in 2023, and elections can shift labor, tax and import regimes. WT leverages diversified warehousing, bonded zones and government partnerships to ease permits and speed expansions.

- Stability impact on continuity

- Election-driven policy risk

- Diversified warehouses & bonded zones

- Government partnerships accelerate permits

Export curbs and CHIPS funds reshape chips; Taiwan foundry dominance, Strait risk raise costs

Export controls since 2022 limit 14 nm+ shipments, cutting PRC high-margin sales; CHIPS Act $52.7B and EU €43B spur regional demand. Taiwan/TSMC (~50–55% foundry share 2024) and Strait tensions raise insurance/freight premiums ~+25% (2021–24). Tariff/FTA shifts (USMCA 75% rule, RCEP ≈30% GDP) force routing, localization and customs-service monetization.

| Metric | Value |

|---|---|

| CHIPS Act | $52.7B |

| EU Chips | €43B |

| TSMC foundry share 2024 | 50–55% |

| APAC war-risk premium rise | ~+25% (2021–24) |

| RCEP share | ≈30% world GDP |

What is included in the product

Explores how external macro-environmental factors uniquely affect WT Microelectronics across six dimensions—Political, Economic, Social, Technological, Environmental, and Legal—providing data-backed trends and forward-looking insights to inform strategy, investor communications, and scenario planning.

A concise, visually segmented PESTLE summary of WT Microelectronics that eases meeting prep and cross-team alignment, allows quick annotation for regional or product-specific risks, and drops straight into presentations or strategy packs.

Economic factors

Semiconductor cycle

The semiconductor market is highly cyclical; global chip sales were $556.8 billion in 2023 (WSTS) and experienced sharp inventory corrections after PC, smartphone and server booms. AI accelerators and automotive chips have grown share, cushioning troughs but not removing volatility. WT must tightly balance inventory risk versus service levels. Forecast accuracy and supplier allocation access directly drive margin and profitability.

Currency exposure

Revenue and procurement span USD, TWD, CNY, JPY and EUR, exposing WT Microelectronics to multi-currency risk that compressed gross margins during 2023–2024 FX turbulence. FX swings, notably JPY and CNY moves, materially affect pricing competitiveness and required pass-through in customer contracts. Robust hedging policies and natural offsets (local sourcing vs sales) are critical to protect margins.

Logistics and freight costs

Air and ocean rates remain highly sensitive to fuel prices and capacity swings; Red Sea reroutes in 2023–24 added up to 3,000 nautical miles on some voyages, lengthening transit and raising spot costs. Port congestion and blank sailings further extend lead times, increasing inventory carrying costs. WT’s multi-carrier contracts and near-shore stocking dampen rate volatility and shorten response times. Efficient logistics therefore protects gross margins.

Interest rates and credit

WT Microelectronics faces high working-capital intensity with inventory ~90–120 days and receivables ~60–75 days; US policy rates around 5.25–5.50% mid-2025 raise borrowing costs and tighten customer credit, increasing liquidity strain. Robust credit underwriting and insured receivables (up to ~80% coverage) reduce bad-debt risk, while supplier financing programs that extend payables 60–90 days can preserve cash-conversion cycles.

- Working capital: inventory 90–120 days, DSO 60–75 days

- Financing cost: policy rate ~5.25–5.50% (mid-2025)

- Credit risk mitigation: insured receivables ~80% coverage

- Supplier finance: extend payables 60–90 days

End-market mix

End-market mix spans AI servers, EVs, industrial automation and IoT, each with distinct demand curves; global EV sales reached about 14 million in 2023, while rising AI/data-center spend and IoT deployments underpin diversified semiconductor demand. Diversification reduces reliance on consumer electronics and WT's design-win pipeline provides medium-term revenue visibility, enabling portfolio tilt toward structurally growing segments.

- Design-wins = medium-term revenue visibility

- EVs ~14m global sales (2023)

- IoT and AI: structural double-digit growth

Export curbs and CHIPS funds reshape chips; Taiwan foundry dominance, Strait risk raise costs

WT faces cyclical semiconductor demand (global chip sales $556.8B in 2023) with AI and automotive moderating but not eliminating volatility; inventory management and forecast accuracy directly drive margins. Multi-currency exposure (USD, TWD, CNY, JPY, EUR) and mid-2025 policy rates ~5.25–5.50% compress margins and raise financing costs. High working-capital (inv 90–120d, DSO 60–75d) and logistics volatility increase cash strain; hedging, insured receivables and supplier finance are essential.

| Metric | Value |

|---|---|

| Global chip sales 2023 | $556.8B (WSTS) |

| Policy rate (mid‑2025) | ~5.25–5.50% |

| Inventory | 90–120 days |

| DSO | 60–75 days |

Full Version Awaits

WT Microelectronics PESTLE Analysis

The WT Microelectronics PESTLE Analysis provides a concise, professionally structured review of political, economic, social, technological, legal and environmental factors affecting the company. The preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use. No placeholders or teasers; this is the final file available for immediate download.