Wuxi Apptec PESTLE Analysis

Skip the Research. Get the Strategy.

Gain strategic clarity with our concise PESTLE Analysis of Wuxi AppTec—highlighting regulatory risks, economic drivers, and technological advances shaping its growth trajectory. Ideal for investors and strategists who need actionable external insights fast. Buy the full analysis to access deep-dive findings, scenario impacts, and ready-to-use recommendations for confident decision-making.

Political factors

US–China geopolitics

Heightened US–China geopolitics, underscored by expanded US export controls on sensitive biotechnologies in 2023–24, raises scrutiny of China-based biomanufacturing partners and could restrict cross-border biotech collaboration and data sharing. Clients may accelerate geographic diversification of CDMO/CRO sourcing, pressuring order flow. Wuxi AppTec’s proactive global footprint and compliance diplomacy remain key mitigants.

Export controls and sanctions

US and allied export controls on advanced biotech and dual-use tools have tightened, constraining imports of certain equipment and services and affecting operations that serve more than 50 countries with sanctions regimes.

Sanctions increase counterparty screening burdens and regulatory complexity, driving compliance costs and lead times higher for CRO/CDMO firms like Wuxi AppTec.

Building alternative supplier networks and regional sourcing has become a strategic mitigation to preserve supply continuity and customer service.

Healthcare industrial policy

China, the US and the EU have stepped up industrial healthcare policy—China's biopharma market exceeded $150 billion in 2023—driving subsidies and grants (combined US/EU national biomanufacturing support programs exceed $20 billion since 2020) that lower capex hurdles but foster local competitors. WuXi AppTec can capture incentive-driven demand yet must comply with in-country-for-country mandates and adapt site strategy rapidly as policy shifts alter allocation of clinical and commercial manufacturing volumes.

Drug pricing and reimbursement politics

Global cost‑containment debates—with the US/EU accounting for roughly 40–45% of global pharma spend—pressure sponsors to trim R&D budgets and reprioritize pipelines; price pressure can slow late‑stage programs yet boosts demand for outsourcing as sponsors seek 10–20% cost savings via CRO/CDMO partnerships. Stable public funding for priority diseases (e.g., oncology, vaccines) sustains demand; scenario planning aligns Wuxi AppTec capacity to 3–5 year policy cycles.

- Policy pressure → smaller late‑stage portfolios

- Outsourcing demand up for cost reduction

- Priority disease funding provides stable revenue

- Scenario planning matches capacity to 3–5y policy cycles

Trade tariffs and customs

Tariffs on lab consumables, chemicals and equipment can raise Wuxi AppTec's input costs, with trade measures historically reaching up to 25% on affected goods; this compresses margins on low-value, high-volume items. Customs delays complicate sample and material flows, increasing lead times and working capital needs. Bonded logistics and localized inventories reduce disruption risk, and contracts increasingly include pass-through clauses for tariff shocks.

- Tariff exposure: up to 25%

- Customs risk: higher lead times, greater working capital

- Mitigation: bonded warehouses, local inventory

- Contracting: pass-through tariff clauses

US–China biotech tensions push firms to diversify CDMO/CROs, raising compliance and costs

Heightened US–China biotech tensions and 2023–24 US export controls raise scrutiny of China-based CDMO/CRO partners, prompting client diversification and higher compliance costs. China’s biopharma market exceeded $150B in 2023 while US/EU biomanufacturing support >$20B since 2020, boosting regional competition. Tariffs up to 25% and customs delays raise input costs and working capital needs; bonded logistics and pass-through clauses mitigate risk.

| Metric | Value |

|---|---|

| China biopharma 2023 | $150B+ |

| US/EU support since 2020 | $20B+ |

| Tariff exposure | Up to 25% |

What is included in the product

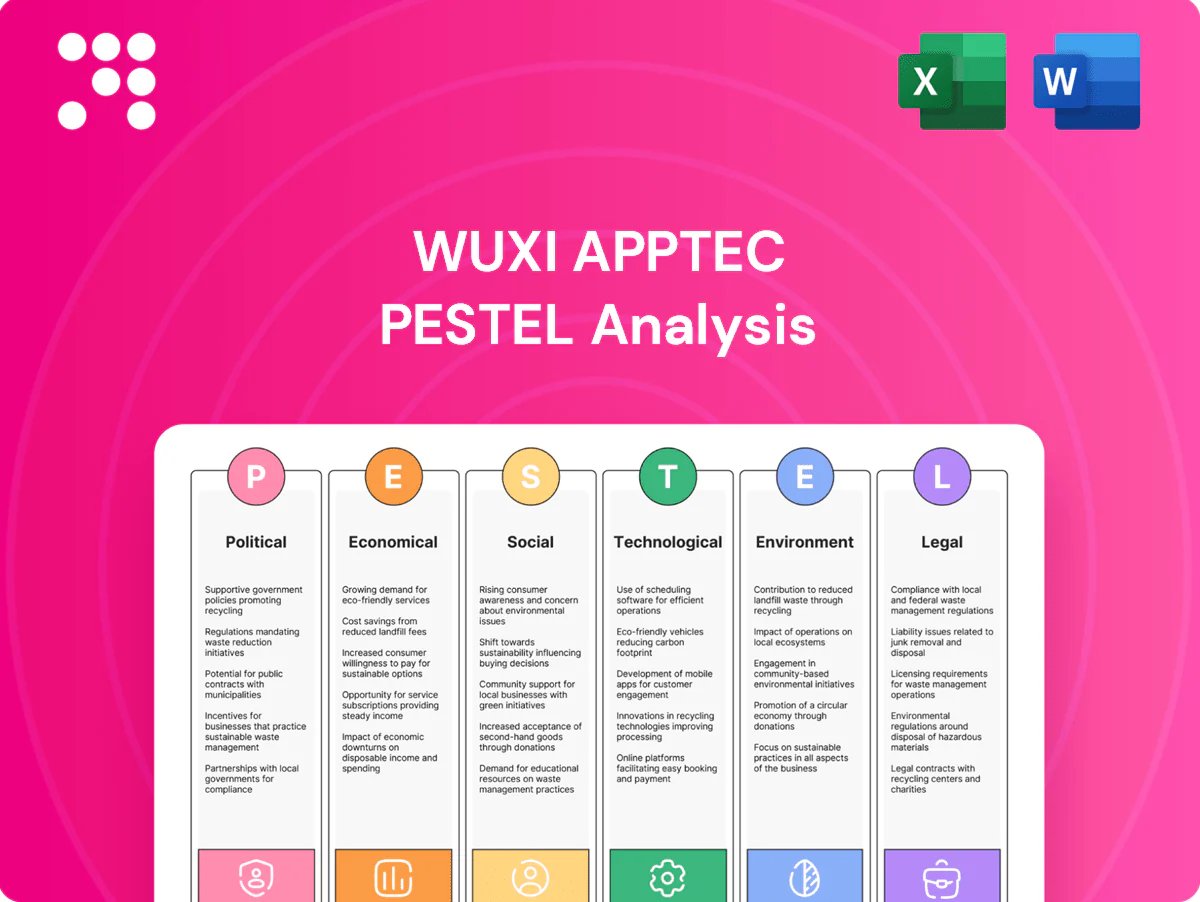

Explores how Political, Economic, Social, Technological, Environmental and Legal forces uniquely impact Wuxi AppTec, combining data-driven trends and region/industry specifics to identify risks and opportunities for executives, investors and strategists; includes forward-looking insights for scenario planning and funding readiness.

A concise, visually segmented PESTLE summary of Wuxi AppTec that’s easy to drop into presentations, share across teams, and annotate for regional or business-line risks—ideal for meetings and strategy sessions.

Economic factors

Biotech funding cycles

Venture and public-market swings drive project starts and cancellations: the biotech funding retrenchment through 2023–24 cut early-stage starts, while strong funding spurts boost discovery and preclinical demand. Wuxi’s diversification across big-pharma clients and 30+ country footprint smooths revenue volatility. Flexible pricing and modular capacity helped lift utilization toward ~80% in 2024, cushioning rate pressure in downturns.

Currency and interest rates

FX moves (USD/CNY around 7.2 in mid-2025) materially affect Wuxi AppTec where USD-linked contract revenues can outpace RMB-denominated operating costs, widening margins or eroding them on yuan strength. Higher global rates (US Fed funds ~5.25–5.50% mid-2025) raise sponsor WACC, reprioritizing pipelines and outsourcing depth. Active hedging, multi-currency billing and timing capex to rate trajectories reduce exposure and finance cost shock.

Global demand for modalities

Shifts from small molecules to biologics and cell & gene therapies (CGT) force Wuxi AppTec to rebalance asset mix toward biologics/CGT, with CGT forecast CAGR about 20.8% through 2030 supporting higher ASPs and margins. Aligning capacity to these high-growth modalities preserves pricing power and reduces idle fixed costs. Platform standardization boosts throughput and unit economics. Active portfolio balancing limits concentration risk across modalities.

Input cost inflation

Input cost inflation at Wuxi AppTec has been driven by chemicals, single-use systems, energy and labor, with specialty chemical prices up about 15% from 2021–23 and industrial energy costs rising roughly 10% in the same period; long-term supplier contracts and vertical integration are used to stabilize costs. Operational excellence programs offset margin compression, though surcharges may be applied in extreme markets.

- Chemicals +15% (2021–23)

- Energy +10% (2021–23)

- Vertical integration mitigates volatility

- Surcharges for extreme-market pass-throughs

Supply chain resilience

Sponsors now expect redundancy for critical reagents and consumables, prompting Wuxi AppTec to expand dual-sourcing and regional warehouses to cut disruption risk; McKinsey estimates digital supply visibility can boost OTIF by up to 20%, and ISO/GMP/GLP certifications remain decisive for preferred‑vendor status and contracting in 2024.

- Redundancy: required by sponsors

- Dual-sourcing: lowers single‑point risk

- Regional warehouses: shorten lead times

- Digital visibility: +up to 20% OTIF (McKinsey)

- Certifications: drive preferred‑vendor and contracts

US–China biotech tensions push firms to diversify CDMO/CROs, raising compliance and costs

Venture/public-market volatility drove early-stage cuts through 2023–24 but stronger funding lifted Wuxi utilization to ~80% in 2024; diversified client base across 30+ countries smooths revenue swings. FX (USD/CNY ~7.2 mid‑2025) and higher rates (Fed funds 5.25–5.50% mid‑2025) materially affect margins and outsourcing demand. Biologics/CGT (CAGR ~20.8% to 2030) require capacity rebalancing; input inflation (chemicals +15%, energy +10% 2021–23) and supply redundancy remain key cost drivers.

| Metric | Value |

|---|---|

| Utilization (2024) | ~80% |

| USD/CNY (mid‑2025) | ~7.2 |

| Fed funds (mid‑2025) | 5.25–5.50% |

| CGT CAGR to 2030 | ~20.8% |

| Chemicals (2021–23) | +15% |

| Energy (2021–23) | +10% |

| Geographic footprint | 30+ countries |

Same Document Delivered

Wuxi Apptec PESTLE Analysis

The preview shown here is the exact Wuxi AppTec PESTLE Analysis you’ll receive after purchase—fully formatted and ready to use. It covers political, economic, social, technological, legal and environmental factors with professional structure and no placeholders. Download the finished file instantly after checkout.

Skip the Research. Get the Strategy.

Gain strategic clarity with our concise PESTLE Analysis of Wuxi AppTec—highlighting regulatory risks, economic drivers, and technological advances shaping its growth trajectory. Ideal for investors and strategists who need actionable external insights fast. Buy the full analysis to access deep-dive findings, scenario impacts, and ready-to-use recommendations for confident decision-making.

Political factors

US–China geopolitics

Heightened US–China geopolitics, underscored by expanded US export controls on sensitive biotechnologies in 2023–24, raises scrutiny of China-based biomanufacturing partners and could restrict cross-border biotech collaboration and data sharing. Clients may accelerate geographic diversification of CDMO/CRO sourcing, pressuring order flow. Wuxi AppTec’s proactive global footprint and compliance diplomacy remain key mitigants.

Export controls and sanctions

US and allied export controls on advanced biotech and dual-use tools have tightened, constraining imports of certain equipment and services and affecting operations that serve more than 50 countries with sanctions regimes.

Sanctions increase counterparty screening burdens and regulatory complexity, driving compliance costs and lead times higher for CRO/CDMO firms like Wuxi AppTec.

Building alternative supplier networks and regional sourcing has become a strategic mitigation to preserve supply continuity and customer service.

Healthcare industrial policy

China, the US and the EU have stepped up industrial healthcare policy—China's biopharma market exceeded $150 billion in 2023—driving subsidies and grants (combined US/EU national biomanufacturing support programs exceed $20 billion since 2020) that lower capex hurdles but foster local competitors. WuXi AppTec can capture incentive-driven demand yet must comply with in-country-for-country mandates and adapt site strategy rapidly as policy shifts alter allocation of clinical and commercial manufacturing volumes.

Drug pricing and reimbursement politics

Global cost‑containment debates—with the US/EU accounting for roughly 40–45% of global pharma spend—pressure sponsors to trim R&D budgets and reprioritize pipelines; price pressure can slow late‑stage programs yet boosts demand for outsourcing as sponsors seek 10–20% cost savings via CRO/CDMO partnerships. Stable public funding for priority diseases (e.g., oncology, vaccines) sustains demand; scenario planning aligns Wuxi AppTec capacity to 3–5 year policy cycles.

- Policy pressure → smaller late‑stage portfolios

- Outsourcing demand up for cost reduction

- Priority disease funding provides stable revenue

- Scenario planning matches capacity to 3–5y policy cycles

Trade tariffs and customs

Tariffs on lab consumables, chemicals and equipment can raise Wuxi AppTec's input costs, with trade measures historically reaching up to 25% on affected goods; this compresses margins on low-value, high-volume items. Customs delays complicate sample and material flows, increasing lead times and working capital needs. Bonded logistics and localized inventories reduce disruption risk, and contracts increasingly include pass-through clauses for tariff shocks.

- Tariff exposure: up to 25%

- Customs risk: higher lead times, greater working capital

- Mitigation: bonded warehouses, local inventory

- Contracting: pass-through tariff clauses

US–China biotech tensions push firms to diversify CDMO/CROs, raising compliance and costs

Heightened US–China biotech tensions and 2023–24 US export controls raise scrutiny of China-based CDMO/CRO partners, prompting client diversification and higher compliance costs. China’s biopharma market exceeded $150B in 2023 while US/EU biomanufacturing support >$20B since 2020, boosting regional competition. Tariffs up to 25% and customs delays raise input costs and working capital needs; bonded logistics and pass-through clauses mitigate risk.

| Metric | Value |

|---|---|

| China biopharma 2023 | $150B+ |

| US/EU support since 2020 | $20B+ |

| Tariff exposure | Up to 25% |

What is included in the product

Explores how Political, Economic, Social, Technological, Environmental and Legal forces uniquely impact Wuxi AppTec, combining data-driven trends and region/industry specifics to identify risks and opportunities for executives, investors and strategists; includes forward-looking insights for scenario planning and funding readiness.

A concise, visually segmented PESTLE summary of Wuxi AppTec that’s easy to drop into presentations, share across teams, and annotate for regional or business-line risks—ideal for meetings and strategy sessions.

Economic factors

Biotech funding cycles

Venture and public-market swings drive project starts and cancellations: the biotech funding retrenchment through 2023–24 cut early-stage starts, while strong funding spurts boost discovery and preclinical demand. Wuxi’s diversification across big-pharma clients and 30+ country footprint smooths revenue volatility. Flexible pricing and modular capacity helped lift utilization toward ~80% in 2024, cushioning rate pressure in downturns.

Currency and interest rates

FX moves (USD/CNY around 7.2 in mid-2025) materially affect Wuxi AppTec where USD-linked contract revenues can outpace RMB-denominated operating costs, widening margins or eroding them on yuan strength. Higher global rates (US Fed funds ~5.25–5.50% mid-2025) raise sponsor WACC, reprioritizing pipelines and outsourcing depth. Active hedging, multi-currency billing and timing capex to rate trajectories reduce exposure and finance cost shock.

Global demand for modalities

Shifts from small molecules to biologics and cell & gene therapies (CGT) force Wuxi AppTec to rebalance asset mix toward biologics/CGT, with CGT forecast CAGR about 20.8% through 2030 supporting higher ASPs and margins. Aligning capacity to these high-growth modalities preserves pricing power and reduces idle fixed costs. Platform standardization boosts throughput and unit economics. Active portfolio balancing limits concentration risk across modalities.

Input cost inflation

Input cost inflation at Wuxi AppTec has been driven by chemicals, single-use systems, energy and labor, with specialty chemical prices up about 15% from 2021–23 and industrial energy costs rising roughly 10% in the same period; long-term supplier contracts and vertical integration are used to stabilize costs. Operational excellence programs offset margin compression, though surcharges may be applied in extreme markets.

- Chemicals +15% (2021–23)

- Energy +10% (2021–23)

- Vertical integration mitigates volatility

- Surcharges for extreme-market pass-throughs

Supply chain resilience

Sponsors now expect redundancy for critical reagents and consumables, prompting Wuxi AppTec to expand dual-sourcing and regional warehouses to cut disruption risk; McKinsey estimates digital supply visibility can boost OTIF by up to 20%, and ISO/GMP/GLP certifications remain decisive for preferred‑vendor status and contracting in 2024.

- Redundancy: required by sponsors

- Dual-sourcing: lowers single‑point risk

- Regional warehouses: shorten lead times

- Digital visibility: +up to 20% OTIF (McKinsey)

- Certifications: drive preferred‑vendor and contracts

US–China biotech tensions push firms to diversify CDMO/CROs, raising compliance and costs

Venture/public-market volatility drove early-stage cuts through 2023–24 but stronger funding lifted Wuxi utilization to ~80% in 2024; diversified client base across 30+ countries smooths revenue swings. FX (USD/CNY ~7.2 mid‑2025) and higher rates (Fed funds 5.25–5.50% mid‑2025) materially affect margins and outsourcing demand. Biologics/CGT (CAGR ~20.8% to 2030) require capacity rebalancing; input inflation (chemicals +15%, energy +10% 2021–23) and supply redundancy remain key cost drivers.

| Metric | Value |

|---|---|

| Utilization (2024) | ~80% |

| USD/CNY (mid‑2025) | ~7.2 |

| Fed funds (mid‑2025) | 5.25–5.50% |

| CGT CAGR to 2030 | ~20.8% |

| Chemicals (2021–23) | +15% |

| Energy (2021–23) | +10% |

| Geographic footprint | 30+ countries |

Same Document Delivered

Wuxi Apptec PESTLE Analysis

The preview shown here is the exact Wuxi AppTec PESTLE Analysis you’ll receive after purchase—fully formatted and ready to use. It covers political, economic, social, technological, legal and environmental factors with professional structure and no placeholders. Download the finished file instantly after checkout.

Description

Skip the Research. Get the Strategy.

Gain strategic clarity with our concise PESTLE Analysis of Wuxi AppTec—highlighting regulatory risks, economic drivers, and technological advances shaping its growth trajectory. Ideal for investors and strategists who need actionable external insights fast. Buy the full analysis to access deep-dive findings, scenario impacts, and ready-to-use recommendations for confident decision-making.

Political factors

US–China geopolitics

Heightened US–China geopolitics, underscored by expanded US export controls on sensitive biotechnologies in 2023–24, raises scrutiny of China-based biomanufacturing partners and could restrict cross-border biotech collaboration and data sharing. Clients may accelerate geographic diversification of CDMO/CRO sourcing, pressuring order flow. Wuxi AppTec’s proactive global footprint and compliance diplomacy remain key mitigants.

Export controls and sanctions

US and allied export controls on advanced biotech and dual-use tools have tightened, constraining imports of certain equipment and services and affecting operations that serve more than 50 countries with sanctions regimes.

Sanctions increase counterparty screening burdens and regulatory complexity, driving compliance costs and lead times higher for CRO/CDMO firms like Wuxi AppTec.

Building alternative supplier networks and regional sourcing has become a strategic mitigation to preserve supply continuity and customer service.

Healthcare industrial policy

China, the US and the EU have stepped up industrial healthcare policy—China's biopharma market exceeded $150 billion in 2023—driving subsidies and grants (combined US/EU national biomanufacturing support programs exceed $20 billion since 2020) that lower capex hurdles but foster local competitors. WuXi AppTec can capture incentive-driven demand yet must comply with in-country-for-country mandates and adapt site strategy rapidly as policy shifts alter allocation of clinical and commercial manufacturing volumes.

Drug pricing and reimbursement politics

Global cost‑containment debates—with the US/EU accounting for roughly 40–45% of global pharma spend—pressure sponsors to trim R&D budgets and reprioritize pipelines; price pressure can slow late‑stage programs yet boosts demand for outsourcing as sponsors seek 10–20% cost savings via CRO/CDMO partnerships. Stable public funding for priority diseases (e.g., oncology, vaccines) sustains demand; scenario planning aligns Wuxi AppTec capacity to 3–5 year policy cycles.

- Policy pressure → smaller late‑stage portfolios

- Outsourcing demand up for cost reduction

- Priority disease funding provides stable revenue

- Scenario planning matches capacity to 3–5y policy cycles

Trade tariffs and customs

Tariffs on lab consumables, chemicals and equipment can raise Wuxi AppTec's input costs, with trade measures historically reaching up to 25% on affected goods; this compresses margins on low-value, high-volume items. Customs delays complicate sample and material flows, increasing lead times and working capital needs. Bonded logistics and localized inventories reduce disruption risk, and contracts increasingly include pass-through clauses for tariff shocks.

- Tariff exposure: up to 25%

- Customs risk: higher lead times, greater working capital

- Mitigation: bonded warehouses, local inventory

- Contracting: pass-through tariff clauses

US–China biotech tensions push firms to diversify CDMO/CROs, raising compliance and costs

Heightened US–China biotech tensions and 2023–24 US export controls raise scrutiny of China-based CDMO/CRO partners, prompting client diversification and higher compliance costs. China’s biopharma market exceeded $150B in 2023 while US/EU biomanufacturing support >$20B since 2020, boosting regional competition. Tariffs up to 25% and customs delays raise input costs and working capital needs; bonded logistics and pass-through clauses mitigate risk.

| Metric | Value |

|---|---|

| China biopharma 2023 | $150B+ |

| US/EU support since 2020 | $20B+ |

| Tariff exposure | Up to 25% |

What is included in the product

Explores how Political, Economic, Social, Technological, Environmental and Legal forces uniquely impact Wuxi AppTec, combining data-driven trends and region/industry specifics to identify risks and opportunities for executives, investors and strategists; includes forward-looking insights for scenario planning and funding readiness.

A concise, visually segmented PESTLE summary of Wuxi AppTec that’s easy to drop into presentations, share across teams, and annotate for regional or business-line risks—ideal for meetings and strategy sessions.

Economic factors

Biotech funding cycles

Venture and public-market swings drive project starts and cancellations: the biotech funding retrenchment through 2023–24 cut early-stage starts, while strong funding spurts boost discovery and preclinical demand. Wuxi’s diversification across big-pharma clients and 30+ country footprint smooths revenue volatility. Flexible pricing and modular capacity helped lift utilization toward ~80% in 2024, cushioning rate pressure in downturns.

Currency and interest rates

FX moves (USD/CNY around 7.2 in mid-2025) materially affect Wuxi AppTec where USD-linked contract revenues can outpace RMB-denominated operating costs, widening margins or eroding them on yuan strength. Higher global rates (US Fed funds ~5.25–5.50% mid-2025) raise sponsor WACC, reprioritizing pipelines and outsourcing depth. Active hedging, multi-currency billing and timing capex to rate trajectories reduce exposure and finance cost shock.

Global demand for modalities

Shifts from small molecules to biologics and cell & gene therapies (CGT) force Wuxi AppTec to rebalance asset mix toward biologics/CGT, with CGT forecast CAGR about 20.8% through 2030 supporting higher ASPs and margins. Aligning capacity to these high-growth modalities preserves pricing power and reduces idle fixed costs. Platform standardization boosts throughput and unit economics. Active portfolio balancing limits concentration risk across modalities.

Input cost inflation

Input cost inflation at Wuxi AppTec has been driven by chemicals, single-use systems, energy and labor, with specialty chemical prices up about 15% from 2021–23 and industrial energy costs rising roughly 10% in the same period; long-term supplier contracts and vertical integration are used to stabilize costs. Operational excellence programs offset margin compression, though surcharges may be applied in extreme markets.

- Chemicals +15% (2021–23)

- Energy +10% (2021–23)

- Vertical integration mitigates volatility

- Surcharges for extreme-market pass-throughs

Supply chain resilience

Sponsors now expect redundancy for critical reagents and consumables, prompting Wuxi AppTec to expand dual-sourcing and regional warehouses to cut disruption risk; McKinsey estimates digital supply visibility can boost OTIF by up to 20%, and ISO/GMP/GLP certifications remain decisive for preferred‑vendor status and contracting in 2024.

- Redundancy: required by sponsors

- Dual-sourcing: lowers single‑point risk

- Regional warehouses: shorten lead times

- Digital visibility: +up to 20% OTIF (McKinsey)

- Certifications: drive preferred‑vendor and contracts

US–China biotech tensions push firms to diversify CDMO/CROs, raising compliance and costs

Venture/public-market volatility drove early-stage cuts through 2023–24 but stronger funding lifted Wuxi utilization to ~80% in 2024; diversified client base across 30+ countries smooths revenue swings. FX (USD/CNY ~7.2 mid‑2025) and higher rates (Fed funds 5.25–5.50% mid‑2025) materially affect margins and outsourcing demand. Biologics/CGT (CAGR ~20.8% to 2030) require capacity rebalancing; input inflation (chemicals +15%, energy +10% 2021–23) and supply redundancy remain key cost drivers.

| Metric | Value |

|---|---|

| Utilization (2024) | ~80% |

| USD/CNY (mid‑2025) | ~7.2 |

| Fed funds (mid‑2025) | 5.25–5.50% |

| CGT CAGR to 2030 | ~20.8% |

| Chemicals (2021–23) | +15% |

| Energy (2021–23) | +10% |

| Geographic footprint | 30+ countries |

Same Document Delivered

Wuxi Apptec PESTLE Analysis

The preview shown here is the exact Wuxi AppTec PESTLE Analysis you’ll receive after purchase—fully formatted and ready to use. It covers political, economic, social, technological, legal and environmental factors with professional structure and no placeholders. Download the finished file instantly after checkout.