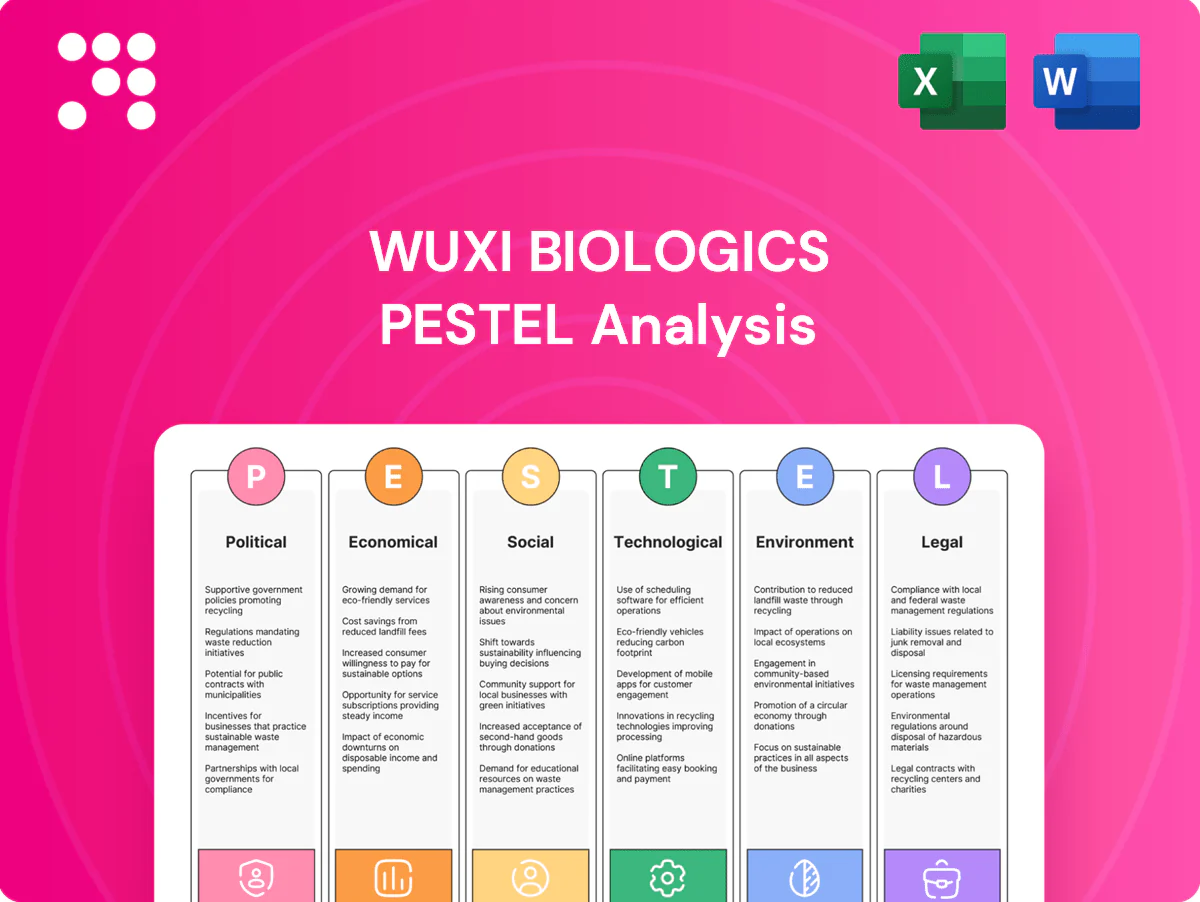

WuXi Biologics PESTLE Analysis

Make Smarter Strategic Decisions with a Complete PESTEL View

Discover how political shifts, regulatory scrutiny, economic cycles, and rapid biotech innovation are shaping WuXi Biologics' strategic outlook in this concise PESTLE snapshot. Our analysis highlights key risks—from IP and trade pressure to supply-chain and sustainability trends—that could affect growth and valuation. Purchase the full, editable PESTLE to access deep insights and actionable recommendations for investors and strategists.

Political factors

US–China geopolitics and export controls

US–China great-power tensions since 2023–24 have raised scrutiny of cross-border projects, slowing approvals for sensitive biologics programs and complicating tech access. Expanded export controls on biotech equipment, software and data flows have made technology transfers and global platform harmonization more difficult. Clients are increasingly diversifying vendors to reduce geopolitical concentration risk. Proactive compliance programs and multi-region capacity can materially mitigate disruption.

Biopharma industrial policies and incentives

National strategies that fund biomanufacturing and onshoring have shifted demand and site selection, with China and the US driving roughly 35% of new global biologics capacity additions in 2023–24, steering WuXi Biologics toward regional buildouts. Subsidies, tax credits and public–private partnerships can cut operating and capex costs by up to 20%, improving project IRRs. Local content rules and JV requirements frequently determine expansion locations, so tracking policy cycles is essential to time capacity deployment and maximize incentives.

Public health preparedness spending

Government stockpiles and pandemic readiness programs drive episodic surges in demand for vaccines and biologics, creating significant but irregular commercial opportunities for WuXi Biologics. Centralized procurement frameworks give volume visibility yet impose tighter pricing and stringent delivery terms that compress margins. Transitions from emergency to routine budgets can produce sharp demand cliffs, so a balanced portfolio across modalities helps smooth revenue volatility and operational strain.

Trade agreements and market access

Trade pacts like RCEP (15 members, ~30% global GDP since 2022) and bilateral FTAs shape tariffs, customs timelines and regulatory cooperation; favorable rules of origin and mutual recognition shorten tech transfer and batch-release cycles, while protectionism raises cost-to-serve and lead times; WuXi Biologics leverages a strategic footprint across China, US and EU to sustain global reach.

- RCEP: 15 members, ~30% global GDP

- Favorable ROO/mutual recognition → faster tech transfer/batch release

- Protectionism → higher logistics/tariff costs, longer lead times

- Strategic hubs in treaty-aligned markets support market access

Political scrutiny of supply chains

Geopolitics, onshoring and DSCSA reshape biologics supply: China+US lead ~35% of new capacity

Geopolitical tensions since 2023–24 have heightened export controls and review of cross‑border biologics projects, slowing approvals and driving clients to diversify vendors. National onshoring subsidies and tax credits cut capex/opex by ~15–20% and China+US drove ~35% of new biologics capacity in 2023–24. Centralized procurement and DSCSA serialization (live Nov 2023) create episodic demand but tighter pricing and compliance burdens.

| Indicator | Value |

|---|---|

| China+US share of new capacity (2023–24) | ~35% |

| Estimated subsidy/tax impact on costs | ~15–20% |

| RCEP membership/global GDP | 15 members, ~30% |

| DSCSA serialization | Live Nov 2023 |

What is included in the product

Explores how macro-environmental forces—Political, Economic, Social, Technological, Environmental and Legal—uniquely affect WuXi Biologics, integrating data-driven trends and region-specific regulatory dynamics; designed to help executives, investors and strategists identify risks, opportunities and forward-looking scenarios for planning and funding decisions.

A clean, visually segmented PESTLE summary of WuXi Biologics that’s editable for region- or business-specific notes, ideal for drop-in PowerPoints, quick team alignment, and supporting external risk and market-positioning discussions during planning sessions.

Economic factors

Biologics market growth and outsourcing trend

Biologics now comprise roughly half of late‑stage pharma pipelines, expanding the CRDMO addressable market (industry CDMO biologics market forecast >$50bn by 2030). Sponsors increasingly outsource to accelerate timelines, cut capex and access specialty talent, while cyclical biotech funding—IPO and VC slowdowns (>50% drop in 2022–23 deal activity)—can curtail project starts. WuXi’s diversified client mix and broad modality capabilities help stabilize facility utilization.

Capacity utilization and pricing power

High capacity utilization at WuXi Biologics supports gross margins and gives the company pricing power, while slack capacity in the contract biologics market tends to drive stronger price competition and margin pressure.

Long-duration master service agreements and multi-product suites provide revenue visibility and reduce downtime between campaigns, and the mix of late-stage and commercial programs strengthens revenue resilience across cycles.

Dynamic slot management and optimized batch scheduling increase yield per bioreactor-day, improving overall asset turnover and effective capacity without immediate capital expenditure.

Input costs, FX, and interest rates

Single-use systems, chromatography resins and energy (Brent ~$86/bbl in 2024) are material cost drivers for WuXi Biologics and remain sensitive to inflationary pressures. FX swings — USD/CNY ~7.2 and EUR/USD ~1.10 in mid-2025 — affect reported results and export competitiveness. Higher interest rates (US policy ~5.25–5.50%) constrain client funding and raise capex costs. Active hedging and flexible procurement help damp volatility.

Client consolidation and portfolio reprioritization

Consolidation in pharma drives vendor rationalization and re-tenders, shifting volumes as pipelines reprioritize toward mAbs, ADCs and a rising mRNA cohort; biologics comprised over 30% of global R&D pipeline by 2024, amplifying modality mix risk. Robust scenario planning mitigates cancellation impact, while cross-selling across WuXi Biologics end-to-end platform helps defend and recover share.

- Vendor cuts raise re-tender frequency

- Biologics >30% of pipeline (2024)

- Scenario planning limits cancellation risk

- Cross-selling sustains platform share

Regional diversification of demand

Regional diversification keeps US/EU demand as the core revenue base while APAC and emerging markets contribute incremental volumes; local pricing and reimbursement regimes materially shape commercial ramp timing and peak realization. Establishing multi-region release testing lowers logistics costs and lead times, and regional commercial teams improve client capture and retention through localized engagement.

- US/EU core demand

- APAC incremental volumes

- Pricing/reimbursement drive ramps

- Multi-region release testing cuts logistics

- Regional teams boost retention

Geopolitics, onshoring and DSCSA reshape biologics supply: China+US lead ~35% of new capacity

Growing biologics demand expands CRDMO TAM (> $50bn by 2030) while biotech funding fell >50% in 2022–23, limiting new project starts. High utilization supports margins but slack capacity can pressure pricing. Input costs (Brent ~$86/bbl 2024), FX USD/CNY ~7.2 (mid‑2025) and US rates 5.25–5.50% raise operating and capex costs.

| Metric | Value |

|---|---|

| TAM (2030) | > $50bn |

| Biotech funding change | −50% (2022–23) |

| Brent (2024) | ~$86/bbl |

| USD/CNY | ~7.2 (mid‑2025) |

Same Document Delivered

WuXi Biologics PESTLE Analysis

The preview shown here is the exact WuXi Biologics PESTLE Analysis document you’ll receive after purchase—fully formatted and ready to use. It contains the complete political, economic, social, technological, legal, and environmental assessment as displayed, with charts and structured findings. No placeholders or teasers—this is the final file you’ll download immediately after checkout.

Make Smarter Strategic Decisions with a Complete PESTEL View

Discover how political shifts, regulatory scrutiny, economic cycles, and rapid biotech innovation are shaping WuXi Biologics' strategic outlook in this concise PESTLE snapshot. Our analysis highlights key risks—from IP and trade pressure to supply-chain and sustainability trends—that could affect growth and valuation. Purchase the full, editable PESTLE to access deep insights and actionable recommendations for investors and strategists.

Political factors

US–China geopolitics and export controls

US–China great-power tensions since 2023–24 have raised scrutiny of cross-border projects, slowing approvals for sensitive biologics programs and complicating tech access. Expanded export controls on biotech equipment, software and data flows have made technology transfers and global platform harmonization more difficult. Clients are increasingly diversifying vendors to reduce geopolitical concentration risk. Proactive compliance programs and multi-region capacity can materially mitigate disruption.

Biopharma industrial policies and incentives

National strategies that fund biomanufacturing and onshoring have shifted demand and site selection, with China and the US driving roughly 35% of new global biologics capacity additions in 2023–24, steering WuXi Biologics toward regional buildouts. Subsidies, tax credits and public–private partnerships can cut operating and capex costs by up to 20%, improving project IRRs. Local content rules and JV requirements frequently determine expansion locations, so tracking policy cycles is essential to time capacity deployment and maximize incentives.

Public health preparedness spending

Government stockpiles and pandemic readiness programs drive episodic surges in demand for vaccines and biologics, creating significant but irregular commercial opportunities for WuXi Biologics. Centralized procurement frameworks give volume visibility yet impose tighter pricing and stringent delivery terms that compress margins. Transitions from emergency to routine budgets can produce sharp demand cliffs, so a balanced portfolio across modalities helps smooth revenue volatility and operational strain.

Trade agreements and market access

Trade pacts like RCEP (15 members, ~30% global GDP since 2022) and bilateral FTAs shape tariffs, customs timelines and regulatory cooperation; favorable rules of origin and mutual recognition shorten tech transfer and batch-release cycles, while protectionism raises cost-to-serve and lead times; WuXi Biologics leverages a strategic footprint across China, US and EU to sustain global reach.

- RCEP: 15 members, ~30% global GDP

- Favorable ROO/mutual recognition → faster tech transfer/batch release

- Protectionism → higher logistics/tariff costs, longer lead times

- Strategic hubs in treaty-aligned markets support market access

Political scrutiny of supply chains

Geopolitics, onshoring and DSCSA reshape biologics supply: China+US lead ~35% of new capacity

Geopolitical tensions since 2023–24 have heightened export controls and review of cross‑border biologics projects, slowing approvals and driving clients to diversify vendors. National onshoring subsidies and tax credits cut capex/opex by ~15–20% and China+US drove ~35% of new biologics capacity in 2023–24. Centralized procurement and DSCSA serialization (live Nov 2023) create episodic demand but tighter pricing and compliance burdens.

| Indicator | Value |

|---|---|

| China+US share of new capacity (2023–24) | ~35% |

| Estimated subsidy/tax impact on costs | ~15–20% |

| RCEP membership/global GDP | 15 members, ~30% |

| DSCSA serialization | Live Nov 2023 |

What is included in the product

Explores how macro-environmental forces—Political, Economic, Social, Technological, Environmental and Legal—uniquely affect WuXi Biologics, integrating data-driven trends and region-specific regulatory dynamics; designed to help executives, investors and strategists identify risks, opportunities and forward-looking scenarios for planning and funding decisions.

A clean, visually segmented PESTLE summary of WuXi Biologics that’s editable for region- or business-specific notes, ideal for drop-in PowerPoints, quick team alignment, and supporting external risk and market-positioning discussions during planning sessions.

Economic factors

Biologics market growth and outsourcing trend

Biologics now comprise roughly half of late‑stage pharma pipelines, expanding the CRDMO addressable market (industry CDMO biologics market forecast >$50bn by 2030). Sponsors increasingly outsource to accelerate timelines, cut capex and access specialty talent, while cyclical biotech funding—IPO and VC slowdowns (>50% drop in 2022–23 deal activity)—can curtail project starts. WuXi’s diversified client mix and broad modality capabilities help stabilize facility utilization.

Capacity utilization and pricing power

High capacity utilization at WuXi Biologics supports gross margins and gives the company pricing power, while slack capacity in the contract biologics market tends to drive stronger price competition and margin pressure.

Long-duration master service agreements and multi-product suites provide revenue visibility and reduce downtime between campaigns, and the mix of late-stage and commercial programs strengthens revenue resilience across cycles.

Dynamic slot management and optimized batch scheduling increase yield per bioreactor-day, improving overall asset turnover and effective capacity without immediate capital expenditure.

Input costs, FX, and interest rates

Single-use systems, chromatography resins and energy (Brent ~$86/bbl in 2024) are material cost drivers for WuXi Biologics and remain sensitive to inflationary pressures. FX swings — USD/CNY ~7.2 and EUR/USD ~1.10 in mid-2025 — affect reported results and export competitiveness. Higher interest rates (US policy ~5.25–5.50%) constrain client funding and raise capex costs. Active hedging and flexible procurement help damp volatility.

Client consolidation and portfolio reprioritization

Consolidation in pharma drives vendor rationalization and re-tenders, shifting volumes as pipelines reprioritize toward mAbs, ADCs and a rising mRNA cohort; biologics comprised over 30% of global R&D pipeline by 2024, amplifying modality mix risk. Robust scenario planning mitigates cancellation impact, while cross-selling across WuXi Biologics end-to-end platform helps defend and recover share.

- Vendor cuts raise re-tender frequency

- Biologics >30% of pipeline (2024)

- Scenario planning limits cancellation risk

- Cross-selling sustains platform share

Regional diversification of demand

Regional diversification keeps US/EU demand as the core revenue base while APAC and emerging markets contribute incremental volumes; local pricing and reimbursement regimes materially shape commercial ramp timing and peak realization. Establishing multi-region release testing lowers logistics costs and lead times, and regional commercial teams improve client capture and retention through localized engagement.

- US/EU core demand

- APAC incremental volumes

- Pricing/reimbursement drive ramps

- Multi-region release testing cuts logistics

- Regional teams boost retention

Geopolitics, onshoring and DSCSA reshape biologics supply: China+US lead ~35% of new capacity

Growing biologics demand expands CRDMO TAM (> $50bn by 2030) while biotech funding fell >50% in 2022–23, limiting new project starts. High utilization supports margins but slack capacity can pressure pricing. Input costs (Brent ~$86/bbl 2024), FX USD/CNY ~7.2 (mid‑2025) and US rates 5.25–5.50% raise operating and capex costs.

| Metric | Value |

|---|---|

| TAM (2030) | > $50bn |

| Biotech funding change | −50% (2022–23) |

| Brent (2024) | ~$86/bbl |

| USD/CNY | ~7.2 (mid‑2025) |

Same Document Delivered

WuXi Biologics PESTLE Analysis

The preview shown here is the exact WuXi Biologics PESTLE Analysis document you’ll receive after purchase—fully formatted and ready to use. It contains the complete political, economic, social, technological, legal, and environmental assessment as displayed, with charts and structured findings. No placeholders or teasers—this is the final file you’ll download immediately after checkout.

Original: $10.00

-65%$10.00

$3.50Description

Make Smarter Strategic Decisions with a Complete PESTEL View

Discover how political shifts, regulatory scrutiny, economic cycles, and rapid biotech innovation are shaping WuXi Biologics' strategic outlook in this concise PESTLE snapshot. Our analysis highlights key risks—from IP and trade pressure to supply-chain and sustainability trends—that could affect growth and valuation. Purchase the full, editable PESTLE to access deep insights and actionable recommendations for investors and strategists.

Political factors

US–China geopolitics and export controls

US–China great-power tensions since 2023–24 have raised scrutiny of cross-border projects, slowing approvals for sensitive biologics programs and complicating tech access. Expanded export controls on biotech equipment, software and data flows have made technology transfers and global platform harmonization more difficult. Clients are increasingly diversifying vendors to reduce geopolitical concentration risk. Proactive compliance programs and multi-region capacity can materially mitigate disruption.

Biopharma industrial policies and incentives

National strategies that fund biomanufacturing and onshoring have shifted demand and site selection, with China and the US driving roughly 35% of new global biologics capacity additions in 2023–24, steering WuXi Biologics toward regional buildouts. Subsidies, tax credits and public–private partnerships can cut operating and capex costs by up to 20%, improving project IRRs. Local content rules and JV requirements frequently determine expansion locations, so tracking policy cycles is essential to time capacity deployment and maximize incentives.

Public health preparedness spending

Government stockpiles and pandemic readiness programs drive episodic surges in demand for vaccines and biologics, creating significant but irregular commercial opportunities for WuXi Biologics. Centralized procurement frameworks give volume visibility yet impose tighter pricing and stringent delivery terms that compress margins. Transitions from emergency to routine budgets can produce sharp demand cliffs, so a balanced portfolio across modalities helps smooth revenue volatility and operational strain.

Trade agreements and market access

Trade pacts like RCEP (15 members, ~30% global GDP since 2022) and bilateral FTAs shape tariffs, customs timelines and regulatory cooperation; favorable rules of origin and mutual recognition shorten tech transfer and batch-release cycles, while protectionism raises cost-to-serve and lead times; WuXi Biologics leverages a strategic footprint across China, US and EU to sustain global reach.

- RCEP: 15 members, ~30% global GDP

- Favorable ROO/mutual recognition → faster tech transfer/batch release

- Protectionism → higher logistics/tariff costs, longer lead times

- Strategic hubs in treaty-aligned markets support market access

Political scrutiny of supply chains

Geopolitics, onshoring and DSCSA reshape biologics supply: China+US lead ~35% of new capacity

Geopolitical tensions since 2023–24 have heightened export controls and review of cross‑border biologics projects, slowing approvals and driving clients to diversify vendors. National onshoring subsidies and tax credits cut capex/opex by ~15–20% and China+US drove ~35% of new biologics capacity in 2023–24. Centralized procurement and DSCSA serialization (live Nov 2023) create episodic demand but tighter pricing and compliance burdens.

| Indicator | Value |

|---|---|

| China+US share of new capacity (2023–24) | ~35% |

| Estimated subsidy/tax impact on costs | ~15–20% |

| RCEP membership/global GDP | 15 members, ~30% |

| DSCSA serialization | Live Nov 2023 |

What is included in the product

Explores how macro-environmental forces—Political, Economic, Social, Technological, Environmental and Legal—uniquely affect WuXi Biologics, integrating data-driven trends and region-specific regulatory dynamics; designed to help executives, investors and strategists identify risks, opportunities and forward-looking scenarios for planning and funding decisions.

A clean, visually segmented PESTLE summary of WuXi Biologics that’s editable for region- or business-specific notes, ideal for drop-in PowerPoints, quick team alignment, and supporting external risk and market-positioning discussions during planning sessions.

Economic factors

Biologics market growth and outsourcing trend

Biologics now comprise roughly half of late‑stage pharma pipelines, expanding the CRDMO addressable market (industry CDMO biologics market forecast >$50bn by 2030). Sponsors increasingly outsource to accelerate timelines, cut capex and access specialty talent, while cyclical biotech funding—IPO and VC slowdowns (>50% drop in 2022–23 deal activity)—can curtail project starts. WuXi’s diversified client mix and broad modality capabilities help stabilize facility utilization.

Capacity utilization and pricing power

High capacity utilization at WuXi Biologics supports gross margins and gives the company pricing power, while slack capacity in the contract biologics market tends to drive stronger price competition and margin pressure.

Long-duration master service agreements and multi-product suites provide revenue visibility and reduce downtime between campaigns, and the mix of late-stage and commercial programs strengthens revenue resilience across cycles.

Dynamic slot management and optimized batch scheduling increase yield per bioreactor-day, improving overall asset turnover and effective capacity without immediate capital expenditure.

Input costs, FX, and interest rates

Single-use systems, chromatography resins and energy (Brent ~$86/bbl in 2024) are material cost drivers for WuXi Biologics and remain sensitive to inflationary pressures. FX swings — USD/CNY ~7.2 and EUR/USD ~1.10 in mid-2025 — affect reported results and export competitiveness. Higher interest rates (US policy ~5.25–5.50%) constrain client funding and raise capex costs. Active hedging and flexible procurement help damp volatility.

Client consolidation and portfolio reprioritization

Consolidation in pharma drives vendor rationalization and re-tenders, shifting volumes as pipelines reprioritize toward mAbs, ADCs and a rising mRNA cohort; biologics comprised over 30% of global R&D pipeline by 2024, amplifying modality mix risk. Robust scenario planning mitigates cancellation impact, while cross-selling across WuXi Biologics end-to-end platform helps defend and recover share.

- Vendor cuts raise re-tender frequency

- Biologics >30% of pipeline (2024)

- Scenario planning limits cancellation risk

- Cross-selling sustains platform share

Regional diversification of demand

Regional diversification keeps US/EU demand as the core revenue base while APAC and emerging markets contribute incremental volumes; local pricing and reimbursement regimes materially shape commercial ramp timing and peak realization. Establishing multi-region release testing lowers logistics costs and lead times, and regional commercial teams improve client capture and retention through localized engagement.

- US/EU core demand

- APAC incremental volumes

- Pricing/reimbursement drive ramps

- Multi-region release testing cuts logistics

- Regional teams boost retention

Geopolitics, onshoring and DSCSA reshape biologics supply: China+US lead ~35% of new capacity

Growing biologics demand expands CRDMO TAM (> $50bn by 2030) while biotech funding fell >50% in 2022–23, limiting new project starts. High utilization supports margins but slack capacity can pressure pricing. Input costs (Brent ~$86/bbl 2024), FX USD/CNY ~7.2 (mid‑2025) and US rates 5.25–5.50% raise operating and capex costs.

| Metric | Value |

|---|---|

| TAM (2030) | > $50bn |

| Biotech funding change | −50% (2022–23) |

| Brent (2024) | ~$86/bbl |

| USD/CNY | ~7.2 (mid‑2025) |

Same Document Delivered

WuXi Biologics PESTLE Analysis

The preview shown here is the exact WuXi Biologics PESTLE Analysis document you’ll receive after purchase—fully formatted and ready to use. It contains the complete political, economic, social, technological, legal, and environmental assessment as displayed, with charts and structured findings. No placeholders or teasers—this is the final file you’ll download immediately after checkout.