Guangxi Wuzhou Zhongheng Group Porter's Five Forces Analysis

Go Beyond the Preview—Access the Full Strategic Report

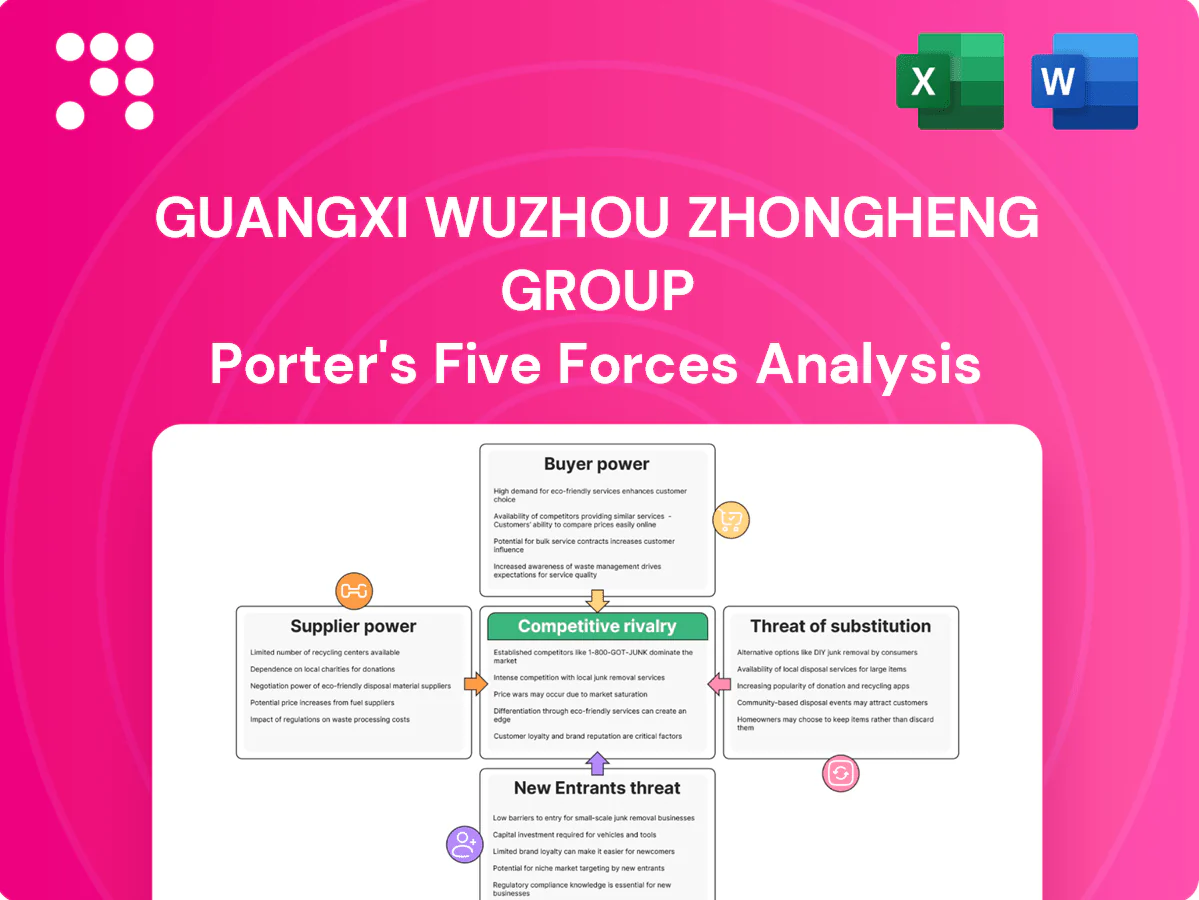

Guangxi Wuzhou Zhongheng Group faces moderate supplier power, rising buyer expectations, and niche barriers to entry that shape its regional logistics and materials business. Competitive rivalry is intensifying as peers expand capacity while substitute threats remain limited but evolving. This brief snapshot only scratches the surface — unlock the full Porter's Five Forces Analysis to get force-by-force ratings, visuals, and actionable strategy guidance.

Suppliers Bargaining Power

APIs and excipients availability

China supplies roughly 40% of global API volume (2023), keeping supplier leverage moderate, but truly NMPA-compliant, high-quality API/excipient vendors are a minority, elevating switching costs for regulated lines. Qualification, audits and stability programs typically take 6–18 months and can cost hundreds of thousands of dollars, so reliable suppliers gain meaningful pricing and delivery influence.

Traditional herbal inputs volatility

Herbal input volatility for TCM in 2024 shows pronounced harvest variability, regional climate risks and quality inconsistency, with limited GAP-certified growers increasing dependence on select suppliers; price spikes and supply shocks have repeatedly compressed margins, and while long-term farming contracts and origin traceability reduce exposure they do not eliminate sourcing risk.

Specialized equipment and maintenance

GMP facilities at Guangxi Wuzhou Zhongheng depend on specialized mixers, sterilizers and packaging lines dominated by concentrated OEMs (≈70% market share in validated line supply in 2024), with after-sales service and validated parts representing roughly 15–25% of lifecycle spend, locking in recurring costs. Downtime can cost up to US$100,000 per day, raising vendor leverage in negotiations. Multi-sourcing and standardizing specs materially reduce this dependence.

Packaging and compliance materials

Regulatory-grade packaging, leaflets and serialization labels for Guangxi Wuzhou Zhongheng require certified vendors; compliance lapses can halt distribution, giving suppliers indirect leverage. In 2024 China’s pharma packaging market was roughly US$20bn with over 200 certified suppliers, which caps unilateral price hikes. Strategic volume bundling and multi-year contracts can secure 5–15% cost savings.

- Compliance dependency: certified vendors required

- Market depth: >200 certified suppliers (2024)

- Price cap: competition limits markup

- Leverage: volume bundling → 5–15% savings

R&D and CRO partnerships

For new formulations or bioequivalence studies Guangxi Wuzhou Zhongheng favors CROs and labs with proven 2024 track records; the global CRO market was about $52 billion in 2024, concentrating work at top sites. Capacity bottlenecks at reputable CROs—utilization often above 90%—have driven protocol fees and timelines up roughly 10–20%. Strict data integrity and audit trails make mid-project switching costly and risky, so strategic partnerships and pipeline smoothing are used to improve bargaining leverage.

- Preferred CROs: proven 2024 performance and regulatory records

- Market size: global CRO market ≈ $52B (2024)

- Capacity: top CRO utilization >90% → fees +10–20%

- Data integrity: switching mid-study increases audit risk

- Mitigation: long-term partnerships and pipeline smoothing

China supplies 40% APIs; NMPA costs raise switching; CROs at 90%

China supplies ~40% of global APIs (2023), keeping supplier leverage moderate, but NMPA‑compliant vendors are few, with qualification taking 6–18 months and costing hundreds of thousands, raising switching costs. Herbal input volatility in 2024 and limited GAP growers amplify supply risk. Packaging market ≈US$20bn (2024) with >200 certified suppliers caps markups; CRO market ≈US$52bn (2024) with top CRO utilization >90% increases fees.

| Category | Metric | Impact |

|---|---|---|

| API supply | China ~40% (2023) | Moderate leverage |

| Qualification | 6–18 months, ~$100k+ | High switching cost |

| Packaging | US$20bn, >200 suppliers (2024) | Price cap |

| CROs | US$52bn, utilization >90% (2024) | Higher fees |

What is included in the product

Tailored Porter's Five Forces analysis for Guangxi Wuzhou Zhongheng Group, uncovering competitive drivers, buyer and supplier power, entry barriers, substitutes, and emerging threats to its market share, with strategic commentary to inform investor and management decision-making.

A compact Porter's Five Forces one-sheet for Guangxi Wuzhou Zhongheng Group—clarifies supplier, buyer, entrant, substitute, and competitive rivalry pressures for rapid strategic decisions and easy inclusion in decks.

Customers Bargaining Power

Centralized procurement pressure

China’s 2024 volume-based procurement and hospital tenders drove average bid-price cuts roughly 60–70%, forcing winners to swap margin for scale while losers face steep volume loss; public buyers thus exert substantial leverage over generics, with winning suppliers often securing over 70% of tendered hospital volumes. Differentiated TCM or non-VBP SKUs remain less exposed to this centralized pressure.

Distributor consolidation

Pharma distribution in China is concentrated among national and large regional players whose scale lets them demand extended payment terms of 60–180 days and negotiate rebates commonly in the 5–15% range (2024 market practices). Multiple strong regional distributors in Guangxi and neighboring provinces cap any single partner’s leverage, and growing direct-to-hospital procurement—reaching double-digit share in several therapeutic areas in 2024—further rebalances bargaining power.

Retail and e-commerce channels

OTC and health foods sell through pharmacies and online platforms where algorithmic price transparency drives rapid price discovery; platforms commonly extract commissions and favored-placement fees in the 5–20% range. High visibility on marketplaces heightens price sensitivity, with roughly 70–80% of shoppers comparing prices before purchase. Strong brand equity and unique formulations reduce churn, enabling 5–15% price premiums and higher repurchase rates.

Physician and patient preferences

Physician prescribing habits and clinical guidelines strongly drive product pull for Guangxi Wuzhou Zhongheng, while patient trust in TCM brands and perceived efficacy often override price sensitivity; interchangeability of cardiovascular and gynecology generics, however, increases buyer leverage. Education campaigns and emerging real-world evidence in 2024 can shift prescriber and patient preferences toward specific formulations.

- Prescriber influence: high

- Patient brand trust: key

- Generics interchangeability: raises leverage

- 2024 RWE/education: pivotal

Real estate and non-pharma buyers

Real estate and non-pharma buyers are few and deal-specific, giving them strong price and terms leverage; in 2024 China new-home sales volumes were down about 10% year-on-year, amplifying buyer pressure during cyclical downturns. Cross-subsidization from the pharma segment is limited in these negotiations, and while the group's diversification spreads revenue risk, it does not remove concentrated buyer leverage in each segment.

- Few large deals → concentrated leverage

- 2024 sales decline ≈10% → stronger buyer power

- Pharma cross-subsidies limited

- Diversification reduces risk but not buyer bargaining

2024 tenders cut prices 60–70%, winners >70% volume, buyers gain leverage

Public procurement and hospital tenders in 2024 drove 60–70% bid-price cuts, giving buyers strong leverage while winners gain >70% tender volumes. Large distributors (60–180 day terms, 5–15% rebates) and platform fees (5–20%) intensify buyer bargaining. OTC online price transparency sees 70–80% comparison, elevating price sensitivity. Real-estate buyers are concentrated; 2024 new-home sales fell ~10%, boosting deal leverage.

| Metric | 2024 Value |

|---|---|

| VBP bid-price cuts | 60–70% |

| Winner hospital share | >70% |

| Distributor payment terms | 60–180 days |

| Distributor rebates | 5–15% |

| Platform fees | 5–20% |

| Shoppers price comparison | 70–80% |

| New-home sales YoY | ≈-10% |

Preview Before You Purchase

Guangxi Wuzhou Zhongheng Group Porter's Five Forces Analysis

This preview shows the exact Porter's Five Forces analysis for Guangxi Wuzhou Zhongheng Group that you'll receive—fully authored, formatted, and ready to use. The document visible here is the same file delivered instantly after purchase. No placeholders, no samples—just the complete analysis.

Go Beyond the Preview—Access the Full Strategic Report

Guangxi Wuzhou Zhongheng Group faces moderate supplier power, rising buyer expectations, and niche barriers to entry that shape its regional logistics and materials business. Competitive rivalry is intensifying as peers expand capacity while substitute threats remain limited but evolving. This brief snapshot only scratches the surface — unlock the full Porter's Five Forces Analysis to get force-by-force ratings, visuals, and actionable strategy guidance.

Suppliers Bargaining Power

APIs and excipients availability

China supplies roughly 40% of global API volume (2023), keeping supplier leverage moderate, but truly NMPA-compliant, high-quality API/excipient vendors are a minority, elevating switching costs for regulated lines. Qualification, audits and stability programs typically take 6–18 months and can cost hundreds of thousands of dollars, so reliable suppliers gain meaningful pricing and delivery influence.

Traditional herbal inputs volatility

Herbal input volatility for TCM in 2024 shows pronounced harvest variability, regional climate risks and quality inconsistency, with limited GAP-certified growers increasing dependence on select suppliers; price spikes and supply shocks have repeatedly compressed margins, and while long-term farming contracts and origin traceability reduce exposure they do not eliminate sourcing risk.

Specialized equipment and maintenance

GMP facilities at Guangxi Wuzhou Zhongheng depend on specialized mixers, sterilizers and packaging lines dominated by concentrated OEMs (≈70% market share in validated line supply in 2024), with after-sales service and validated parts representing roughly 15–25% of lifecycle spend, locking in recurring costs. Downtime can cost up to US$100,000 per day, raising vendor leverage in negotiations. Multi-sourcing and standardizing specs materially reduce this dependence.

Packaging and compliance materials

Regulatory-grade packaging, leaflets and serialization labels for Guangxi Wuzhou Zhongheng require certified vendors; compliance lapses can halt distribution, giving suppliers indirect leverage. In 2024 China’s pharma packaging market was roughly US$20bn with over 200 certified suppliers, which caps unilateral price hikes. Strategic volume bundling and multi-year contracts can secure 5–15% cost savings.

- Compliance dependency: certified vendors required

- Market depth: >200 certified suppliers (2024)

- Price cap: competition limits markup

- Leverage: volume bundling → 5–15% savings

R&D and CRO partnerships

For new formulations or bioequivalence studies Guangxi Wuzhou Zhongheng favors CROs and labs with proven 2024 track records; the global CRO market was about $52 billion in 2024, concentrating work at top sites. Capacity bottlenecks at reputable CROs—utilization often above 90%—have driven protocol fees and timelines up roughly 10–20%. Strict data integrity and audit trails make mid-project switching costly and risky, so strategic partnerships and pipeline smoothing are used to improve bargaining leverage.

- Preferred CROs: proven 2024 performance and regulatory records

- Market size: global CRO market ≈ $52B (2024)

- Capacity: top CRO utilization >90% → fees +10–20%

- Data integrity: switching mid-study increases audit risk

- Mitigation: long-term partnerships and pipeline smoothing

China supplies 40% APIs; NMPA costs raise switching; CROs at 90%

China supplies ~40% of global APIs (2023), keeping supplier leverage moderate, but NMPA‑compliant vendors are few, with qualification taking 6–18 months and costing hundreds of thousands, raising switching costs. Herbal input volatility in 2024 and limited GAP growers amplify supply risk. Packaging market ≈US$20bn (2024) with >200 certified suppliers caps markups; CRO market ≈US$52bn (2024) with top CRO utilization >90% increases fees.

| Category | Metric | Impact |

|---|---|---|

| API supply | China ~40% (2023) | Moderate leverage |

| Qualification | 6–18 months, ~$100k+ | High switching cost |

| Packaging | US$20bn, >200 suppliers (2024) | Price cap |

| CROs | US$52bn, utilization >90% (2024) | Higher fees |

What is included in the product

Tailored Porter's Five Forces analysis for Guangxi Wuzhou Zhongheng Group, uncovering competitive drivers, buyer and supplier power, entry barriers, substitutes, and emerging threats to its market share, with strategic commentary to inform investor and management decision-making.

A compact Porter's Five Forces one-sheet for Guangxi Wuzhou Zhongheng Group—clarifies supplier, buyer, entrant, substitute, and competitive rivalry pressures for rapid strategic decisions and easy inclusion in decks.

Customers Bargaining Power

Centralized procurement pressure

China’s 2024 volume-based procurement and hospital tenders drove average bid-price cuts roughly 60–70%, forcing winners to swap margin for scale while losers face steep volume loss; public buyers thus exert substantial leverage over generics, with winning suppliers often securing over 70% of tendered hospital volumes. Differentiated TCM or non-VBP SKUs remain less exposed to this centralized pressure.

Distributor consolidation

Pharma distribution in China is concentrated among national and large regional players whose scale lets them demand extended payment terms of 60–180 days and negotiate rebates commonly in the 5–15% range (2024 market practices). Multiple strong regional distributors in Guangxi and neighboring provinces cap any single partner’s leverage, and growing direct-to-hospital procurement—reaching double-digit share in several therapeutic areas in 2024—further rebalances bargaining power.

Retail and e-commerce channels

OTC and health foods sell through pharmacies and online platforms where algorithmic price transparency drives rapid price discovery; platforms commonly extract commissions and favored-placement fees in the 5–20% range. High visibility on marketplaces heightens price sensitivity, with roughly 70–80% of shoppers comparing prices before purchase. Strong brand equity and unique formulations reduce churn, enabling 5–15% price premiums and higher repurchase rates.

Physician and patient preferences

Physician prescribing habits and clinical guidelines strongly drive product pull for Guangxi Wuzhou Zhongheng, while patient trust in TCM brands and perceived efficacy often override price sensitivity; interchangeability of cardiovascular and gynecology generics, however, increases buyer leverage. Education campaigns and emerging real-world evidence in 2024 can shift prescriber and patient preferences toward specific formulations.

- Prescriber influence: high

- Patient brand trust: key

- Generics interchangeability: raises leverage

- 2024 RWE/education: pivotal

Real estate and non-pharma buyers

Real estate and non-pharma buyers are few and deal-specific, giving them strong price and terms leverage; in 2024 China new-home sales volumes were down about 10% year-on-year, amplifying buyer pressure during cyclical downturns. Cross-subsidization from the pharma segment is limited in these negotiations, and while the group's diversification spreads revenue risk, it does not remove concentrated buyer leverage in each segment.

- Few large deals → concentrated leverage

- 2024 sales decline ≈10% → stronger buyer power

- Pharma cross-subsidies limited

- Diversification reduces risk but not buyer bargaining

2024 tenders cut prices 60–70%, winners >70% volume, buyers gain leverage

Public procurement and hospital tenders in 2024 drove 60–70% bid-price cuts, giving buyers strong leverage while winners gain >70% tender volumes. Large distributors (60–180 day terms, 5–15% rebates) and platform fees (5–20%) intensify buyer bargaining. OTC online price transparency sees 70–80% comparison, elevating price sensitivity. Real-estate buyers are concentrated; 2024 new-home sales fell ~10%, boosting deal leverage.

| Metric | 2024 Value |

|---|---|

| VBP bid-price cuts | 60–70% |

| Winner hospital share | >70% |

| Distributor payment terms | 60–180 days |

| Distributor rebates | 5–15% |

| Platform fees | 5–20% |

| Shoppers price comparison | 70–80% |

| New-home sales YoY | ≈-10% |

Preview Before You Purchase

Guangxi Wuzhou Zhongheng Group Porter's Five Forces Analysis

This preview shows the exact Porter's Five Forces analysis for Guangxi Wuzhou Zhongheng Group that you'll receive—fully authored, formatted, and ready to use. The document visible here is the same file delivered instantly after purchase. No placeholders, no samples—just the complete analysis.

Original: $10.00

-65%$10.00

$3.50Description

Go Beyond the Preview—Access the Full Strategic Report

Guangxi Wuzhou Zhongheng Group faces moderate supplier power, rising buyer expectations, and niche barriers to entry that shape its regional logistics and materials business. Competitive rivalry is intensifying as peers expand capacity while substitute threats remain limited but evolving. This brief snapshot only scratches the surface — unlock the full Porter's Five Forces Analysis to get force-by-force ratings, visuals, and actionable strategy guidance.

Suppliers Bargaining Power

APIs and excipients availability

China supplies roughly 40% of global API volume (2023), keeping supplier leverage moderate, but truly NMPA-compliant, high-quality API/excipient vendors are a minority, elevating switching costs for regulated lines. Qualification, audits and stability programs typically take 6–18 months and can cost hundreds of thousands of dollars, so reliable suppliers gain meaningful pricing and delivery influence.

Traditional herbal inputs volatility

Herbal input volatility for TCM in 2024 shows pronounced harvest variability, regional climate risks and quality inconsistency, with limited GAP-certified growers increasing dependence on select suppliers; price spikes and supply shocks have repeatedly compressed margins, and while long-term farming contracts and origin traceability reduce exposure they do not eliminate sourcing risk.

Specialized equipment and maintenance

GMP facilities at Guangxi Wuzhou Zhongheng depend on specialized mixers, sterilizers and packaging lines dominated by concentrated OEMs (≈70% market share in validated line supply in 2024), with after-sales service and validated parts representing roughly 15–25% of lifecycle spend, locking in recurring costs. Downtime can cost up to US$100,000 per day, raising vendor leverage in negotiations. Multi-sourcing and standardizing specs materially reduce this dependence.

Packaging and compliance materials

Regulatory-grade packaging, leaflets and serialization labels for Guangxi Wuzhou Zhongheng require certified vendors; compliance lapses can halt distribution, giving suppliers indirect leverage. In 2024 China’s pharma packaging market was roughly US$20bn with over 200 certified suppliers, which caps unilateral price hikes. Strategic volume bundling and multi-year contracts can secure 5–15% cost savings.

- Compliance dependency: certified vendors required

- Market depth: >200 certified suppliers (2024)

- Price cap: competition limits markup

- Leverage: volume bundling → 5–15% savings

R&D and CRO partnerships

For new formulations or bioequivalence studies Guangxi Wuzhou Zhongheng favors CROs and labs with proven 2024 track records; the global CRO market was about $52 billion in 2024, concentrating work at top sites. Capacity bottlenecks at reputable CROs—utilization often above 90%—have driven protocol fees and timelines up roughly 10–20%. Strict data integrity and audit trails make mid-project switching costly and risky, so strategic partnerships and pipeline smoothing are used to improve bargaining leverage.

- Preferred CROs: proven 2024 performance and regulatory records

- Market size: global CRO market ≈ $52B (2024)

- Capacity: top CRO utilization >90% → fees +10–20%

- Data integrity: switching mid-study increases audit risk

- Mitigation: long-term partnerships and pipeline smoothing

China supplies 40% APIs; NMPA costs raise switching; CROs at 90%

China supplies ~40% of global APIs (2023), keeping supplier leverage moderate, but NMPA‑compliant vendors are few, with qualification taking 6–18 months and costing hundreds of thousands, raising switching costs. Herbal input volatility in 2024 and limited GAP growers amplify supply risk. Packaging market ≈US$20bn (2024) with >200 certified suppliers caps markups; CRO market ≈US$52bn (2024) with top CRO utilization >90% increases fees.

| Category | Metric | Impact |

|---|---|---|

| API supply | China ~40% (2023) | Moderate leverage |

| Qualification | 6–18 months, ~$100k+ | High switching cost |

| Packaging | US$20bn, >200 suppliers (2024) | Price cap |

| CROs | US$52bn, utilization >90% (2024) | Higher fees |

What is included in the product

Tailored Porter's Five Forces analysis for Guangxi Wuzhou Zhongheng Group, uncovering competitive drivers, buyer and supplier power, entry barriers, substitutes, and emerging threats to its market share, with strategic commentary to inform investor and management decision-making.

A compact Porter's Five Forces one-sheet for Guangxi Wuzhou Zhongheng Group—clarifies supplier, buyer, entrant, substitute, and competitive rivalry pressures for rapid strategic decisions and easy inclusion in decks.

Customers Bargaining Power

Centralized procurement pressure

China’s 2024 volume-based procurement and hospital tenders drove average bid-price cuts roughly 60–70%, forcing winners to swap margin for scale while losers face steep volume loss; public buyers thus exert substantial leverage over generics, with winning suppliers often securing over 70% of tendered hospital volumes. Differentiated TCM or non-VBP SKUs remain less exposed to this centralized pressure.

Distributor consolidation

Pharma distribution in China is concentrated among national and large regional players whose scale lets them demand extended payment terms of 60–180 days and negotiate rebates commonly in the 5–15% range (2024 market practices). Multiple strong regional distributors in Guangxi and neighboring provinces cap any single partner’s leverage, and growing direct-to-hospital procurement—reaching double-digit share in several therapeutic areas in 2024—further rebalances bargaining power.

Retail and e-commerce channels

OTC and health foods sell through pharmacies and online platforms where algorithmic price transparency drives rapid price discovery; platforms commonly extract commissions and favored-placement fees in the 5–20% range. High visibility on marketplaces heightens price sensitivity, with roughly 70–80% of shoppers comparing prices before purchase. Strong brand equity and unique formulations reduce churn, enabling 5–15% price premiums and higher repurchase rates.

Physician and patient preferences

Physician prescribing habits and clinical guidelines strongly drive product pull for Guangxi Wuzhou Zhongheng, while patient trust in TCM brands and perceived efficacy often override price sensitivity; interchangeability of cardiovascular and gynecology generics, however, increases buyer leverage. Education campaigns and emerging real-world evidence in 2024 can shift prescriber and patient preferences toward specific formulations.

- Prescriber influence: high

- Patient brand trust: key

- Generics interchangeability: raises leverage

- 2024 RWE/education: pivotal

Real estate and non-pharma buyers

Real estate and non-pharma buyers are few and deal-specific, giving them strong price and terms leverage; in 2024 China new-home sales volumes were down about 10% year-on-year, amplifying buyer pressure during cyclical downturns. Cross-subsidization from the pharma segment is limited in these negotiations, and while the group's diversification spreads revenue risk, it does not remove concentrated buyer leverage in each segment.

- Few large deals → concentrated leverage

- 2024 sales decline ≈10% → stronger buyer power

- Pharma cross-subsidies limited

- Diversification reduces risk but not buyer bargaining

2024 tenders cut prices 60–70%, winners >70% volume, buyers gain leverage

Public procurement and hospital tenders in 2024 drove 60–70% bid-price cuts, giving buyers strong leverage while winners gain >70% tender volumes. Large distributors (60–180 day terms, 5–15% rebates) and platform fees (5–20%) intensify buyer bargaining. OTC online price transparency sees 70–80% comparison, elevating price sensitivity. Real-estate buyers are concentrated; 2024 new-home sales fell ~10%, boosting deal leverage.

| Metric | 2024 Value |

|---|---|

| VBP bid-price cuts | 60–70% |

| Winner hospital share | >70% |

| Distributor payment terms | 60–180 days |

| Distributor rebates | 5–15% |

| Platform fees | 5–20% |

| Shoppers price comparison | 70–80% |

| New-home sales YoY | ≈-10% |

Preview Before You Purchase

Guangxi Wuzhou Zhongheng Group Porter's Five Forces Analysis

This preview shows the exact Porter's Five Forces analysis for Guangxi Wuzhou Zhongheng Group that you'll receive—fully authored, formatted, and ready to use. The document visible here is the same file delivered instantly after purchase. No placeholders, no samples—just the complete analysis.