Xaar Porter's Five Forces Analysis

Don't Miss the Bigger Picture

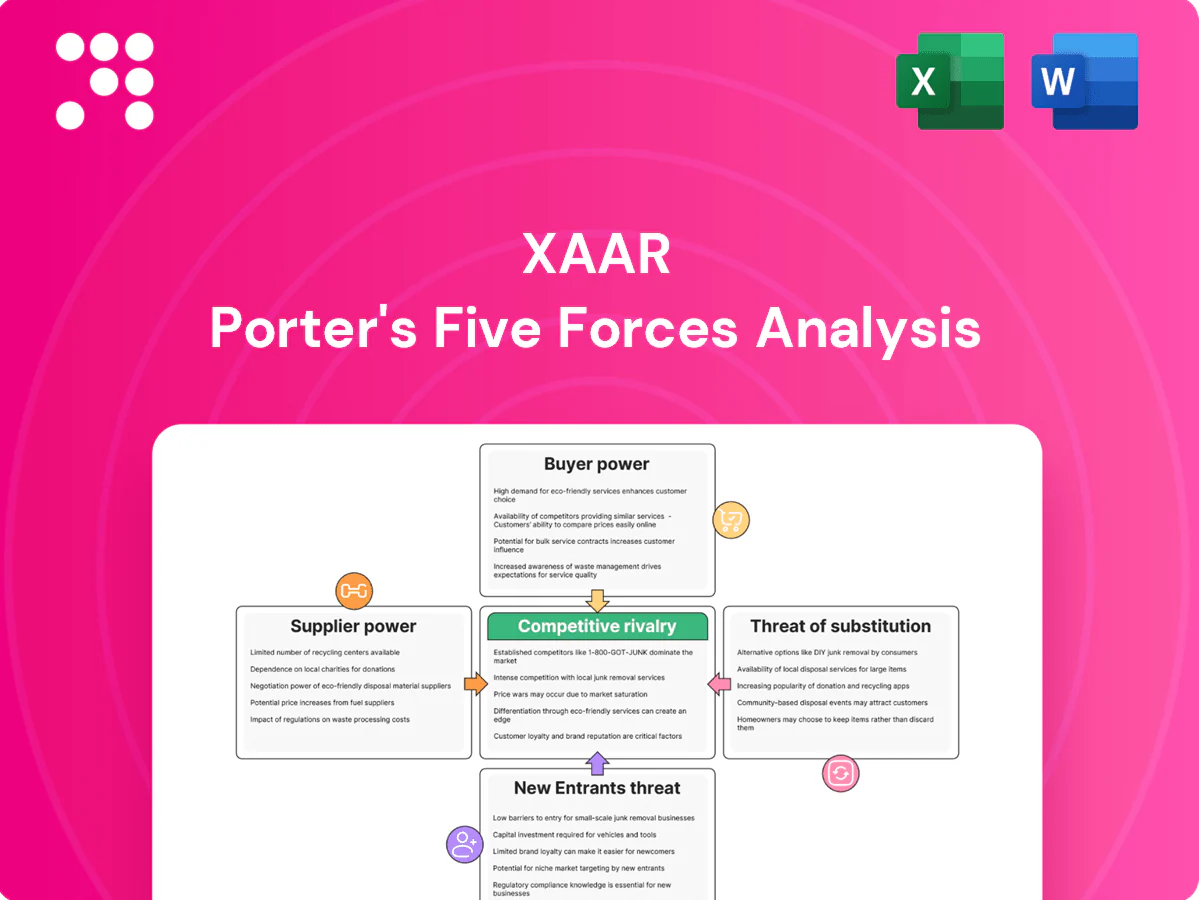

Xaar operates in a niche industrial-printing market where supplier concentration and technological differentiation shape margins, while buyer power and emerging substitutes gradually shift competitive dynamics. Our snapshot highlights key threats and strategic levers for growth. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Xaar’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentrated critical materials

Core inputs like piezoelectric ceramics, precision nozzles and specialty ASICs come from a very limited global supplier base, leaving Xaar exposed; ASIC lead times in 2024 commonly run 20–30 weeks and nozzle qualification cycles exceed 6–12 months. Scarcity and certification hurdles give vendors pricing and lead-time leverage, with disruptions cascading into multi-month production delays. Dual-sourcing is feasible but typically costs $0.5–2m and 12–18 months to validate.

High switching and qualification costs

Substituting a printhead component requires extensive testing to meet jetting reliability and lifetime specs, with re-qualification commonly taking 3–9 months and tying up 2–5 engineering FTEs. These time and resource burdens increase supplier bargaining power in negotiations. Long-term supply agreements (typically 3–5 years) reduce but do not eliminate this risk.

Process equipment dependence

Cleanroom tools, coating lines and precision assembly for inkjet/printed electronics are highly vendor-specific, giving OEMs leverage as service and spare parts often carry markups in the 30–50% range and aftermarket services can represent roughly 30–40% of equipment lifecycle value (2024 industry data). Downtime costs—routinely thousands to tens of thousands USD per hour in high-mix manufacturing—strengthen suppliers’ pricing power. Preventive maintenance contracts and onsite parts buffers materially reduce outage risk and supplier hold-up.

Ink and fluid ecosystem interdependence

Xaar's printhead performance hinges on compatibility with inks and functional fluids from specialist chemical formulators; co-development creates mutual dependence but supplier concentration can skew bargaining power when few meet required viscosity and particle-size specs.

- Approved-ink lists restrict customer flexibility

- Co-development raises switching costs

- Joint testing frameworks can rebalance terms

Potential for selective vertical integration

Xaar can insource certain modules or develop proprietary coatings to reduce supplier reliance, but capital intensity and steep learning curves limit the breadth of integration, preserving leverage with specialist suppliers for advanced parts.

Strategic partnerships or licensing can secure critical technologies and supply continuity without full vertical integration, enabling focus on commoditized modules while outsourcing high-tech components.

- Selective insourcing of commoditized modules

- Capital barriers and learning curves constrain scope

- Specialist suppliers retain leverage for advanced parts

- Partnerships secure key technologies without full integration

Supplier concentration raises risk — long lead times, high markups; partial insourcing offsets

Supplier concentration gives high bargaining power: ASIC lead times 20–30 weeks and nozzle qualification 6–12 months (2024), dual-sourcing costs $0.5–2m and 12–18 months, and vendor markups 30–50% with aftermarket ≈30–40% of lifecycle value. Co-development raises switching costs; selective insourcing/partnerships can partially mitigate risk.

| Metric | 2024 Value |

|---|---|

| ASIC lead time | 20–30 weeks |

| Nozzle qualification | 6–12 months |

| Dual-source cost/time | $0.5–2m / 12–18m |

| Vendor markups | 30–50% |

| Aftermarket share | 30–40% |

What is included in the product

Uncovers key drivers of competition, supplier and buyer power, entry barriers and substitutes specific to Xaar, identifying disruptive threats and strategic levers to protect market share; fully editable for reports and decks.

A concise one-sheet Porter's Five Forces for Xaar that maps competitive pressure via an instant spider chart—customize inputs, duplicate scenarios (pre/post regulation) and drop into pitch decks to streamline board-ready analysis without macros.

Customers Bargaining Power

Concentrated OEM and integrator base

Industrial printer OEMs and systems integrators buy in sizeable but episodic batches, with the largest OEMs and integrators commonly representing a majority of supplier revenues; their concentration enables aggressive price and service negotiations and contested initial terms for design wins. Design wins are sticky, yet losing a top account can reduce supplier volumes materially, often by more than 20% in a single year (2024 market observation).

High switching costs but credible alternatives

Printheads are deeply integrated into mechanics, electronics and software, so switching typically requires weeks to months of redesign, revalidation and operator retraining.

Despite these high switching costs, buyers in 2024 can pivot to credible rivals such as Kyocera, Ricoh, Epson, Seiko and Dimatix.

That available set of alternatives gives customers meaningful bargaining leverage despite the integration frictions.

Performance-driven procurement

Buyers prioritize throughput, drop placement accuracy (typically <20 microns), viscosity range and total cost of ownership when sourcing inkjet heads. Demonstrable gains in uptime and laydown—often cited as 20–30% productivity improvements in supplier case studies—justify premium pricing. Conversely, reliability issues trigger concessions; field performance data and extended warranties are primary bargaining chips in 2024 negotiations.

Aftermarket and service expectations

Customers demand rapid support, ready spares and timely firmware updates, making SLAs and operator training core negotiation points; strong service reduces price sensitivity while weak geographic or technical coverage amplifies buyer power.

- Service SLAs drive contract terms

- Spare parts availability lowers churn

- Firmware/updates affect uptime and loyalty

Cyclical capex and project timing

Cyclical capex in end-markets such as ceramics, labels and packaging—the global packaging market was about USD 1.03 trillion in 2024—means buyers batch purchases to meet budget windows, forcing discounts and contract timing leverage against suppliers like Xaar; deferred projects amplify pricing pressure while flexible financing and demo programs reduce churn and smooth order flows.

- Batch buying: forces seasonal discounts

- Deferred projects: raises price sensitivity

- Financing/demo: mitigates cyclicality

OEM buyer concentration threatens >20% supplier exposure amid 20–30% productivity pitch

Large OEMs/integradors concentrate purchases, enabling aggressive price/service negotiation and risking >20% supplier volume loss from a single lost design win (2024 observation).

High switching costs (weeks–months) are offset by multiple credible rivals, giving buyers meaningful leverage despite integration frictions.

Buyers prioritize TCO, uptime and accuracy; supplier case studies cite 20–30% productivity gains, and global packaging was ~USD 1.03T in 2024.

| Metric | 2024 Value |

|---|---|

| Single-account loss impact | >20% |

| Productivity uplift (supplier claims) | 20–30% |

| Global packaging market | USD 1.03T |

Same Document Delivered

Xaar Porter's Five Forces Analysis

This preview shows the exact Xaar Porter's Five Forces Analysis you'll receive upon purchase—no placeholders or mockups. The document displayed is the full, professionally formatted analysis ready for immediate download and use. You're viewing the same file you'll get instantly after payment.

Don't Miss the Bigger Picture

Xaar operates in a niche industrial-printing market where supplier concentration and technological differentiation shape margins, while buyer power and emerging substitutes gradually shift competitive dynamics. Our snapshot highlights key threats and strategic levers for growth. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Xaar’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentrated critical materials

Core inputs like piezoelectric ceramics, precision nozzles and specialty ASICs come from a very limited global supplier base, leaving Xaar exposed; ASIC lead times in 2024 commonly run 20–30 weeks and nozzle qualification cycles exceed 6–12 months. Scarcity and certification hurdles give vendors pricing and lead-time leverage, with disruptions cascading into multi-month production delays. Dual-sourcing is feasible but typically costs $0.5–2m and 12–18 months to validate.

High switching and qualification costs

Substituting a printhead component requires extensive testing to meet jetting reliability and lifetime specs, with re-qualification commonly taking 3–9 months and tying up 2–5 engineering FTEs. These time and resource burdens increase supplier bargaining power in negotiations. Long-term supply agreements (typically 3–5 years) reduce but do not eliminate this risk.

Process equipment dependence

Cleanroom tools, coating lines and precision assembly for inkjet/printed electronics are highly vendor-specific, giving OEMs leverage as service and spare parts often carry markups in the 30–50% range and aftermarket services can represent roughly 30–40% of equipment lifecycle value (2024 industry data). Downtime costs—routinely thousands to tens of thousands USD per hour in high-mix manufacturing—strengthen suppliers’ pricing power. Preventive maintenance contracts and onsite parts buffers materially reduce outage risk and supplier hold-up.

Ink and fluid ecosystem interdependence

Xaar's printhead performance hinges on compatibility with inks and functional fluids from specialist chemical formulators; co-development creates mutual dependence but supplier concentration can skew bargaining power when few meet required viscosity and particle-size specs.

- Approved-ink lists restrict customer flexibility

- Co-development raises switching costs

- Joint testing frameworks can rebalance terms

Potential for selective vertical integration

Xaar can insource certain modules or develop proprietary coatings to reduce supplier reliance, but capital intensity and steep learning curves limit the breadth of integration, preserving leverage with specialist suppliers for advanced parts.

Strategic partnerships or licensing can secure critical technologies and supply continuity without full vertical integration, enabling focus on commoditized modules while outsourcing high-tech components.

- Selective insourcing of commoditized modules

- Capital barriers and learning curves constrain scope

- Specialist suppliers retain leverage for advanced parts

- Partnerships secure key technologies without full integration

Supplier concentration raises risk — long lead times, high markups; partial insourcing offsets

Supplier concentration gives high bargaining power: ASIC lead times 20–30 weeks and nozzle qualification 6–12 months (2024), dual-sourcing costs $0.5–2m and 12–18 months, and vendor markups 30–50% with aftermarket ≈30–40% of lifecycle value. Co-development raises switching costs; selective insourcing/partnerships can partially mitigate risk.

| Metric | 2024 Value |

|---|---|

| ASIC lead time | 20–30 weeks |

| Nozzle qualification | 6–12 months |

| Dual-source cost/time | $0.5–2m / 12–18m |

| Vendor markups | 30–50% |

| Aftermarket share | 30–40% |

What is included in the product

Uncovers key drivers of competition, supplier and buyer power, entry barriers and substitutes specific to Xaar, identifying disruptive threats and strategic levers to protect market share; fully editable for reports and decks.

A concise one-sheet Porter's Five Forces for Xaar that maps competitive pressure via an instant spider chart—customize inputs, duplicate scenarios (pre/post regulation) and drop into pitch decks to streamline board-ready analysis without macros.

Customers Bargaining Power

Concentrated OEM and integrator base

Industrial printer OEMs and systems integrators buy in sizeable but episodic batches, with the largest OEMs and integrators commonly representing a majority of supplier revenues; their concentration enables aggressive price and service negotiations and contested initial terms for design wins. Design wins are sticky, yet losing a top account can reduce supplier volumes materially, often by more than 20% in a single year (2024 market observation).

High switching costs but credible alternatives

Printheads are deeply integrated into mechanics, electronics and software, so switching typically requires weeks to months of redesign, revalidation and operator retraining.

Despite these high switching costs, buyers in 2024 can pivot to credible rivals such as Kyocera, Ricoh, Epson, Seiko and Dimatix.

That available set of alternatives gives customers meaningful bargaining leverage despite the integration frictions.

Performance-driven procurement

Buyers prioritize throughput, drop placement accuracy (typically <20 microns), viscosity range and total cost of ownership when sourcing inkjet heads. Demonstrable gains in uptime and laydown—often cited as 20–30% productivity improvements in supplier case studies—justify premium pricing. Conversely, reliability issues trigger concessions; field performance data and extended warranties are primary bargaining chips in 2024 negotiations.

Aftermarket and service expectations

Customers demand rapid support, ready spares and timely firmware updates, making SLAs and operator training core negotiation points; strong service reduces price sensitivity while weak geographic or technical coverage amplifies buyer power.

- Service SLAs drive contract terms

- Spare parts availability lowers churn

- Firmware/updates affect uptime and loyalty

Cyclical capex and project timing

Cyclical capex in end-markets such as ceramics, labels and packaging—the global packaging market was about USD 1.03 trillion in 2024—means buyers batch purchases to meet budget windows, forcing discounts and contract timing leverage against suppliers like Xaar; deferred projects amplify pricing pressure while flexible financing and demo programs reduce churn and smooth order flows.

- Batch buying: forces seasonal discounts

- Deferred projects: raises price sensitivity

- Financing/demo: mitigates cyclicality

OEM buyer concentration threatens >20% supplier exposure amid 20–30% productivity pitch

Large OEMs/integradors concentrate purchases, enabling aggressive price/service negotiation and risking >20% supplier volume loss from a single lost design win (2024 observation).

High switching costs (weeks–months) are offset by multiple credible rivals, giving buyers meaningful leverage despite integration frictions.

Buyers prioritize TCO, uptime and accuracy; supplier case studies cite 20–30% productivity gains, and global packaging was ~USD 1.03T in 2024.

| Metric | 2024 Value |

|---|---|

| Single-account loss impact | >20% |

| Productivity uplift (supplier claims) | 20–30% |

| Global packaging market | USD 1.03T |

Same Document Delivered

Xaar Porter's Five Forces Analysis

This preview shows the exact Xaar Porter's Five Forces Analysis you'll receive upon purchase—no placeholders or mockups. The document displayed is the full, professionally formatted analysis ready for immediate download and use. You're viewing the same file you'll get instantly after payment.

Original: $10.00

-65%$10.00

$3.50Description

Don't Miss the Bigger Picture

Xaar operates in a niche industrial-printing market where supplier concentration and technological differentiation shape margins, while buyer power and emerging substitutes gradually shift competitive dynamics. Our snapshot highlights key threats and strategic levers for growth. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Xaar’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentrated critical materials

Core inputs like piezoelectric ceramics, precision nozzles and specialty ASICs come from a very limited global supplier base, leaving Xaar exposed; ASIC lead times in 2024 commonly run 20–30 weeks and nozzle qualification cycles exceed 6–12 months. Scarcity and certification hurdles give vendors pricing and lead-time leverage, with disruptions cascading into multi-month production delays. Dual-sourcing is feasible but typically costs $0.5–2m and 12–18 months to validate.

High switching and qualification costs

Substituting a printhead component requires extensive testing to meet jetting reliability and lifetime specs, with re-qualification commonly taking 3–9 months and tying up 2–5 engineering FTEs. These time and resource burdens increase supplier bargaining power in negotiations. Long-term supply agreements (typically 3–5 years) reduce but do not eliminate this risk.

Process equipment dependence

Cleanroom tools, coating lines and precision assembly for inkjet/printed electronics are highly vendor-specific, giving OEMs leverage as service and spare parts often carry markups in the 30–50% range and aftermarket services can represent roughly 30–40% of equipment lifecycle value (2024 industry data). Downtime costs—routinely thousands to tens of thousands USD per hour in high-mix manufacturing—strengthen suppliers’ pricing power. Preventive maintenance contracts and onsite parts buffers materially reduce outage risk and supplier hold-up.

Ink and fluid ecosystem interdependence

Xaar's printhead performance hinges on compatibility with inks and functional fluids from specialist chemical formulators; co-development creates mutual dependence but supplier concentration can skew bargaining power when few meet required viscosity and particle-size specs.

- Approved-ink lists restrict customer flexibility

- Co-development raises switching costs

- Joint testing frameworks can rebalance terms

Potential for selective vertical integration

Xaar can insource certain modules or develop proprietary coatings to reduce supplier reliance, but capital intensity and steep learning curves limit the breadth of integration, preserving leverage with specialist suppliers for advanced parts.

Strategic partnerships or licensing can secure critical technologies and supply continuity without full vertical integration, enabling focus on commoditized modules while outsourcing high-tech components.

- Selective insourcing of commoditized modules

- Capital barriers and learning curves constrain scope

- Specialist suppliers retain leverage for advanced parts

- Partnerships secure key technologies without full integration

Supplier concentration raises risk — long lead times, high markups; partial insourcing offsets

Supplier concentration gives high bargaining power: ASIC lead times 20–30 weeks and nozzle qualification 6–12 months (2024), dual-sourcing costs $0.5–2m and 12–18 months, and vendor markups 30–50% with aftermarket ≈30–40% of lifecycle value. Co-development raises switching costs; selective insourcing/partnerships can partially mitigate risk.

| Metric | 2024 Value |

|---|---|

| ASIC lead time | 20–30 weeks |

| Nozzle qualification | 6–12 months |

| Dual-source cost/time | $0.5–2m / 12–18m |

| Vendor markups | 30–50% |

| Aftermarket share | 30–40% |

What is included in the product

Uncovers key drivers of competition, supplier and buyer power, entry barriers and substitutes specific to Xaar, identifying disruptive threats and strategic levers to protect market share; fully editable for reports and decks.

A concise one-sheet Porter's Five Forces for Xaar that maps competitive pressure via an instant spider chart—customize inputs, duplicate scenarios (pre/post regulation) and drop into pitch decks to streamline board-ready analysis without macros.

Customers Bargaining Power

Concentrated OEM and integrator base

Industrial printer OEMs and systems integrators buy in sizeable but episodic batches, with the largest OEMs and integrators commonly representing a majority of supplier revenues; their concentration enables aggressive price and service negotiations and contested initial terms for design wins. Design wins are sticky, yet losing a top account can reduce supplier volumes materially, often by more than 20% in a single year (2024 market observation).

High switching costs but credible alternatives

Printheads are deeply integrated into mechanics, electronics and software, so switching typically requires weeks to months of redesign, revalidation and operator retraining.

Despite these high switching costs, buyers in 2024 can pivot to credible rivals such as Kyocera, Ricoh, Epson, Seiko and Dimatix.

That available set of alternatives gives customers meaningful bargaining leverage despite the integration frictions.

Performance-driven procurement

Buyers prioritize throughput, drop placement accuracy (typically <20 microns), viscosity range and total cost of ownership when sourcing inkjet heads. Demonstrable gains in uptime and laydown—often cited as 20–30% productivity improvements in supplier case studies—justify premium pricing. Conversely, reliability issues trigger concessions; field performance data and extended warranties are primary bargaining chips in 2024 negotiations.

Aftermarket and service expectations

Customers demand rapid support, ready spares and timely firmware updates, making SLAs and operator training core negotiation points; strong service reduces price sensitivity while weak geographic or technical coverage amplifies buyer power.

- Service SLAs drive contract terms

- Spare parts availability lowers churn

- Firmware/updates affect uptime and loyalty

Cyclical capex and project timing

Cyclical capex in end-markets such as ceramics, labels and packaging—the global packaging market was about USD 1.03 trillion in 2024—means buyers batch purchases to meet budget windows, forcing discounts and contract timing leverage against suppliers like Xaar; deferred projects amplify pricing pressure while flexible financing and demo programs reduce churn and smooth order flows.

- Batch buying: forces seasonal discounts

- Deferred projects: raises price sensitivity

- Financing/demo: mitigates cyclicality

OEM buyer concentration threatens >20% supplier exposure amid 20–30% productivity pitch

Large OEMs/integradors concentrate purchases, enabling aggressive price/service negotiation and risking >20% supplier volume loss from a single lost design win (2024 observation).

High switching costs (weeks–months) are offset by multiple credible rivals, giving buyers meaningful leverage despite integration frictions.

Buyers prioritize TCO, uptime and accuracy; supplier case studies cite 20–30% productivity gains, and global packaging was ~USD 1.03T in 2024.

| Metric | 2024 Value |

|---|---|

| Single-account loss impact | >20% |

| Productivity uplift (supplier claims) | 20–30% |

| Global packaging market | USD 1.03T |

Same Document Delivered

Xaar Porter's Five Forces Analysis

This preview shows the exact Xaar Porter's Five Forces Analysis you'll receive upon purchase—no placeholders or mockups. The document displayed is the full, professionally formatted analysis ready for immediate download and use. You're viewing the same file you'll get instantly after payment.