XCMG Construction Machinery PESTLE Analysis

Your Competitive Advantage Starts with This Report

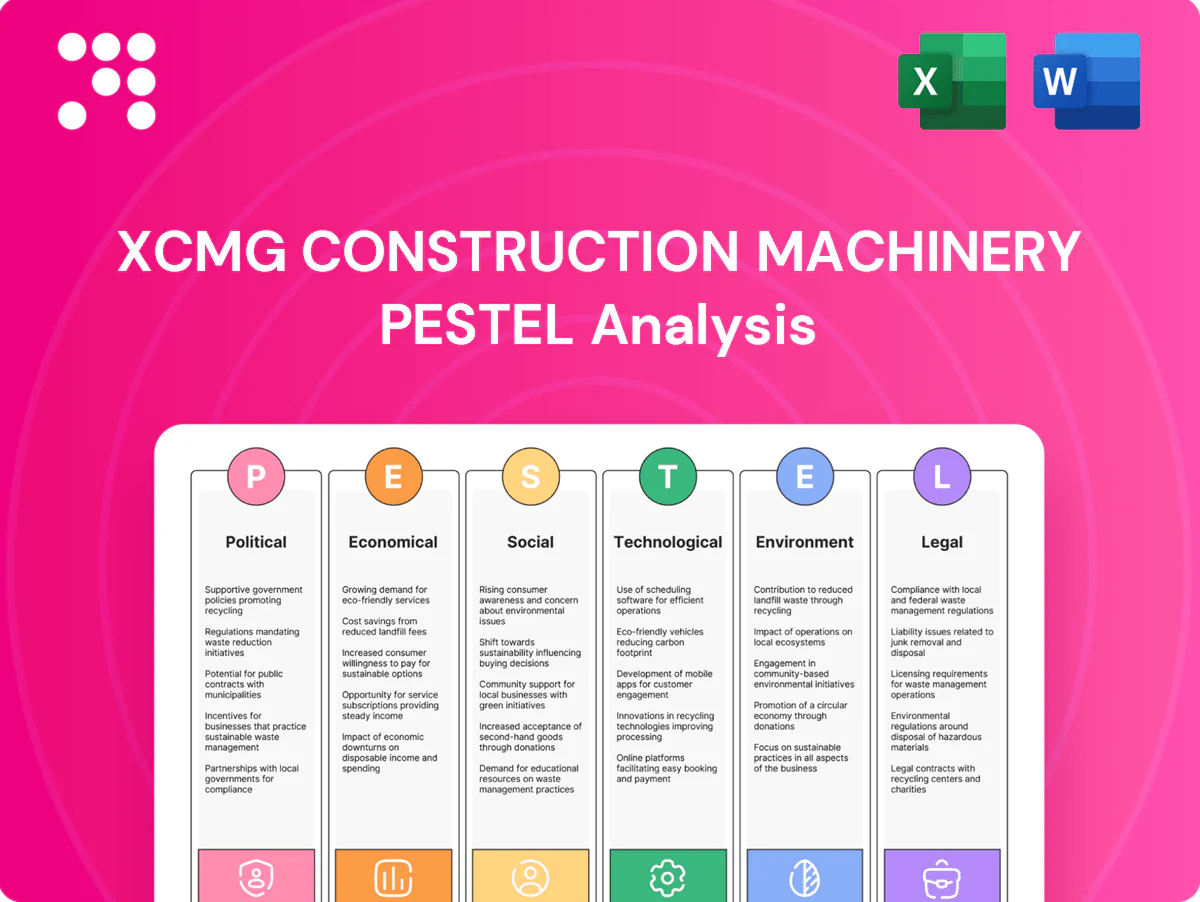

Unlock strategic clarity with our PESTLE Analysis of XCMG Construction Machinery—three to five concise insights into political, economic, social, technological, legal and environmental drivers shaping its outlook. Ideal for investors and strategists, this report surfaces risks and growth levers you can act on immediately. Purchase the full analysis for the complete, ready-to-use intelligence pack.

Political factors

Infrastructure-driven public spending

National and regional stimulus for roads, rail and housing drives cyclical demand for cranes, excavators and road machinery, and XCMG stands to gain when governments use infrastructure as an economic lever; China issued about 3.65 trillion yuan in special local government bonds in 2024 to fund projects. Delays in budget approvals or austerity can abruptly slow order intake, so monitoring multi-year public investment pipelines is critical for capacity planning.

Trade policy, tariffs, and localization

Tariffs, import quotas and localization mandates drive XCMG pricing and plant-siting choices; since 2020 India and several ASEAN states tightened local-assembly expectations and LATAM governments increased procurement preference for local content, prompting XCMG to expand CKD and JV models to protect margins and access public tenders. Rapid customs-duty adjustments in 2023–24 forced short-term supply‑chain reroutes to regional hubs.

Geopolitics and export controls

Sanctions, export licensing and dual-use scrutiny have tightened XCMG sales into sensitive markets, risking shipments to over 100 export destinations and complicating dealer networks. Geopolitical tensions among major economies raise logistics delays and increase financing costs via higher country-risk premiums. XCMG must bolster compliance programs, set explicit country-risk thresholds and expand market diversification. Political risk insurance can protect margins against sudden trade restrictions.

Government procurement and SOE relations

Government procurement and SOE projects drive large fleet orders for XCMG, with vendor qualification, local track record and firm aftersales commitments often decisive in tender awards; transparent bidding and anti-corruption safeguards are prerequisites for participation, while preferential policies for domestic champions can tilt competition.

- Vendor qualification: local track record

- Aftersales: maintenance guarantees

- Compliance: transparent bidding, anti-corruption

- Policy risk: preferential domestic support

Industrial policy and incentives

- Subsidies: boost EV/green product adoption

- Tax/land grants: lower upfront capex

- Compliance: local content, R&D, training required

- Risk: policy reversals can strand assets

Stimulus and green policy boost EV demand; trade rules and sanctions disrupt orders

Infrastructure stimulus (China 3.65 trillion yuan 2024 special bonds) and SOE procurement drive cyclical demand, but budget delays and austerity create order volatility. Trade measures and localization (India/ASEAN policies since 2020) force CKD/JV expansion. Sanctions and export controls constrain sales to 100+ destinations and raise financing costs. Green incentives (US IRA ~369bn) accelerate EV/green lineup.

| Factor | Key metric | Impact |

|---|---|---|

| Stimulus | 3.65tn CNY (2024) | ↑ orders |

| Trade/local | Policies since 2020 | ↑ local plants |

| Sanctions | 100+ markets | ↑ risk |

| Green policy | US IRA $369bn | ↑ EV demand |

What is included in the product

Explores how Political, Economic, Social, Technological, Environmental and Legal forces uniquely affect XCMG Construction Machinery, using current market and regulatory data to identify threats and opportunities. Designed for executives and investors, it delivers region-specific, data-backed insights and forward-looking scenarios in clean, ready-to-use format for strategy and financing decisions.

A clean, visually segmented PESTLE summary of XCMG Construction Machinery that relieves briefing pain points by enabling quick interpretation, easy annotations for region- or line-specific risks, and seamless inclusion into presentations or team-alignment decks.

Economic factors

Global CAPEX and construction cycles

Equipment demand tracks building permits, mining CAPEX and infrastructure backlogs, with the global construction equipment market estimated at about USD 120–130 billion in 2024 and mining CAPEX rising after 2022 commodity recoveries. Recessions defer fleet renewal while recoveries trigger pent‑up purchases, historically producing double‑digit upticks in orders within 12–18 months of recovery. XCMG can smooth cycles via rental fleets, captive financing and expanded aftermarket services; backlog quality and cancellation risk (contract size, funding status) are key leading indicators.

Commodity prices and mining activity

Elevated commodity prices—iron ore 62% Fe ~US$120/t (H1 2025), copper ~US$9,500/t (June 2025) and Brent ~US$82/bbl (June 2025)—support demand for heavy-duty mining machinery from XCMG. Mining downturns compress fleet utilization and spare-parts consumption, reducing short-term aftermarket sales. XCMGs exposure to resource economies diversifies revenue beyond construction. Long-term service and maintenance contracts help stabilize cash flow through commodity cycles.

Interest rates and credit availability

Higher global rates (US fed funds 5.25–5.50% in 2024–25, China 1‑yr LPR ~3.65%) raise financing costs for buyers and XCMG’s captive finance, squeezing margins. Tight credit cycles have reduced dealer inventories and retail sales in 2024, lowering OEM order visibility. Flexible financing, operating leases and used‑equipment trade‑ins have sustained volumes. Interest‑rate hedges and cash/liquidity buffers protect profitability.

FX volatility and cost inflation

FX volatility (RMB/USD swung roughly 6.7–7.3 in 2024) altered export pricing and raised costs for imported components, while steel, energy and freight inflation eroded margins—commodity swings reached double digits in parts of 2023–24. Local sourcing and price-indexed contracts reduced pass-through risk; active hedging and dynamic pricing preserved gross margins during currency and input-cost shocks.

- FX range: RMB/USD ~6.7–7.3 (2024)

- Commodity swings: double-digit moves in 2023–24

- Mitigants: local sourcing, price-indexed contracts, hedging, dynamic pricing

Emerging markets and BRI demand

- BRI scale: >1 trillion USD since 2013

- Developing Asia need: ~26 trillion USD to 2030

- UN urban growth: +2.5 billion by 2050

- Mitigants: local partners, credit terms, risk underwriting

Stimulus and green policy boost EV demand; trade rules and sanctions disrupt orders

Equipment demand ties to construction/mining CAPEX; global CE market ~USD 120–130bn (2024) with cyclic double‑digit rebounds post‑recovery. Elevated commodities (iron ore ~US$120/t H1 2025, copper ~US$9,500/t, Brent ~US$82/bbl) support mining gear; higher rates (US 5.25–5.50%, China 1‑yr LPR ~3.65%) and FX (RMB/USD 6.7–7.3) press financing and margins.

| Metric | Value |

|---|---|

| Global CE market (2024) | USD 120–130bn |

| Iron ore (H1 2025) | ~USD 120/t |

| Copper (Jun 2025) | ~USD 9,500/t |

| Brent (Jun 2025) | ~USD 82/bbl |

| US rates (2024–25) | 5.25–5.50% |

| China 1‑yr LPR | ~3.65% |

| RMB/USD (2024) | 6.7–7.3 |

Preview Before You Purchase

XCMG Construction Machinery PESTLE Analysis

This XCMG Construction Machinery PESTLE Analysis is a comprehensive, professionally structured report and the preview shown here is the exact document you’ll receive after purchase. It covers political, economic, social, technological, legal, and environmental factors affecting XCMG. The layout and content are final and fully formatted, ready to download immediately after payment.

Your Competitive Advantage Starts with This Report

Unlock strategic clarity with our PESTLE Analysis of XCMG Construction Machinery—three to five concise insights into political, economic, social, technological, legal and environmental drivers shaping its outlook. Ideal for investors and strategists, this report surfaces risks and growth levers you can act on immediately. Purchase the full analysis for the complete, ready-to-use intelligence pack.

Political factors

Infrastructure-driven public spending

National and regional stimulus for roads, rail and housing drives cyclical demand for cranes, excavators and road machinery, and XCMG stands to gain when governments use infrastructure as an economic lever; China issued about 3.65 trillion yuan in special local government bonds in 2024 to fund projects. Delays in budget approvals or austerity can abruptly slow order intake, so monitoring multi-year public investment pipelines is critical for capacity planning.

Trade policy, tariffs, and localization

Tariffs, import quotas and localization mandates drive XCMG pricing and plant-siting choices; since 2020 India and several ASEAN states tightened local-assembly expectations and LATAM governments increased procurement preference for local content, prompting XCMG to expand CKD and JV models to protect margins and access public tenders. Rapid customs-duty adjustments in 2023–24 forced short-term supply‑chain reroutes to regional hubs.

Geopolitics and export controls

Sanctions, export licensing and dual-use scrutiny have tightened XCMG sales into sensitive markets, risking shipments to over 100 export destinations and complicating dealer networks. Geopolitical tensions among major economies raise logistics delays and increase financing costs via higher country-risk premiums. XCMG must bolster compliance programs, set explicit country-risk thresholds and expand market diversification. Political risk insurance can protect margins against sudden trade restrictions.

Government procurement and SOE relations

Government procurement and SOE projects drive large fleet orders for XCMG, with vendor qualification, local track record and firm aftersales commitments often decisive in tender awards; transparent bidding and anti-corruption safeguards are prerequisites for participation, while preferential policies for domestic champions can tilt competition.

- Vendor qualification: local track record

- Aftersales: maintenance guarantees

- Compliance: transparent bidding, anti-corruption

- Policy risk: preferential domestic support

Industrial policy and incentives

- Subsidies: boost EV/green product adoption

- Tax/land grants: lower upfront capex

- Compliance: local content, R&D, training required

- Risk: policy reversals can strand assets

Stimulus and green policy boost EV demand; trade rules and sanctions disrupt orders

Infrastructure stimulus (China 3.65 trillion yuan 2024 special bonds) and SOE procurement drive cyclical demand, but budget delays and austerity create order volatility. Trade measures and localization (India/ASEAN policies since 2020) force CKD/JV expansion. Sanctions and export controls constrain sales to 100+ destinations and raise financing costs. Green incentives (US IRA ~369bn) accelerate EV/green lineup.

| Factor | Key metric | Impact |

|---|---|---|

| Stimulus | 3.65tn CNY (2024) | ↑ orders |

| Trade/local | Policies since 2020 | ↑ local plants |

| Sanctions | 100+ markets | ↑ risk |

| Green policy | US IRA $369bn | ↑ EV demand |

What is included in the product

Explores how Political, Economic, Social, Technological, Environmental and Legal forces uniquely affect XCMG Construction Machinery, using current market and regulatory data to identify threats and opportunities. Designed for executives and investors, it delivers region-specific, data-backed insights and forward-looking scenarios in clean, ready-to-use format for strategy and financing decisions.

A clean, visually segmented PESTLE summary of XCMG Construction Machinery that relieves briefing pain points by enabling quick interpretation, easy annotations for region- or line-specific risks, and seamless inclusion into presentations or team-alignment decks.

Economic factors

Global CAPEX and construction cycles

Equipment demand tracks building permits, mining CAPEX and infrastructure backlogs, with the global construction equipment market estimated at about USD 120–130 billion in 2024 and mining CAPEX rising after 2022 commodity recoveries. Recessions defer fleet renewal while recoveries trigger pent‑up purchases, historically producing double‑digit upticks in orders within 12–18 months of recovery. XCMG can smooth cycles via rental fleets, captive financing and expanded aftermarket services; backlog quality and cancellation risk (contract size, funding status) are key leading indicators.

Commodity prices and mining activity

Elevated commodity prices—iron ore 62% Fe ~US$120/t (H1 2025), copper ~US$9,500/t (June 2025) and Brent ~US$82/bbl (June 2025)—support demand for heavy-duty mining machinery from XCMG. Mining downturns compress fleet utilization and spare-parts consumption, reducing short-term aftermarket sales. XCMGs exposure to resource economies diversifies revenue beyond construction. Long-term service and maintenance contracts help stabilize cash flow through commodity cycles.

Interest rates and credit availability

Higher global rates (US fed funds 5.25–5.50% in 2024–25, China 1‑yr LPR ~3.65%) raise financing costs for buyers and XCMG’s captive finance, squeezing margins. Tight credit cycles have reduced dealer inventories and retail sales in 2024, lowering OEM order visibility. Flexible financing, operating leases and used‑equipment trade‑ins have sustained volumes. Interest‑rate hedges and cash/liquidity buffers protect profitability.

FX volatility and cost inflation

FX volatility (RMB/USD swung roughly 6.7–7.3 in 2024) altered export pricing and raised costs for imported components, while steel, energy and freight inflation eroded margins—commodity swings reached double digits in parts of 2023–24. Local sourcing and price-indexed contracts reduced pass-through risk; active hedging and dynamic pricing preserved gross margins during currency and input-cost shocks.

- FX range: RMB/USD ~6.7–7.3 (2024)

- Commodity swings: double-digit moves in 2023–24

- Mitigants: local sourcing, price-indexed contracts, hedging, dynamic pricing

Emerging markets and BRI demand

- BRI scale: >1 trillion USD since 2013

- Developing Asia need: ~26 trillion USD to 2030

- UN urban growth: +2.5 billion by 2050

- Mitigants: local partners, credit terms, risk underwriting

Stimulus and green policy boost EV demand; trade rules and sanctions disrupt orders

Equipment demand ties to construction/mining CAPEX; global CE market ~USD 120–130bn (2024) with cyclic double‑digit rebounds post‑recovery. Elevated commodities (iron ore ~US$120/t H1 2025, copper ~US$9,500/t, Brent ~US$82/bbl) support mining gear; higher rates (US 5.25–5.50%, China 1‑yr LPR ~3.65%) and FX (RMB/USD 6.7–7.3) press financing and margins.

| Metric | Value |

|---|---|

| Global CE market (2024) | USD 120–130bn |

| Iron ore (H1 2025) | ~USD 120/t |

| Copper (Jun 2025) | ~USD 9,500/t |

| Brent (Jun 2025) | ~USD 82/bbl |

| US rates (2024–25) | 5.25–5.50% |

| China 1‑yr LPR | ~3.65% |

| RMB/USD (2024) | 6.7–7.3 |

Preview Before You Purchase

XCMG Construction Machinery PESTLE Analysis

This XCMG Construction Machinery PESTLE Analysis is a comprehensive, professionally structured report and the preview shown here is the exact document you’ll receive after purchase. It covers political, economic, social, technological, legal, and environmental factors affecting XCMG. The layout and content are final and fully formatted, ready to download immediately after payment.

Original: $10.00

-65%$10.00

$3.50Description

Your Competitive Advantage Starts with This Report

Unlock strategic clarity with our PESTLE Analysis of XCMG Construction Machinery—three to five concise insights into political, economic, social, technological, legal and environmental drivers shaping its outlook. Ideal for investors and strategists, this report surfaces risks and growth levers you can act on immediately. Purchase the full analysis for the complete, ready-to-use intelligence pack.

Political factors

Infrastructure-driven public spending

National and regional stimulus for roads, rail and housing drives cyclical demand for cranes, excavators and road machinery, and XCMG stands to gain when governments use infrastructure as an economic lever; China issued about 3.65 trillion yuan in special local government bonds in 2024 to fund projects. Delays in budget approvals or austerity can abruptly slow order intake, so monitoring multi-year public investment pipelines is critical for capacity planning.

Trade policy, tariffs, and localization

Tariffs, import quotas and localization mandates drive XCMG pricing and plant-siting choices; since 2020 India and several ASEAN states tightened local-assembly expectations and LATAM governments increased procurement preference for local content, prompting XCMG to expand CKD and JV models to protect margins and access public tenders. Rapid customs-duty adjustments in 2023–24 forced short-term supply‑chain reroutes to regional hubs.

Geopolitics and export controls

Sanctions, export licensing and dual-use scrutiny have tightened XCMG sales into sensitive markets, risking shipments to over 100 export destinations and complicating dealer networks. Geopolitical tensions among major economies raise logistics delays and increase financing costs via higher country-risk premiums. XCMG must bolster compliance programs, set explicit country-risk thresholds and expand market diversification. Political risk insurance can protect margins against sudden trade restrictions.

Government procurement and SOE relations

Government procurement and SOE projects drive large fleet orders for XCMG, with vendor qualification, local track record and firm aftersales commitments often decisive in tender awards; transparent bidding and anti-corruption safeguards are prerequisites for participation, while preferential policies for domestic champions can tilt competition.

- Vendor qualification: local track record

- Aftersales: maintenance guarantees

- Compliance: transparent bidding, anti-corruption

- Policy risk: preferential domestic support

Industrial policy and incentives

- Subsidies: boost EV/green product adoption

- Tax/land grants: lower upfront capex

- Compliance: local content, R&D, training required

- Risk: policy reversals can strand assets

Stimulus and green policy boost EV demand; trade rules and sanctions disrupt orders

Infrastructure stimulus (China 3.65 trillion yuan 2024 special bonds) and SOE procurement drive cyclical demand, but budget delays and austerity create order volatility. Trade measures and localization (India/ASEAN policies since 2020) force CKD/JV expansion. Sanctions and export controls constrain sales to 100+ destinations and raise financing costs. Green incentives (US IRA ~369bn) accelerate EV/green lineup.

| Factor | Key metric | Impact |

|---|---|---|

| Stimulus | 3.65tn CNY (2024) | ↑ orders |

| Trade/local | Policies since 2020 | ↑ local plants |

| Sanctions | 100+ markets | ↑ risk |

| Green policy | US IRA $369bn | ↑ EV demand |

What is included in the product

Explores how Political, Economic, Social, Technological, Environmental and Legal forces uniquely affect XCMG Construction Machinery, using current market and regulatory data to identify threats and opportunities. Designed for executives and investors, it delivers region-specific, data-backed insights and forward-looking scenarios in clean, ready-to-use format for strategy and financing decisions.

A clean, visually segmented PESTLE summary of XCMG Construction Machinery that relieves briefing pain points by enabling quick interpretation, easy annotations for region- or line-specific risks, and seamless inclusion into presentations or team-alignment decks.

Economic factors

Global CAPEX and construction cycles

Equipment demand tracks building permits, mining CAPEX and infrastructure backlogs, with the global construction equipment market estimated at about USD 120–130 billion in 2024 and mining CAPEX rising after 2022 commodity recoveries. Recessions defer fleet renewal while recoveries trigger pent‑up purchases, historically producing double‑digit upticks in orders within 12–18 months of recovery. XCMG can smooth cycles via rental fleets, captive financing and expanded aftermarket services; backlog quality and cancellation risk (contract size, funding status) are key leading indicators.

Commodity prices and mining activity

Elevated commodity prices—iron ore 62% Fe ~US$120/t (H1 2025), copper ~US$9,500/t (June 2025) and Brent ~US$82/bbl (June 2025)—support demand for heavy-duty mining machinery from XCMG. Mining downturns compress fleet utilization and spare-parts consumption, reducing short-term aftermarket sales. XCMGs exposure to resource economies diversifies revenue beyond construction. Long-term service and maintenance contracts help stabilize cash flow through commodity cycles.

Interest rates and credit availability

Higher global rates (US fed funds 5.25–5.50% in 2024–25, China 1‑yr LPR ~3.65%) raise financing costs for buyers and XCMG’s captive finance, squeezing margins. Tight credit cycles have reduced dealer inventories and retail sales in 2024, lowering OEM order visibility. Flexible financing, operating leases and used‑equipment trade‑ins have sustained volumes. Interest‑rate hedges and cash/liquidity buffers protect profitability.

FX volatility and cost inflation

FX volatility (RMB/USD swung roughly 6.7–7.3 in 2024) altered export pricing and raised costs for imported components, while steel, energy and freight inflation eroded margins—commodity swings reached double digits in parts of 2023–24. Local sourcing and price-indexed contracts reduced pass-through risk; active hedging and dynamic pricing preserved gross margins during currency and input-cost shocks.

- FX range: RMB/USD ~6.7–7.3 (2024)

- Commodity swings: double-digit moves in 2023–24

- Mitigants: local sourcing, price-indexed contracts, hedging, dynamic pricing

Emerging markets and BRI demand

- BRI scale: >1 trillion USD since 2013

- Developing Asia need: ~26 trillion USD to 2030

- UN urban growth: +2.5 billion by 2050

- Mitigants: local partners, credit terms, risk underwriting

Stimulus and green policy boost EV demand; trade rules and sanctions disrupt orders

Equipment demand ties to construction/mining CAPEX; global CE market ~USD 120–130bn (2024) with cyclic double‑digit rebounds post‑recovery. Elevated commodities (iron ore ~US$120/t H1 2025, copper ~US$9,500/t, Brent ~US$82/bbl) support mining gear; higher rates (US 5.25–5.50%, China 1‑yr LPR ~3.65%) and FX (RMB/USD 6.7–7.3) press financing and margins.

| Metric | Value |

|---|---|

| Global CE market (2024) | USD 120–130bn |

| Iron ore (H1 2025) | ~USD 120/t |

| Copper (Jun 2025) | ~USD 9,500/t |

| Brent (Jun 2025) | ~USD 82/bbl |

| US rates (2024–25) | 5.25–5.50% |

| China 1‑yr LPR | ~3.65% |

| RMB/USD (2024) | 6.7–7.3 |

Preview Before You Purchase

XCMG Construction Machinery PESTLE Analysis

This XCMG Construction Machinery PESTLE Analysis is a comprehensive, professionally structured report and the preview shown here is the exact document you’ll receive after purchase. It covers political, economic, social, technological, legal, and environmental factors affecting XCMG. The layout and content are final and fully formatted, ready to download immediately after payment.