Xeris Business Model Canvas

Strategic Business Model Canvas: Actionable Blueprint to Scale Value and Revenue

Unlock the full strategic blueprint behind Xeris’s Business Model Canvas — three to five sentences reveal how it creates value, scales revenue streams, and sustains competitive advantages. This concise, editable canvas is ideal for investors, founders, and analysts seeking actionable insights. Purchase the full Word and Excel files to benchmark, plan, and execute with confidence.

Partnerships

Biopharma co-development partners

In 2024 Xeris partnered with larger biopharma companies to apply XeriSol and XeriJect to partner molecules, expanding the pipeline beyond internal assets. These co-development alliances de-risk programs through shared R&D and cost-sharing while enabling partner salesforce access for commercialization. Agreements typically structure upfronts, milestone payments and royalties, creating diversified revenue streams tied to partner progress.

Contract manufacturing organizations (CMOs)

External CMOs deliver sterile fill-finish, scale-up and redundancy for ready-to-use injectables, meeting cGMP and handling variable demand without heavy fixed capital outlay. They enable rapid tech transfer of XeriSol/XeriJect formulations and facilitate dual sourcing to mitigate supply-chain risk and ensure continuity. As of 2024 the global pharmaceutical CMO market exceeded $100 billion, underscoring outsourcing reliance.

Distributors, wholesalers, and specialty pharmacies

Channel partners—notably the three national wholesalers that together handle roughly 85% of U.S. pharmaceutical distribution—ensure Xeris products reach >95% of hospitals, clinics and retail outlets. Specialty pharmacies provide cold-chain logistics and patient onboarding, supporting biologic and temperature-sensitive formulations. Strong distributor relationships improve inventory turns and cut stockouts, while secure data-sharing enhances demand forecasting and adherence program effectiveness.

Payers and pharmacy benefit managers (PBMs)

Reimbursement partners—payers and PBMs—are critical for coverage decisions, tiering and prior authorization criteria; in 2024 the top three PBMs (CVS Caremark, Express Scripts, OptumRx) together serve roughly 70–80% of US lives, shaping formulary access. Value dossiers and real-world outcomes data support favorable placement and contracting, which can include rebates and value-based arrangements. Close collaboration lowers patient out-of-pocket barriers and expands adoption.

- Coverage influence: top three PBMs ~70–80% market share (2024)

- Evidence: dossiers + outcomes drive formulary tiering

- Contracts: rebates and VBRs common

- Patient access: reduces OOP and prior auth friction

Regulators, CROs, and key opinion leaders (KOLs)

Clinical research organizations streamline trial execution and post‑marketing studies, conducting an estimated 60% of global trial activities in 2024; KOLs guide study design, real‑world evidence and guideline inclusion, accelerating clinical adoption; proactive engagement with FDA and ex‑US agencies (review targets ~6–10 months) expedites approvals and increases market uptake and credibility.

- 60% — CRO share of trial activities (2024)

- 6–10 months — regulatory review target windows

- KOLs — faster guideline adoption and real‑world uptake

Co-development with biopharma shares R&D risk; CMOs, wholesalers and PBMs drive scale

Xeris leverages co-development deals with large biopharma to expand XeriSol/XeriJect, sharing R&D risk and revenue; CMOs provide cGMP fill-finish and scale (global CMO market >$100B in 2024); three national wholesalers cover ~85% US distribution and top 3 PBMs control ~70–80% payer access; CROs run ~60% of trials, KOLs and regulators shorten adoption timelines.

| Partner | Role | 2024 metric |

|---|---|---|

| Biopharma | Co-development/commercial | Upfronts/milestones/royalties |

| CMOs | Fill-finish/scale | Global market >$100B |

| Wholesalers/PBMs | Distribution/reimbursement | ~85% / 70–80% |

| CROs/KOLs | Trials/evidence | ~60% trial share |

What is included in the product

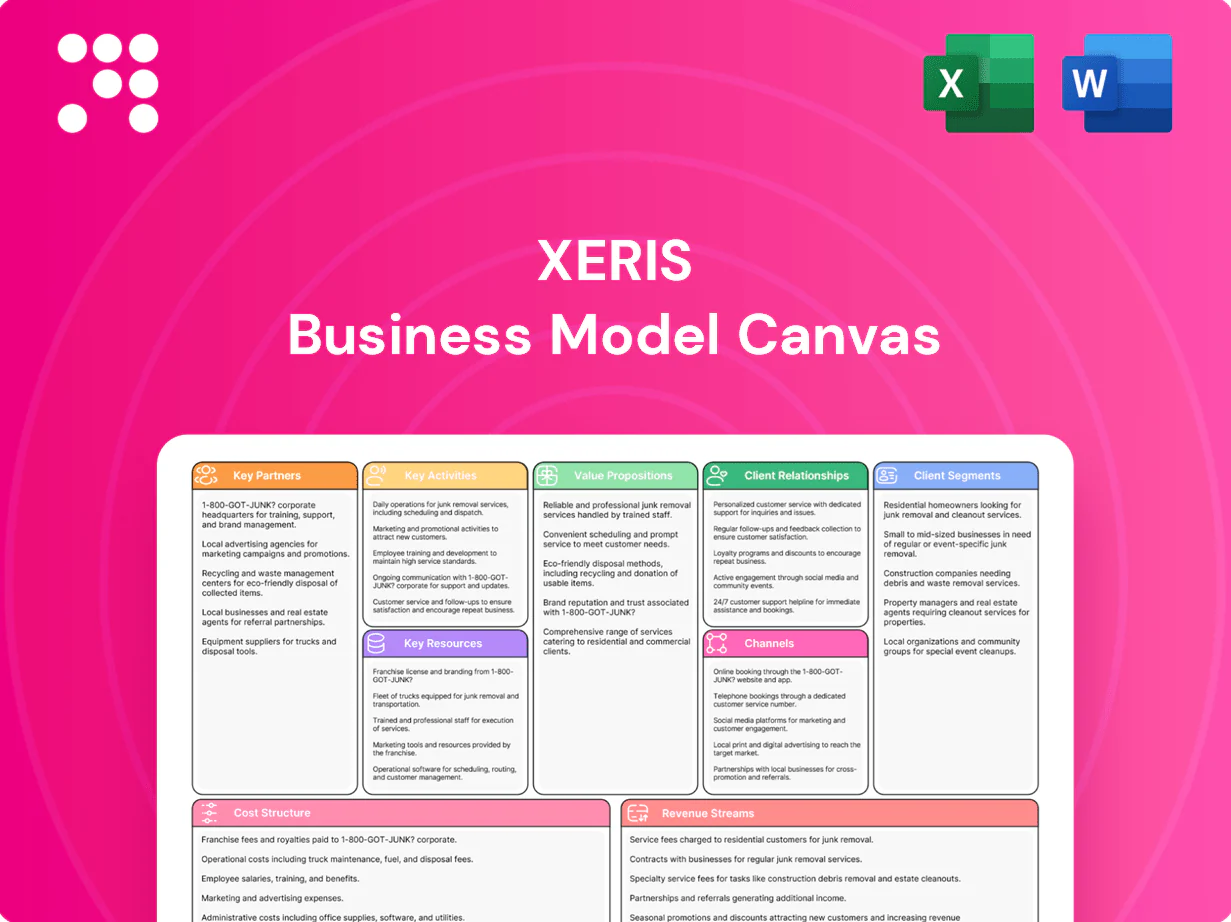

A comprehensive Business Model Canvas for Xeris detailing customer segments, channels, value propositions, revenue streams and cost structure across the 9 classic BMC blocks, aligned with real-world operations and strategic plans. Ideal for investor presentations and internal strategy, it includes SWOT-linked insights, competitive advantages and validation support to guide decision-making.

Condenses Xeris’ strategy into a digestible one-page canvas with editable cells to quickly relieve planning bottlenecks and save hours of formatting. Perfect for team collaboration, fast deliverables, and comparing models side-by-side.

Activities

Formulation innovation with XeriSol and XeriJect

Core activity converts unstable or inconvenient therapies into stable, ready-to-use injectable/infusible formats, enabling high-concentration, small-volume subcutaneous delivery (up to 200 mg/mL) to reduce dosing volume and improve adherence. Iterative formulation screening and stability testing—including accelerated and real-time 24-month stability studies—underpin product robustness. IP generation secures differentiated formats and freedom-to-operate.

Clinical development and regulatory submissions

Xeris conducts Phase 1–4 clinical programs to demonstrate safety, efficacy and usability advantages, with human factors and device compatibility studies embedded across trials. Regulatory dossiers and labeling strategies emphasize patient convenience and potential cost offsets versus hospitalization, informing payer discussions. Ongoing pharmacovigilance and post-approval commitments continued through 2024 to maintain compliance and real-world safety monitoring.

Manufacturing scale-up and quality management

Tech transfer to CMOs, validation and tight process controls in 2024 enabled scalable production to support millions of doses and ensured reliable supply for acute and chronic use-cases. Lot release testing and ongoing stability programs preserve product integrity across shelf life and regulatory filings. Capacity planning aligns CMO slots with seasonal and chronic demand patterns. Continuous improvement programs target sustained COGS reduction and greater yield over time.

Commercialization and market access

Field teams engage endocrinologists, hospitalists, and emergency departments to drive formulary adoption and protocol inclusion, supported by health economics evidence that demonstrates value to payers and hospitals. Digital outreach and patient programs increase awareness and adherence, while contracting with payers and integrated delivery networks expands market access.

- Field engagement: specialists, hospitalists, EDs

- HEOR: formulary & protocol support

- Digital/patient programs: awareness & adherence

- Payer/IDN contracting: broaden reach

Business development and licensing

Prospecting for molecules that benefit from XeriSol and XeriJect broadens optionality, targeting injectables and rescued oral-to-parenteral candidates to expand partnerable assets; in 2024 the team prioritized in-licensing opportunities to feed the pipeline.

Negotiating out-licensing, co-development, and regional deals monetizes the platform while alliance management enforces milestones and timelines to protect value; active deal terms in 2024 emphasized milestone and tiered royalties.

Disciplined portfolio pruning reallocates capital toward highest-ROI assets, reducing burn and increasing probability of value-creating exits and partnerships.

- Prospecting: XeriSol/XeriJect focus

- Licensing: out-lic, co-dev, regional monetization

- Alliances: milestone/timeline governance

- Pruning: capital to high-ROI assets

Core platform: high‑concentration SC therapeutics, 24‑month stability, millions of CMO doses

Core formulation converts unstable therapies to high‑concentration subcutaneous injectables; 24‑month stability and Ph1–4 clinical programs supported approvals and pharmacovigilance in 2024. Tech transfer to CMOs scaled supply for millions of doses; BD prioritized in‑licensing and milestone/tiered‑royalty deals to monetize the platform.

| Activity | 2024 metric |

|---|---|

| Stability trials | 24‑month RT |

| Supply | CMOs: millions doses |

| Clinical | Ph1–4 programs |

| BD | In‑licensing focus; milestone royalties |

Full Version Awaits

Business Model Canvas

The document you're previewing is the actual Xeris Business Model Canvas—not a mockup or sample—and contains the same structure, content, and layout you’ll receive after purchase. Upon ordering you’ll instantly get the complete, editable file ready for presentation, customization, and sharing.

Strategic Business Model Canvas: Actionable Blueprint to Scale Value and Revenue

Unlock the full strategic blueprint behind Xeris’s Business Model Canvas — three to five sentences reveal how it creates value, scales revenue streams, and sustains competitive advantages. This concise, editable canvas is ideal for investors, founders, and analysts seeking actionable insights. Purchase the full Word and Excel files to benchmark, plan, and execute with confidence.

Partnerships

Biopharma co-development partners

In 2024 Xeris partnered with larger biopharma companies to apply XeriSol and XeriJect to partner molecules, expanding the pipeline beyond internal assets. These co-development alliances de-risk programs through shared R&D and cost-sharing while enabling partner salesforce access for commercialization. Agreements typically structure upfronts, milestone payments and royalties, creating diversified revenue streams tied to partner progress.

Contract manufacturing organizations (CMOs)

External CMOs deliver sterile fill-finish, scale-up and redundancy for ready-to-use injectables, meeting cGMP and handling variable demand without heavy fixed capital outlay. They enable rapid tech transfer of XeriSol/XeriJect formulations and facilitate dual sourcing to mitigate supply-chain risk and ensure continuity. As of 2024 the global pharmaceutical CMO market exceeded $100 billion, underscoring outsourcing reliance.

Distributors, wholesalers, and specialty pharmacies

Channel partners—notably the three national wholesalers that together handle roughly 85% of U.S. pharmaceutical distribution—ensure Xeris products reach >95% of hospitals, clinics and retail outlets. Specialty pharmacies provide cold-chain logistics and patient onboarding, supporting biologic and temperature-sensitive formulations. Strong distributor relationships improve inventory turns and cut stockouts, while secure data-sharing enhances demand forecasting and adherence program effectiveness.

Payers and pharmacy benefit managers (PBMs)

Reimbursement partners—payers and PBMs—are critical for coverage decisions, tiering and prior authorization criteria; in 2024 the top three PBMs (CVS Caremark, Express Scripts, OptumRx) together serve roughly 70–80% of US lives, shaping formulary access. Value dossiers and real-world outcomes data support favorable placement and contracting, which can include rebates and value-based arrangements. Close collaboration lowers patient out-of-pocket barriers and expands adoption.

- Coverage influence: top three PBMs ~70–80% market share (2024)

- Evidence: dossiers + outcomes drive formulary tiering

- Contracts: rebates and VBRs common

- Patient access: reduces OOP and prior auth friction

Regulators, CROs, and key opinion leaders (KOLs)

Clinical research organizations streamline trial execution and post‑marketing studies, conducting an estimated 60% of global trial activities in 2024; KOLs guide study design, real‑world evidence and guideline inclusion, accelerating clinical adoption; proactive engagement with FDA and ex‑US agencies (review targets ~6–10 months) expedites approvals and increases market uptake and credibility.

- 60% — CRO share of trial activities (2024)

- 6–10 months — regulatory review target windows

- KOLs — faster guideline adoption and real‑world uptake

Co-development with biopharma shares R&D risk; CMOs, wholesalers and PBMs drive scale

Xeris leverages co-development deals with large biopharma to expand XeriSol/XeriJect, sharing R&D risk and revenue; CMOs provide cGMP fill-finish and scale (global CMO market >$100B in 2024); three national wholesalers cover ~85% US distribution and top 3 PBMs control ~70–80% payer access; CROs run ~60% of trials, KOLs and regulators shorten adoption timelines.

| Partner | Role | 2024 metric |

|---|---|---|

| Biopharma | Co-development/commercial | Upfronts/milestones/royalties |

| CMOs | Fill-finish/scale | Global market >$100B |

| Wholesalers/PBMs | Distribution/reimbursement | ~85% / 70–80% |

| CROs/KOLs | Trials/evidence | ~60% trial share |

What is included in the product

A comprehensive Business Model Canvas for Xeris detailing customer segments, channels, value propositions, revenue streams and cost structure across the 9 classic BMC blocks, aligned with real-world operations and strategic plans. Ideal for investor presentations and internal strategy, it includes SWOT-linked insights, competitive advantages and validation support to guide decision-making.

Condenses Xeris’ strategy into a digestible one-page canvas with editable cells to quickly relieve planning bottlenecks and save hours of formatting. Perfect for team collaboration, fast deliverables, and comparing models side-by-side.

Activities

Formulation innovation with XeriSol and XeriJect

Core activity converts unstable or inconvenient therapies into stable, ready-to-use injectable/infusible formats, enabling high-concentration, small-volume subcutaneous delivery (up to 200 mg/mL) to reduce dosing volume and improve adherence. Iterative formulation screening and stability testing—including accelerated and real-time 24-month stability studies—underpin product robustness. IP generation secures differentiated formats and freedom-to-operate.

Clinical development and regulatory submissions

Xeris conducts Phase 1–4 clinical programs to demonstrate safety, efficacy and usability advantages, with human factors and device compatibility studies embedded across trials. Regulatory dossiers and labeling strategies emphasize patient convenience and potential cost offsets versus hospitalization, informing payer discussions. Ongoing pharmacovigilance and post-approval commitments continued through 2024 to maintain compliance and real-world safety monitoring.

Manufacturing scale-up and quality management

Tech transfer to CMOs, validation and tight process controls in 2024 enabled scalable production to support millions of doses and ensured reliable supply for acute and chronic use-cases. Lot release testing and ongoing stability programs preserve product integrity across shelf life and regulatory filings. Capacity planning aligns CMO slots with seasonal and chronic demand patterns. Continuous improvement programs target sustained COGS reduction and greater yield over time.

Commercialization and market access

Field teams engage endocrinologists, hospitalists, and emergency departments to drive formulary adoption and protocol inclusion, supported by health economics evidence that demonstrates value to payers and hospitals. Digital outreach and patient programs increase awareness and adherence, while contracting with payers and integrated delivery networks expands market access.

- Field engagement: specialists, hospitalists, EDs

- HEOR: formulary & protocol support

- Digital/patient programs: awareness & adherence

- Payer/IDN contracting: broaden reach

Business development and licensing

Prospecting for molecules that benefit from XeriSol and XeriJect broadens optionality, targeting injectables and rescued oral-to-parenteral candidates to expand partnerable assets; in 2024 the team prioritized in-licensing opportunities to feed the pipeline.

Negotiating out-licensing, co-development, and regional deals monetizes the platform while alliance management enforces milestones and timelines to protect value; active deal terms in 2024 emphasized milestone and tiered royalties.

Disciplined portfolio pruning reallocates capital toward highest-ROI assets, reducing burn and increasing probability of value-creating exits and partnerships.

- Prospecting: XeriSol/XeriJect focus

- Licensing: out-lic, co-dev, regional monetization

- Alliances: milestone/timeline governance

- Pruning: capital to high-ROI assets

Core platform: high‑concentration SC therapeutics, 24‑month stability, millions of CMO doses

Core formulation converts unstable therapies to high‑concentration subcutaneous injectables; 24‑month stability and Ph1–4 clinical programs supported approvals and pharmacovigilance in 2024. Tech transfer to CMOs scaled supply for millions of doses; BD prioritized in‑licensing and milestone/tiered‑royalty deals to monetize the platform.

| Activity | 2024 metric |

|---|---|

| Stability trials | 24‑month RT |

| Supply | CMOs: millions doses |

| Clinical | Ph1–4 programs |

| BD | In‑licensing focus; milestone royalties |

Full Version Awaits

Business Model Canvas

The document you're previewing is the actual Xeris Business Model Canvas—not a mockup or sample—and contains the same structure, content, and layout you’ll receive after purchase. Upon ordering you’ll instantly get the complete, editable file ready for presentation, customization, and sharing.

Original: $10.00

-65%$10.00

$3.50Description

Strategic Business Model Canvas: Actionable Blueprint to Scale Value and Revenue

Unlock the full strategic blueprint behind Xeris’s Business Model Canvas — three to five sentences reveal how it creates value, scales revenue streams, and sustains competitive advantages. This concise, editable canvas is ideal for investors, founders, and analysts seeking actionable insights. Purchase the full Word and Excel files to benchmark, plan, and execute with confidence.

Partnerships

Biopharma co-development partners

In 2024 Xeris partnered with larger biopharma companies to apply XeriSol and XeriJect to partner molecules, expanding the pipeline beyond internal assets. These co-development alliances de-risk programs through shared R&D and cost-sharing while enabling partner salesforce access for commercialization. Agreements typically structure upfronts, milestone payments and royalties, creating diversified revenue streams tied to partner progress.

Contract manufacturing organizations (CMOs)

External CMOs deliver sterile fill-finish, scale-up and redundancy for ready-to-use injectables, meeting cGMP and handling variable demand without heavy fixed capital outlay. They enable rapid tech transfer of XeriSol/XeriJect formulations and facilitate dual sourcing to mitigate supply-chain risk and ensure continuity. As of 2024 the global pharmaceutical CMO market exceeded $100 billion, underscoring outsourcing reliance.

Distributors, wholesalers, and specialty pharmacies

Channel partners—notably the three national wholesalers that together handle roughly 85% of U.S. pharmaceutical distribution—ensure Xeris products reach >95% of hospitals, clinics and retail outlets. Specialty pharmacies provide cold-chain logistics and patient onboarding, supporting biologic and temperature-sensitive formulations. Strong distributor relationships improve inventory turns and cut stockouts, while secure data-sharing enhances demand forecasting and adherence program effectiveness.

Payers and pharmacy benefit managers (PBMs)

Reimbursement partners—payers and PBMs—are critical for coverage decisions, tiering and prior authorization criteria; in 2024 the top three PBMs (CVS Caremark, Express Scripts, OptumRx) together serve roughly 70–80% of US lives, shaping formulary access. Value dossiers and real-world outcomes data support favorable placement and contracting, which can include rebates and value-based arrangements. Close collaboration lowers patient out-of-pocket barriers and expands adoption.

- Coverage influence: top three PBMs ~70–80% market share (2024)

- Evidence: dossiers + outcomes drive formulary tiering

- Contracts: rebates and VBRs common

- Patient access: reduces OOP and prior auth friction

Regulators, CROs, and key opinion leaders (KOLs)

Clinical research organizations streamline trial execution and post‑marketing studies, conducting an estimated 60% of global trial activities in 2024; KOLs guide study design, real‑world evidence and guideline inclusion, accelerating clinical adoption; proactive engagement with FDA and ex‑US agencies (review targets ~6–10 months) expedites approvals and increases market uptake and credibility.

- 60% — CRO share of trial activities (2024)

- 6–10 months — regulatory review target windows

- KOLs — faster guideline adoption and real‑world uptake

Co-development with biopharma shares R&D risk; CMOs, wholesalers and PBMs drive scale

Xeris leverages co-development deals with large biopharma to expand XeriSol/XeriJect, sharing R&D risk and revenue; CMOs provide cGMP fill-finish and scale (global CMO market >$100B in 2024); three national wholesalers cover ~85% US distribution and top 3 PBMs control ~70–80% payer access; CROs run ~60% of trials, KOLs and regulators shorten adoption timelines.

| Partner | Role | 2024 metric |

|---|---|---|

| Biopharma | Co-development/commercial | Upfronts/milestones/royalties |

| CMOs | Fill-finish/scale | Global market >$100B |

| Wholesalers/PBMs | Distribution/reimbursement | ~85% / 70–80% |

| CROs/KOLs | Trials/evidence | ~60% trial share |

What is included in the product

A comprehensive Business Model Canvas for Xeris detailing customer segments, channels, value propositions, revenue streams and cost structure across the 9 classic BMC blocks, aligned with real-world operations and strategic plans. Ideal for investor presentations and internal strategy, it includes SWOT-linked insights, competitive advantages and validation support to guide decision-making.

Condenses Xeris’ strategy into a digestible one-page canvas with editable cells to quickly relieve planning bottlenecks and save hours of formatting. Perfect for team collaboration, fast deliverables, and comparing models side-by-side.

Activities

Formulation innovation with XeriSol and XeriJect

Core activity converts unstable or inconvenient therapies into stable, ready-to-use injectable/infusible formats, enabling high-concentration, small-volume subcutaneous delivery (up to 200 mg/mL) to reduce dosing volume and improve adherence. Iterative formulation screening and stability testing—including accelerated and real-time 24-month stability studies—underpin product robustness. IP generation secures differentiated formats and freedom-to-operate.

Clinical development and regulatory submissions

Xeris conducts Phase 1–4 clinical programs to demonstrate safety, efficacy and usability advantages, with human factors and device compatibility studies embedded across trials. Regulatory dossiers and labeling strategies emphasize patient convenience and potential cost offsets versus hospitalization, informing payer discussions. Ongoing pharmacovigilance and post-approval commitments continued through 2024 to maintain compliance and real-world safety monitoring.

Manufacturing scale-up and quality management

Tech transfer to CMOs, validation and tight process controls in 2024 enabled scalable production to support millions of doses and ensured reliable supply for acute and chronic use-cases. Lot release testing and ongoing stability programs preserve product integrity across shelf life and regulatory filings. Capacity planning aligns CMO slots with seasonal and chronic demand patterns. Continuous improvement programs target sustained COGS reduction and greater yield over time.

Commercialization and market access

Field teams engage endocrinologists, hospitalists, and emergency departments to drive formulary adoption and protocol inclusion, supported by health economics evidence that demonstrates value to payers and hospitals. Digital outreach and patient programs increase awareness and adherence, while contracting with payers and integrated delivery networks expands market access.

- Field engagement: specialists, hospitalists, EDs

- HEOR: formulary & protocol support

- Digital/patient programs: awareness & adherence

- Payer/IDN contracting: broaden reach

Business development and licensing

Prospecting for molecules that benefit from XeriSol and XeriJect broadens optionality, targeting injectables and rescued oral-to-parenteral candidates to expand partnerable assets; in 2024 the team prioritized in-licensing opportunities to feed the pipeline.

Negotiating out-licensing, co-development, and regional deals monetizes the platform while alliance management enforces milestones and timelines to protect value; active deal terms in 2024 emphasized milestone and tiered royalties.

Disciplined portfolio pruning reallocates capital toward highest-ROI assets, reducing burn and increasing probability of value-creating exits and partnerships.

- Prospecting: XeriSol/XeriJect focus

- Licensing: out-lic, co-dev, regional monetization

- Alliances: milestone/timeline governance

- Pruning: capital to high-ROI assets

Core platform: high‑concentration SC therapeutics, 24‑month stability, millions of CMO doses

Core formulation converts unstable therapies to high‑concentration subcutaneous injectables; 24‑month stability and Ph1–4 clinical programs supported approvals and pharmacovigilance in 2024. Tech transfer to CMOs scaled supply for millions of doses; BD prioritized in‑licensing and milestone/tiered‑royalty deals to monetize the platform.

| Activity | 2024 metric |

|---|---|

| Stability trials | 24‑month RT |

| Supply | CMOs: millions doses |

| Clinical | Ph1–4 programs |

| BD | In‑licensing focus; milestone royalties |

Full Version Awaits

Business Model Canvas

The document you're previewing is the actual Xeris Business Model Canvas—not a mockup or sample—and contains the same structure, content, and layout you’ll receive after purchase. Upon ordering you’ll instantly get the complete, editable file ready for presentation, customization, and sharing.