Uxin Porter's Five Forces Analysis

Don't Miss the Bigger Picture

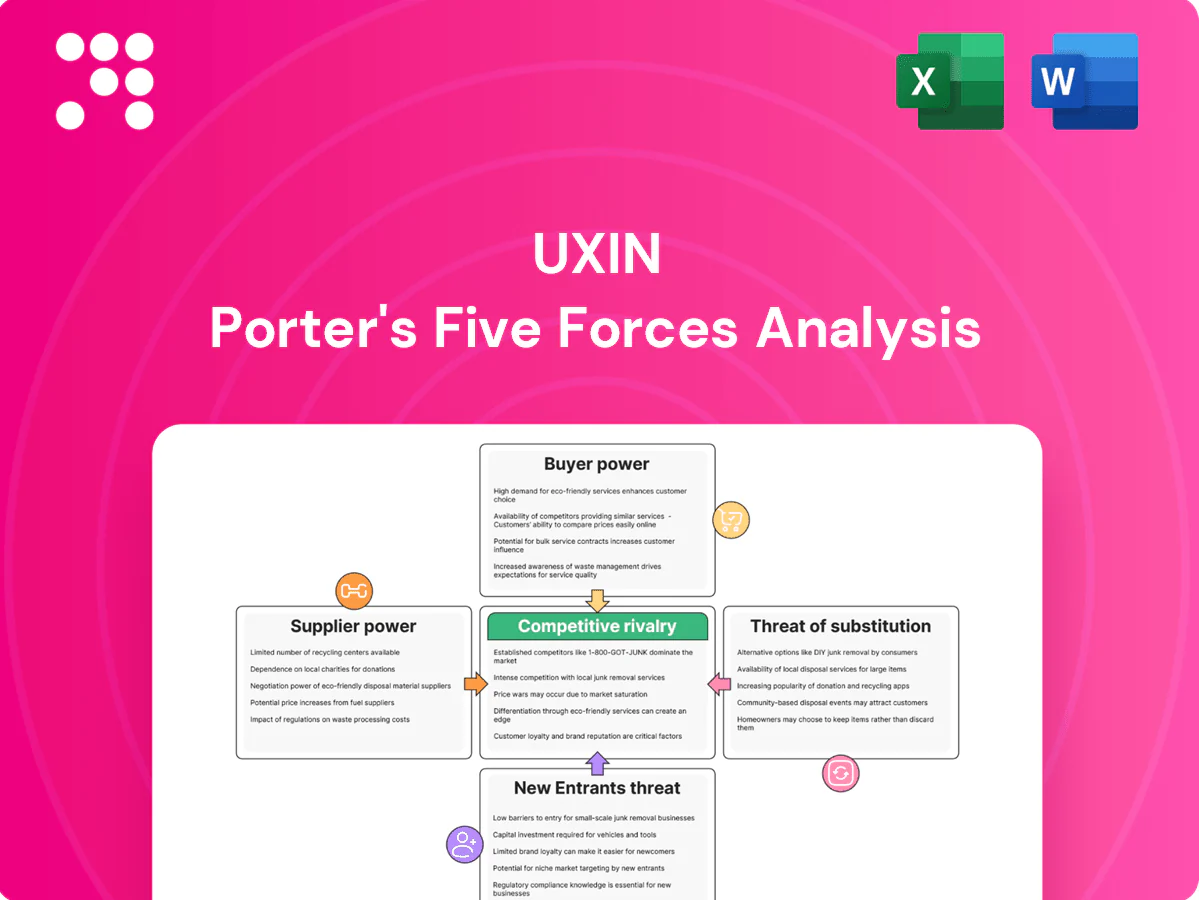

Uxin’s Porter's Five Forces snapshot highlights intense rivalry, moderate buyer power, supplier constraints, emerging substitute threats, and barriers that temper new entrants. These dynamics shape pricing, margins, and strategic options for the company. This brief only scratches the surface—unlock the full Porter's Five Forces Analysis to explore force-by-force ratings, visuals, and actionable implications for investment and strategy.

Suppliers Bargaining Power

Fragmented vehicle sources

Supply for Uxin stems from numerous individual sellers and small dealers, limiting any single supplier’s leverage; China’s used-car market handled about 22.3 million transactions in 2024, sustaining a broad funnel. Uxin can curate inventory and set quality standards across thousands of listings, using scale to negotiate prices and selection. Fragmentation empowers price negotiation, though localized shortages in hot models can temporarily raise supplier power.

Dependence on inspection partners

Quality assurance for Uxin depends heavily on inspection staff, tools and third-party providers, with inspection processes accounting for a meaningful portion of pre-sale costs; Uxin reported expanding its in-house inspection team by 30% in 2024 to reduce reliance on partners.

Financing and capital providers

Auto-loan partners significantly influence Uxin’s approval rates and take rates, and tighter credit cycles raise funding costs or reduce approvals, increasing supplier power. In 2024 China’s one-year LPR remained at 3.45%, constraining cheap funding and pressuring margins for originators. Diversifying across multiple lenders and offering flexible products lowers concentration risk and improves resilience. Embedding financing data into underwriting cuts observed default rates, strengthening Uxin’s bargaining position.

Logistics and reconditioning capacity

Transporters, warehouses and refurbishers directly shape turnaround times and unit economics; peak-season capacity constraints can inflate logistics prices 10-30% and add 2–7 days to cycle time. Multi-vendor networks and volume commitments typically cut logistics cost 5–15%. Higher geographic density enables stronger SLAs and can lower cost-per-km by around 10% in dense clusters.

- Transporters: impact on turnaround/unit cost

- Peaks: prices +10–30%, time +2–7 days

- Network/volume: cost −5–15%

- Geographic density: SLA & cost-per-km ≈ −10%

Data and traffic channels

Ad platforms, map/traffic partners and data APIs control lead flow and verification, giving suppliers pricing leverage—iResearch 2024 estimates the top 3 mobile ad platforms capture about 70% of ad spend—so dependency on search/short-video inflates CPCs. Building direct mobile traffic, CRM and first-party data reduces reliance and improves verification, strengthening Uxin’s negotiating position.

- Platform concentration ~70% (iResearch 2024)

- Direct mobile/CRM lowers acquisition costs

- First-party data => higher bargaining power

- APIs/map partners control lead quality and verification

Fragmented sellers (22.3M) curb supplier power; inspections +30%, LPR 3.45%

Supplier power is limited by fragmented individual sellers amid 22.3M used-car transactions in China (2024), enabling Uxin to negotiate on price and quality. Dependence on inspections (in-house team +30% in 2024) and lenders (one-year LPR 3.45% in 2024) creates pockets of supplier leverage. Ad/platform concentration (~70% top‑3 ad spend, iResearch 2024) raises acquisition costs until first‑party traffic scales.

| Supplier | Driver | 2024 metric |

|---|---|---|

| Sellers | Fragmentation | 22.3M txns |

| Inspections | Staff/tools | +30% in‑house |

| Lenders | Funding/cost | LPR 3.45% |

| Ad platforms | Lead costs | Top3 ~70% |

What is included in the product

Tailored Porter’s Five Forces analysis for Uxin uncovering competitive drivers, buyer and supplier power, entry barriers, substitutes, and disruptive threats, with strategic commentary and actionable insights to inform investor materials, strategy decks, or academic projects.

A concise Uxin Porter's Five Forces summary that pinpoints competitive pain points and suggests targeted strategic levers—perfect for rapid decision-making, boardroom slides, or quick integration into broader strategy decks.

Customers Bargaining Power

High price transparency

With ~26 million used-car transactions in China in 2023 and online channels capturing roughly 20% of volume, buyers easily compare listings on Uxin, Guazi, Autohome and offline dealers. VIN checks and publicly available histories increase buyer leverage, forcing transparent pricing. Low switching costs push platforms to compete on total cost and assurances; Uxin must differentiate with certified quality inspections and robust warranties.

Sensitivity to total ownership cost

Customers weigh price, financing rate, insurance, taxes, and after-sales; in China the used-car market exceeded 13 million transactions in 2023, making total ownership cost decisive. Bundled value—warranty, certified inspection, trade-in credit—can offset headline price pressure. Financing promotions often sway buyers but compress dealer margins. Clear TCO communication reduces haggling and returns.

Trust and assurance demands

Buyers in 2C increasingly demand reliable inspections, 7–15 day return windows, and guarantees; strong return and escrow policies raise conversion but shift bargaining power to buyers. Transparent claims processes and escrow mechanisms shape perceived fairness and reduce chargebacks. In 2024, platforms report that data-backed grading cuts dispute rates and coupon costs materially, improving unit economics.

Regional inventory preferences

Local tastes and emissions rules materially shape model desirability, shifting buyer preference toward compliant, regionally popular trims; when local stock is thin buyers frequently demand transfers or price concessions, and longer cross-province logistics further strengthen buyer bargaining power; dynamic pricing and real-time inventory balancing reduce forced concessions by matching supply to demand.

- regional_compliance

- stock_shortage

- logistics_delay

- dynamic_pricing

Review and social influence

Ratings, KOLs and social forums magnify buyer voice: 2024 data show review-driven leads rose ~20%, making negative virality able to force fee concessions and faster returns, raising buyer leverage over service terms; proactive service recovery and transparent reporting cut dispute rates and preserve margins; referral programs convert influence into growth while capping acquisition cost per user.

- Ratings impact: +20% review-driven leads (2024)

- KOLs/social reach: amplifies complaints

- Recovery/reporting: lowers dispute rates

- Referrals: growth with controlled CAC

Buyers win: 26M trades, 20% online sway

Buyers hold high bargaining power: ~26M used-car transactions in China in 2023 with ~20% online share lets shoppers compare listings across Uxin, Guazi and dealers, pressuring price and guarantees. Low switching costs and VIN/history transparency force platforms to compete on TCO, warranties and inspection quality. Review-driven leads rose ~20% in 2024, amplifying buyer leverage.

| Metric | Value |

|---|---|

| 2023 used-car volume | ~26M |

| Online share | ~20% |

| Review-driven leads (2024) | +20% |

Full Version Awaits

Uxin Porter's Five Forces Analysis

This preview shows the exact document you'll receive immediately after purchase—no surprises, no placeholders. Uxin Porter's Five Forces Analysis examines competitive rivalry, supplier and buyer power, threat of substitutes, and barriers to entry, offering actionable insights and strategic recommendations tailored to Uxin's used‑car marketplace.

Don't Miss the Bigger Picture

Uxin’s Porter's Five Forces snapshot highlights intense rivalry, moderate buyer power, supplier constraints, emerging substitute threats, and barriers that temper new entrants. These dynamics shape pricing, margins, and strategic options for the company. This brief only scratches the surface—unlock the full Porter's Five Forces Analysis to explore force-by-force ratings, visuals, and actionable implications for investment and strategy.

Suppliers Bargaining Power

Fragmented vehicle sources

Supply for Uxin stems from numerous individual sellers and small dealers, limiting any single supplier’s leverage; China’s used-car market handled about 22.3 million transactions in 2024, sustaining a broad funnel. Uxin can curate inventory and set quality standards across thousands of listings, using scale to negotiate prices and selection. Fragmentation empowers price negotiation, though localized shortages in hot models can temporarily raise supplier power.

Dependence on inspection partners

Quality assurance for Uxin depends heavily on inspection staff, tools and third-party providers, with inspection processes accounting for a meaningful portion of pre-sale costs; Uxin reported expanding its in-house inspection team by 30% in 2024 to reduce reliance on partners.

Financing and capital providers

Auto-loan partners significantly influence Uxin’s approval rates and take rates, and tighter credit cycles raise funding costs or reduce approvals, increasing supplier power. In 2024 China’s one-year LPR remained at 3.45%, constraining cheap funding and pressuring margins for originators. Diversifying across multiple lenders and offering flexible products lowers concentration risk and improves resilience. Embedding financing data into underwriting cuts observed default rates, strengthening Uxin’s bargaining position.

Logistics and reconditioning capacity

Transporters, warehouses and refurbishers directly shape turnaround times and unit economics; peak-season capacity constraints can inflate logistics prices 10-30% and add 2–7 days to cycle time. Multi-vendor networks and volume commitments typically cut logistics cost 5–15%. Higher geographic density enables stronger SLAs and can lower cost-per-km by around 10% in dense clusters.

- Transporters: impact on turnaround/unit cost

- Peaks: prices +10–30%, time +2–7 days

- Network/volume: cost −5–15%

- Geographic density: SLA & cost-per-km ≈ −10%

Data and traffic channels

Ad platforms, map/traffic partners and data APIs control lead flow and verification, giving suppliers pricing leverage—iResearch 2024 estimates the top 3 mobile ad platforms capture about 70% of ad spend—so dependency on search/short-video inflates CPCs. Building direct mobile traffic, CRM and first-party data reduces reliance and improves verification, strengthening Uxin’s negotiating position.

- Platform concentration ~70% (iResearch 2024)

- Direct mobile/CRM lowers acquisition costs

- First-party data => higher bargaining power

- APIs/map partners control lead quality and verification

Fragmented sellers (22.3M) curb supplier power; inspections +30%, LPR 3.45%

Supplier power is limited by fragmented individual sellers amid 22.3M used-car transactions in China (2024), enabling Uxin to negotiate on price and quality. Dependence on inspections (in-house team +30% in 2024) and lenders (one-year LPR 3.45% in 2024) creates pockets of supplier leverage. Ad/platform concentration (~70% top‑3 ad spend, iResearch 2024) raises acquisition costs until first‑party traffic scales.

| Supplier | Driver | 2024 metric |

|---|---|---|

| Sellers | Fragmentation | 22.3M txns |

| Inspections | Staff/tools | +30% in‑house |

| Lenders | Funding/cost | LPR 3.45% |

| Ad platforms | Lead costs | Top3 ~70% |

What is included in the product

Tailored Porter’s Five Forces analysis for Uxin uncovering competitive drivers, buyer and supplier power, entry barriers, substitutes, and disruptive threats, with strategic commentary and actionable insights to inform investor materials, strategy decks, or academic projects.

A concise Uxin Porter's Five Forces summary that pinpoints competitive pain points and suggests targeted strategic levers—perfect for rapid decision-making, boardroom slides, or quick integration into broader strategy decks.

Customers Bargaining Power

High price transparency

With ~26 million used-car transactions in China in 2023 and online channels capturing roughly 20% of volume, buyers easily compare listings on Uxin, Guazi, Autohome and offline dealers. VIN checks and publicly available histories increase buyer leverage, forcing transparent pricing. Low switching costs push platforms to compete on total cost and assurances; Uxin must differentiate with certified quality inspections and robust warranties.

Sensitivity to total ownership cost

Customers weigh price, financing rate, insurance, taxes, and after-sales; in China the used-car market exceeded 13 million transactions in 2023, making total ownership cost decisive. Bundled value—warranty, certified inspection, trade-in credit—can offset headline price pressure. Financing promotions often sway buyers but compress dealer margins. Clear TCO communication reduces haggling and returns.

Trust and assurance demands

Buyers in 2C increasingly demand reliable inspections, 7–15 day return windows, and guarantees; strong return and escrow policies raise conversion but shift bargaining power to buyers. Transparent claims processes and escrow mechanisms shape perceived fairness and reduce chargebacks. In 2024, platforms report that data-backed grading cuts dispute rates and coupon costs materially, improving unit economics.

Regional inventory preferences

Local tastes and emissions rules materially shape model desirability, shifting buyer preference toward compliant, regionally popular trims; when local stock is thin buyers frequently demand transfers or price concessions, and longer cross-province logistics further strengthen buyer bargaining power; dynamic pricing and real-time inventory balancing reduce forced concessions by matching supply to demand.

- regional_compliance

- stock_shortage

- logistics_delay

- dynamic_pricing

Review and social influence

Ratings, KOLs and social forums magnify buyer voice: 2024 data show review-driven leads rose ~20%, making negative virality able to force fee concessions and faster returns, raising buyer leverage over service terms; proactive service recovery and transparent reporting cut dispute rates and preserve margins; referral programs convert influence into growth while capping acquisition cost per user.

- Ratings impact: +20% review-driven leads (2024)

- KOLs/social reach: amplifies complaints

- Recovery/reporting: lowers dispute rates

- Referrals: growth with controlled CAC

Buyers win: 26M trades, 20% online sway

Buyers hold high bargaining power: ~26M used-car transactions in China in 2023 with ~20% online share lets shoppers compare listings across Uxin, Guazi and dealers, pressuring price and guarantees. Low switching costs and VIN/history transparency force platforms to compete on TCO, warranties and inspection quality. Review-driven leads rose ~20% in 2024, amplifying buyer leverage.

| Metric | Value |

|---|---|

| 2023 used-car volume | ~26M |

| Online share | ~20% |

| Review-driven leads (2024) | +20% |

Full Version Awaits

Uxin Porter's Five Forces Analysis

This preview shows the exact document you'll receive immediately after purchase—no surprises, no placeholders. Uxin Porter's Five Forces Analysis examines competitive rivalry, supplier and buyer power, threat of substitutes, and barriers to entry, offering actionable insights and strategic recommendations tailored to Uxin's used‑car marketplace.

Original: $10.00

-65%$10.00

$3.50Description

Don't Miss the Bigger Picture

Uxin’s Porter's Five Forces snapshot highlights intense rivalry, moderate buyer power, supplier constraints, emerging substitute threats, and barriers that temper new entrants. These dynamics shape pricing, margins, and strategic options for the company. This brief only scratches the surface—unlock the full Porter's Five Forces Analysis to explore force-by-force ratings, visuals, and actionable implications for investment and strategy.

Suppliers Bargaining Power

Fragmented vehicle sources

Supply for Uxin stems from numerous individual sellers and small dealers, limiting any single supplier’s leverage; China’s used-car market handled about 22.3 million transactions in 2024, sustaining a broad funnel. Uxin can curate inventory and set quality standards across thousands of listings, using scale to negotiate prices and selection. Fragmentation empowers price negotiation, though localized shortages in hot models can temporarily raise supplier power.

Dependence on inspection partners

Quality assurance for Uxin depends heavily on inspection staff, tools and third-party providers, with inspection processes accounting for a meaningful portion of pre-sale costs; Uxin reported expanding its in-house inspection team by 30% in 2024 to reduce reliance on partners.

Financing and capital providers

Auto-loan partners significantly influence Uxin’s approval rates and take rates, and tighter credit cycles raise funding costs or reduce approvals, increasing supplier power. In 2024 China’s one-year LPR remained at 3.45%, constraining cheap funding and pressuring margins for originators. Diversifying across multiple lenders and offering flexible products lowers concentration risk and improves resilience. Embedding financing data into underwriting cuts observed default rates, strengthening Uxin’s bargaining position.

Logistics and reconditioning capacity

Transporters, warehouses and refurbishers directly shape turnaround times and unit economics; peak-season capacity constraints can inflate logistics prices 10-30% and add 2–7 days to cycle time. Multi-vendor networks and volume commitments typically cut logistics cost 5–15%. Higher geographic density enables stronger SLAs and can lower cost-per-km by around 10% in dense clusters.

- Transporters: impact on turnaround/unit cost

- Peaks: prices +10–30%, time +2–7 days

- Network/volume: cost −5–15%

- Geographic density: SLA & cost-per-km ≈ −10%

Data and traffic channels

Ad platforms, map/traffic partners and data APIs control lead flow and verification, giving suppliers pricing leverage—iResearch 2024 estimates the top 3 mobile ad platforms capture about 70% of ad spend—so dependency on search/short-video inflates CPCs. Building direct mobile traffic, CRM and first-party data reduces reliance and improves verification, strengthening Uxin’s negotiating position.

- Platform concentration ~70% (iResearch 2024)

- Direct mobile/CRM lowers acquisition costs

- First-party data => higher bargaining power

- APIs/map partners control lead quality and verification

Fragmented sellers (22.3M) curb supplier power; inspections +30%, LPR 3.45%

Supplier power is limited by fragmented individual sellers amid 22.3M used-car transactions in China (2024), enabling Uxin to negotiate on price and quality. Dependence on inspections (in-house team +30% in 2024) and lenders (one-year LPR 3.45% in 2024) creates pockets of supplier leverage. Ad/platform concentration (~70% top‑3 ad spend, iResearch 2024) raises acquisition costs until first‑party traffic scales.

| Supplier | Driver | 2024 metric |

|---|---|---|

| Sellers | Fragmentation | 22.3M txns |

| Inspections | Staff/tools | +30% in‑house |

| Lenders | Funding/cost | LPR 3.45% |

| Ad platforms | Lead costs | Top3 ~70% |

What is included in the product

Tailored Porter’s Five Forces analysis for Uxin uncovering competitive drivers, buyer and supplier power, entry barriers, substitutes, and disruptive threats, with strategic commentary and actionable insights to inform investor materials, strategy decks, or academic projects.

A concise Uxin Porter's Five Forces summary that pinpoints competitive pain points and suggests targeted strategic levers—perfect for rapid decision-making, boardroom slides, or quick integration into broader strategy decks.

Customers Bargaining Power

High price transparency

With ~26 million used-car transactions in China in 2023 and online channels capturing roughly 20% of volume, buyers easily compare listings on Uxin, Guazi, Autohome and offline dealers. VIN checks and publicly available histories increase buyer leverage, forcing transparent pricing. Low switching costs push platforms to compete on total cost and assurances; Uxin must differentiate with certified quality inspections and robust warranties.

Sensitivity to total ownership cost

Customers weigh price, financing rate, insurance, taxes, and after-sales; in China the used-car market exceeded 13 million transactions in 2023, making total ownership cost decisive. Bundled value—warranty, certified inspection, trade-in credit—can offset headline price pressure. Financing promotions often sway buyers but compress dealer margins. Clear TCO communication reduces haggling and returns.

Trust and assurance demands

Buyers in 2C increasingly demand reliable inspections, 7–15 day return windows, and guarantees; strong return and escrow policies raise conversion but shift bargaining power to buyers. Transparent claims processes and escrow mechanisms shape perceived fairness and reduce chargebacks. In 2024, platforms report that data-backed grading cuts dispute rates and coupon costs materially, improving unit economics.

Regional inventory preferences

Local tastes and emissions rules materially shape model desirability, shifting buyer preference toward compliant, regionally popular trims; when local stock is thin buyers frequently demand transfers or price concessions, and longer cross-province logistics further strengthen buyer bargaining power; dynamic pricing and real-time inventory balancing reduce forced concessions by matching supply to demand.

- regional_compliance

- stock_shortage

- logistics_delay

- dynamic_pricing

Review and social influence

Ratings, KOLs and social forums magnify buyer voice: 2024 data show review-driven leads rose ~20%, making negative virality able to force fee concessions and faster returns, raising buyer leverage over service terms; proactive service recovery and transparent reporting cut dispute rates and preserve margins; referral programs convert influence into growth while capping acquisition cost per user.

- Ratings impact: +20% review-driven leads (2024)

- KOLs/social reach: amplifies complaints

- Recovery/reporting: lowers dispute rates

- Referrals: growth with controlled CAC

Buyers win: 26M trades, 20% online sway

Buyers hold high bargaining power: ~26M used-car transactions in China in 2023 with ~20% online share lets shoppers compare listings across Uxin, Guazi and dealers, pressuring price and guarantees. Low switching costs and VIN/history transparency force platforms to compete on TCO, warranties and inspection quality. Review-driven leads rose ~20% in 2024, amplifying buyer leverage.

| Metric | Value |

|---|---|

| 2023 used-car volume | ~26M |

| Online share | ~20% |

| Review-driven leads (2024) | +20% |

Full Version Awaits

Uxin Porter's Five Forces Analysis

This preview shows the exact document you'll receive immediately after purchase—no surprises, no placeholders. Uxin Porter's Five Forces Analysis examines competitive rivalry, supplier and buyer power, threat of substitutes, and barriers to entry, offering actionable insights and strategic recommendations tailored to Uxin's used‑car marketplace.