Tessera. Inc. SWOT Analysis

Go Beyond the Preview—Access the Full Strategic Report

Tessera, Inc. shows strong IP-led product diversification and strategic partnerships, but faces competitive pressure and execution risks as it scales; emerging market demand and technology upgrades present clear growth drivers. Want the full story behind strengths, risks, and growth opportunities? Purchase the complete SWOT analysis for a professionally written, editable Word report plus Excel matrix to plan, pitch, or invest with confidence.

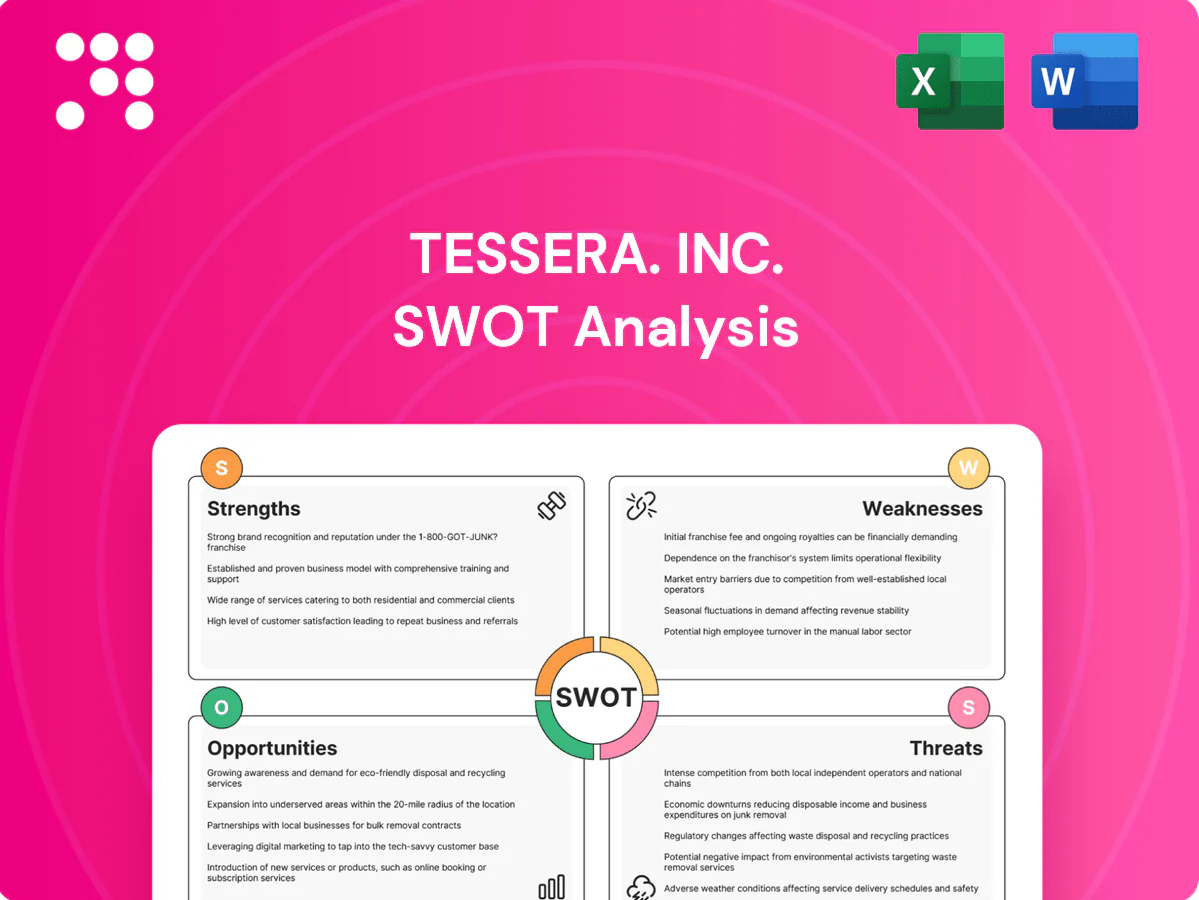

Strengths

Deep IP portfolio

Tessera built a deep IP portfolio—over 1,000 worldwide patents—focused on semiconductor packaging, wafer‑level and 3D integration, producing durable licensing income and strong leverage with OEMs and foundries; the breadth of claims enables cross‑licensing and defensive positioning, and since integration into Xperi the portfolio now spans imaging and audio, widening monetization opportunities.

Proven licensing model

Tessera leverages a scalable, high-margin licensing model rather than capital-heavy manufacturing, delivering predictable profitability. Recurring royalties and periodic settlements have historically smoothed cash flows and reduced capital intensity. Licensing enabled rapid adoption across smartphones, TVs, automotive and IoT devices. The model scales across ecosystems as its technologies are embedded into broader platform stacks.

Technology credibility

As an early pioneer, Tessera built strong technical brand equity in advanced packaging, helping Xperi leverage proven IP across imaging and packaging domains. Credibility with semiconductor leaders eased adoption of its innovations, contributing to broader ecosystem use and licensing momentum. Industry standardization around 2.5D/3D techniques validated its approach, supporting relevance inside Xperi, which reported FY2024 revenue of $1.01 billion.

Diversified tech adjacencies

Expansion into imaging and audio broadened Tessera Inc.s end-market exposure beyond semiconductors, reducing dependence on a single technology cycle and enabling cross-domain IP combinations that produce differentiated, integrable solutions which can stabilize revenue across consumer electronics cycles.

- Broader end-markets

- Lower single-cycle risk

- Cross-domain IP leverage

- Revenue stabilization potential

Litigation and enforcement expertise

Tessera has built robust capabilities to defend and monetize IP through courts and negotiated settlements, converting assertions into licensing revenue. A consistent enforcement track record deters infringement and underpins licensing rates. Structured settlements and periodic enforcement wins provide episodic upside while institutional knowledge strengthens future assertion strategies.

1,000+ patents enable high-margin licensing and recurring revenue across devices

Deep IP portfolio of over 1,000 global patents focused on advanced packaging and 3D/wafer‑level integration, enabling durable licensing leverage with OEMs and foundries.

Scalable, high‑margin licensing model delivers predictable, capital‑light cash flows and broad adoption across smartphones, TVs, automotive and IoT.

Strong technical brand and enforcement track record convert assertions into recurring and episodic settlement income, strengthening licensing rates.

Integration into Xperi broadened monetization into imaging/audio; Xperi reported FY2024 revenue of $1.01 billion.

| Metric | Value |

|---|---|

| FY2024 revenue | $1.01B |

| Patents (global) | >1,000 |

What is included in the product

Provides a concise SWOT overview of Tessera. Inc., highlighting its core strengths and operational weaknesses while mapping market opportunities and external threats shaping strategic decisions.

Provides a concise SWOT matrix highlighting Tessera, Inc.'s IP and technology strengths alongside market and regulatory risks for rapid strategic alignment and decision-making.

Weaknesses

Litigation dependence

Heavy reliance on enforcement imposes direct costs and timing risk, with IP litigation often costing tens of millions and verdicts capable of swinging quarterly results materially. Legal battles distract management and divert R&D/licensing focus, while counterclaims can seek invalidation of core patents and erase expected royalty streams. Aggressive suits also strain relationships with potential licensees, reducing long-term deal flow and predictable revenue.

Narrow productization

Narrow productization limits Tessera Inc.'s control over pricing and channels, shifting value capture to license terms rather than full-stack solutions; this reduces brand visibility with end users and increases dependence on integrators, which can compress royalties and margin over time.

Patent life erosion

Core semiconductor packaging patents have a statutory 20-year term and, as Tessera Inc.’s foundational patents age and expire, the royalty-bearing base faces downward pressure. As portfolios roll off, renewal revenue can decline absent fresh filings or continuations to maintain claim scope. To offset attrition Tessera must sustain R&D and patent prosecution spend so new grants outpace expirations and preserve licensing income.

Customer concentration

Tessera Inc.s royalty stream is concentrated in a small set of large OEMs and chipmakers, giving mega-licensees disproportionate negotiation leverage; pricing disputes or design-outs by a single partner can materially reduce license revenue. Collections are often lumpy across quarters, amplifying earnings volatility and cashflow unpredictability.

- Customer concentration risk

- Mega-licensee leverage

- Design-out sensitivity

- Uneven collections

Integration complexity

Being folded into Xperi forces portfolio rationalization, creating trade-offs that can deprioritize Tessera Inc. legacy packaging advances; cross-unit priorities risk diluting engineering and R&D resources. Systems and culture alignment will take months to years, and persistent misalignment can materially slow deal-making and commercial execution.

- portfolio-rationalization

- R&D-resource-dilution

- systems-culture-misalignment

- slower-deal-execution

Enforcement risk, OEM concentration and aging 20-year patents

Heavy reliance on enforcement imposes direct costs and timing risk, with IP litigation often costing tens of millions and verdicts swinging quarterly results. Narrow productization shifts value to license terms and limits end‑user visibility. Aging 20‑year core patents pressure future royalties absent new grants. Customer concentration gives mega‑licensees outsized leverage.

| Metric | Fact |

|---|---|

| Litigation cost | Often tens of millions USD |

| Patent term | Statutory 20 years |

| Revenue risk | Concentrated among few OEMs |

What You See Is What You Get

Tessera. Inc. SWOT Analysis

This is a real excerpt from the complete Tessera, Inc. SWOT analysis—you’re viewing the exact document provided after purchase. The preview below is taken directly from the full report and reflects the same professional structure, findings, and editable content you’ll download. Buy now to unlock the entire in-depth version with supporting details and recommendations.

Go Beyond the Preview—Access the Full Strategic Report

Tessera, Inc. shows strong IP-led product diversification and strategic partnerships, but faces competitive pressure and execution risks as it scales; emerging market demand and technology upgrades present clear growth drivers. Want the full story behind strengths, risks, and growth opportunities? Purchase the complete SWOT analysis for a professionally written, editable Word report plus Excel matrix to plan, pitch, or invest with confidence.

Strengths

Deep IP portfolio

Tessera built a deep IP portfolio—over 1,000 worldwide patents—focused on semiconductor packaging, wafer‑level and 3D integration, producing durable licensing income and strong leverage with OEMs and foundries; the breadth of claims enables cross‑licensing and defensive positioning, and since integration into Xperi the portfolio now spans imaging and audio, widening monetization opportunities.

Proven licensing model

Tessera leverages a scalable, high-margin licensing model rather than capital-heavy manufacturing, delivering predictable profitability. Recurring royalties and periodic settlements have historically smoothed cash flows and reduced capital intensity. Licensing enabled rapid adoption across smartphones, TVs, automotive and IoT devices. The model scales across ecosystems as its technologies are embedded into broader platform stacks.

Technology credibility

As an early pioneer, Tessera built strong technical brand equity in advanced packaging, helping Xperi leverage proven IP across imaging and packaging domains. Credibility with semiconductor leaders eased adoption of its innovations, contributing to broader ecosystem use and licensing momentum. Industry standardization around 2.5D/3D techniques validated its approach, supporting relevance inside Xperi, which reported FY2024 revenue of $1.01 billion.

Diversified tech adjacencies

Expansion into imaging and audio broadened Tessera Inc.s end-market exposure beyond semiconductors, reducing dependence on a single technology cycle and enabling cross-domain IP combinations that produce differentiated, integrable solutions which can stabilize revenue across consumer electronics cycles.

- Broader end-markets

- Lower single-cycle risk

- Cross-domain IP leverage

- Revenue stabilization potential

Litigation and enforcement expertise

Tessera has built robust capabilities to defend and monetize IP through courts and negotiated settlements, converting assertions into licensing revenue. A consistent enforcement track record deters infringement and underpins licensing rates. Structured settlements and periodic enforcement wins provide episodic upside while institutional knowledge strengthens future assertion strategies.

1,000+ patents enable high-margin licensing and recurring revenue across devices

Deep IP portfolio of over 1,000 global patents focused on advanced packaging and 3D/wafer‑level integration, enabling durable licensing leverage with OEMs and foundries.

Scalable, high‑margin licensing model delivers predictable, capital‑light cash flows and broad adoption across smartphones, TVs, automotive and IoT.

Strong technical brand and enforcement track record convert assertions into recurring and episodic settlement income, strengthening licensing rates.

Integration into Xperi broadened monetization into imaging/audio; Xperi reported FY2024 revenue of $1.01 billion.

| Metric | Value |

|---|---|

| FY2024 revenue | $1.01B |

| Patents (global) | >1,000 |

What is included in the product

Provides a concise SWOT overview of Tessera. Inc., highlighting its core strengths and operational weaknesses while mapping market opportunities and external threats shaping strategic decisions.

Provides a concise SWOT matrix highlighting Tessera, Inc.'s IP and technology strengths alongside market and regulatory risks for rapid strategic alignment and decision-making.

Weaknesses

Litigation dependence

Heavy reliance on enforcement imposes direct costs and timing risk, with IP litigation often costing tens of millions and verdicts capable of swinging quarterly results materially. Legal battles distract management and divert R&D/licensing focus, while counterclaims can seek invalidation of core patents and erase expected royalty streams. Aggressive suits also strain relationships with potential licensees, reducing long-term deal flow and predictable revenue.

Narrow productization

Narrow productization limits Tessera Inc.'s control over pricing and channels, shifting value capture to license terms rather than full-stack solutions; this reduces brand visibility with end users and increases dependence on integrators, which can compress royalties and margin over time.

Patent life erosion

Core semiconductor packaging patents have a statutory 20-year term and, as Tessera Inc.’s foundational patents age and expire, the royalty-bearing base faces downward pressure. As portfolios roll off, renewal revenue can decline absent fresh filings or continuations to maintain claim scope. To offset attrition Tessera must sustain R&D and patent prosecution spend so new grants outpace expirations and preserve licensing income.

Customer concentration

Tessera Inc.s royalty stream is concentrated in a small set of large OEMs and chipmakers, giving mega-licensees disproportionate negotiation leverage; pricing disputes or design-outs by a single partner can materially reduce license revenue. Collections are often lumpy across quarters, amplifying earnings volatility and cashflow unpredictability.

- Customer concentration risk

- Mega-licensee leverage

- Design-out sensitivity

- Uneven collections

Integration complexity

Being folded into Xperi forces portfolio rationalization, creating trade-offs that can deprioritize Tessera Inc. legacy packaging advances; cross-unit priorities risk diluting engineering and R&D resources. Systems and culture alignment will take months to years, and persistent misalignment can materially slow deal-making and commercial execution.

- portfolio-rationalization

- R&D-resource-dilution

- systems-culture-misalignment

- slower-deal-execution

Enforcement risk, OEM concentration and aging 20-year patents

Heavy reliance on enforcement imposes direct costs and timing risk, with IP litigation often costing tens of millions and verdicts swinging quarterly results. Narrow productization shifts value to license terms and limits end‑user visibility. Aging 20‑year core patents pressure future royalties absent new grants. Customer concentration gives mega‑licensees outsized leverage.

| Metric | Fact |

|---|---|

| Litigation cost | Often tens of millions USD |

| Patent term | Statutory 20 years |

| Revenue risk | Concentrated among few OEMs |

What You See Is What You Get

Tessera. Inc. SWOT Analysis

This is a real excerpt from the complete Tessera, Inc. SWOT analysis—you’re viewing the exact document provided after purchase. The preview below is taken directly from the full report and reflects the same professional structure, findings, and editable content you’ll download. Buy now to unlock the entire in-depth version with supporting details and recommendations.

Description

Go Beyond the Preview—Access the Full Strategic Report

Tessera, Inc. shows strong IP-led product diversification and strategic partnerships, but faces competitive pressure and execution risks as it scales; emerging market demand and technology upgrades present clear growth drivers. Want the full story behind strengths, risks, and growth opportunities? Purchase the complete SWOT analysis for a professionally written, editable Word report plus Excel matrix to plan, pitch, or invest with confidence.

Strengths

Deep IP portfolio

Tessera built a deep IP portfolio—over 1,000 worldwide patents—focused on semiconductor packaging, wafer‑level and 3D integration, producing durable licensing income and strong leverage with OEMs and foundries; the breadth of claims enables cross‑licensing and defensive positioning, and since integration into Xperi the portfolio now spans imaging and audio, widening monetization opportunities.

Proven licensing model

Tessera leverages a scalable, high-margin licensing model rather than capital-heavy manufacturing, delivering predictable profitability. Recurring royalties and periodic settlements have historically smoothed cash flows and reduced capital intensity. Licensing enabled rapid adoption across smartphones, TVs, automotive and IoT devices. The model scales across ecosystems as its technologies are embedded into broader platform stacks.

Technology credibility

As an early pioneer, Tessera built strong technical brand equity in advanced packaging, helping Xperi leverage proven IP across imaging and packaging domains. Credibility with semiconductor leaders eased adoption of its innovations, contributing to broader ecosystem use and licensing momentum. Industry standardization around 2.5D/3D techniques validated its approach, supporting relevance inside Xperi, which reported FY2024 revenue of $1.01 billion.

Diversified tech adjacencies

Expansion into imaging and audio broadened Tessera Inc.s end-market exposure beyond semiconductors, reducing dependence on a single technology cycle and enabling cross-domain IP combinations that produce differentiated, integrable solutions which can stabilize revenue across consumer electronics cycles.

- Broader end-markets

- Lower single-cycle risk

- Cross-domain IP leverage

- Revenue stabilization potential

Litigation and enforcement expertise

Tessera has built robust capabilities to defend and monetize IP through courts and negotiated settlements, converting assertions into licensing revenue. A consistent enforcement track record deters infringement and underpins licensing rates. Structured settlements and periodic enforcement wins provide episodic upside while institutional knowledge strengthens future assertion strategies.

1,000+ patents enable high-margin licensing and recurring revenue across devices

Deep IP portfolio of over 1,000 global patents focused on advanced packaging and 3D/wafer‑level integration, enabling durable licensing leverage with OEMs and foundries.

Scalable, high‑margin licensing model delivers predictable, capital‑light cash flows and broad adoption across smartphones, TVs, automotive and IoT.

Strong technical brand and enforcement track record convert assertions into recurring and episodic settlement income, strengthening licensing rates.

Integration into Xperi broadened monetization into imaging/audio; Xperi reported FY2024 revenue of $1.01 billion.

| Metric | Value |

|---|---|

| FY2024 revenue | $1.01B |

| Patents (global) | >1,000 |

What is included in the product

Provides a concise SWOT overview of Tessera. Inc., highlighting its core strengths and operational weaknesses while mapping market opportunities and external threats shaping strategic decisions.

Provides a concise SWOT matrix highlighting Tessera, Inc.'s IP and technology strengths alongside market and regulatory risks for rapid strategic alignment and decision-making.

Weaknesses

Litigation dependence

Heavy reliance on enforcement imposes direct costs and timing risk, with IP litigation often costing tens of millions and verdicts capable of swinging quarterly results materially. Legal battles distract management and divert R&D/licensing focus, while counterclaims can seek invalidation of core patents and erase expected royalty streams. Aggressive suits also strain relationships with potential licensees, reducing long-term deal flow and predictable revenue.

Narrow productization

Narrow productization limits Tessera Inc.'s control over pricing and channels, shifting value capture to license terms rather than full-stack solutions; this reduces brand visibility with end users and increases dependence on integrators, which can compress royalties and margin over time.

Patent life erosion

Core semiconductor packaging patents have a statutory 20-year term and, as Tessera Inc.’s foundational patents age and expire, the royalty-bearing base faces downward pressure. As portfolios roll off, renewal revenue can decline absent fresh filings or continuations to maintain claim scope. To offset attrition Tessera must sustain R&D and patent prosecution spend so new grants outpace expirations and preserve licensing income.

Customer concentration

Tessera Inc.s royalty stream is concentrated in a small set of large OEMs and chipmakers, giving mega-licensees disproportionate negotiation leverage; pricing disputes or design-outs by a single partner can materially reduce license revenue. Collections are often lumpy across quarters, amplifying earnings volatility and cashflow unpredictability.

- Customer concentration risk

- Mega-licensee leverage

- Design-out sensitivity

- Uneven collections

Integration complexity

Being folded into Xperi forces portfolio rationalization, creating trade-offs that can deprioritize Tessera Inc. legacy packaging advances; cross-unit priorities risk diluting engineering and R&D resources. Systems and culture alignment will take months to years, and persistent misalignment can materially slow deal-making and commercial execution.

- portfolio-rationalization

- R&D-resource-dilution

- systems-culture-misalignment

- slower-deal-execution

Enforcement risk, OEM concentration and aging 20-year patents

Heavy reliance on enforcement imposes direct costs and timing risk, with IP litigation often costing tens of millions and verdicts swinging quarterly results. Narrow productization shifts value to license terms and limits end‑user visibility. Aging 20‑year core patents pressure future royalties absent new grants. Customer concentration gives mega‑licensees outsized leverage.

| Metric | Fact |

|---|---|

| Litigation cost | Often tens of millions USD |

| Patent term | Statutory 20 years |

| Revenue risk | Concentrated among few OEMs |

What You See Is What You Get

Tessera. Inc. SWOT Analysis

This is a real excerpt from the complete Tessera, Inc. SWOT analysis—you’re viewing the exact document provided after purchase. The preview below is taken directly from the full report and reflects the same professional structure, findings, and editable content you’ll download. Buy now to unlock the entire in-depth version with supporting details and recommendations.