Xafinity Ltd. Porter's Five Forces Analysis

From Overview to Strategy Blueprint

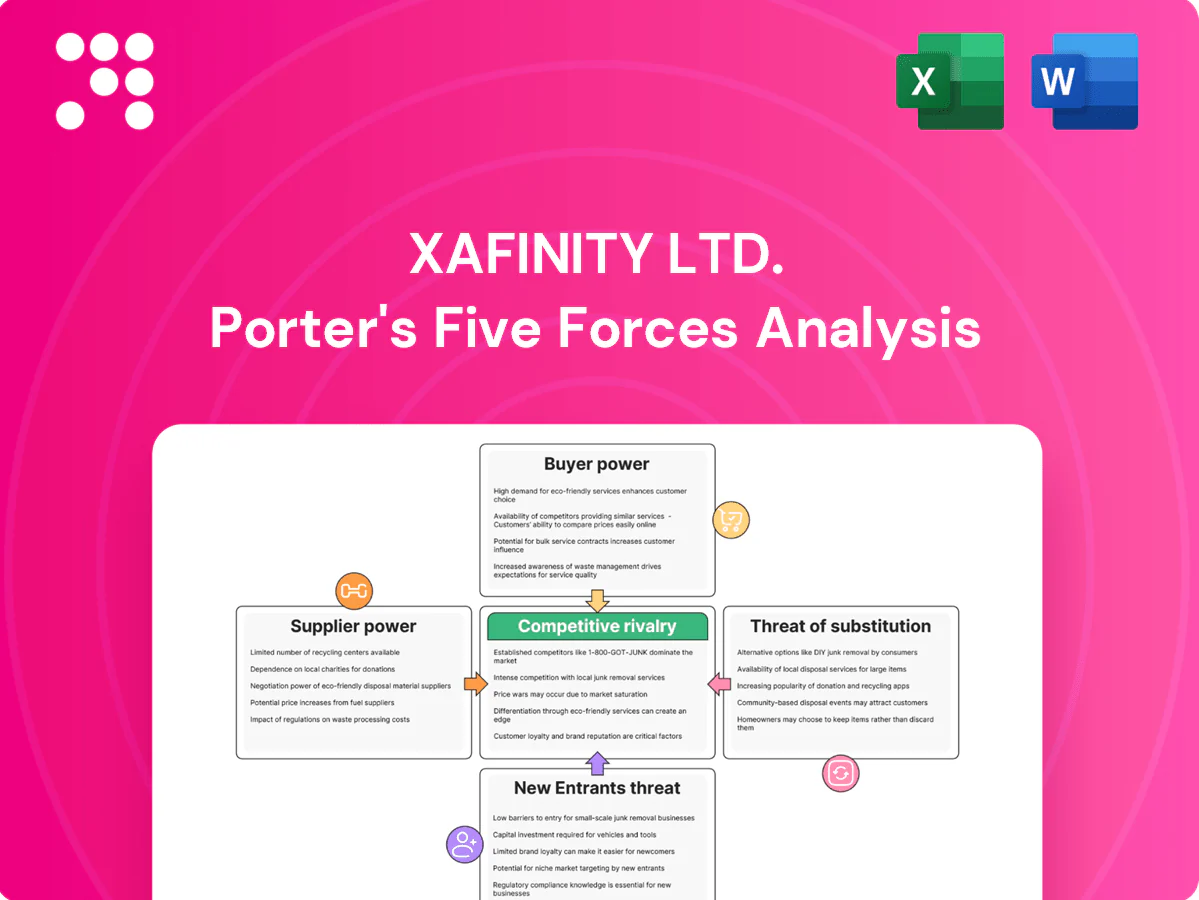

Xafinity Ltd. faces moderate buyer power, niche supplier relationships, low threat of new entrants due to regulatory hurdles, and limited substitute risk given specialized services. Competitive rivalry is steady as firms vie on service depth and client trust. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Xafinity Ltd.’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Scarce actuarial talent

Scarce actuarial talent gives qualified actuaries and pensions specialists strong leverage over pay and flexibility; in 2024 industry surveys reported that over 50% of UK pensions firms experienced recruitment difficulty, pushing salary premia and contractor rates higher. Retention and recruitment costs spike during de-risking cycles, raising short-term operating costs and margin pressure. A strong employer brand, clear training pathways and apprenticeship schemes at firms like Xafinity can soften individual leverage. Widening hiring geographically and offering hybrid roles has expanded the candidate pool, moderating supplier power.

Critical tech and admin platforms

Core admin, workflow and cloud providers are sticky for Xafinity due to deep integration and compliance, with the big three cloud vendors accounting for roughly 65% of infrastructure spend in 2024, concentrating supplier power. Vendors leverage license fees, mandatory upgrades and data-migration frictions to raise costs. Multi-vendor strategies and in-house tools cut dependence, and clear contracts with exit clauses plus open APIs materially lower switching barriers.

Data and analytics providers

Data and analytics providers for longevity tables, market data and ESG feeds hold moderate supplier power: these inputs are specialized but alternative sources and public datasets emerged strongly in 2024, bundled pricing and index licensing can raise costs, yet competitive procurement and internal modeling capabilities limit unilateral price hikes and partially offset dependence.

Insurer/reinsurer partners

Risk transfer execution for Xafinity hinges on a concentrated insurer/reinsurer market; 2024 reinsurance capacity stood near USD 600bn (Aon), so tight-capacity phases push pricing and terms toward insurers. Strong market coverage and disciplined submission processes secure more competitive quotes, while multiple mandates and pipeline visibility reduce counterparty leverage.

- Concentration: high

- 2024 capacity: ~USD 600bn

- Mitigants: multiple mandates, pipeline visibility

Professional services and compliance

Legal, cyber and audit suppliers provide mandatory capabilities for regulated Xafinity work, creating baseline supplier leverage but limited by competitive tendering and public framework agreements that drive price transparency. Peak regulatory change can compress capacity and lift fees temporarily, while long-term panel relationships and standardised playbooks keep ongoing costs predictable and controllable.

- Mandatory capability: regulatory compliance

- Constraint: competitive markets & frameworks

- Risk: fee spikes during regulatory peaks

- Mitigant: long-term panels & standard playbooks

Actuary shortages and cloud concentration push supplier pricing; reinsurers may tighten

Suppliers hold moderate-to-high power: scarce actuaries (50% of UK pensions firms reported recruitment difficulty in 2024) and concentrated cloud vendors (65% of infra spend) raise costs. Reinsurer capacity (~USD 600bn in 2024) can tighten pricing. Legal/cyber panels are price-stable but spike on regulatory peaks.

| Category | 2024 metric |

|---|---|

| Actuarial talent | 50% recruitment difficulty |

| Cloud vendors | 65% infra spend |

| Reinsurance | ~USD 600bn capacity |

What is included in the product

Tailored exclusively for Xafinity Ltd., this Porter's Five Forces analysis uncovers key competitive drivers, buyer and supplier power, threats from substitutes and new entrants, and identifies disruptive forces and market dynamics that shape pricing and profitability.

One-sheet Porter's Five Forces for Xafinity Ltd.—instantly visualise insurer/HR services competitive pressures with a clean radar chart and customizable intensity sliders to model regulation shifts or new entrants.

Customers Bargaining Power

Large, sophisticated buyers

Trustees and corporate sponsors run competitive tenders and benchmark fees; in 2024 UK defined benefit schemes collectively held c.£2.9tn in assets, concentrating spend and increasing bargaining clout for large buyers. They demand bespoke scope, SLAs and measurable outcomes, making referenceability and a proven track record decisive in negotiations.

High switching costs in admin

Migrating member data and processes creates measurable operational risk and direct costs, which materially reduce buyer willingness to switch; buyers nonetheless use retenders to pressure pricing. Strong transition methodologies and proven cutover playbooks lower perceived risk and help Xafinity retain clients. Long multi‑year contracts amortize setup costs, damping churn and increasing customer lock‑in.

Outcome and price sensitivity

Funding outcomes, service KPIs and 2024 FCA Consumer Duty enforcement drive customer value assessments for Xafinity Ltd, raising compliance and reporting expectations. Buyers increasingly demand fixed fees, fee caps and gain-share structures to transfer outcome risk. Clear, auditable ROI and automation of administration can protect margins, while any underperformance typically triggers rapid fee renegotiation and clawbacks.

Multi-sourcing leverage

Schemes routinely multi-source actuarial, investment, administration and covenant work, allowing trustees to pit providers on price and scope; in 2024 UK DB trustees faced multi-advisor procurement in the majority of large buy-ins/buy-outs. Cross-sell success hinges on proven performance and seamless integration; open data standards and interoperability (growing after 2023 API initiatives) lower supplier lock-in and boost buyer leverage.

- Multi-sourcing enables competitive bidding

- Cross-sell requires demonstrable outcomes and systems integration

- Open data/interoperability reduces switching costs

Reputation and risk aversion

In fiduciary contexts for Xafinity Ltd, brand strength and a clear audit trail often outweigh price, as buyers prefer established partners to avoid operational or regulatory failures; a 2024 industry survey found about 70% of institutional clients prioritize reputation over cost. Thought leadership and compliance certifications (eg ISO, SOC reports) visibly reduce perceived risk, limiting extreme price-driven switching and supporting pricing stability.

- Reputation-driven selection

- Audit trail critical

- Compliance lowers perceived risk

- Price sensitivity constrained

UK DB trustees drive competitive tenders as c.£2.9tn in assets boosts bargaining power

Trustees and sponsors ran competitive tenders in 2024 as UK DB schemes held c.£2.9tn of assets, concentrating spend and boosting bargaining power. Long multi‑year contracts and complex data migrations raise switching costs, yet benchmarking and retenders keep price pressure high. Reputation matters: a 2024 survey found ~70% of institutional clients prioritise provider reputation over cost, limiting extreme price-driven churn.

| Metric | 2024 value | Impact |

|---|---|---|

| UK DB assets | c.£2.9tn | Buyer concentration, higher leverage |

| Clients prioritising reputation | ~70% | Price sensitivity constrained |

Same Document Delivered

Xafinity Ltd. Porter's Five Forces Analysis

This preview shows the exact Xafinity Ltd. Porter's Five Forces Analysis you'll receive immediately after purchase—no surprises, fully formatted and ready to use. The report examines competitive rivalry, supplier and buyer power, threats of substitutes and new entrants, and concludes with strategic implications and valuation-sensitive risks to inform decisions.

From Overview to Strategy Blueprint

Xafinity Ltd. faces moderate buyer power, niche supplier relationships, low threat of new entrants due to regulatory hurdles, and limited substitute risk given specialized services. Competitive rivalry is steady as firms vie on service depth and client trust. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Xafinity Ltd.’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Scarce actuarial talent

Scarce actuarial talent gives qualified actuaries and pensions specialists strong leverage over pay and flexibility; in 2024 industry surveys reported that over 50% of UK pensions firms experienced recruitment difficulty, pushing salary premia and contractor rates higher. Retention and recruitment costs spike during de-risking cycles, raising short-term operating costs and margin pressure. A strong employer brand, clear training pathways and apprenticeship schemes at firms like Xafinity can soften individual leverage. Widening hiring geographically and offering hybrid roles has expanded the candidate pool, moderating supplier power.

Critical tech and admin platforms

Core admin, workflow and cloud providers are sticky for Xafinity due to deep integration and compliance, with the big three cloud vendors accounting for roughly 65% of infrastructure spend in 2024, concentrating supplier power. Vendors leverage license fees, mandatory upgrades and data-migration frictions to raise costs. Multi-vendor strategies and in-house tools cut dependence, and clear contracts with exit clauses plus open APIs materially lower switching barriers.

Data and analytics providers

Data and analytics providers for longevity tables, market data and ESG feeds hold moderate supplier power: these inputs are specialized but alternative sources and public datasets emerged strongly in 2024, bundled pricing and index licensing can raise costs, yet competitive procurement and internal modeling capabilities limit unilateral price hikes and partially offset dependence.

Insurer/reinsurer partners

Risk transfer execution for Xafinity hinges on a concentrated insurer/reinsurer market; 2024 reinsurance capacity stood near USD 600bn (Aon), so tight-capacity phases push pricing and terms toward insurers. Strong market coverage and disciplined submission processes secure more competitive quotes, while multiple mandates and pipeline visibility reduce counterparty leverage.

- Concentration: high

- 2024 capacity: ~USD 600bn

- Mitigants: multiple mandates, pipeline visibility

Professional services and compliance

Legal, cyber and audit suppliers provide mandatory capabilities for regulated Xafinity work, creating baseline supplier leverage but limited by competitive tendering and public framework agreements that drive price transparency. Peak regulatory change can compress capacity and lift fees temporarily, while long-term panel relationships and standardised playbooks keep ongoing costs predictable and controllable.

- Mandatory capability: regulatory compliance

- Constraint: competitive markets & frameworks

- Risk: fee spikes during regulatory peaks

- Mitigant: long-term panels & standard playbooks

Actuary shortages and cloud concentration push supplier pricing; reinsurers may tighten

Suppliers hold moderate-to-high power: scarce actuaries (50% of UK pensions firms reported recruitment difficulty in 2024) and concentrated cloud vendors (65% of infra spend) raise costs. Reinsurer capacity (~USD 600bn in 2024) can tighten pricing. Legal/cyber panels are price-stable but spike on regulatory peaks.

| Category | 2024 metric |

|---|---|

| Actuarial talent | 50% recruitment difficulty |

| Cloud vendors | 65% infra spend |

| Reinsurance | ~USD 600bn capacity |

What is included in the product

Tailored exclusively for Xafinity Ltd., this Porter's Five Forces analysis uncovers key competitive drivers, buyer and supplier power, threats from substitutes and new entrants, and identifies disruptive forces and market dynamics that shape pricing and profitability.

One-sheet Porter's Five Forces for Xafinity Ltd.—instantly visualise insurer/HR services competitive pressures with a clean radar chart and customizable intensity sliders to model regulation shifts or new entrants.

Customers Bargaining Power

Large, sophisticated buyers

Trustees and corporate sponsors run competitive tenders and benchmark fees; in 2024 UK defined benefit schemes collectively held c.£2.9tn in assets, concentrating spend and increasing bargaining clout for large buyers. They demand bespoke scope, SLAs and measurable outcomes, making referenceability and a proven track record decisive in negotiations.

High switching costs in admin

Migrating member data and processes creates measurable operational risk and direct costs, which materially reduce buyer willingness to switch; buyers nonetheless use retenders to pressure pricing. Strong transition methodologies and proven cutover playbooks lower perceived risk and help Xafinity retain clients. Long multi‑year contracts amortize setup costs, damping churn and increasing customer lock‑in.

Outcome and price sensitivity

Funding outcomes, service KPIs and 2024 FCA Consumer Duty enforcement drive customer value assessments for Xafinity Ltd, raising compliance and reporting expectations. Buyers increasingly demand fixed fees, fee caps and gain-share structures to transfer outcome risk. Clear, auditable ROI and automation of administration can protect margins, while any underperformance typically triggers rapid fee renegotiation and clawbacks.

Multi-sourcing leverage

Schemes routinely multi-source actuarial, investment, administration and covenant work, allowing trustees to pit providers on price and scope; in 2024 UK DB trustees faced multi-advisor procurement in the majority of large buy-ins/buy-outs. Cross-sell success hinges on proven performance and seamless integration; open data standards and interoperability (growing after 2023 API initiatives) lower supplier lock-in and boost buyer leverage.

- Multi-sourcing enables competitive bidding

- Cross-sell requires demonstrable outcomes and systems integration

- Open data/interoperability reduces switching costs

Reputation and risk aversion

In fiduciary contexts for Xafinity Ltd, brand strength and a clear audit trail often outweigh price, as buyers prefer established partners to avoid operational or regulatory failures; a 2024 industry survey found about 70% of institutional clients prioritize reputation over cost. Thought leadership and compliance certifications (eg ISO, SOC reports) visibly reduce perceived risk, limiting extreme price-driven switching and supporting pricing stability.

- Reputation-driven selection

- Audit trail critical

- Compliance lowers perceived risk

- Price sensitivity constrained

UK DB trustees drive competitive tenders as c.£2.9tn in assets boosts bargaining power

Trustees and sponsors ran competitive tenders in 2024 as UK DB schemes held c.£2.9tn of assets, concentrating spend and boosting bargaining power. Long multi‑year contracts and complex data migrations raise switching costs, yet benchmarking and retenders keep price pressure high. Reputation matters: a 2024 survey found ~70% of institutional clients prioritise provider reputation over cost, limiting extreme price-driven churn.

| Metric | 2024 value | Impact |

|---|---|---|

| UK DB assets | c.£2.9tn | Buyer concentration, higher leverage |

| Clients prioritising reputation | ~70% | Price sensitivity constrained |

Same Document Delivered

Xafinity Ltd. Porter's Five Forces Analysis

This preview shows the exact Xafinity Ltd. Porter's Five Forces Analysis you'll receive immediately after purchase—no surprises, fully formatted and ready to use. The report examines competitive rivalry, supplier and buyer power, threats of substitutes and new entrants, and concludes with strategic implications and valuation-sensitive risks to inform decisions.

Original: $10.00

-65%$10.00

$3.50Description

From Overview to Strategy Blueprint

Xafinity Ltd. faces moderate buyer power, niche supplier relationships, low threat of new entrants due to regulatory hurdles, and limited substitute risk given specialized services. Competitive rivalry is steady as firms vie on service depth and client trust. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Xafinity Ltd.’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Scarce actuarial talent

Scarce actuarial talent gives qualified actuaries and pensions specialists strong leverage over pay and flexibility; in 2024 industry surveys reported that over 50% of UK pensions firms experienced recruitment difficulty, pushing salary premia and contractor rates higher. Retention and recruitment costs spike during de-risking cycles, raising short-term operating costs and margin pressure. A strong employer brand, clear training pathways and apprenticeship schemes at firms like Xafinity can soften individual leverage. Widening hiring geographically and offering hybrid roles has expanded the candidate pool, moderating supplier power.

Critical tech and admin platforms

Core admin, workflow and cloud providers are sticky for Xafinity due to deep integration and compliance, with the big three cloud vendors accounting for roughly 65% of infrastructure spend in 2024, concentrating supplier power. Vendors leverage license fees, mandatory upgrades and data-migration frictions to raise costs. Multi-vendor strategies and in-house tools cut dependence, and clear contracts with exit clauses plus open APIs materially lower switching barriers.

Data and analytics providers

Data and analytics providers for longevity tables, market data and ESG feeds hold moderate supplier power: these inputs are specialized but alternative sources and public datasets emerged strongly in 2024, bundled pricing and index licensing can raise costs, yet competitive procurement and internal modeling capabilities limit unilateral price hikes and partially offset dependence.

Insurer/reinsurer partners

Risk transfer execution for Xafinity hinges on a concentrated insurer/reinsurer market; 2024 reinsurance capacity stood near USD 600bn (Aon), so tight-capacity phases push pricing and terms toward insurers. Strong market coverage and disciplined submission processes secure more competitive quotes, while multiple mandates and pipeline visibility reduce counterparty leverage.

- Concentration: high

- 2024 capacity: ~USD 600bn

- Mitigants: multiple mandates, pipeline visibility

Professional services and compliance

Legal, cyber and audit suppliers provide mandatory capabilities for regulated Xafinity work, creating baseline supplier leverage but limited by competitive tendering and public framework agreements that drive price transparency. Peak regulatory change can compress capacity and lift fees temporarily, while long-term panel relationships and standardised playbooks keep ongoing costs predictable and controllable.

- Mandatory capability: regulatory compliance

- Constraint: competitive markets & frameworks

- Risk: fee spikes during regulatory peaks

- Mitigant: long-term panels & standard playbooks

Actuary shortages and cloud concentration push supplier pricing; reinsurers may tighten

Suppliers hold moderate-to-high power: scarce actuaries (50% of UK pensions firms reported recruitment difficulty in 2024) and concentrated cloud vendors (65% of infra spend) raise costs. Reinsurer capacity (~USD 600bn in 2024) can tighten pricing. Legal/cyber panels are price-stable but spike on regulatory peaks.

| Category | 2024 metric |

|---|---|

| Actuarial talent | 50% recruitment difficulty |

| Cloud vendors | 65% infra spend |

| Reinsurance | ~USD 600bn capacity |

What is included in the product

Tailored exclusively for Xafinity Ltd., this Porter's Five Forces analysis uncovers key competitive drivers, buyer and supplier power, threats from substitutes and new entrants, and identifies disruptive forces and market dynamics that shape pricing and profitability.

One-sheet Porter's Five Forces for Xafinity Ltd.—instantly visualise insurer/HR services competitive pressures with a clean radar chart and customizable intensity sliders to model regulation shifts or new entrants.

Customers Bargaining Power

Large, sophisticated buyers

Trustees and corporate sponsors run competitive tenders and benchmark fees; in 2024 UK defined benefit schemes collectively held c.£2.9tn in assets, concentrating spend and increasing bargaining clout for large buyers. They demand bespoke scope, SLAs and measurable outcomes, making referenceability and a proven track record decisive in negotiations.

High switching costs in admin

Migrating member data and processes creates measurable operational risk and direct costs, which materially reduce buyer willingness to switch; buyers nonetheless use retenders to pressure pricing. Strong transition methodologies and proven cutover playbooks lower perceived risk and help Xafinity retain clients. Long multi‑year contracts amortize setup costs, damping churn and increasing customer lock‑in.

Outcome and price sensitivity

Funding outcomes, service KPIs and 2024 FCA Consumer Duty enforcement drive customer value assessments for Xafinity Ltd, raising compliance and reporting expectations. Buyers increasingly demand fixed fees, fee caps and gain-share structures to transfer outcome risk. Clear, auditable ROI and automation of administration can protect margins, while any underperformance typically triggers rapid fee renegotiation and clawbacks.

Multi-sourcing leverage

Schemes routinely multi-source actuarial, investment, administration and covenant work, allowing trustees to pit providers on price and scope; in 2024 UK DB trustees faced multi-advisor procurement in the majority of large buy-ins/buy-outs. Cross-sell success hinges on proven performance and seamless integration; open data standards and interoperability (growing after 2023 API initiatives) lower supplier lock-in and boost buyer leverage.

- Multi-sourcing enables competitive bidding

- Cross-sell requires demonstrable outcomes and systems integration

- Open data/interoperability reduces switching costs

Reputation and risk aversion

In fiduciary contexts for Xafinity Ltd, brand strength and a clear audit trail often outweigh price, as buyers prefer established partners to avoid operational or regulatory failures; a 2024 industry survey found about 70% of institutional clients prioritize reputation over cost. Thought leadership and compliance certifications (eg ISO, SOC reports) visibly reduce perceived risk, limiting extreme price-driven switching and supporting pricing stability.

- Reputation-driven selection

- Audit trail critical

- Compliance lowers perceived risk

- Price sensitivity constrained

UK DB trustees drive competitive tenders as c.£2.9tn in assets boosts bargaining power

Trustees and sponsors ran competitive tenders in 2024 as UK DB schemes held c.£2.9tn of assets, concentrating spend and boosting bargaining power. Long multi‑year contracts and complex data migrations raise switching costs, yet benchmarking and retenders keep price pressure high. Reputation matters: a 2024 survey found ~70% of institutional clients prioritise provider reputation over cost, limiting extreme price-driven churn.

| Metric | 2024 value | Impact |

|---|---|---|

| UK DB assets | c.£2.9tn | Buyer concentration, higher leverage |

| Clients prioritising reputation | ~70% | Price sensitivity constrained |

Same Document Delivered

Xafinity Ltd. Porter's Five Forces Analysis

This preview shows the exact Xafinity Ltd. Porter's Five Forces Analysis you'll receive immediately after purchase—no surprises, fully formatted and ready to use. The report examines competitive rivalry, supplier and buyer power, threats of substitutes and new entrants, and concludes with strategic implications and valuation-sensitive risks to inform decisions.