Xylem Porter's Five Forces Analysis

From Overview to Strategy Blueprint

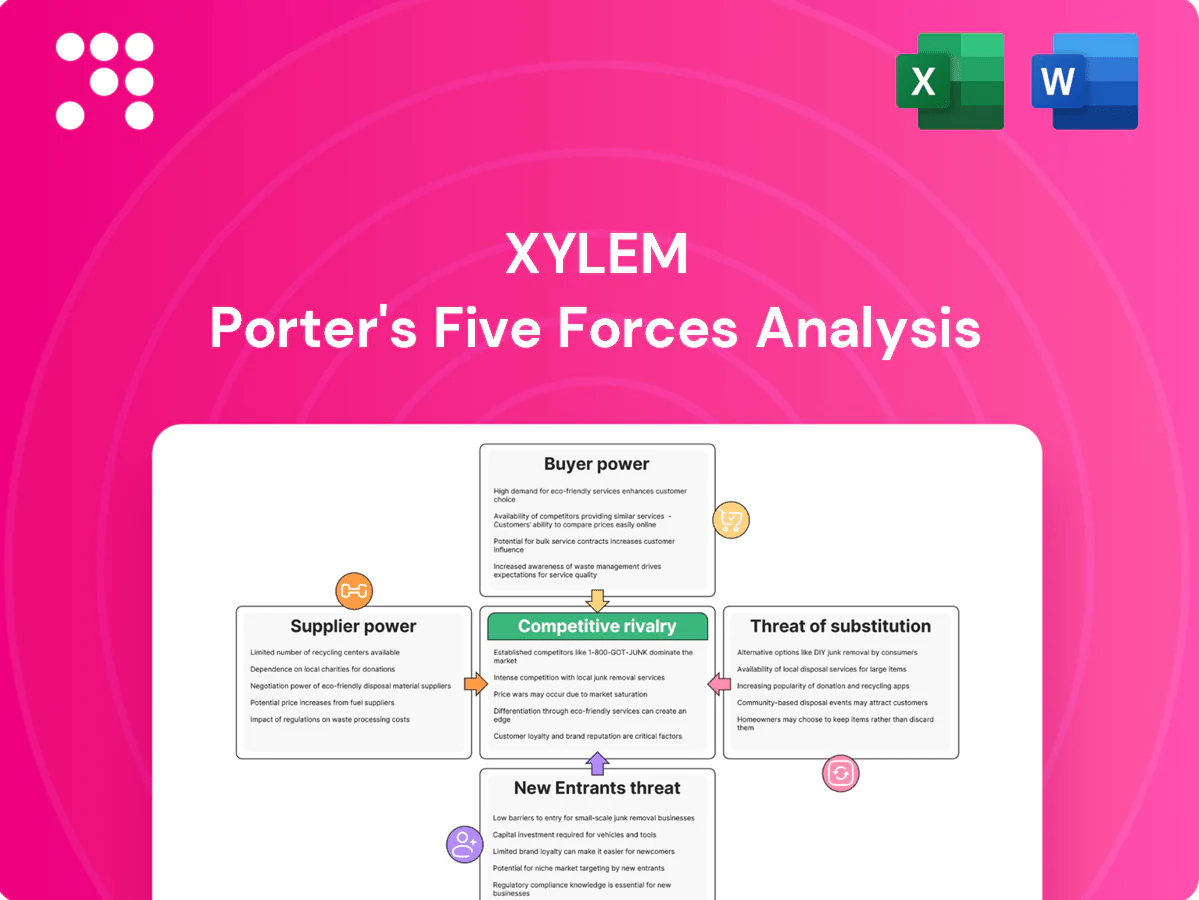

Xylem's Porter's Five Forces snapshot highlights moderate buyer power, fragmented suppliers, high industry rivalry, low substitute threat, and entry barriers driven by scale and regulation. This concise view reveals the competitive pressures shaping Xylem's strategy and margins. The full report provides force-by-force ratings, visuals, and strategic implications to guide investment or corporate decisions—unlock the complete analysis with consultant-grade Excel/Word deliverables.

Suppliers Bargaining Power

Specialized components, limited sources

Many critical inputs—advanced sensors, motors, membranes and specialty alloys—are sourced from a narrow pool of qualified vendors, raising switching costs and long municipal/industrial qualification lead times; this concentration gives select suppliers pricing and allocation leverage. Xylem, with 2023 revenue of about 6.7 billion USD, mitigates exposure through dual sourcing and design-for-substitution where feasible.

Material and energy cost volatility

Steel (~$800/tonne HRC), copper (~$9,000/tonne) and NdPr rare-earths (~$80/kg) plus energy (Brent ~$88/bbl in 2024) swing with global cycles, driving input price volatility for Xylem’s pumps and treatment equipment. Suppliers often pass through surcharges in tight markets, raising short-term input costs. Index-linked contracts and hedging reduce but do not remove exposure. Xylem’s ability to reclaim costs depends on backlog strength and competitive intensity at bid time.

Global supply chain and logistics risk

Complex multi-region supply chains expose Xylem to freight spikes, geopolitical frictions and compliance constraints, with 2024 container rates still volatile after 2021–22 peaks. Critical electronics and semiconductors face allocation risk, pressuring smart-device production. Regionalization and nearshoring lower disruption risk but raise fixed costs and capex. Inventory buffers improve uptime for service-driven customers but tie up working capital against Xylem’s 2024 revenue of about $6.7 billion.

Digital/software vendor dependence

Digital and software vendor dependence for Xylem is high as IoT platforms, connectivity modules and cybersecurity stacks are commonly third-party; the global IoT platform market is projected to exceed $30 billion by 2028, increasing lock-in risks that can raise lifecycle costs and constrain roadmap flexibility.

- Open architectures/in-house firmware lower vendor dependency but require continuous R&D spend

- Vendor lock-in can elevate TCO and slow innovation

- Long-term vendor partnerships align on reliability and security

Supplier bargaining offset by Xylem scale

Xylem’s large installed base and >$6.3B revenue (FY2023) deliver purchasing scale and standardized platforms that provide counter-leverage in supplier negotiations. Long-term volume commitments and strategic sourcing secure capacity and improved terms, while supplier development programs reduce cost and raise quality over time. For bespoke components, supplier power can remain high and situational.

- Scale: >$6.3B revenue (FY2023)

- Leverage: standardized platforms

- Strategy: long-term volume commitments

- Mitigation: supplier development

- Risk: bespoke components = higher supplier power

Concentrated supplier base raises switching costs as commodity and energy swings amplify risk

Many critical inputs (sensors, motors, membranes, rare-earths) come from a narrow supplier pool, raising switching costs and allocation leverage. Xylem (revenue ~6.7B USD 2023) mitigates with dual sourcing, design-for-substitution and long-term contracts. Commodity swings (steel, copper, NdPr) and energy (Brent ~88 USD/bbl 2024) amplify supplier pass-through risk.

| Metric | Value |

|---|---|

| 2023 revenue | $6.7B |

| Brent (2024) | $88/bbl |

| NdPr (2024) | $80/kg |

| IoT platform market | >$30B by 2028 |

What is included in the product

Uncovers key drivers of competition, supplier and buyer power, threat of substitutes and new entrants tailored to Xylem’s water technologies; identifies disruptive forces and strategic vulnerabilities that affect pricing, margins and market share, delivering actionable insights for investor materials, strategy decks or academic analyses.

One-sheet Porter's Five Forces for Xylem that instantly highlights competitive pressures with an editable spider/radar chart—perfect for quick decisions and pitch decks. Customize pressure levels, swap in your data, and integrate into reports with no macros or finance expertise required.

Customers Bargaining Power

Concentrated municipal buyers, formal tenders

Utilities and public agencies predominantly buy via competitive RFPs, concentrating buying power—US municipal water capital spending was roughly $50 billion annually in 2024 (AWWA/EPA estimates), amplifying supplier price pressure. Transparent bidding increases total-cost scrutiny and narrows margins. Multi-year framework agreements frequently lock terms across cycles, while detailed technical specs and prequalification lists limit vendor substitution despite price-driven procurement.

High switching costs, installed-base lock-in

Integration with SCADA, piping and controls creates high switching friction for Xylem customers, reinforced by lifecycle service contracts, spare parts provisioning and warranties that deepen installed-base lock-in. Buyers, facing industry-estimated downtime costs commonly cited in the $100k–$1M per hour range for critical infrastructure, prioritize continuity and compliance, reducing price sensitivity for mission-critical assets.

Industrial buyers seek uptime and TCO

Process operators prioritize uptime, energy efficiency and reuse economics, with energy often representing a large share of plant OPEX (industry estimates up to 40%). Performance guarantees and service SLAs (commonly specifying >99% uptime) frequently sway procurement beyond list price. Retrofit compatibility and digital monitoring deliver measurable TCO gains through reduced downtime and energy use. Multi-sourcing policies, however, keep customer bargaining power at a moderate level.

Budget cycles and funding constraints

Public budgets and grant timing (eg US Bipartisan Infrastructure Law allocated 55 billion for water, wastewater and stormwater) can delay awards or compress project scopes; when funding tightens buyers negotiate harder and defer upgrades. Regulatory mandates that tighten effluent limits reduce price elasticity by forcing spending regardless of cost. Stimulus and ESG-linked financing (green bonds, concessional loans) can shift negotiating leverage back to suppliers.

- Delayed grants → compressed scopes

- Tight budgets → stronger buyer negotiation

- Regulatory mandates → inelastic demand

- ESG/stimulus → supplier leverage restoration

Aftermarket leverage varies by criticality

For critical assets buyers favor OEM parts and certified service, reducing bargaining power; for commoditized pumps and valves third-party parts expand options and strengthen buyers. Multi-year service contracts stabilize pricing but are typically rebid at term end, while digital diagnostics (2024 adoption up ~25% year-over-year in water utilities) enable premium service pricing and tighter OEM capture.

- OEM preference lowers buyer leverage on critical assets

- Third-party parts raise options for commoditized equipment

- Multi-year contracts stabilize revenue but are rebid

- Digital diagnostics justify service premiums (2024 +25% adoption)

US water spend $50B squeezes margins; diagnostics +25% boost OEM

Large public buyers concentrate demand—US municipal water capital ≈ $50B/yr (2024)—driving aggressive RFP scrutiny and narrow margins. Mission-critical uptime (downtime $100k–$1M/hr) and OEM service ties reduce price sensitivity, while commoditized pumps/third-party parts increase buyer leverage. Digital diagnostics adoption +25% (2024) raises OEM capture via premium services.

| Metric | 2024 Value |

|---|---|

| US municipal water capex | $50B/yr |

| Bipartisan Infrastructure Law water | $55B allocated |

| Diagnostics adoption YoY | +25% |

| Downtime cost | $100k–$1M/hr |

What You See Is What You Get

Xylem Porter's Five Forces Analysis

This preview shows the exact Xylem Porter's Five Forces Analysis you'll receive immediately after purchase—no surprises, no placeholders. The document displayed here is the same professionally written, fully formatted analysis file ready for download and use the moment you buy. You're looking at the actual deliverable and will get instant access to this exact file upon payment.

From Overview to Strategy Blueprint

Xylem's Porter's Five Forces snapshot highlights moderate buyer power, fragmented suppliers, high industry rivalry, low substitute threat, and entry barriers driven by scale and regulation. This concise view reveals the competitive pressures shaping Xylem's strategy and margins. The full report provides force-by-force ratings, visuals, and strategic implications to guide investment or corporate decisions—unlock the complete analysis with consultant-grade Excel/Word deliverables.

Suppliers Bargaining Power

Specialized components, limited sources

Many critical inputs—advanced sensors, motors, membranes and specialty alloys—are sourced from a narrow pool of qualified vendors, raising switching costs and long municipal/industrial qualification lead times; this concentration gives select suppliers pricing and allocation leverage. Xylem, with 2023 revenue of about 6.7 billion USD, mitigates exposure through dual sourcing and design-for-substitution where feasible.

Material and energy cost volatility

Steel (~$800/tonne HRC), copper (~$9,000/tonne) and NdPr rare-earths (~$80/kg) plus energy (Brent ~$88/bbl in 2024) swing with global cycles, driving input price volatility for Xylem’s pumps and treatment equipment. Suppliers often pass through surcharges in tight markets, raising short-term input costs. Index-linked contracts and hedging reduce but do not remove exposure. Xylem’s ability to reclaim costs depends on backlog strength and competitive intensity at bid time.

Global supply chain and logistics risk

Complex multi-region supply chains expose Xylem to freight spikes, geopolitical frictions and compliance constraints, with 2024 container rates still volatile after 2021–22 peaks. Critical electronics and semiconductors face allocation risk, pressuring smart-device production. Regionalization and nearshoring lower disruption risk but raise fixed costs and capex. Inventory buffers improve uptime for service-driven customers but tie up working capital against Xylem’s 2024 revenue of about $6.7 billion.

Digital/software vendor dependence

Digital and software vendor dependence for Xylem is high as IoT platforms, connectivity modules and cybersecurity stacks are commonly third-party; the global IoT platform market is projected to exceed $30 billion by 2028, increasing lock-in risks that can raise lifecycle costs and constrain roadmap flexibility.

- Open architectures/in-house firmware lower vendor dependency but require continuous R&D spend

- Vendor lock-in can elevate TCO and slow innovation

- Long-term vendor partnerships align on reliability and security

Supplier bargaining offset by Xylem scale

Xylem’s large installed base and >$6.3B revenue (FY2023) deliver purchasing scale and standardized platforms that provide counter-leverage in supplier negotiations. Long-term volume commitments and strategic sourcing secure capacity and improved terms, while supplier development programs reduce cost and raise quality over time. For bespoke components, supplier power can remain high and situational.

- Scale: >$6.3B revenue (FY2023)

- Leverage: standardized platforms

- Strategy: long-term volume commitments

- Mitigation: supplier development

- Risk: bespoke components = higher supplier power

Concentrated supplier base raises switching costs as commodity and energy swings amplify risk

Many critical inputs (sensors, motors, membranes, rare-earths) come from a narrow supplier pool, raising switching costs and allocation leverage. Xylem (revenue ~6.7B USD 2023) mitigates with dual sourcing, design-for-substitution and long-term contracts. Commodity swings (steel, copper, NdPr) and energy (Brent ~88 USD/bbl 2024) amplify supplier pass-through risk.

| Metric | Value |

|---|---|

| 2023 revenue | $6.7B |

| Brent (2024) | $88/bbl |

| NdPr (2024) | $80/kg |

| IoT platform market | >$30B by 2028 |

What is included in the product

Uncovers key drivers of competition, supplier and buyer power, threat of substitutes and new entrants tailored to Xylem’s water technologies; identifies disruptive forces and strategic vulnerabilities that affect pricing, margins and market share, delivering actionable insights for investor materials, strategy decks or academic analyses.

One-sheet Porter's Five Forces for Xylem that instantly highlights competitive pressures with an editable spider/radar chart—perfect for quick decisions and pitch decks. Customize pressure levels, swap in your data, and integrate into reports with no macros or finance expertise required.

Customers Bargaining Power

Concentrated municipal buyers, formal tenders

Utilities and public agencies predominantly buy via competitive RFPs, concentrating buying power—US municipal water capital spending was roughly $50 billion annually in 2024 (AWWA/EPA estimates), amplifying supplier price pressure. Transparent bidding increases total-cost scrutiny and narrows margins. Multi-year framework agreements frequently lock terms across cycles, while detailed technical specs and prequalification lists limit vendor substitution despite price-driven procurement.

High switching costs, installed-base lock-in

Integration with SCADA, piping and controls creates high switching friction for Xylem customers, reinforced by lifecycle service contracts, spare parts provisioning and warranties that deepen installed-base lock-in. Buyers, facing industry-estimated downtime costs commonly cited in the $100k–$1M per hour range for critical infrastructure, prioritize continuity and compliance, reducing price sensitivity for mission-critical assets.

Industrial buyers seek uptime and TCO

Process operators prioritize uptime, energy efficiency and reuse economics, with energy often representing a large share of plant OPEX (industry estimates up to 40%). Performance guarantees and service SLAs (commonly specifying >99% uptime) frequently sway procurement beyond list price. Retrofit compatibility and digital monitoring deliver measurable TCO gains through reduced downtime and energy use. Multi-sourcing policies, however, keep customer bargaining power at a moderate level.

Budget cycles and funding constraints

Public budgets and grant timing (eg US Bipartisan Infrastructure Law allocated 55 billion for water, wastewater and stormwater) can delay awards or compress project scopes; when funding tightens buyers negotiate harder and defer upgrades. Regulatory mandates that tighten effluent limits reduce price elasticity by forcing spending regardless of cost. Stimulus and ESG-linked financing (green bonds, concessional loans) can shift negotiating leverage back to suppliers.

- Delayed grants → compressed scopes

- Tight budgets → stronger buyer negotiation

- Regulatory mandates → inelastic demand

- ESG/stimulus → supplier leverage restoration

Aftermarket leverage varies by criticality

For critical assets buyers favor OEM parts and certified service, reducing bargaining power; for commoditized pumps and valves third-party parts expand options and strengthen buyers. Multi-year service contracts stabilize pricing but are typically rebid at term end, while digital diagnostics (2024 adoption up ~25% year-over-year in water utilities) enable premium service pricing and tighter OEM capture.

- OEM preference lowers buyer leverage on critical assets

- Third-party parts raise options for commoditized equipment

- Multi-year contracts stabilize revenue but are rebid

- Digital diagnostics justify service premiums (2024 +25% adoption)

US water spend $50B squeezes margins; diagnostics +25% boost OEM

Large public buyers concentrate demand—US municipal water capital ≈ $50B/yr (2024)—driving aggressive RFP scrutiny and narrow margins. Mission-critical uptime (downtime $100k–$1M/hr) and OEM service ties reduce price sensitivity, while commoditized pumps/third-party parts increase buyer leverage. Digital diagnostics adoption +25% (2024) raises OEM capture via premium services.

| Metric | 2024 Value |

|---|---|

| US municipal water capex | $50B/yr |

| Bipartisan Infrastructure Law water | $55B allocated |

| Diagnostics adoption YoY | +25% |

| Downtime cost | $100k–$1M/hr |

What You See Is What You Get

Xylem Porter's Five Forces Analysis

This preview shows the exact Xylem Porter's Five Forces Analysis you'll receive immediately after purchase—no surprises, no placeholders. The document displayed here is the same professionally written, fully formatted analysis file ready for download and use the moment you buy. You're looking at the actual deliverable and will get instant access to this exact file upon payment.

Original: $10.00

-65%$10.00

$3.50Description

From Overview to Strategy Blueprint

Xylem's Porter's Five Forces snapshot highlights moderate buyer power, fragmented suppliers, high industry rivalry, low substitute threat, and entry barriers driven by scale and regulation. This concise view reveals the competitive pressures shaping Xylem's strategy and margins. The full report provides force-by-force ratings, visuals, and strategic implications to guide investment or corporate decisions—unlock the complete analysis with consultant-grade Excel/Word deliverables.

Suppliers Bargaining Power

Specialized components, limited sources

Many critical inputs—advanced sensors, motors, membranes and specialty alloys—are sourced from a narrow pool of qualified vendors, raising switching costs and long municipal/industrial qualification lead times; this concentration gives select suppliers pricing and allocation leverage. Xylem, with 2023 revenue of about 6.7 billion USD, mitigates exposure through dual sourcing and design-for-substitution where feasible.

Material and energy cost volatility

Steel (~$800/tonne HRC), copper (~$9,000/tonne) and NdPr rare-earths (~$80/kg) plus energy (Brent ~$88/bbl in 2024) swing with global cycles, driving input price volatility for Xylem’s pumps and treatment equipment. Suppliers often pass through surcharges in tight markets, raising short-term input costs. Index-linked contracts and hedging reduce but do not remove exposure. Xylem’s ability to reclaim costs depends on backlog strength and competitive intensity at bid time.

Global supply chain and logistics risk

Complex multi-region supply chains expose Xylem to freight spikes, geopolitical frictions and compliance constraints, with 2024 container rates still volatile after 2021–22 peaks. Critical electronics and semiconductors face allocation risk, pressuring smart-device production. Regionalization and nearshoring lower disruption risk but raise fixed costs and capex. Inventory buffers improve uptime for service-driven customers but tie up working capital against Xylem’s 2024 revenue of about $6.7 billion.

Digital/software vendor dependence

Digital and software vendor dependence for Xylem is high as IoT platforms, connectivity modules and cybersecurity stacks are commonly third-party; the global IoT platform market is projected to exceed $30 billion by 2028, increasing lock-in risks that can raise lifecycle costs and constrain roadmap flexibility.

- Open architectures/in-house firmware lower vendor dependency but require continuous R&D spend

- Vendor lock-in can elevate TCO and slow innovation

- Long-term vendor partnerships align on reliability and security

Supplier bargaining offset by Xylem scale

Xylem’s large installed base and >$6.3B revenue (FY2023) deliver purchasing scale and standardized platforms that provide counter-leverage in supplier negotiations. Long-term volume commitments and strategic sourcing secure capacity and improved terms, while supplier development programs reduce cost and raise quality over time. For bespoke components, supplier power can remain high and situational.

- Scale: >$6.3B revenue (FY2023)

- Leverage: standardized platforms

- Strategy: long-term volume commitments

- Mitigation: supplier development

- Risk: bespoke components = higher supplier power

Concentrated supplier base raises switching costs as commodity and energy swings amplify risk

Many critical inputs (sensors, motors, membranes, rare-earths) come from a narrow supplier pool, raising switching costs and allocation leverage. Xylem (revenue ~6.7B USD 2023) mitigates with dual sourcing, design-for-substitution and long-term contracts. Commodity swings (steel, copper, NdPr) and energy (Brent ~88 USD/bbl 2024) amplify supplier pass-through risk.

| Metric | Value |

|---|---|

| 2023 revenue | $6.7B |

| Brent (2024) | $88/bbl |

| NdPr (2024) | $80/kg |

| IoT platform market | >$30B by 2028 |

What is included in the product

Uncovers key drivers of competition, supplier and buyer power, threat of substitutes and new entrants tailored to Xylem’s water technologies; identifies disruptive forces and strategic vulnerabilities that affect pricing, margins and market share, delivering actionable insights for investor materials, strategy decks or academic analyses.

One-sheet Porter's Five Forces for Xylem that instantly highlights competitive pressures with an editable spider/radar chart—perfect for quick decisions and pitch decks. Customize pressure levels, swap in your data, and integrate into reports with no macros or finance expertise required.

Customers Bargaining Power

Concentrated municipal buyers, formal tenders

Utilities and public agencies predominantly buy via competitive RFPs, concentrating buying power—US municipal water capital spending was roughly $50 billion annually in 2024 (AWWA/EPA estimates), amplifying supplier price pressure. Transparent bidding increases total-cost scrutiny and narrows margins. Multi-year framework agreements frequently lock terms across cycles, while detailed technical specs and prequalification lists limit vendor substitution despite price-driven procurement.

High switching costs, installed-base lock-in

Integration with SCADA, piping and controls creates high switching friction for Xylem customers, reinforced by lifecycle service contracts, spare parts provisioning and warranties that deepen installed-base lock-in. Buyers, facing industry-estimated downtime costs commonly cited in the $100k–$1M per hour range for critical infrastructure, prioritize continuity and compliance, reducing price sensitivity for mission-critical assets.

Industrial buyers seek uptime and TCO

Process operators prioritize uptime, energy efficiency and reuse economics, with energy often representing a large share of plant OPEX (industry estimates up to 40%). Performance guarantees and service SLAs (commonly specifying >99% uptime) frequently sway procurement beyond list price. Retrofit compatibility and digital monitoring deliver measurable TCO gains through reduced downtime and energy use. Multi-sourcing policies, however, keep customer bargaining power at a moderate level.

Budget cycles and funding constraints

Public budgets and grant timing (eg US Bipartisan Infrastructure Law allocated 55 billion for water, wastewater and stormwater) can delay awards or compress project scopes; when funding tightens buyers negotiate harder and defer upgrades. Regulatory mandates that tighten effluent limits reduce price elasticity by forcing spending regardless of cost. Stimulus and ESG-linked financing (green bonds, concessional loans) can shift negotiating leverage back to suppliers.

- Delayed grants → compressed scopes

- Tight budgets → stronger buyer negotiation

- Regulatory mandates → inelastic demand

- ESG/stimulus → supplier leverage restoration

Aftermarket leverage varies by criticality

For critical assets buyers favor OEM parts and certified service, reducing bargaining power; for commoditized pumps and valves third-party parts expand options and strengthen buyers. Multi-year service contracts stabilize pricing but are typically rebid at term end, while digital diagnostics (2024 adoption up ~25% year-over-year in water utilities) enable premium service pricing and tighter OEM capture.

- OEM preference lowers buyer leverage on critical assets

- Third-party parts raise options for commoditized equipment

- Multi-year contracts stabilize revenue but are rebid

- Digital diagnostics justify service premiums (2024 +25% adoption)

US water spend $50B squeezes margins; diagnostics +25% boost OEM

Large public buyers concentrate demand—US municipal water capital ≈ $50B/yr (2024)—driving aggressive RFP scrutiny and narrow margins. Mission-critical uptime (downtime $100k–$1M/hr) and OEM service ties reduce price sensitivity, while commoditized pumps/third-party parts increase buyer leverage. Digital diagnostics adoption +25% (2024) raises OEM capture via premium services.

| Metric | 2024 Value |

|---|---|

| US municipal water capex | $50B/yr |

| Bipartisan Infrastructure Law water | $55B allocated |

| Diagnostics adoption YoY | +25% |

| Downtime cost | $100k–$1M/hr |

What You See Is What You Get

Xylem Porter's Five Forces Analysis

This preview shows the exact Xylem Porter's Five Forces Analysis you'll receive immediately after purchase—no surprises, no placeholders. The document displayed here is the same professionally written, fully formatted analysis file ready for download and use the moment you buy. You're looking at the actual deliverable and will get instant access to this exact file upon payment.